China Rare Disease Industry Report: Policy Reforms, Market Access, and Future Outlook

Pfizer

Pharmaceutical R&D Developer

AstraZeneca

Biopharmaceutical Manufacturer

Since 2015, the Chinese government has issued a series of policies and regulations to deepen reforms in the pharmaceutical industry, covering clinical trial data verification, consistency evaluation, review and approval reforms, priority review and approval, the CFDA’s (now NMPA) accession to the ICH, adjustments to and negotiations for the National Reimbursement Drug List, and the pilot “4+7” volume-based procurement program along with its nationwide expansion. These reform measures have been closely interconnected and implemented with unprecedented intensity, dispelling the darkest clouds over the pharmaceutical sector. As a result, there has been a surge in clinical development and marketing applications for innovative drugs since 2015, including in the long-neglected field of rare disease treatments.

Although rare diseases lack a clear definition, they are not actually rare in China, given its large population. Due to the convergence of various real-world factors—including pharmaceutical R&D, patient populations, and insurance coverage—most patients with rare diseases either have no access to effective medications or cannot afford the cost of treatment, placing a heavy economic and psychological burden on their families.

To address the practical medication needs of patients with rare diseases, China has repeatedly highlighted the field of orphan drugs in various healthcare reform documents. Measures include accelerating the market approval of new drugs for rare diseases, lowering regulatory barriers for research and development and clinical trials through policy support, facilitating the inclusion of orphan drugs in the national medical insurance catalog, simplifying market access procedures, and significantly reducing patients’ financial burden through the availability of generic orphan drugs. Through these concerted efforts, the aim is to effectively implement solutions and resolve the most pressing medication concerns for patients with rare diseases.

To help readers understand and study the rare disease market, VCBeat’s VBInsight and Aimeda jointly authored and released the “China Rare Disease Industry Report.” This article excerpts selected content from the report, aiming to present readers with the opportunities and challenges in the rare disease field both domestically and internationally.

According to statistics, since 2013, more than ten policy documents issued by relevant authorities have all focused on accelerating the review and approval of rare disease drugs. In 2015, the State Council issued the “Opinions on Reforming the Drug and Medical Device Review and Approval System,” aiming to expedite the review and approval of innovative drugs for the prevention and treatment of HIV/AIDS, malignant tumors, major infectious diseases, and rare diseases. The first batch of the Priority Review and Approval List was officially released at the end of 2015, followed by 34 subsequent batches; by the end of 2018, regular updates to the priority review and approval process had become institutionalized. Meanwhile, overseas rare disease drugs urgently needed for clinical use benefited from accelerated review and approval; the “implicit approval” system for clinical trials was formally implemented, making new drug marketing applications the “centerpiece” of priority review and approval; furthermore, the combination of “time-limited priority” and “conditional approval” facilitated the entry of globally marketed novel rare disease drugs into the Chinese market.

Among the rare disease products included in the priority review and approval program, there were a total of 87 application numbers. Of these, 53 had completed certificate issuance or had already received approval documents.

By comparing the average time interval between the CDE acceptance date and the priority review and approval announcement date with the average time interval from the priority review and approval announcement date to the completion of certificate issuance or the status change to “approval letter issued,” it can be seen that priority review and approval has, to some extent, accelerated the clinical approval process for rare disease drugs.

However, a detailed examination of the acceptance numbers for each rare disease drug reveals that applications with a longer interval between the acceptance date and the public announcement date for priority review and approval (a difference of more than 500 days) were reviewed and approved relatively quickly after being included in the priority review and approval program. In contrast, applications with a shorter interval between the acceptance date and the public announcement date (a difference within 200 days) still faced an average of more than 300 days to complete the review and approval process after the announcement date. Of course, the reasons for the prolonged review and approval timeline are multifaceted, such as complex communication processes.

Although priority review and approval allow applications for drugs targeting rare diseases and those with high clinical value to stand out from the vast number of drug applications, they still face queuing within the priority review pipeline and prolonged review timelines due to various factors. In this context, the accelerated approval of urgently needed overseas new drugs for clinical use, coupled with the gradual implementation of the “implicit approval” system for clinical trials, has served as a significant “accelerator” for the rapid market launch of all related products.

Accelerated Approval of Overseas New Drugs in Urgent Clinical Need

On October 23, 2018, the National Medical Products Administration (NMPA) and the National Health Commission jointly issued the “Procedures for the Review and Approval of Overseas New Drugs in Urgent Clinical Need.” Under these procedures, the Center for Drug Evaluation (CDE) established a dedicated channel to conduct reviews: technical review for drugs treating rare diseases is to be completed within three months of acceptance, while technical review for other overseas new drugs is to be completed within six months of acceptance. The aforementioned timelines exclude the time taken by applicants to submit supplementary materials.

On November 1, 2018, the Center for Drug Evaluation of the National Medical Products Administration issued the “Notice on Publishing the First Batch of Overseas New Drugs Urgently Needed for Clinical Use,” announcing a list of 40 products. On March 28, 2019, the Center for Drug Evaluation of the National Medical Products Administration released a public notice regarding the second batch of overseas new drugs urgently needed for clinical use, listing 30 selected overseas-marketed products.

First/Second Batch of Overseas New Drugs Urgently Needed for Clinical Use Listed in China

“After the ‘Tacit Approval System,’ What Is the Future of Priority Review?”

Prior to the implementation of the “implied approval” system for clinical trials, priority review and approval helped alleviate, to some extent, the excessively long queues for rare disease drug clinical trial applications and marketing authorization submissions. Following the formal adoption of the “implied approval” system, priority review and approval has focused on reducing prolonged waiting times for new drug marketing applications, thereby also benefiting rare disease drug submissions.

On November 5, 2018, the Center for Drug Evaluation (CDE) announced the first batch of eight application numbers granted implicit approval for clinical trials. Industry experts believe this marks the implementation of the “implicit approval” system for the review and approval of drug clinical trials, which will accelerate the new drug development process for pharmaceutical companies, speed up the market launch of new drugs, and facilitate the forward development of innovative pharmaceutical enterprises.

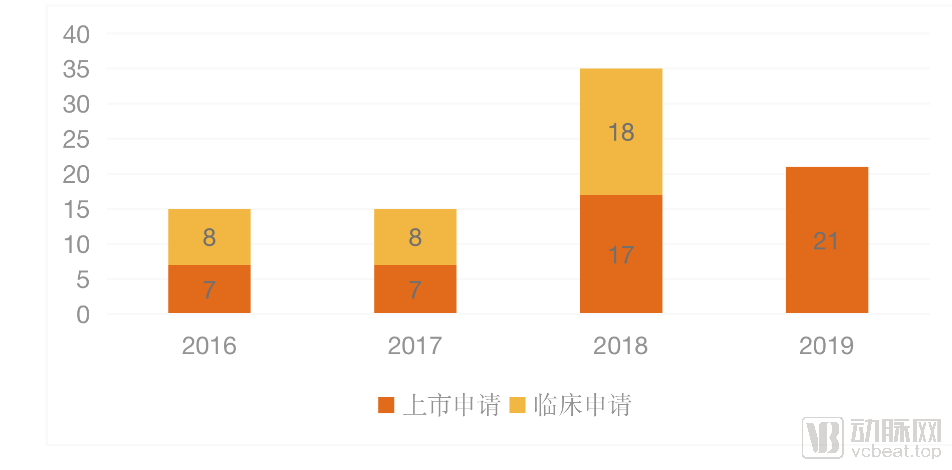

In 2018, a total of 35 application numbers were included in the priority review and approval process, including 17 marketing applications and 18 clinical trial applications; as of October 30, 2019, a total of 21 rare disease drug application numbers had been included in the priority review and approval process.

Public Notice on the Priority Review and Approval of Orphan Drugs by the CDE (2016–October 30, 2019)

Globally, more than 7,000 rare diseases have been diagnosed, yet fewer than 10% have approved therapeutic drugs or regimens. Clinical research represents a major bottleneck in the development of medicines for rare diseases (orphan drugs). In the field of orphan drug development, the United States has long maintained a dominant position, whereas China is just getting started.

For a long time, due to factors such as the inadequate regulatory framework for orphan drugs in China, the lack of industrial policies, and high research and development (R&D) costs, the returns on orphan drug development have been difficult to predict. Consequently, domestic companies have shown little interest in researching or developing drugs for rare diseases. Although China’s support policies for R&D of rare disease treatments have improved significantly, detailed implementation rules still need to be gradually established and enforced.

In 2018, the Chinese government introduced various policies to support the entry of foreign rare disease drugs into the Chinese market, resulting in a significant increase in the number of overseas pharmaceutical products approved for marketing in China, with 10 drugs approved in 2018 alone. According to the two batches of lists of urgently needed overseas new drugs for clinical use released by the Center for Drug Evaluation of the National Medical Products Administration, a total of 66 varieties were involved, among which more than 50% were rare disease drugs, totaling 37.

For drugs included in the List of Overseas New Drugs in Urgent Clinical Need, relevant materials may be submitted in accordance with the "Review and Approval Procedures for Overseas New Drugs in Urgent Clinical Need" to directly apply for marketing authorization. The Center for Drug Evaluation (CDE) has established a dedicated channel to expedite the review process, completing the technical review for rare disease treatments within three months of acceptance. As of November 8, 2019, six drugs from this list had been successively approved for marketing, thereby bypassing the need for domestic clinical trials and significantly shortening the time required for overseas rare disease drugs to reach the Chinese market.

Rare Disease Drugs Already Approved for Marketing in the List of Clinically Urgent New Drugs Already Marketed Abroad (I, II)

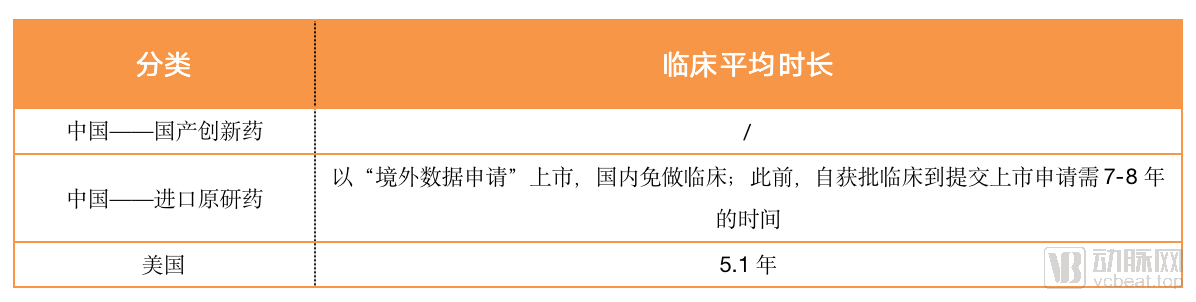

For the foreseeable future, orphan drugs in China will continue to be predominantly imported. On one hand, international pharmaceutical companies can launch their products by submitting overseas clinical data, thereby bypassing the need for domestic clinical trials and significantly accelerating the market entry of foreign orphan drugs in China. On the other hand, Chinese enterprises benefit from multiple favorable policies in the clinical development of orphan drugs, which help alleviate their operational burdens. For instance, in December 2017, the former China Food and Drug Administration (CFDA) issued the "Opinions on Encouraging Drug Innovation and Implementing Priority Review and Approval" (No. 126 [2017] of the CFDA). This document further revised and clarified that priority review and approval would be granted to registration applications for drugs treating rare diseases, and allowed applicants to request a reduction in the number of clinical trial cases or even an exemption from conducting clinical trials at the time of submitting their clinical trial applications.

Comparison of Clinical Trial Durations Between China and the United States

Overall, China is still in a transitional phase of innovation, characterized by relatively weak foundational research and insufficient translational capacity. Clinical research resources remain inadequate, with clinical research capabilities and data quality requiring improvement. There are few institutions conducting clinical trials for rare disease drugs, and they lack experience. Shortcomings such as the absence of detailed technical guidelines for rare disease drug development still need to be gradually addressed.

Inclusion in the National Reimbursement Drug List (NRDL) is a critical pathway for new drugs in China to achieve rapid market penetration and volume growth. For all pharmaceutical products, securing NRDL inclusion represents half the battle in successful product promotion, and this holds true for orphan drugs as well. To facilitate the inclusion of more new orphan drugs in the NRDL, the National Healthcare Security Administration dynamically adjusts the list’s composition through two mechanisms: routine annual adjustments and negotiated access for drug reimbursement.

On the morning of October 19, 2019, Li Tao, a member of the Party Leadership Group and Deputy Director of the National Healthcare Security Administration (NHSA), stated at the 2019 China Rare Disease Conference that the NHSA had initiated the adjustment of the National Reimbursement Drug List in 2019. The results of the routine access phase were announced on August 20, with 148 drugs added and 150 removed from the list, while 128 drugs were selected for price negotiations. The adjustment strategy focused on addressing shortcomings, optimizing the structure, and encouraging innovation. Special attention was given to medications for rare diseases; during the review process, input was solicited from rare disease patients, experts, and local healthcare security administrations.

。

According to statistics, among the 60 drugs approved for marketing in China that can treat rare diseases (counted by generic names, with approved indications clearly specifying the treatment of a particular rare disease), 45 (counted by generic names) have been included in the National Reimbursement Drug List, covering 26 rare diseases. Among these, six drugs newly added to the list in 2019 are indicated for conditions such as primary carnitine deficiency and early-onset Parkinson’s disease. Seven drugs newly incorporated into Category B of the list through negotiations in 2019 are indicated for conditions such as pulmonary arterial hypertension and Niemann-Pick disease type C. The rare disease drug whose negotiation for renewal failed in 2019 was recombinant human interferon β-1b.

For rare disease drugs included in the Class B reimbursement list through national medical insurance negotiations and routine catalog adjustments, price reductions vary, ranging from 10% to 70%. Although inclusion in the medical insurance catalog is the most critical step for market access, it does not necessarily lead to a surge in sales.

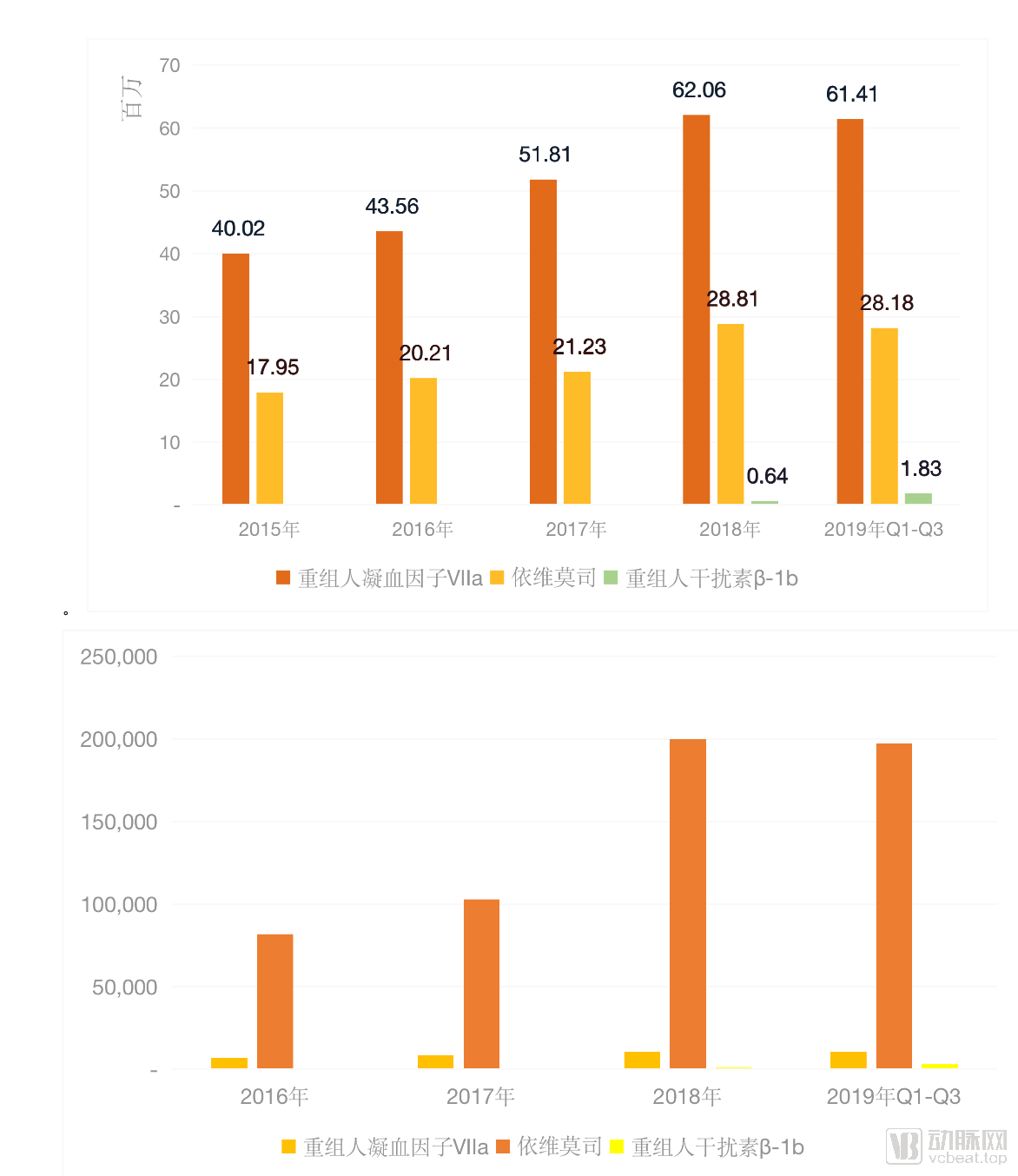

Taking recombinant human coagulation factor VIIa, everolimus, and recombinant human interferon beta-1b as examples, these three products are used to treat hemophilia, tuberous sclerosis complex, and multiple sclerosis, respectively, with price reductions of 10%, 42%, and 30% through national medical insurance negotiations. According to the 2018 IQVIA sample public hospital database, the sales revenue of recombinant human coagulation factor VIIa increased by 19.8% year-on-year, and that of everolimus increased by 35.7% year-on-year; the minimum package size and unit sales volume of recombinant human coagulation factor VIIa increased by 27.2% year-on-year, and those of everolimus increased by 94.2% year-on-year.

As can be seen from the above data, after price reductions through medical insurance negotiations and inclusion in the reimbursement list, the sales revenue of the three drugs increased steadily, with a relatively high growth in sales volume. However, both sales revenue and volume remained far from reaching an explosive surge. Nevertheless, among the drugs subject to renewal negotiations in 2019, Recombinant Human Interferon β-1b failed to secure contract renewal.

In such circumstances, even after inclusion in the national medical insurance scheme, market cultivation and promotion of orphan drugs remain indispensable, and necessary education for clinicians and patients must continue. However, given the unique characteristics of rare diseases, relevant government departments may have greater scope to provide support in the education of clinicians and patients.

Companies must prioritize sustainable profitability as a prerequisite, enabling them to plan the launch of higher-quality products on the basis of normal operations. Admittedly, some companies have chosen orphan drugs as an entry point to transform their product portfolios and build brand reputation. In such cases, although orphan drugs generate limited profits, they help establish a positive corporate image, create social impact, and cultivate resources across various stakeholders, thereby laying the foundation for the promotion of other product lines. However, for R&D-driven innovative drugs, inadequate price protection may lead to insufficient incentives for subsequent research and development. Unlike conventional medications, orphan drugs require a balanced pricing strategy that offers hope for both enterprises and patients to move forward together.

It is well known that patients with rare diseases bear a heavy medication burden. The “2019 Comprehensive Social Survey of Patients with Rare Diseases in China,” led by the Chinese Alliance for Rare Diseases, co-initiated by Peking Union Medical College Hospital, supported by the Beijing Pain Challenge Public Welfare Foundation, and implemented by the Jockey Club School of Public Health and Primary Care at The Chinese University of Hong Kong, revealed that among the 13,235 patients surveyed, nearly half (49.2%) came from households with an annual income below RMB 50,000, including 2.4% of households that reported no income at all in 2018. On average, the annual household income for the 13,235 patient families was RMB 87,969.5 in 2018. Specifically, the average annual household income for families with adult patients was RMB 88,201.9, while for families with pediatric patients, it was RMB 90,400.9.

Overall, the medical expenses incurred by surveyed patients in 2018 (including direct and indirect medical costs as well as non-medical healthcare-related expenditures) amounted to approximately RMB 67,528.77 per capita; of this, the out-of-pocket expense was RMB 57,900.77, accounting for 85.7% of total medical spending. Specifically, the average out-of-pocket medical expenditure for adult patients was RMB 50,472.30, representing 57.2% of their household’s annual income; for minor patients, the average medical expenditure was RMB 65,245.90, accounting for 72.2% of household annual income. The financial burden of medical care on families with minor patients is heavier than that on families with adult patients.

Among the 11,623 patients who have received or are currently receiving treatment, 90.5% primarily rely on pharmacological therapy. In this context, reducing the medication cost burden for patients with rare diseases has become one of the core issues of greatest concern to government authorities.

On February 22, 2019, the Ministry of Finance and three other departments issued the “Notice on Value-Added Tax Policies for Orphan Drugs,” which stipulates that, effective March 1, 2019, imported orphan drugs shall be subject to import-stage value-added tax (VAT) at a reduced rate of 3%. General VAT taxpayers engaged in the production, sale, wholesale, or retail of orphan drugs may opt to calculate and pay VAT under the simplified method at a 3% levy rate.

。

The initial list of 21 rare disease drugs eligible for tax reduction policies has also been released, with several medications indicated for the treatment of pulmonary arterial hypertension. The list also includes therapies for pediatric conditions such as Gaucher disease, Pompe disease, and hyperphenylalaninemia. Patients are expected to benefit from these price reductions.

On the morning of October 19, 2019, Li Tao, a member of the Party Leadership Group and Deputy Director of the National Healthcare Security Administration, stated at the 2019 China Rare Disease Conference: “We are currently considering and exploring new mechanisms for ensuring access to medications for rare diseases outside the existing basic medical insurance framework, as well as feasible pathways to further enhance the level of coverage for rare diseases... At the same time, we will tilt policies related to critical illness insurance and medical assistance further toward patients with rare diseases.” She indicated that, in addition to medication costs, other eligible medical expenses incurred by rare disease patients will be fully covered by medical insurance. Furthermore, some impoverished patients will receive assistance through critical illness insurance and medical assistance programs to alleviate their substantial financial burden.

However, Li Tao also pointed out that due to constraints such as national economic development and the fund’s affordability, certain extremely expensive drugs and treatments are currently excluded from basic medical insurance coverage. In the next step, the National Healthcare Security Administration will adopt various measures to significantly enhance the level of coverage for rare diseases.

The National Healthcare Security Administration’s specific measures are as follows: First, improve the dynamic adjustment mechanism for the National Reimbursement Drug List (NRDL), continue to prioritize the inclusion of medicines for rare diseases, and promptly add eligible drugs to the list. Second, continue to conduct NRDL access negotiations and centralized volume-based procurement to leverage the advantages of bulk purchasing, striving to further reduce the prices of expensive rare-disease medications. Third, strengthen coordination and communication with relevant departments to explore new mechanisms for ensuring access to rare-disease medications beyond the existing basic medical insurance system, thereby identifying feasible pathways to further enhance protection levels for rare diseases. At the same time, policies related to critical illness insurance and medical assistance will be further tilted in favor of patients with rare diseases.

It is evident that the National Healthcare Security Administration and the Ministry of Finance have adopted multiple measures to reduce the medication burden for patients with rare diseases. However, what is the actual financial burden borne by these patients in real-world settings? Data must provide the answer.

How Many Problems Can Medical Insurance Reimbursement Solve?

Compared with new technologies and products, conventional traditional drugs for rare diseases impose a relatively lower medication burden on patients. This chapter focuses on rare disease drugs newly included in the National Reimbursement Drug List (NRDL) in 2017 and 2019, aiming to assess the medication burden on patients.

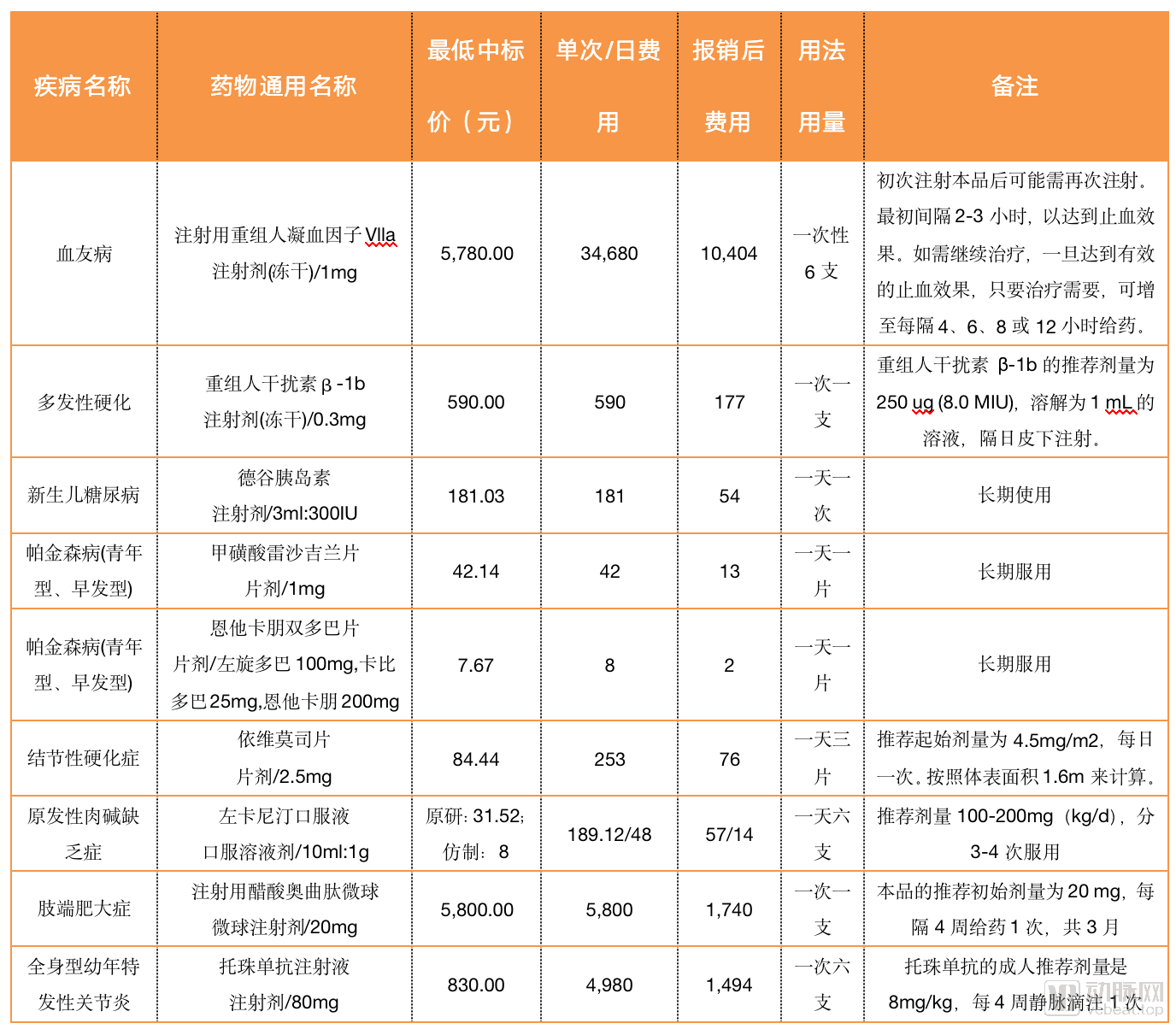

Based on a standard adult weight of 60 kg, the single-dose or daily medication burden for the following drugs is calculated. The financial burden of medications for different rare diseases varies significantly. For hemophilia, the cost per injection is nearly RMB 35,000. Even after a 30% reimbursement through medical insurance, patients still face an out-of-pocket cost of approximately RMB 10,000 per dose. Furthermore, according to the dosage and administration instructions in the package insert, a second injection may be required after the initial dose to achieve hemostasis, with an initial interval of 2–3 hours. If continued treatment is necessary, once effective hemostasis is achieved, the dosing interval can be extended to every 4, 6, 8, or 12 hours as clinically indicated. For patients, the daily out-of-pocket medication cost after insurance reimbursement may range between RMB 20,000 and RMB 60,000.

Meanwhile, the cost of medications for certain rare diseases is relatively low. For example, in cases of Parkinson’s disease (juvenile-onset and early-onset), the average monthly out-of-pocket expense ranges from RMB 60 to 400 after 30% reimbursement by medical insurance, which remains affordable for households. For other rare diseases, the average monthly medication costs range from RMB 1,000 to 2,200 after insurance reimbursement.

As can be seen, medical insurance reimbursement has significantly reduced the out-of-pocket expenses for patients. However, due to constraints on medical insurance funds, it is not yet feasible to include all rare disease medications in the coverage. Incorporating rare disease drugs into the medical insurance catalog involves budget impact analysis: what would be the financial strain on the medical insurance fund after their inclusion? During the development of the aforementioned model, accurate and authentic patient data are essential. What are the actual incidence rates of these rare diseases? Are the patient population size and the market volume for rare disease medications within expected ranges? Without such foundational data, not only will pharmaceutical companies struggle to move forward, but medical insurance authorities will also face significant challenges. In this context, leveraging the convenience of internet-based information collection can greatly streamline the cumbersome process of gathering patient data. By utilizing these data, the government can better assess the medication burden on patients. Meanwhile, if enterprises leverage these data, they can make more informed project decisions and identify genuine blue-ocean opportunities in the rare disease market, rather than chasing mirages that turn out to be bottomless pits.

How can the financial burden on patients be alleviated for orphan drugs not included in the National Reimbursement Drug List?

Reducing Medication Costs Through Generics?

Among drugs capable of treating rare diseases, many are also indicated for other conditions. In other words, treating common diseases is their primary indication, while providing therapeutic benefits for rare diseases is an unexpected yet logical extension. For example, ursodeoxycholic acid, currently approved for production by 42 manufacturers, is used to treat gallbladder cholesterol stones, cholestatic liver disease, and bile reflux gastritis; for rare diseases, it is indicated for congenital bile acid synthesis disorders. Other examples of drugs that treat both common and rare diseases include desmopressin acetate injection, human coagulation factor VIII, prothrombin complex concentrate, and teniposide injection, among others from various therapeutic areas. Multiple generic versions of these drugs have already been marketed.

For drug varieties manufactured by multiple generic pharmaceutical companies, market competition is relatively robust, resulting in lower market prices for generics compared to the originator drug. In contrast, for varieties with only one or two generic manufacturers, market competition is insufficient, granting these enterprises stronger bargaining power. One particular variety has drawn our attention: levodopa combined with carbidopa. The generic version, produced by Jinghua Pharmaceutical Group Co., Ltd., containing 25 mg of carbidopa and 0.25 g of levodopa per tablet, has a minimum price of RMB 2.47 per tablet. Meanwhile, the originator product from Merck & Co., formulated as extended-release tablets containing 50 mg of carbidopa and 200 mg of levodopa, is priced at RMB 1.78 per tablet. This price inversion warrants in-depth investigation; however, this report will not delve further into this matter.

How to Reduce the Medication Burden for Patients with Rare Diseases When No Generic Drugs Are Available? Given the limited funds of the medical insurance system, it is not feasible to include all rare disease medications in the coverage. Furthermore, China’s national volume-based procurement program is restricted to rare disease drugs that have generic equivalents. So, what about the remaining patients’ medication needs?

Commercial Health Insurance for Rare Diseases Urgently Needs to Be Elevated

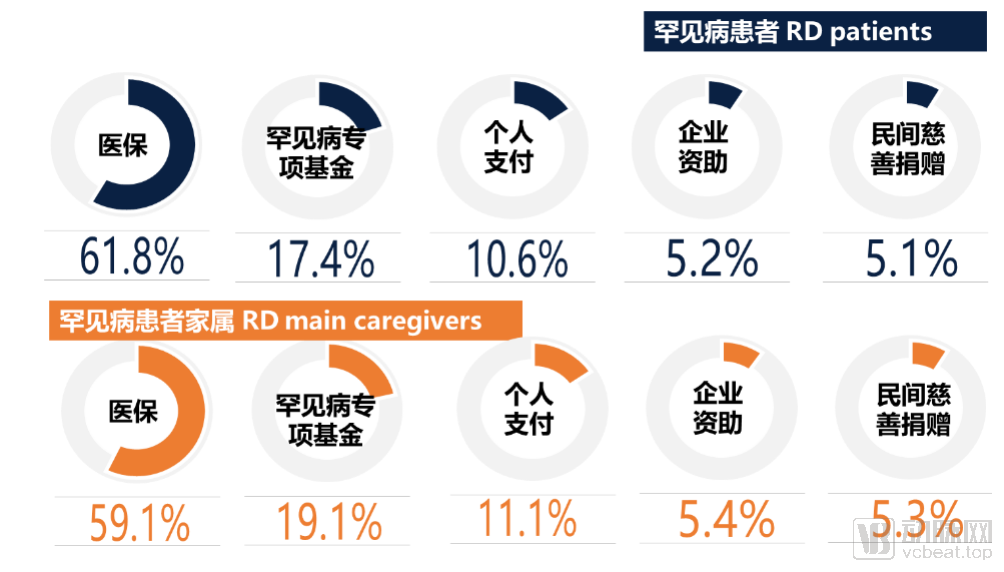

“The 2019 Comprehensive Social Survey of Rare Disease Patients in China” shows that rare disease patients and their families hope for greater policy support in areas such as medical insurance, special funds for rare diseases, corporate sponsorship, and private charitable donations.

Survey Results on the Comprehensive Social Status of Patients with Rare Diseases in China (2019)

The National Healthcare Security Administration is working to reduce the financial burden of rare disease medications through medical insurance negotiations and volume-based procurement. Meanwhile, corporate and private charitable donations can also help alleviate the medication cost burden for patients with rare diseases to a certain extent.

On July 18, 2019, the Management Committee of the Rare Disease Prevention and Control Development Special Fund under the China Health Promotion Foundation was established in Beijing. As a public welfare fund supporting the prevention and control of rare diseases in China, this special fund is committed to promoting a series of related public welfare activities, including rare disease screening, diagnosis, treatment, education, academic exchanges, and orphan drug research and development.

Imeda believes that the only sustainable solution is to commercialize rare disease medications, leveraging profit incentives to encourage companies to strengthen R&D efforts and bring more drugs to market, thereby addressing cost issues from a business perspective. In alleviating the financial burden on patients, reliance should not be placed solely on government and pharmaceutical companies; commercial insurance must also play its due role. Currently, commercial medical insurance, critical illness insurance, and accident insurance products are highly mature in the market, yet few insurance products cover medical expenses for rare diseases. It is understood that there is currently only one consumer-type critical illness insurance product in the market that includes coverage for specified rare disease medical expenses. Although insurance products targeting rare disease medical costs are scarce, they still demonstrate a viable market-oriented insurance model. Furthermore, companies developing and launching rare disease treatments could collaborate with insurance providers to explore diverse models, thereby reducing market entry risks for enterprises and lowering the medication burden for patients.

Certainly, when designing rare disease insurance products, insurers cannot do without essential baseline data—such as epidemiology, patient population size, and market potential—all of which need to be collected with the aid of internet-based tools. Insurers are poised to play a more significant role in the field of rare disease treatment.

In May 2018, the National Health Commission, the Ministry of Science and Technology, the Ministry of Industry and Information Technology, the National Medical Products Administration, and the National Administration of Traditional Chinese Medicine jointly released the "First Batch of Rare Diseases Catalog," which includes 121 rare diseases. According to epidemiological literature and public data estimates, these 121 rare diseases affect approximately 3 million patients in mainland China.

Most rare diseases are genetic disorders, typically characterized by severe clinical manifestations, progressive degenerative changes, and high mortality rates. Epidemiological data on rare diseases in China are lacking, with only a few rare diseases having reported epidemiological studies.

For certain rare diseases, this report conducted market research using hemophilia and idiopathic pulmonary arterial hypertension as case studies.

Hemophilia: A Large Market for Rare Diseases

According to Medgadget, the global hemophilia drug market was valued at approximately $9.875 billion in 2018, with hemophilia A drugs accounting for about 85% ($8.394 billion) of the market. Hemophilia B and C drugs collectively held a market share of approximately 15%. With the continuous launch of new therapeutic agents in the future, the global hemophilia drug market is projected to reach $15.83 billion by 2025. Currently, key players in the global hemophilia drug market include Shire, Novo Nordisk, Pfizer, Bayer, Sanofi, Roche Ltd, Grifols SA, Bioverativ Inc., Octapharma, Aptevo Therapeutics, CSL Behring, and Hoffmann-La Roche Ltd. According to disclosures by Shire, in 2018, Shire (including its subsidiary Baxalta), Novo Nordisk, Pfizer, Bayer, Sanofi, and CSL held global hemophilia drug market shares of approximately 38%, 15%, 11%, 11%, 11%, and 10%, respectively.

Coagulation factor replacement therapy remains the absolute mainstream treatment for hemophilia on the current market. Data published by Decision Resources Group shows that coagulation factor replacement therapy accounted for more than 99.9% of total sales in 2017. Experts predict that these therapies will continue to be the primary treatments for hemophilia; however, over the next decade, more non-factor therapies and gene therapies are expected to gain approval, offering hemophilia patients a broader range of treatment options.

In the domestic market, coagulation factor replacement therapy is the mainstream treatment for hemophilia in China. Currently, two primary prophylactic regimens are widely used internationally: the Malmö regimen (high-dose) and the Utrecht regimen (intermediate-dose). Based on China’s actual conditions, a low-dose regimen is currently being piloted (e.g., for patients with hemophilia A, 10 IU/kg per dose, administered twice weekly). Calculated based on this low-dose regimen, the average annual cost of prophylactic treatment for hemophilia per patient in China is RMB 140,400 (ranging from RMB 98,800 to RMB 182,000), resulting in a total market size for hemophilia in China of nearly RMB 5.5 billion.

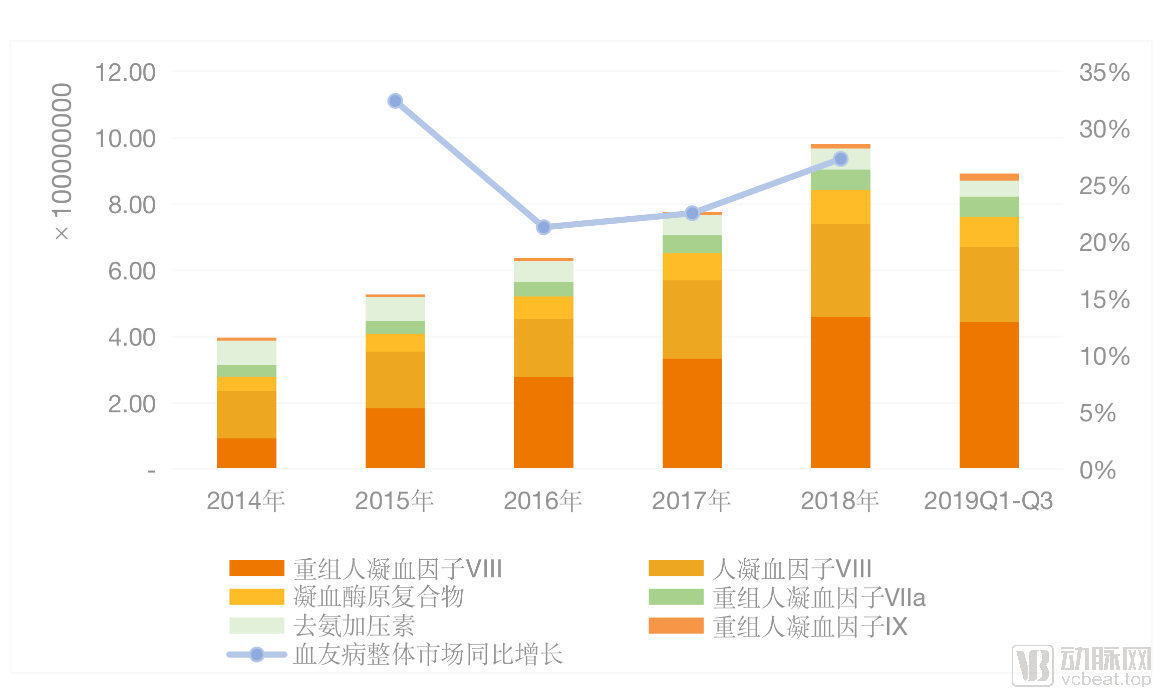

By analyzing six generic drugs—human coagulation factor VIII, recombinant human coagulation factor VIII, prothrombin complex concentrate, recombinant human coagulation factor VIIa, recombinant human coagulation factor IX, and desmopressin—we can estimate the hemophilia market.

Recombinant human coagulation factor VIII has demonstrated relatively stable growth, with a compound annual growth rate (CAGR) of 49% over the past five years. Sales reached RMB 440 million in the first three quarters of 2019, involving three foreign companies (Baxter, Bayer, and Pfizer). In contrast, human plasma-derived coagulation factor VIII has experienced slower growth, with a CAGR of 19% over the past five years. Total sales amounted to RMB 230 million in the first three quarters of 2019, involving four domestic companies. Both recombinant coagulation factor VIII and human plasma-derived coagulation factor VIII are used to treat hemophilia A, which accounts for 80%–85% of all hemophilia cases. This aligns closely with data from the Aimeda sample public hospital database, where the market volume of recombinant and human plasma-derived coagulation factor VIII represented 72% of the total volume for the products included in this analysis.

In the Yimeda sample public hospital database, prothrombin complex concentrate (PCC) and recombinant coagulation factor VIIa accounted for approximately 17% of the overall hemophilia treatment market. The total sales amount for PCC in the first three quarters of 2019 was RMB 88.81 million, while that for recombinant coagulation factor VIIa was RMB 61.41 million, with compound annual growth rates (CAGR) of 24% and 16%, respectively. Five domestic companies reported sales of PCC, whereas recombinant coagulation factor VIIa was supplied by Novo Nordisk. In addition to treating hemophilia, PCC has been approved for multiple indications.

Desmopressin is indicated for bleeding episodes in patients with mild hemophilia A and carriers, or for the treatment of mild bleeding in hemophilia A patients with low-titer inhibitors; it is ineffective for bleeding in patients with hemophilia B. According to the Yimeda sample database of public hospitals, desmopressin accounted for 5.53% of the total market sales value in the first three quarters of 2019, with total sales amounting to RMB 49.37 million. Its market share has shown a declining trend year by year, with a five-year compound annual growth rate (CAGR) of -4%. Sales were recorded from three manufacturers (one foreign-funded and two domestically produced). In addition to hemophilia, desmopressin is used for various other indications. Although desmopressin’s share of total sales value in the overall hemophilia market has declined annually, it accounts for approximately 80% of the total market volume in terms of the number of minimum dosage units sold, which is largely attributable to its pricing factors.

Overall, hemophilia medications represent a relatively mature niche within the orphan drug sector. As treatment is typically lifelong for patients, the market potential is substantial. For new drugs, this area offers significant market space and high feasibility.

Idiopathic Pulmonary Arterial Hypertension — Market Expectations Show Slow Growth

According to estimates by the information company GlobalData, the global market for pulmonary arterial hypertension (PAH) drugs across the seven major pharmaceutical markets (the United States, Japan, and the five major European countries: France, Germany, Italy, Spain, and the United Kingdom) was approximately USD 3.79 billion in 2016. GlobalData predicts that over the next decade, the overall market will grow to USD 4.72 billion, representing a compound annual growth rate (CAGR) of 2.2%. An epidemiological study conducted in France indicated that idiopathic pulmonary arterial hypertension (IPAH) accounts for approximately 39.2% of all PAH cases¹⁷. Based on this rough estimate, the market size for IPAH is projected to increase from USD 1.49 billion in 2016 to USD 1.86 billion in 2026.

The five major European countries will be the fastest-growing among these three regions, with a compound annual growth rate (CAGR) of approximately 5.4%, compared to 1.2% in the United States and 1.0% in Japan. By 2026, the U.S. is expected to account for approximately 67% of the global market share, while the five major European countries and Japan will hold 28% and 5%, respectively. The larger market share in the U.S. can be attributed to higher drug prices and a higher diagnosis rate of pulmonary arterial hypertension (PAH) in the region.

In the domestic market, pulmonary arterial hypertension (PAH) drugs mainly rely on imports, including four major categories: prostacyclins, endothelin receptor antagonists, guanylate cyclase stimulators, and selective prostacyclin IP receptor agonists. Based on an average annual treatment cost of RMB 100,000 per patient for domestically available oral therapies such as bosentan, ambrisentan, riociguat, and macitentan, the total market size for PAH in China is estimated at approximately RMB 2 billion, with the idiopathic pulmonary arterial hypertension (IPAH) segment accounting for around RMB 800 million.

Currently, the targeted therapies approved in China for the treatment of pulmonary arterial hypertension include: bosentan, ambrisentan, macitentan, iloprost, treprostinil, riociguat, and selexipag. Among these, riociguat and selexipag have no sales data recorded in the Aimeida sample public hospital database. This chapter defines the total market size for targeted therapies in idiopathic pulmonary arterial hypertension based on the following five generic drugs: bosentan, ambrisentan, macitentan, iloprost, and treprostinil.

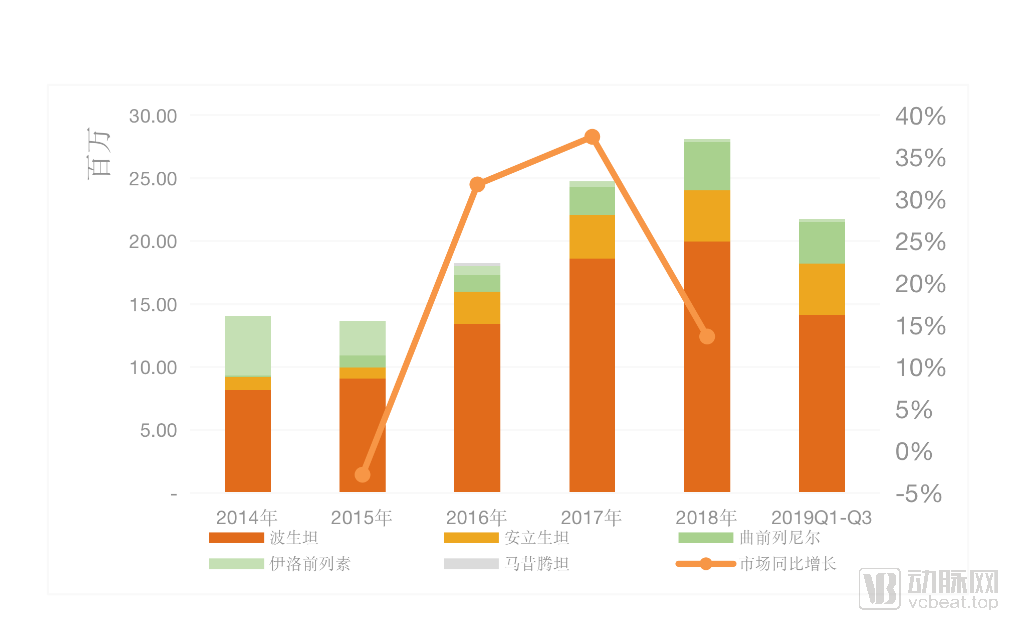

Overall, in the Yimeda sample database of public hospitals, the total market size for targeted therapies for idiopathic pulmonary arterial hypertension was nearly 30 million yuan in 2018, with a compound annual growth rate (CAGR) of 18.9% over the past five years.

Total Sales Revenue and Year-on-Year Growth Rate of Targeted Drugs for Idiopathic Pulmonary Arterial Hypertension in Public Hospitals Based on the Aimada Sample

According to the Yimida Sample Public Hospital Database, bosentan is an endothelin receptor antagonist and currently the primary targeted therapy for pulmonary arterial hypertension. In the first three quarters of 2019, it accounted for 64.95% of the overall market share, with total sales amounting to RMB 14.128 million and a five-year compound annual growth rate (CAGR) of 22%. Bosentan was launched in China in 2006. Currently, only GlaxoSmithKline reports sales figures for this drug, as no generic versions have yet been marketed.

Ambrisentan, another endothelin receptor antagonist developed and manufactured by GlaxoSmithKline, was launched in China in 2010, with two generic versions currently approved for marketing. In the first three quarters of 2019, ambrisentan accounted for 18.83% of the total market, with sales reaching RMB 4.096 million and a compound annual growth rate (CAGR) of 26% over the past five years.

Treprostinil and iloprost are prostacyclin analogs. The former is a first-line treatment for patients with WHO functional class III or IV, while the latter serves not only as an agent for acute pulmonary vasodilator testing but also for the emergency management of pulmonary hypertensive crises. According to the Aimeida Public Hospital Database for the first three quarters of 2019, treprostinil accounted for 15.13% of the total market, with sales reaching RMB 3.291 million and a five-year compound annual growth rate (CAGR) of 71%; however, its market share has been declining rapidly year by year. Iloprost accounted for 1.08% of the total market, with sales of RMB 236,000 and a five-year CAGR of -42%.

Notably, in June 2019, the National Health Commission issued the First Batch of Encouraged Generic Drug List, explicitly listing 33 generic drug varieties for initial encouragement. It proposed that relevant departments should provide support in areas such as clinical trials, research on key common technologies, and priority review and approval, in accordance with relevant regulations. Bosentan and treprostinil were included in this list. However, an analysis of sales data from public hospitals in the sample reveals that the sales performance of treatments for idiopathic pulmonary arterial hypertension over the past five years has been far from optimistic. When generic drug manufacturers see no market prospects, it is difficult to entice them into this field merely through government appeals or incentives.

On the morning of October 19, 2019, Wang Hesheng, Deputy Director of the National Health Commission, stated at the 2019 China Rare Disease Conference that to strengthen the relatively centralized diagnosis and treatment of rare disease patients and promote two-way referrals, a National Rare Disease Diagnosis and Treatment Collaboration Network had been established. This network comprises one national-level lead hospital, 32 provincial-level lead hospitals, and 291 member hospitals, thereby creating a comprehensive rare disease diagnosis and treatment framework. By establishing smooth collaborative mechanisms, the network leverages the radiating and driving role of high-quality medical resources. The establishment of this collaboration network in China will help enhance clinical diagnosis and treatment capabilities for rare diseases, clarify the disease burden of rare diseases in the country, and provide important support for the formulation and improvement of relevant policies.

Meanwhile, China has launched a nationwide initiative to register diagnostic and treatment information for rare disease cases. The National Rare Disease Registry System (NRDRS) is a foundational data platform that captures specific patient information. By registering basic demographic data of patients and their families, clinical histories, biological samples, multi-omics results, imaging, and pathological image data, the system accurately reflects the incidence and prevalence of rare diseases among the affected population in China.

With the rapid development of the Internet, the permeability and synergy of information have been enhanced. Leveraging the Internet and big data to establish and improve China’s rare disease database will address the lack of foundational data on rare diseases in China, providing a critical basis for disease diagnosis and treatment, drug research and development, and policy formulation.

However, the rare disease drug development industry has its own unique characteristics. There are numerous types of rare diseases, and for the vast majority, their pathogenesis remains unclear.

In the short term, there remains a gap in the accessibility of orphan drugs in China, particularly those for conditions listed in the First Batch of Rare Diseases Catalog, compared with developed countries and regions. For near-term development, enterprises are advised to closely track orphan drugs already marketed internationally, as well as those approved in China but not yet indicated for rare diseases, so as to accelerate the market launch of orphan drugs in China and prioritize addressing accessibility issues.

In the long term, companies developing orphan drugs, particularly innovative agents, must adopt an international perspective. Given the small patient populations associated with rare diseases, focusing solely on the Chinese market may obscure their commercial value. In light of the current lack of foundational epidemiological data on rare diseases in China, treating rare diseases as global conditions and leveraging existing international data can support corporate R&D project initiation. Although China is gradually establishing clinical policies and technical guidelines for rare diseases, these efforts remain in an exploratory phase. During this process, companies should draw upon the R&D experience and relevant regulatory guidance from developed countries such as those in Europe, the United States, and Japan to formulate strategies for rare disease drug development, while actively engaging in communication with Chinese regulatory authorities. As clinical research represents a major bottleneck in rare disease drug development, domestic companies should prioritize adopting innovative clinical trial designs used abroad—such as basket trials, umbrella trials, and platform trials—to advance clinical development.

In the past two years, with adjustments in national pharmaceutical policies, companies with single-product structures and those driven by marketing have been adversely affected, resulting in declining performance. Facing business dilemmas and intense market competition, many traditional pharmaceutical enterprises are actively seeking new growth points for the future, transforming towards the development of new drugs such as small-molecule chemical drugs, and even biologics including monoclonal antibodies, bispecific antibodies, and cell therapies. For instance, Buchang Pharmaceuticals has laid out a strategy for biologics such as PD-1 inhibitors and bispecific antibodies, while Xiangxue Pharmaceutical has entered the field of cell therapy. Traditional pharmaceutical companies possess abundant resources across the pharmaceutical industry chain, have a profound understanding of the industry, policy, and profit distribution landscape, and demonstrate certain capabilities in resource integration. For these enterprises, venturing into the rare disease sector represents a path for upgrading and transformation, which to some extent facilitates the accumulation of reputation, brand image building, and the development of government relations. However, constrained by their existing resources, it is difficult and unrealistic for these companies to fully independently develop innovative drugs. In the short term, they can introduce or collaboratively develop innovative drugs for rare diseases and Me-too drugs by leveraging external forces; or focus primarily on generic drugs and improved new drugs. In the long term, they can set their sights on the research and development of innovative drugs.

On the one hand, companies can introduce rare disease drugs from abroad through license-in agreements to address the lack of effective treatments for certain rare diseases in China. For example, Canaan Healthcare has entered into strategic collaborations with South Korea’s GC Pharma and WuXi Biologics, among others, to accelerate the development of rare disease therapies in the country.

On the other hand, the development of generic or improved new drugs for rare diseases in China remains largely untapped, presenting significant opportunities for pharmaceutical companies. For instance, treprostinil, a drug used to treat pulmonary arterial hypertension (PAH), has been developed with a focus on clinical needs, undergoing two formulation improvements since its initial launch. The injectable form of treprostinil was approved by the U.S. Food and Drug Administration (FDA) on May 21, 2002. However, due to adverse reactions such as erythema and pain at the injection site, the originator company, United Therapeutics, developed an inhalable formulation of treprostinil (Tyvaso), which received FDA approval on July 30, 2009. Although the inhalable formulation reduced systemic adverse effects, its efficacy was inferior to that of subcutaneous and intravenous injections due to the lower delivered dose. On December 20, 2013, the FDA approved an extended-release tablet formulation of treprostinil (Orenitram), replacing subcutaneous, intravenous, and inhalation administration routes and thereby improving patient compliance. Currently, only the original injectable treprostinil is available in China, with only one domestic company, Lee’s Pharmaceutical, having submitted an application for marketing approval of a generic version.

In either scenario, the ultimate goal for pharmaceutical companies today is to deliver products with clinical value. Only by adhering to this objective can they achieve market success. This may involve addressing entirely unmet clinical needs by creating global first-in-class therapies to fill gaps in clinical treatment options, or offering alternatives to existing regimens to reduce the medication burden. In the development of Me-too/Me-better drugs, a product’s market potential hinges on either a price advantage or an efficacy advantage. In other words, the product offers superior efficacy at the same price, or comparable efficacy at a lower cost. Only such products can demonstrate clinical value, secure market share, and generate revenue for the company.

Rare diseases, as a new sector receiving substantial policy support in China in recent years, have begun to attract the attention of major international pharmaceutical companies, with foreign enterprises successively introducing new products into the Chinese market. For domestic companies dedicated to rare disease therapeutics, it is essential to establish clear positioning, select development pathways suited to their capabilities, and make more long-term and stable economic investments in R&D, thereby truly delivering more effective treatments to patients with rare diseases.