Domestic Health Sector IPOs in Review: Sci-Tech Board Gains Momentum, Biopharma Firms Favor HKEX, US Listings Underwhelm

Hansoh Pharma

Pharmaceutical Research, Production, and Sales

CHISON

Medical Ultrasound Imaging Equipment Developer

Hengrui Pharma

Innovative and High-Quality Pharmaceutical Developer

Pharmaron

Life Science R&D Service Provider

Henlius

Innovative Biopharmaceutical Company

At the beginning of 2019, many people lamented that “winter is coming,” viewing 2019 as the worst economic year in the past decade, yet also the best in the next ten years. Even the healthcare industry, long a favorite in investment markets, was not immune to this sentiment, with companies increasingly struggling to secure financing. However, the situation in the secondary markets was relatively better; driven by signals from global central banks, stock markets around the world performed well in the first half of 2019. Now that 2019 has passed, what was the final outcome? VCBeat has compiled a review of initial public offerings (IPOs) in China’s healthcare sector in 2019.

Rebound After Initial Suppression: IPO Conditions Significantly Improved in 2019

The number of corporate initial public offerings (IPOs) serves, to some extent, as an indicator of the vitality of the financing market. A higher volume of IPOs reflects investors’ optimism about market prospects and constitutes a key metric for the stock market.

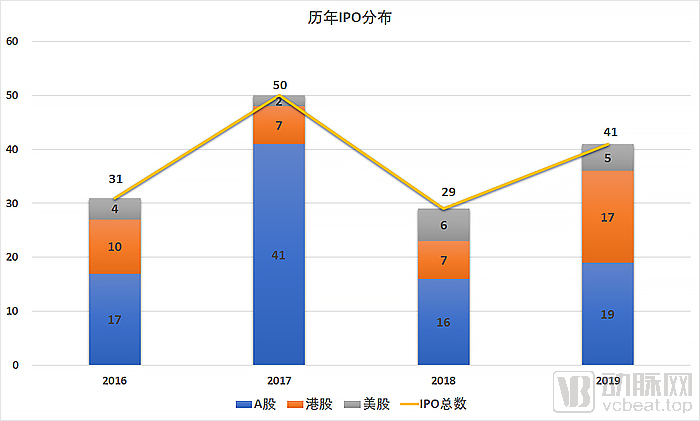

According to data compiled by VCBeat from the Choice Financial Terminal, a total of 40 domestic health and wellness companies completed 41 IPOs in 2019 (from January 1, 2019, to December 31, 2019), with Pharmaron listing on both the A-share and H-share markets. The number of IPOs increased by 41.4% compared to 2018, demonstrating the vitality of the secondary market.

Among them, there were 19 A-share IPOs; Hong Kong stock IPOs followed closely with 17; additionally, five IPOs took place in the United States across the ocean.

Compared with 2018, the number of initial public offerings (IPOs) in 2019 saw a significant increase. In 2018, there were a total of 29 IPOs among big health companies. Of these, 16 companies listed on the Hong Kong Stock Exchange, accounting for more than half of the total; the numbers of companies choosing to list in the domestic Chinese market and on the US stock market were comparable, with 7 and 6 companies respectively.

2017 was undoubtedly a peak year for corporate IPOs, with a total of 50 initial public offerings throughout the year. Among these, 41 companies chose to list domestically, accounting for the vast majority; 7 companies opted for listings on the Hong Kong Stock Exchange, while another 2 listed on U.S. stock exchanges.

In 2016, there were a total of 31 IPOs throughout the year. Among them, 17 companies listed in China, 10 on the Hong Kong stock market, and 4 on the US stock market.

Among the companies that went public in 2019, the vast majority chose to list in the second half of the year. Only 13 companies opted to list before June 30, 2019, accounting for less than one-third of the total. Consequently, the dismal performance in the first half of the year led most analysts to hold a highly pessimistic outlook on the market situation for 2019.

However, the situation in the second half of the year saw a gratifying reversal. Judging from the final results, the 2019 data was quite respectable; although the 42 companies involved did not match the 50 enterprises recorded in 2017, they were far ahead of the dismal figures from 2018. It would be no exaggeration to describe this as a significant rebound.

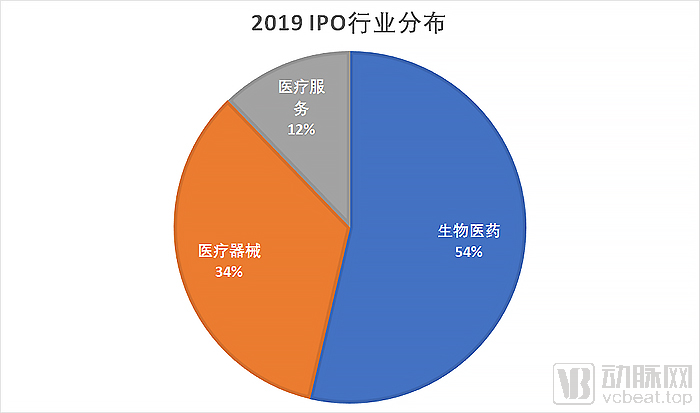

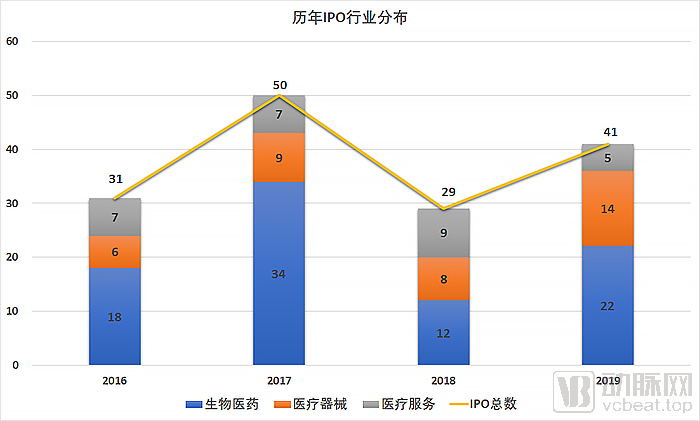

From the perspective of IPO company classifications, in 2019, there were a total of 41 IPOs. Biopharmaceutical companies accounted for more than half, with 22 IPOs (8 on the A-share market, 12 on the Hong Kong stock market, and 2 on the US stock market; since Pharmaron listed on both the A-share and Hong Kong markets, it was counted as two IPOs). There were 14 IPOs in the medical devices sector, with the A-share market accounting for the vast majority at 11 instances, while the Hong Kong stock market saw 3 medical device IPOs. The healthcare services sector had 5 IPOs, including 2 on the Hong Kong stock market and 3 on the US stock market.

In contrast, the classification of companies that went public in 2018 was more balanced, whereas those in 2017 and 2016 were predominantly biopharmaceutical firms.

In terms of industry classification for IPO companies, biopharmaceuticals have remained the dominant sector in recent years. However, their share of annual IPOs has been gradually declining. As China pursues the goal of import substitution for medical devices, the proportion of medical device companies going public has increased year by year. In 2019, IPOs of medical device companies accounted for one-third of the total.

A-Shares: The STAR Market Brings Tremendous Vitality

Compared to the sluggish performance in 2018, A-shares showed a significant improvement in 2019. The IPO ratio rebounded from 24% in 2018 to 46.3% in 2019. This surge was undoubtedly driven largely by the establishment of the STAR Market. Statistics show that health care companies accounted for the vast majority of IPOs on the STAR Market, with a proportion as high as 78.9%.

From the announcement of the establishment of the STAR Market at the opening ceremony of the first China International Import Expo on November 5, 2018, to its official launch on July 22, 2019, the STAR Market took only eight months, creating a miracle in the capital market.

China’s establishment of the STAR Market on the Shanghai Stock Exchange aims to adhere to the orientation toward the global scientific and technological frontier, the main battlefield of economic development, and major national needs, primarily serving technology-driven innovation enterprises that align with national strategies, achieve breakthroughs in key core technologies, and enjoy high market recognition.

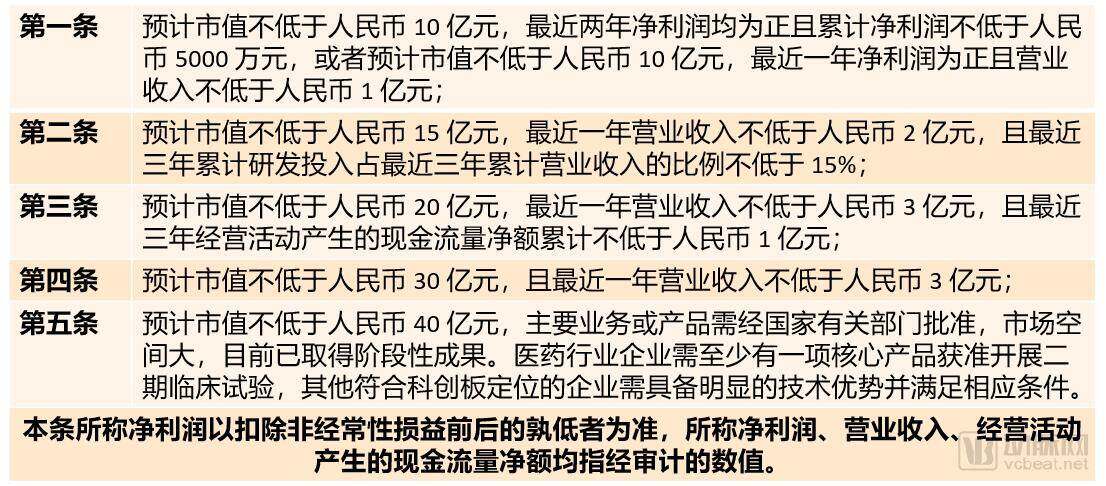

Therefore, the establishment of the STAR Market requires prioritizing support for technological innovation enterprises in seven major fields—namely, next-generation information technology, high-end equipment, new materials, new energy, energy conservation and environmental protection, and biomedicine—which constitute high-tech industries and strategic emerging industries, and five listing standards have been established.

These five listing standards are centered on company market capitalization, combining it with corporate financial metrics such as revenue, cash flow, profitability, and R&D investment to form a set of inclusive listing requirements. For an issuer applying for listing on the STAR Market, it is sufficient to meet just one of the five standards in terms of market capitalization and financial indicators, provided this is clearly stated in the prospectus and the sponsor’s listing recommendation letter.

Among these, the fifth set of standards is of greatest concern to the public. Profitability is no longer a barrier to a company’s initial public offering (IPO); as long as the market capitalization exceeds RMB 4 billion, there are no requirements for profitability. This follows the principle that “the higher the market capitalization, the lower the profitability requirement.” However, additional requirements regarding research and development progress have been imposed on pharmaceutical companies, which must have at least one core product approved to enter Phase II clinical trials.

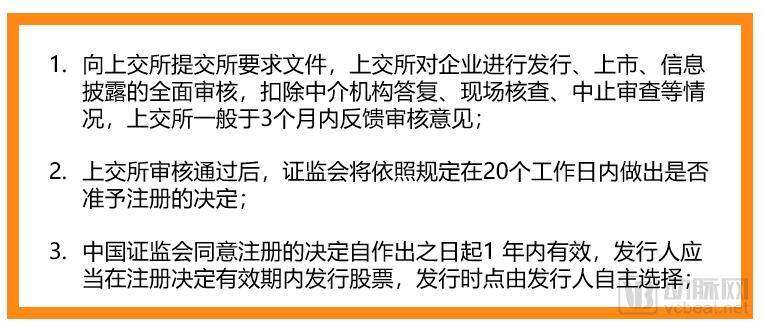

Meanwhile, the STAR Market piloted the registration-based IPO system. Under this review framework, it typically takes 6 to 9 months for a company to complete the entire process from submitting its initial public offering (IPO) application to final review and registration. The key steps are as follows:

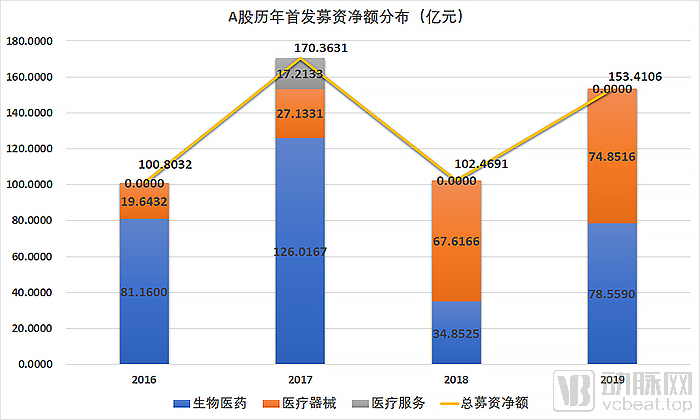

In 2019, the net proceeds raised by big health companies listed on China’s A-share market reached RMB 15.34106 billion, representing a significant year-on-year increase of 49.7%. This figure was second only to the RMB 17.03631 billion raised in 2017. In 2018, 2017, and 2016, the net proceeds from A-share IPOs amounted to RMB 10.24691 billion, RMB 17.03631 billion, and RMB 10.08032 billion, respectively. Evidently, the STAR Market has demonstrated strong fundraising capabilities, at least at the current stage.

According to statistics, the average net proceeds raised by companies conducting initial public offerings (IPOs) on China’s A-share market amounted to RMB 807 million. However, there was significant variation in net proceeds among individual companies, with only seven firms exceeding the average. These seven companies raised a combined net total of RMB 9.516 billion, accounting for as much as 62% of the overall amount.

Among these seven companies, three are medical device firms and four are biopharmaceutical enterprises. Notably, Bloomage Biotech (688363.SH) raised a net amount of RMB 2.249 billion in its initial public offering (IPO), making it the healthcare company with the highest net IPO proceeds.

Medical device companies emerged as the main force in A-share IPOs in 2019, with a total of 11 companies listing, while the remaining eight were all biopharmaceutical firms. However, in terms of total funds raised, biopharmaceutical companies demonstrated stronger fundraising capabilities. The net proceeds from the eight biopharmaceutical firms amounted to RMB 7.856 billion, accounting for 54.6% of the total, which was higher than that raised by the 11 medical device companies.

Judging by the stock price trends, the share prices of the vast majority of enterprises rose rapidly after their initial public offerings (IPOs). With only one company’s stock falling below its issue price, the remaining 18 companies experienced varying degrees of price increases. The average gain was 109.15% five days post-listing and reached 118.52% thirty days post-listing. As of February 7, 2020, the closing prices of all 19 companies were significantly higher than their initial offering prices, with most companies seeing their stock prices multiply several times over.

Pharmaron (300759.SZ), although listed on the ChiNext board with fundraising proceeds below the average, set a record for the largest 30-day gain at 435%. In other words, its closing price on the 30th day was more than five times its initial public offering (IPO) price. As of February 7, 2020, its total market capitalization stood at RMB 43.278 billion, making it the healthcare company with the highest market value among domestic IPOs in China in 2019. Meanwhile, Pharmaron also conducted an IPO on the Hong Kong Stock Exchange, delivering impressive performance.

Chipscreen Biosciences (688321.SH) ranked second in terms of 30-day price increase with a surge of 226.82%, making it the STAR Market healthcare company with the highest 30-day gain. Its market capitalization reached RMB 26.326 billion (as of February 7, 2020), ranking third. In second place was Bloomage Biotechnology, which raised the largest net proceeds, with a market capitalization of RMB 39.25 billion.

Based on the latest average return on equity (ROE), these A-share IPO companies have demonstrated strong profitability, with an average of 12.64%. Ten companies met this benchmark, indicating a relatively even distribution.

CHISON (688358.SH) leads the rankings with an average return on equity (ROE) of 29.34%, while BaiRen Medical and Bloomage Biotech rank second and third with 21.64% and 21.59%, respectively.

The medical device sector ranks second among the thematic industries on the STAR Market, trailing only the next-generation information technology industry. Medical enterprises account for 24% of the number of IPOs and 19% of the total funds raised on the STAR Market.

The STAR Market has introduced innovations in listing criteria, the registration-based IPO system, issuance pricing, trading rules, and delisting mechanisms, truly handing over selection power to the market. Meanwhile, stringent IPO supervision has become the norm, and oversight of delistings has been intensified. The trend toward a more market-oriented and normalized delisting process in the A-share market is clear, and capital market reforms will continue to deepen.

As of December 16, 2019, the number of STAR Market companies in the queue at the Shanghai Stock Exchange had reached 161. The approval rate for new stock issuances climbed to 88%, representing a 30 percentage point increase compared to 2018. However, following the initiation of on-site inspections in the second half of the year, the number of terminated reviews for new stock listings also showed a significant upward trend, surging by 170% year-on-year compared to the first half.

As the value of the STAR Market is further unlocked, and with the sustained high level of attention on the broader health sector driven by the pandemic, we anticipate that the STAR Market will remain active in 2020, becoming a key channel for initial public offerings (IPOs) by healthcare companies.

Hong Kong Stocks: The Golden Channel for Biopharmaceuticals

Prior to 2018, there were few healthcare companies listed on the Hong Kong Stock Exchange (HKEX), with the majority concentrated in medical service sectors such as private healthcare and medical aesthetics. As biopharmaceuticals constitute the mainstay of initial public offerings (IPOs) in the healthcare industry, this resulted in a limited number of low-quality healthcare IPOs on the HKEX before 2018.

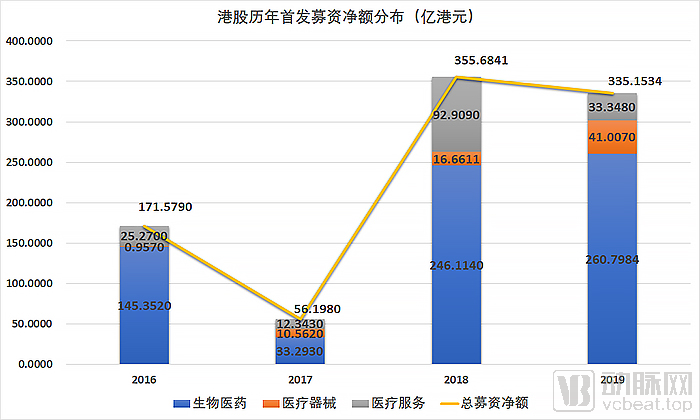

In 2017, seven healthcare companies chose to list on the Hong Kong stock market, including four healthcare service providers and two medical device manufacturers. The net proceeds from their initial public offerings (IPOs) amounted to only HK$5.62 billion. In 2016, ten healthcare companies went public on the Hong Kong Stock Exchange, six of which were healthcare service providers, with total net IPO proceeds reaching HK$17.158 billion. However, China Resources Pharmaceutical Group Limited (03320.HK) alone accounted for HK$13.672 billion of the net proceeds.

After June 2017, the Hong Kong Stock Exchange officially decided to broaden its existing listing regime, allowing biotechnology companies that are not yet profitable, as well as emerging and innovative industry companies with weighted voting rights structures, to list on the Main Board, subject to additional disclosures and safeguard measures.

In February 2018, the Hong Kong Stock Exchange (HKEX) released a consultation paper on the “Listing Regime for Emerging and Innovative Companies,” proposing amendments to the “Listing Rules.” In March of the same year, the Stock Exchange of Hong Kong (SEHK) also held the inaugural “Hong Kong BioTech Summit” to build momentum for attracting biotechnology companies to list.

Traditional enterprises have been slow to transform, while fully innovative companies have been unable to pursue domestic listings. This has long been a major dilemma for Chinese biopharmaceutical enterprises, with only a few leading firms able to seek listings on NASDAQ. The opening of the Hong Kong market is akin to having a “NASDAQ” right at the doorstep of domestic innovative biopharmaceutical entrepreneurs.

On August 1, 2018, Ascletis Pharma became the first pre-profit biopharmaceutical company to list on the Hong Kong Stock Exchange. In 2018, a total of seven biopharmaceutical companies conducted initial public offerings (IPOs) on the Hong Kong Stock Exchange, accounting for nearly half of all healthcare sector IPOs that year. These seven companies raised a combined net proceeds of HK$24.611 billion, representing the majority of the total net proceeds of HK$35.568 billion raised by healthcare companies in that year.

In 2019, innovative biopharmaceutical companies flocked to launch initial public offerings (IPOs) on the Hong Kong Stock Exchange. Among the healthcare companies that went public on the Hong Kong Stock Exchange in 2019, apart from three medical device companies and two healthcare service providers, the remaining twelve were all biopharmaceutical companies, accounting for an absolute majority.

These 17 companies raised a total net proceeds of HK$33.515 billion, of which HK$26.08 billion was attributed to biopharmaceutical enterprises, accounting for a significant 77.8%. The top three in terms of net proceeds were all secured by biopharmaceutical companies: Hansoh Pharma (03692.HK) with HK$7.64 billion, Pharmaron (03759.HK) with HK$4.344 billion, and Henlius-B (02696.HK) with HK$3.096 billion.

However, judging by stock price trends, the performance of these companies has been mixed. Within five days of listing, four companies saw their stock prices fall below the initial public offering (IPO) price; within 30 days, the number of companies trading below their IPO price rose to six. Among the 11 companies whose stock prices remained above the issue price, the average 30-day gain was only 29.8%, a somewhat disappointing performance.

As of February 7, 2020, the closing prices of seven companies fell below their initial public offering (IPO) prices on that day, accounting for nearly half.

As of February 7, 2020, the combined market capitalization of these 17 companies reached HK$282.025 billion. Among them, Hansoh Pharma’s market cap had already hit HK$158.029 billion, making it a corporate giant. Interestingly, Zhong Huijuan, founder and chairwoman of Hansoh Pharma, is married to Sun Piaoyang, the actual controller and chairman of Hengrui Pharma (600276.SH), which ranks among the top by market capitalization in the A-share pharmaceutical sector. This means the total market value of listed companies controlled by their family has exceeded RMB 500 billion.

Based on the latest average return on equity (ROE), excluding five companies with negative ROE, the average ROE of the remaining 12 companies stands at 113.96%. However, in reality, only China Antibody-B (03681.HK) and TopAlliance Biosciences-B (01875.HK) surpassed this average, with respective figures of 710.18% and 500.25%. Ascent Pharmaceuticals-B (06855.HK), ranking third, recorded an ROE of only 48.07%, also falling short of the average.

The Hong Kong Stock Exchange’s relaxed listing requirements for biopharmaceutical companies have made Hong Kong-listed shares one of the top choices for IPOs in the sector, establishing it as the premier IPO channel for biopharmaceutical enterprises.

However, valuation discrepancies exist between the Hong Kong stock market and the A-share market. This has directly led to a surge in share prices on the STAR Market, while Hong Kong-listed stocks have consecutively fallen below their IPO prices. With the launch of the STAR Market, biopharmaceutical companies now have an additional IPO channel, which may prompt some of them to pursue listings on the STAR Market in the future.

Meanwhile, the ongoing illegal protests and demonstrations since late 2019 may also heighten concerns among businesses and investors, leading them to forgo Hong Kong stocks in favor of raising capital in other financial markets.

US Stocks: Chinese Health and Wellness Companies Out of Favor, Peaking at IPO

Given the United States’ overwhelming global lead in biopharmaceuticals and medical devices, few Chinese companies in these two sectors choose to list in the U.S., with only a rare handful possessing truly proprietary technologies doing so.

In 2016 and 2017, several innovative biopharmaceutical companies still chose to list on the U.S. stock market. With the Hong Kong Stock Exchange lowering its listing thresholds for biopharmaceutical companies and the establishment of the STAR Market, innovative biopharmaceutical enterprises now have more IPO channels.

On the contrary, traditional Chinese medicine (TCM)-related stocks have drawn attention in the U.S. market. In 2019, two pharmaceutical companies that chose to go public via IPOs on U.S. exchanges—Su Xuan Tang (SXTC.O) and Happy Life (HAPP.O)—both specialized primarily in TCM.

Relatively speaking, healthcare service companies with innovative business models are more inclined to list on U.S. stock exchanges. For instance, So-Young and Pengai Medical were standouts among innovative big health enterprises in 2019, while Yiheng Health is a cross-border e-commerce platform specializing in big health products. This further confirms that, compared with advanced countries, innovation in China’s medical sector remains largely confined to business model innovation.

The state has long recognized this limitation and has vigorously promoted the enhancement of core capabilities in the healthcare sector in recent years. Based on the aforementioned analysis of A-shares and Hong Kong-listed stocks, it is evident that the pharmaceutical biotechnology and medical device industries have already achieved certain improvements under the impetus of this policy.

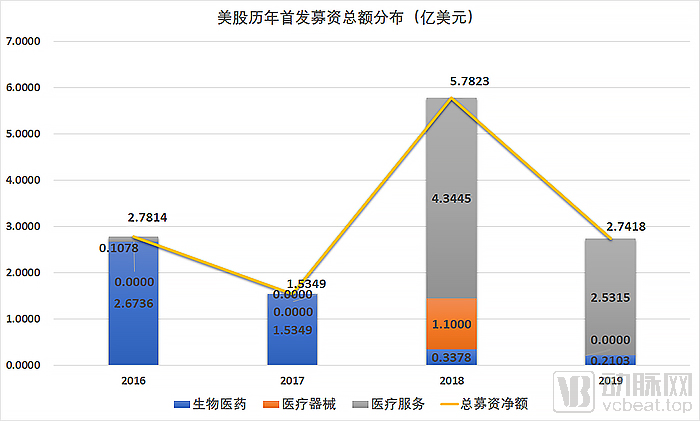

The total net proceeds from the initial public offerings (IPOs) of these six companies amounted to $364 million, marking a significant decline from the $534 million raised in 2018. However, this performance remains quite strong compared to the $183 million raised in 2017 and the $249 million raised in 2016. Notably, So-Young alone accounted for nearly half of the total net IPO proceeds, raising $179 million.

In terms of stock price performance, these companies have not fared well on the Nasdaq. Only two of them had closing prices higher than their IPO prices after five days, while the other four all fell below their IPO prices. By the 30-day closing price, the decline in stock prices continued to widen. Even for the two companies that remained above their IPO prices, the data was not very promising—one company’s stock price had already dropped to match its IPO price, and the other saw its gain drop from 93.75% at five days to just 31.25%.

As of the market close on February 7, 2020, all six companies had fallen below their initial public offering (IPO) prices. So-Young was the best-performing healthcare company among them, with a closing price of $13.34 on that day, only slightly down from its IPO price of $13.80. The other five companies experienced significant declines in their stock prices.

In terms of average return on equity (ROE), although only two companies reported negative values, the performance of the remaining companies was also lackluster, with the highest ROE reaching merely 21.39%.

Overall, U.S. stocks are more favored by Chinese internet and technology companies. Even for these enterprises with glamorous titles, most experience their peak performance at the time of listing, with share prices quickly falling below the IPO price and continuing to decline. For the broader healthcare sector, the U.S. stock market is not as attractive as it appears.

In addition to the continuous decline in stock prices, domestic political uncertainty in the United States and the intensification of Sino-US trade frictions have made Chinese companies more hesitant when choosing to pursue an IPO in the US stock market.

Given the United States’ overwhelming leadership in the pharmaceutical and medical device industries, U.S. stock investors naturally prefer to invest in biopharmaceuticals and medical devices, which constitute the core of the healthcare sector. In contrast, the majority of large-health companies among Chinese concept stocks lack distinctive technological advantages, significantly diminishing their investment value.

Finally, the establishment of the STAR Market has provided a more favorable venue for companies’ initial public offerings (IPOs), along with higher valuations.

Therefore, barring any significant changes, the number of healthcare companies opting for U.S. IPOs is likely to remain low in the future.

Final Remarks

Based on our review of initial public offerings (IPOs) by healthcare companies in 2019, the IPO market showed signs of recovery compared to 2018. In particular, the establishment of the STAR Market emerged as a significant highlight, providing a more favorable financing channel for medical enterprises with innovative technologies that had not yet achieved profitability.

Due to the impact of the epidemic at the beginning of the year, the public will pay more attention to the medical field in the future, and some emerging medical models will be favored by the capital market. Therefore, even if a capital winter comes, the overall health sector is expected to be relatively less affected.

Driven by strong national policy support, initial public offerings (IPOs) in the medical device and biopharmaceutical sectors—previously characterized by large scale but limited competitiveness—have shown significant improvement compared to the past. This development is beneficial for enhancing the core capabilities of China’s healthcare industry.

Currently, a clear trend has emerged: medical device companies are listing on the STAR Market, while biopharmaceutical firms are turning to the Hong Kong stock exchange. However, as the STAR Market continues to gain strength and various factors impact the Hong Kong market, whether the STAR Market will replace Hong Kong as the preferred IPO destination for biopharmaceutical companies remains a topic worth watching.

Capital Bond: Mid-Year Review of 2019 Chinese ADR IPOs: How Are the Luckin Coffees That Listed in the U.S. Amid Controversy Faring?

Financial Circle: A Review of the 2019 IPO Landscape for Pharmaceutical and Biotech Companies: Which Is Superior, the STAR Market or the Hong Kong Stock Exchange?

EY: A-share IPOs Up 90% Year-on-Year

Zhitong Finance: 2019 Pharmaceutical Stocks: Happy Yet Painful