Is Virus Tracking Enough? How Capital and Industry Are Collaborating to Accelerate Digital Transformation in the Greater Health Sector

Singular Medical

Developer, Manufacturer, and Seller of Cardiac Rhythm Management Products

Digital preparedness enables the precise tracing of viral transmission paths down to a specific train car, a single floor, or even an individual dining table. What is the overall level of digitalization in the broader health industry? How is capital engaging in this sector? In what ways will capital collaborate with the industry to co-create the future of broad health? The answers to these questions may hold significant importance for clarifying the direction of the broad health industry and driving its development. The following presents research observations from Zero2IPO Capital, examining the landscape from both an overarching perspective and through representative case studies:

Is Virus Tracking Enough? What More Is Needed for Digitalization in the Greater Health Industry

In terms of supply and demand in the broader health sector: On the demand side, both acute-phase medical needs arising from short-term epidemics and the long-term demand for high-quality healthy living are growing rapidly in tandem. This shift, ranging from hospital-based care covered by medical insurance to out-of-pocket expenses for home-based patient care, is driving the total output value of the healthcare industry from its current RMB 5.79 trillion to the projected RMB 16 trillion under the “Healthy China 2030” initiative.

On the supply side, there is a severe imbalance in the regional distribution of medical resources. Beijing, Shanghai, Guangzhou, and provincial capital cities boast the strongest medical personnel and the highest concentration of high-quality hospitals. However, a larger proportion of patients are dispersed across vast grassroots communities and rural areas. Cultivating healthcare professionals and building high-quality hospitals require long-term investment. During this period, mature medical products (pharmaceuticals and medical devices) can partially address these challenges by delivering standardized diagnostic and therapeutic outcomes. However, a closer examination of the pharmaceutical and medical device industries reveals low efficiency due to various constraints, including policy, technology, and talent. For instance, in the pharmaceutical sector, the research and development of innovative drugs, along with clinical trials, demand enormous investments—often cited as “10 years and $1 billion”—yet yield an overall product launch success rate of less than 10%. Meanwhile, in the mature market for generic drugs, exorbitant marketing expenses, accounting for 30%–60% of costs, prominently reflect industrial inefficiency. Therefore, transforming the healthcare industry to enhance efficiency is an urgent imperative.

It Is Now: The Big Health Industry Embraces Digital Transformation

The digital economy represents the future direction of global development and serves as the core driver for economic transformation and upgrading. Currently, digitalization is deeply integrating with various industries. The first step in this digital journey involves migrating fragmented offline operations to online platforms. The recent pandemic, for instance, accelerated this forced transition to digital channels. A critical question arises: Is moving online merely a short-term contingency, or does it represent a long-term trend? Entrepreneurs who proactively prepared for digitalization are demonstrating through their actions and sustained performance growth that cloud-based operations and digital transformation are inevitable paths for the development and transition of traditional enterprises, as well as a long-term trend for the healthcare industry. As wise entrepreneurs note, it is better to proactively embrace the long-term trend of digitalization than to passively wait.

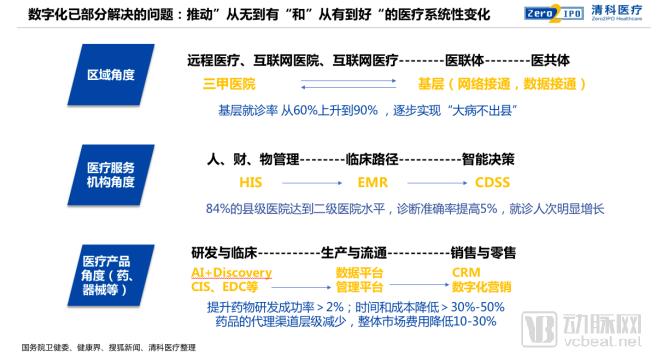

Digitalization has helped resolve some issues in supply-side reform. For instance, by connecting networks and data between tertiary hospitals and primary care institutions, and leveraging tools such as telemedicine, internet hospitals, and various out-of-hospital digital healthcare solutions, medical consortia and healthcare communities have been established. This has increased the consultation rate at primary care institutions from 60% in 2016 to 90% in 2019, gradually fulfilling the policy goal of “managing serious illnesses within the county.” The informatization of healthcare service providers has evolved from general management software (HIS), to clinical-centric Electronic Medical Records (EMR), and further to Clinical Decision Support Systems (CDSS) for intelligent auxiliary decision-making. Currently, 84% of county-level hospitals across China have reached the standards of secondary hospitals, with diagnostic accuracy improved by 5%, and significant growth in both outpatient and inpatient visits. Digitalization in R&D and clinical practice has increased the success rate of new drug development by 2%, while reducing time and costs by 30%-50%, serving as a powerful leverage point. Furthermore, digitalization in pharmaceutical distribution and sales has reduced the layers of agency channels, lowering overall market expense ratios by at least 10%-30%, demonstrating substantial value.

Mature Healthcare Product (Pharmaceuticals and Medical Devices) Marketing and Retail: Digital Transformation Rapidly Enhances Industry Efficiency

In contrast to the long timelines required for healthcare professional training and the establishment of R&D infrastructure, the efficient distribution and precise patient access of mature medical products (pharmaceuticals and medical devices) can yield visible improvements in industrial efficiency within a short period.

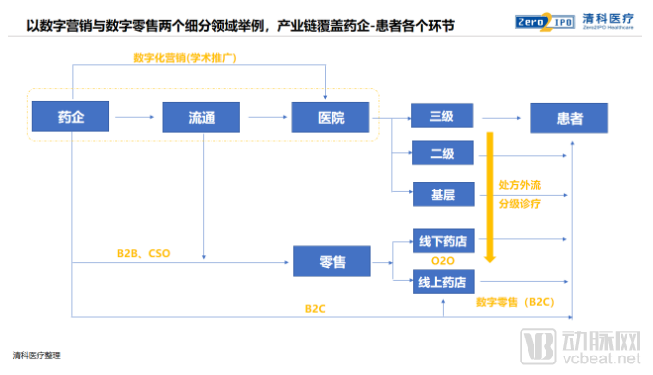

Overall, digital transformation enables a win-win scenario for pharmaceutical companies, physicians, patients, and the government. From the perspective of pharmaceutical companies, digitalization in the pharmaceutical sector effectively reduces costs and sales expenses through more compliant and efficient methods, enhances marketing efficiency, and improves access to medications at the primary care level, such as through online physician communities and vertical SaaS marketing platforms. From the physicians’ standpoint, online training and academic exchanges can improve the diagnostic and treatment capabilities of primary care physicians, exemplified by online departmental meetings and remote consultations. For patients, the application of pharmaceutical digitalization makes medication purchasing more convenient and faster, meets higher healthcare demands, and ensures price transparency throughout the process, as seen in telemedicine and online pharmacy services. From the government’s viewpoint, compliant digital platforms signify a reduction in gray-area marketing practices and an increase in transparent, legitimate activities, marking a significant step toward a healthier industry ecosystem.

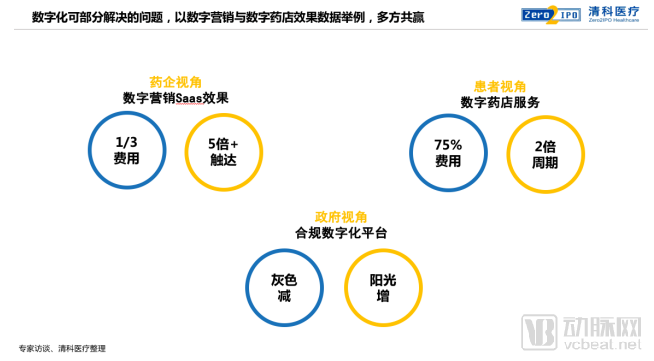

In terms of effectiveness, taking digital marketing and digital retail as specific examples, digital transformation has created a win-win situation for pharmaceutical companies, patients, and the government. From the perspective of pharmaceutical companies, thanks to the SaaS system for digital marketing, they can reach five times as many physicians within the same time frame while incurring only one-third of the original costs. From the patient’s perspective, digital pharmacy services have doubled medication adherence duration—significantly reducing the risk of disease recurrence—while lowering per-unit medication costs by more than 25%, demonstrating substantial value. The recent pandemic significantly accelerated the digital transformation of pharmaceutical enterprises. The online distribution of medicines and supply of protective materials greatly alleviated the supply-demand imbalance of domestic medical resources and helped address disparities in resource allocation. Furthermore, digital healthcare has provided safeguards for epidemic prevention and monitoring, thereby supporting the long-term enhancement of public health capabilities.

Overall, terminal drug sales in China have continued to grow, but the growth rate has been slowing. In 2018, the total scale of drug sales reached RMB 1.7 trillion, with a growth rate of approximately 6.3%; compared to the 15% growth rate in 2013, the pace has gradually decelerated, and future growth is expected to follow an even slower trend. Regarding changes in the structure of medication use within the terminal sales market, the overall trend indicates a shift from hospitals to primary care institutions, and from offline channels to online platforms. For in-hospital drug sales, municipal public hospitals recorded the lowest growth rate at 7.6%, county-level hospitals grew by 12.9%, while primary care institutions accounted for the largest share, with a growth rate of 13–15%. For out-of-hospital drug sales, the growth rate of retail pharmacies declined to 4.5%, whereas online pharmacies achieved an annual growth rate exceeding 40%. These changes and shifts are primarily driven by long-term healthcare reform policies aimed at cost containment, with the recent epidemic serving as a powerful catalyst. During the COVID-19 outbreak, retail pharmacies assumed a critical role in terminal drug sales due to their extensive coverage, strong accessibility, and low risk of cross-infection, while hospital terminal sales relatively decreased. This has, to some extent, altered consumer habits, and the resulting changes in demand require enterprises to capitalize on the outward flow of prescriptions during the epidemic and share in the long-term value of retail channels offered by pharmacies.

The results indicate that during the pandemic, online academic exchanges among physicians, online patient consultations, and online medication purchases all increased by more than 60%. According to MobTech big data, the daily new installations for the online consultation platform “Ping An Good Doctor” surged from 23,000 before the pandemic to over 45,000 during the outbreak, with a peak of 82,000. Platforms such as WeDoctor and Haodf Online also experienced significant growth during this period, particularly among users in Hubei Province. The peak number of active users for pharmaceutical e-commerce platforms—including 1 Drug Network, Dingdang Kuaiyao, Ali Health, Kuaifang Songyao, and Dekai Pharmaceutical—reached 1.4821 million during the pandemic, representing an average growth of 5.44%. The daily launch frequency of pharmaceutical O2O (Online-to-Offline) providers rose markedly, with an increase of nearly 50%. Meanwhile, sales of commonly stocked prescription drugs during the Spring Festival surged by 237%.

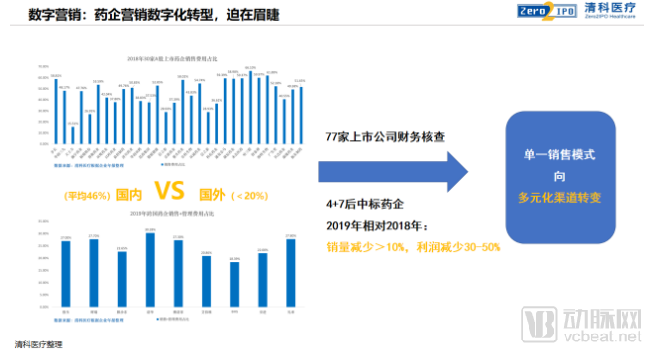

(1) Taking digital marketing as an example: The digital transformation of marketing in the general health industry is imminent.

China currently has over 2 million pharmaceutical sales representatives, primarily responsible for conveying and promoting the academic value of drugs. Their services are mainly directed toward physicians in tertiary Grade A hospitals, resulting in high sales costs and constraints related to visitation times and locations. Statistics show that due to the nationwide implementation of the "Two-Invoice System" from 2016 to 2017, listed companies moved off-balance-sheet sales expenses onto their balance sheets, with these expenses averaging 32% of revenue. For chronic disease medications and traditional Chinese medicines, sales expenses can reach as high as 50%. This figure contrasts significantly with the average combined "sales and administrative" expense ratio of 20%-30% observed in multinational pharmaceutical companies. As cost pressures rise, the continuous introduction of volume-based procurement (VBP) policies has rendered the traditional sales models of pharmaceutical companies ineffective, creating an urgent need for diversified sales channels. The first round of "4+7" VBP at the end of 2018 resulted in an average price reduction of 52% for 25 selected drugs, with a maximum reduction of 96%. In September 2019, the second round expanded the "4+7" pilot from 11 cities to the entire country, leading to an additional average price reduction of 25% for the same 25 selected drugs on top of the previous cuts. In December 2019, the third round of VBP covered 33 drug varieties, achieving an average price reduction of 53%, with a maximum reduction of 93%. The three rounds of VBP policies have driven drug price reductions exceeding 50%, posing severe challenges and new requirements for transforming corporate marketing strategies. The effective implementation and tangible outcomes of these policies depend on enhancing the digitalization level of the industry.

(2) Taking Digital Retail as an Example: Accelerating the Innovative Development of New Retail in the Greater Health Sector, the “Last Mile” Goldmine

At this stage, the increasing share of online sales in China’s pharmaceutical retail market is driving a gradual narrowing of inter-regional drug price disparities, thereby lowering the overall average drug price. The emerging nationwide unified retail pricing has intensified competition among pharmaceutical products. Only new retail pharmaceutical enterprises with strong source control capabilities, efficient supply chain operations, and refined user management can stand out in this competitive landscape.

Pharmaceutical New Retail Enterprises Actively Embrace Digital Transformation: They create and launch more innovative retail models and services for brick-and-mortar pharmacies, making this a key focus of digital upgrading and thereby driving the “Smart+” transformation of the distribution sector. Meanwhile, by bridging pharmaceutical manufacturers and physical pharmacies, they are poised to become the primary force behind the industry’s “Smart+” upgrade. This type of upgrade is low-cost, quick to implement, and user-friendly, enabling a rapid boost in terminal efficiency for pharmaceutical new retail.

(3) Digital-Driven Surge in Big Health Marketing and Multi-Format New Retail

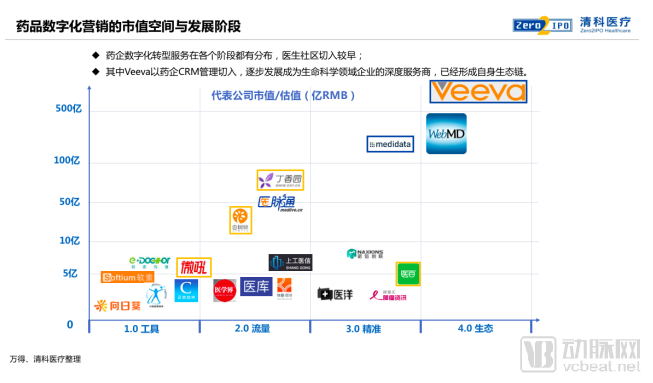

The path of industrial digitalization can be summarized into four stages: Stage 1.0 (Tool Stage), Stage 2.0 (Traffic Stage), Stage 3.0 (Precision Stage), and Stage 4.0 (Ecosystem Stage). It is easy to understand that the beginning of digital transformation must start with a specific functional attribute, moving online through particular tools such as live-streaming software and office approval systems. Subsequently, it enters the realm of communication and market demand, namely brand promotion and traffic attraction provided by media and specialized vertical platforms. However, with the rapid rise in traffic acquisition costs, the need for precise user reach has been elevated to a more critical position. Platforms capable of rapidly identifying and matching new users, while facilitating quick connections and sustained maintenance of existing customers, have gained greater favor. Ultimately, To-C and To-B enterprises will choose to collaborate in building an ecosystem for niche industries, working further toward expanding industrial scale and ensuring the rational distribution of industrial efficiency, so that all participants in the industry can achieve sustainable benefits and operations.

The undisputed giant in digital pharmaceutical retail is CVS, which leads globally in its OTO (Online-to-Offline) and PBM (Pharmacy Benefit Manager) businesses, with a market capitalization of USD 93.9 billion. Veeva, the pioneer in digital transformation for pharmaceutical companies, started with pharmaceutical CRM and has gradually evolved into a deep-service provider in the life sciences sector, boasting a market capitalization as high as USD 24 billion. In light of this, there is still significant room for growth in both business scope and valuation for leading domestic enterprises in China.

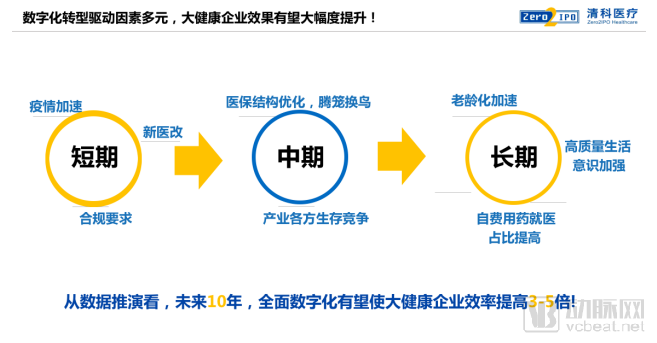

Short-, Medium-, and Long-Term Multi-Drivers Significantly Boost Digital Transformation in the Big Health Industry

In the digital transformation of the broader healthcare industry, driving factors are becoming increasingly diverse from the short to the long term. According to relevant data projections, comprehensive digitization is expected to boost the efficiency of healthcare enterprises by 3–5 times over the next decade.

Capital Infusion Drives Deeper Digital Transformation in the Healthcare Industry

From a capital perspective, the top three largest financing deals in the healthcare sector in 2019 were all in the digital health space. Therefore, it is evident that in the post-pandemic era, the capital market will pay greater attention to the digitalization of pharmaceuticals and healthcare. This represents not only a short-term opportunity but also a long-term solution to evolving medical needs, progressing from “availability” to “quality.” New business models will gradually emerge, and superior commercial models will quickly come to the forefront. Pharmaceutical sales will shift from a single-channel model to a multi-channel approach, with a focus on digital enterprises that effectively address these needs. Meanwhile, the market for online new retail in pharmaceuticals will continue to expand, further highlighting companies with innovative solutions, supply chain advantages, and refined operational capabilities.

Numerous healthcare enterprises operate in the digital space, with innovations spanning across various sectors of the broader health industry. Among them, many dynamic companies have also shone brightly in the capital market, with representative firms from multiple sectors demonstrating high activity levels from financing to IPOs.

Still Facing Numerous Challenges, Solutions Will Eventually Emerge

From an optimistic perspective, digitalization in the broader health sector has garnered significant favor from capital markets. However, for the healthcare and wellness industry itself, digital transformation encounters certain obstacles when penetrating into the deeper layers of medical practice, such as

1) The pharmaceutical industry features a long value chain and a complex industrial landscape;

2) The decision-making mechanisms and processes in hospitals and other institutions are complex;

3) The pharmaceutical industry requires long-term cultivation of user habits, among other factors. As a driving force for industrial development, digitalization still has a long way to go. Only through greater professional specialization and collaboration can we promote systematic upgrades across the industry, enabling all participating parties to achieve synergistic win-win outcomes. We will join forces with multiple research institutions to regularly release weekly research reports on the digital transformation of the broader healthcare sector, aiming to provide data and informational support to enterprises and investors in this field, thereby serving as a reference for collaborative decision-making.

In the face of unknown viruses, we recognize our own insignificance and fragility; witnessing healthcare workers become warriors who advance against the tide, safeguarding us with their lives, we further realize the responsibility borne by professionals in the medical and health industry.

Amid the severe epidemic, with a surge in patients at fever clinics and intensive care units, there was a critical shortage of protective equipment for healthcare workers and daily necessities for both medical staff and patients across healthcare institutions at all levels. In response, we partnered with the Yihujia team to launch a public welfare initiative at midnight on Chinese New Year’s Eve, aiming to deliver urgently needed supplies to frontline healthcare workers in Hubei Province. With an initial contribution of RMB 200,000 as seed funding, we rapidly raised over RMB 1.6 million in cash and kind. Within ten days, through a relay effort involving multiple medical enterprises, socially responsible companies, and compassionate individuals, essential items—including medical masks, antiviral medications, disinfection products, and medical linens—were delivered to 15 healthcare institutions in Wuhan and its surrounding cities and counties.

We believe that many friends, like us, are contributing their care and support to epidemic-affected areas and the people there through various means. From the collective charitable actions across society, we witness the power of inter-enterprise collaboration. Spanning from supplies to logistics, and from commerce to philanthropy, organizational boundaries dissolve, replaced by a unified determination to act in concert. Efficiency is the goal of digitalization, but it stems even more from shared objectives and aligned hearts. We have launched a long-term public welfare initiative called “Heju Yinuo” (United Medical Promise). In the future, we hope to drive greater commercial接力 (relay/continuity) through research, consulting, and training, fostering multi-party collaboration within the broader health industry. We advocate for collaborative symbiosis, united efforts for mutual benefit, and business for good. The companions on our journey are as important as, if not more important than, the destination itself. We look forward to walking this path together with you!