Strategic Moves by Global Pharma Giants in 2020: Innovation, Pandemic Response, and Portfolio Restructuring

Roche

Oncology Drug Research, Development, and Manufacturing

In the early stages of human development, much of our time was spent battling hunger and plagues. However, with the gradual accumulation of civilization and the successive iterations and leaps in technology, most countries and regions around the world today seem to have escaped the existential threat of hunger. Yet plagues have never truly disappeared; we still face the threat of viruses.

In recent years, outbreaks of a series of viruses—including swine flu, Ebola, and the novel coronavirus—have inflicted immense destruction and harm on humanity. In 2020, a year marked by numerous "black swan" events, we once again faced significant uncertainty about the future. As critical assets in humanity’s fight against disease, pharmaceuticals and the pharmaceutical industry have remained indispensable. With the rising likelihood of infectious disease outbreaks, the importance of this sector has become more pronounced than ever before.

Pharmaceutical giants have always been at the forefront of human disease research, and their massive scale inevitably requires them to shoulder this responsibility. Heavy is the head that wears the crown; if pharmaceutical giants fail to remain fully vigilant and consistently at the forefront of the fight against diseases, failure is inevitable.

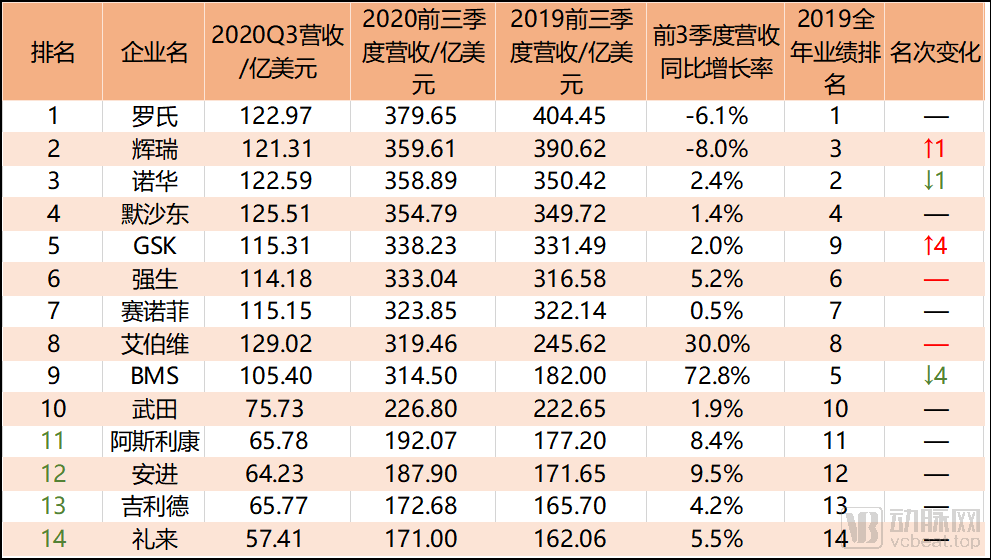

By compiling and organizing the financial data of pharmaceutical giants for the first three quarters of 2020, VCBeat has ranked the top ten pharmaceutical companies by revenue (with non-pharmaceutical business data excluded for Roche, Merck & Co., and Johnson & Johnson due to their significant non-pharmaceutical operations). Furthermore, this report analyzes and summarizes these top ten companies from perspectives such as R&D pipelines (innovation index) and news reviews, aiming to provide readers with insights into the strategic layouts implemented by the world’s top 10 pharmaceutical giants from early 2020 to date (January 1, 2020 – December 9, 2020), thereby offering food for thought.

(Data source: Q1-Q3 2020 financial reports of major pharmaceutical companies)

Around October 2020, pharmaceutical giants successively announced their Q3 financial reports, clearly revealing their performance for the first nine months.

As shown in the table above, although there were slight adjustments in the rankings of the top 10 pharmaceutical companies, overall, these companies largely maintained their top-10 positions in the cumulative performance for the first three quarters of this year compared to their rankings last year.

Due to the global spread of the COVID-19 pandemic, the related businesses and R&D pipelines of various pharmaceutical companies have been affected to varying degrees. However, judging from the financial data of these pharmaceutical companies in the first three quarters of 2020,Among the top ten pharmaceutical companies by revenue, all except Pfizer and Roche reported year-on-year growth, with these two experiencing a decline in performance compared to the same period last year.

RocheThe decline in performance was primarily due to the impact of the COVID-19 pandemic, which led to a significant drop in outpatient and inpatient visits.In addition, Roche’s “three flagship products” (bevacizumab, rituximab, and trastuzumab) experienced a significant decline in performance due to competitive pressure from biosimilars. However, Roche’s multiple sclerosis drug Ocrevus, breast cancer drug Perjeta, PD-L1 inhibitor Tecentriq, and new hemophilia treatment Hemlibra demonstrated robust growth momentum.

PfizerThe decline in revenue for the first three quarters was primarily due to a reversal in forward-looking procurement demand from the public, a downturn in retail operations, and the termination of certain contracts in the United States. However, given the strategic prioritization of COVID-19 vaccines,The RNA-based COVID-19 vaccine product, developed in collaboration between Pfizer and BioNTech, has currently received emergency use authorization from the FDA and is expected to begin administration this week.This first-mover advantage means that Pfizer, relying solely on its COVID-19 vaccine, has reaped substantial profits.

In recent years, Pfizer has broken away from its long-standing business-oriented management structure and shifted toward a regionally oriented management framework.This initiative aims to address a volatile market, changes in policies and regulations, and the integration of business lines. Pfizer CEO Albert Bourla publicly stated mid-year that “despite the pandemic-induced decline in company performance, approximately 25–30 products are expected to gain approval before 2022, with 15 of them poised to become blockbusters. Pfizer’s new organizational structure is projected to deliver higher and more sustainable revenue growth beyond the 2020 transition period.”

Two other pharmaceutical companies worth noting are AbbVie and BMS.These two companies achieved year-on-year performance growth of 30.0% and 72.8%, respectively, in the first three quarters of 2020, demonstrating remarkable results.

SelfAbbVieAbbVie’s sales revenue surged, driven by the completion of its full acquisition of Allergan in Q2 and the strong recovery of its aesthetics portfolio.Achieved sales of up to $12.902 billion in Q3, a year-on-year increase of 52.1%, becomingThe Undisputed Performance King of Q3 2020.If this trend continues, AbbVie may still have a chance to improve its ranking by the end of 2020.

Having acquired the massive Celgene and holding the highly promising Opdivo,BMSBecame the company with the most rapid growth momentum in the first three quarters of 2020,It comes as no surprise. With substantial financial resources, BMS announced in mid-November that it had completed the all-cash acquisition of MyoKardia for $13.1 billion, aiming to strengthen its cardiovascular drug business and expand its pipeline of candidate drugs with significant market potential.

Currently,With more than 20 clinical trials of Opdivo still ongoing, if combined with its own Yervoy or other IO pipeline drugs to achieve better efficacy, Opdivo still has the possibility of surpassing Keytruda in certain indications.BMS appears to be striving to recapture its former glory.

IDE Pharma is a pharmaceutical consulting firm based in San Francisco, USA. Each year, the firm releases an Innovation Index ranking for pharmaceutical companies—the Top 10 Innovative Pharmaceutical Companies.

Comparison of IDE Pharma’s Top 10 Innovative Pharmaceutical Companies of 2020 with the Top 10 by Revenue in the First Three Quarters of 2020

As shown in the table above, we can observe that:Only eight of the top ten pharmaceutical companies by revenue in the first three quarters of 2020 made it onto the 2020 Top 10 Innovative Pharmaceutical Companies list, with significant changes in their rankings; BMS and AbbVie did not appear in the top ten of the innovation list.AstraZeneca and Eli Lilly, which ranked 11th and 14th respectively in revenue for the first three quarters of 2020, placed 2nd and 10th respectively on the 2020 Top 10 Innovative Pharmaceutical Companies list.

This suggests, to some extent, that there is no strong direct linear correlation between robust revenue performance and a high innovation index. Nevertheless, as the absolute trump card for pharmaceutical companies, innovation capability remains a critical factor that cannot be overlooked.Currently, enterprises with strong innovation capabilities are highly likely to achieve leapfrog advancement over their former competitors in the future.

Regarding Roche’s ascent to the top spot, IDE Pharma stated:Roche’s outstanding performance in clinical diagnostics and precision medicine, its innovative partnerships, and its digital transformation are key reasons for its leading position.Such examples include the collaboration with Illumina, the FDA approval of its FoundationOne Liquid CDx pan-cancer liquid biopsy test, the CE marking of the AccuView SugarView application, the development of the COBAS platform integrated with laboratory management applications, and the launch of automated digital pathology algorithms.

AstraZeneca and Eli Lilly, which did not rank among the top ten in revenue for the first three quarters of 2020, are also worth special mention.

IDE Pharma stated that AstraZeneca has consistently performed well in leading “innovative partnerships,” recently establishing strong collaborations with a series of AI and data analytics-focused companies, including RenalytixAI, DeepMatter, and Eko. Meanwhile, AstraZeneca has also launched and leveraged various small-scale digital innovations, including mobile applications and digital platforms, to provide direct support for patients and clinical trial operations.

AstraZeneca has also demonstrated its continued commitment to investing in the future of digital health, pledging to collaborate with or invest in multiple “incubation hubs.” These deals include investments in numerous accelerator programs or direct collaborations with global tech startups.Multi-faceted innovation initiatives placed AstraZeneca second only to Roche on the 2020 Innovation List.

Eli Lilly primarily secured its spot in the Top 10 Innovative Pharmaceutical Companies due to its innovative performance in COVID-19 and advancements in digital technology.It is understood that Eli Lilly was the first company to announce and initiate research on an antibody therapeutic for COVID-19. The company is also seeking FDA approval for Olumiant as a contingency measure. In addition to these initiatives, Eli Lilly has launched multiple digital and in-person patient assistance programs, including a mobile research unit serving elderly patients, an insulin supply program, and an AI platform that automates adverse event reporting for clinical trials during the pandemic.

By partnering with Dexcom, Eli Lilly has developed a personalized insulin delivery system and software analytics capabilities to alleviate the burden of diabetes for patients. In terms of manufacturing, Eli Lilly is collaborating with Strateos to launch an innovative remotely operated robotic cloud laboratory in San Diego, making it one of the first facilities of its kind to enable remote research.

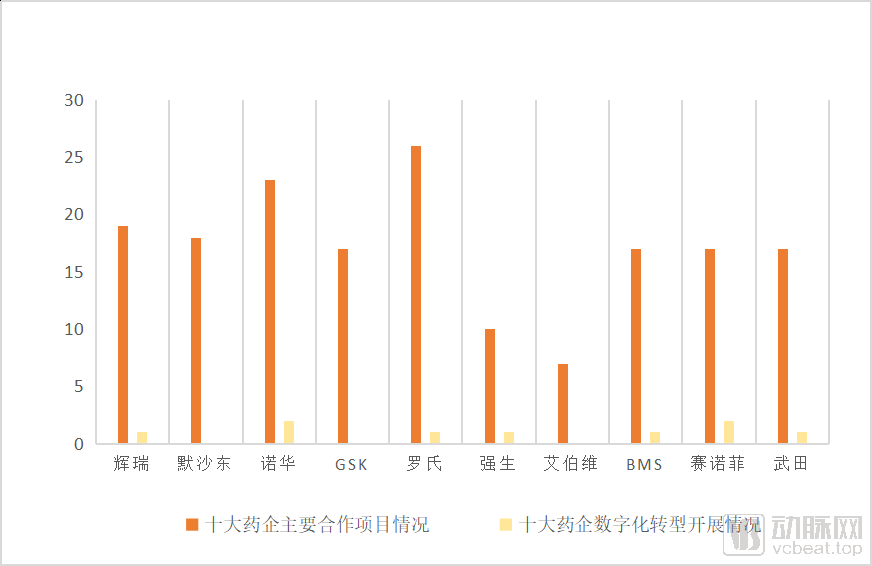

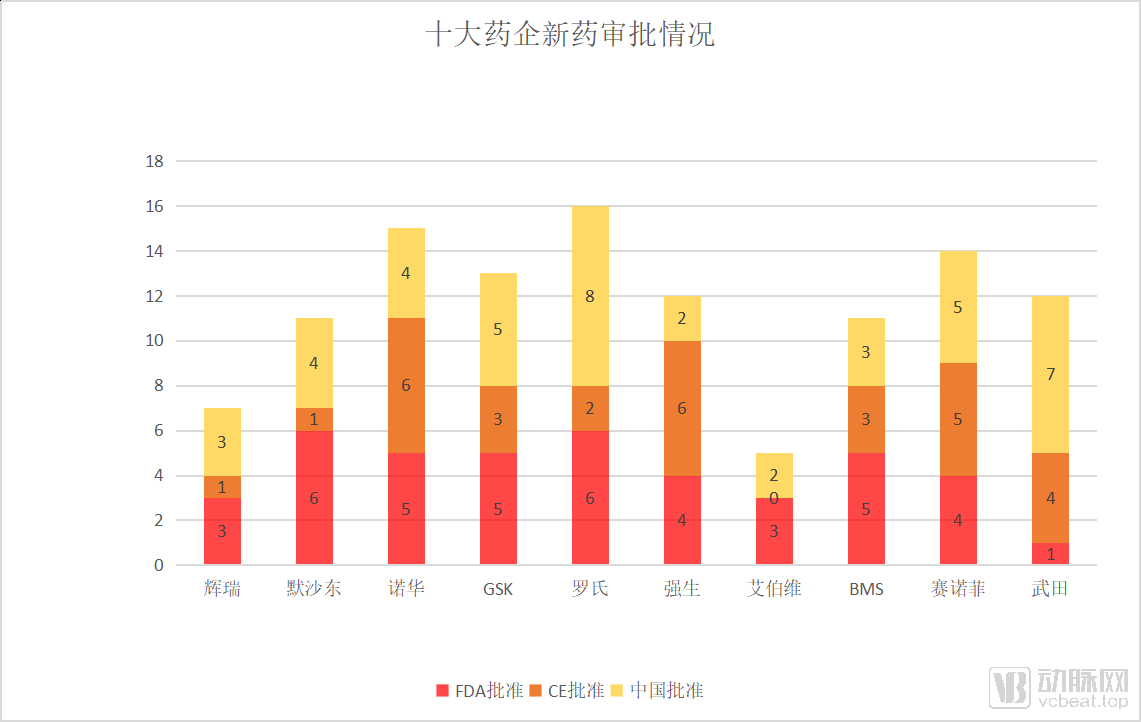

As IDE Pharma’s innovation index is primarily calculated based on pharmaceutical companies’ digital layouts, technological innovations, clinical trial performance, and partnerships, VCBeat has compiled and visualized news and information from January 2020 to the present regarding collaborative initiatives, digital transformation, and new drug approvals for the top 10 pharmaceutical companies by revenue in the first three quarters of 2020. This intuitive graphical representation may help readers gain a clearer understanding of the reasons behind the disparity between the top 10 companies by revenue and the top 10 by innovation.

(Chart by VCBeat; data source: Dongmai Cheng Database)

(Statistics of Major Events from January 1, 2020 to December 9, 2020)

(Chart by VCBeat; data source: Dongmaicheng Database)

(Statistics of Major Events from January 1, 2020 to December 9, 2020)

As can be seen from the data charts,Roche ranks among the top ten pharmaceutical companies in terms of partnerships, technological innovation, digital transformation strategies, and new drug approvals, making it the undisputed king of innovation.As for AbbVie and BMS not appearing in the Top 10 Innovation List, clues may be found in their digital transformation and new drug approval status. Due to AbbVie’s acquisition of Allergan and BMS’s acquisition of Celgene, their robust product pipelines have provided strong support for their respective revenues. Their inclusion in the Top 10 Revenue List, like other pharmaceutical giants, is driven by their substantial corporate scale.

However, it must be clear that the competition among industry giants is intensely ongoing at all times. It is the ability to meet the latest challenges, deploy forward-looking strategic plans and actions, and actively keep pace with the times that will determine who ultimately prevails.

The COVID-19 pandemic marked another arduous battle between humanity and viruses. For the top pharmaceutical giants commanding the most advanced R&D resources, it also served as a major test. Facing the same challenge, competition hinged not only on scale but also on all critical elements of successful corporate operations: talent, efficient management across all levels and departments, strong collaborative relationships both between companies and among internal teams, and strategic deployment by senior leadership. Speed and quality were the keys to victory.

(Data source: VCBeat Orange Database)

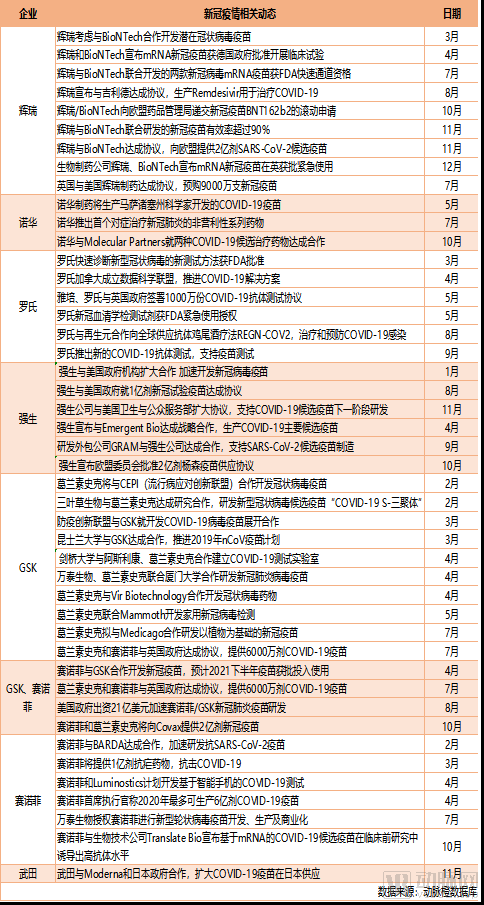

(Statistics of Major Events from January 1, 2020 to December 9, 2020)

Most top pharmaceutical companies have either conducted independent research or are collaborating with other organizations to develop COVID-19 vaccines.Currently, pharmaceutical companies such as Pfizer, Novartis, Roche, Johnson & Johnson, GSK, and Sanofi have all joined the vaccine pipeline development, with their candidates at various stages of clinical trials.As pharmaceutical giants face mounting pressure, former rivals are transforming into collaborators, sharing not only specialized expertise but also validated research and infrastructure repositories.

For example, Sanofi partnered with Translate Bio, leveraging Sanofi’s vaccine expertise in combination with Translate Bio’s mRNA platform, to develop several COVID-19 vaccine candidates.

Other companies collaborate with government agencies or organizations to accelerate their research.

Johnson & Johnson is collaborating with the Biomedical Advanced Research and Development Authority (BARDA) to develop a vaccine candidate; in February, GSK announced that it would partner with the University of Queensland in Australia, providing access to its vaccine adjuvant platform. Recently, GSK has also entered into a related collaboration with Xiamen Innovax Biotech Co., Ltd.

Pfizer, in collaboration with BioNTech, developed the RNA-based COVID-19 vaccine candidate BNT162b, making them the first pharmaceutical company to report successful data from large-scale clinical trials of a coronavirus vaccine.On November 18, Pfizer officially announced the results of its Phase III clinical trial: BNT162b demonstrated a 95% efficacy rate in preventing COVID-19 infection, with no serious side effects. On December 3, the UK health authorities granted emergency use authorization for this vaccine, making it the first vaccine to be launched globally. Immediately following this,On December 11, the FDA granted emergency use authorization for Pfizer’s COVID-19 vaccine, with vaccinations to commence in the near future.

Although reports of deaths and cases of facial paralysis in Pfizer’s vaccine trials have caused considerable public alarm, the FDA responded in its vaccine report that the incidence of these events does not exceed the expected rate in the general population. The rates of death and facial paralysis were similar to those observed in age-matched individuals from the general population, indicating no evidence of vaccine-related safety issues.

Currently,Two vaccines have entered the FDA review stage: one jointly developed by Pfizer and BioNTech, and the other by Moderna.

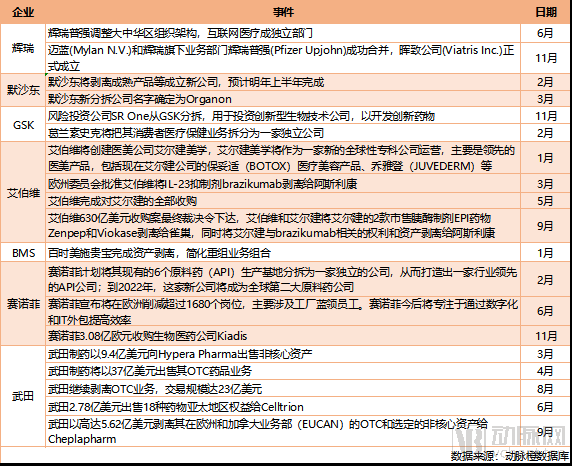

In recent years,To focus on the more profitable innovative drug business, major pharmaceutical companies have been continuously selling off or spinning out their lower-margin divisions.Examples are too numerous to count.

Novartis had formed a consumer health joint venture with GlaxoSmithKline (GSK) in 2015. Due to the low profit margins in this segment, Novartis sold its entire stake to GSK for $15 billion in 2018. In November 2019, Sanofi disclosed that it was formally considering spinning off its consumer healthcare division to focus on specialty medicines, vaccines, and generic drugs.

Similarly,Since the beginning of 2020, several pharmaceutical giants have announced plans for business spin-offs:

February 5,Merck & Co.Announced the spin-off plan: the oncology, in-hospital products, vaccine, and animal health businesses will be retained, while a new company comprising women’s health products, mature products, and biosimilars will be established and listed independently, with completion expected in the first half of 2021;

February 5,GSKAnnouncement of Spin-off Plan: Within the next two years, GSK will split into two separate corporate entities: one focused on pharmaceuticals and drug development, and the other dedicated to consumer health products; GSK estimates that by 2022, the company will achieve annual cost savings of £700 million and improve operational performance.

February 24,SanofiAnnounced the consolidation of its six active pharmaceutical ingredient (API) manufacturing sites in Europe to establish an independent API company;

November 16,PfizerSuccessfully spun off its Pfizer Upjohn generics business and merged it with Mylan, officially establishing Viatris Inc.

(Data source: VCBeat Orange Database)

(Statistics of Major Events from January 1, 2020 to December 9, 2020)

It is worth noting that,The underlying rationale behind Takeda’s asset divestiture is not merely to boost profit margins and enhance shareholder value; rather, it stems from a deeper need to alleviate the heavy financial burden resulting from the substantial expenditures incurred in acquiring Shire.In January 2019, Takeda acquired Shire, a giant in the field of rare diseases, for $62 billion. To cope with the heavy financial burden behind this huge payment, Takeda began to cut costs significantly through measures such as layoffs and selling non-core assets.

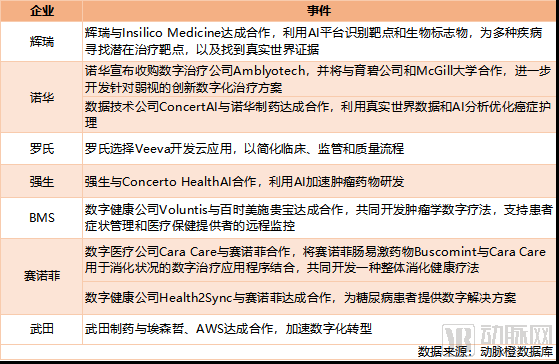

With the advent of the big data era, digital technologies are reshaping the pharmaceutical industry, and the wave of digital transformation in this sector has arrived.

Top 10 Pharmaceutical Companies’ Digitalization Initiatives in 2020 (Key Events from January 1, 2020 to December 9, 2020)

In pursuit of new business growth drivers, an increasing number of large pharmaceutical companies have strategically deployed digital technologies, applying them extensively across drug research and development, clinical trials, patient services, marketing, and internal management.and achieved some results.

In today's internet era,Digital technology has reached a sufficient level of maturity.Whether it is artificial intelligence, big data, or mobile internet, all have undergone years of development and seem to be at the stage where they should be applied to specific scenarios.

Secondly, as the costs and risks associated with new drug development and clinical research continue to rise, the industry requires new tools to transform its traditional production models; this constitutes the internal driving force for “change” within the sector, whileThe application of digital technologies in digital marketing and patient services will help the industry address issues such as accessibility and satisfaction.A New Business Order Is Being Established.

VCBeat believes that the digital transformation of pharmaceutical companies will see significant changes in two major directions in the future.

On the one hand, pharmaceutical marketing— Face-to-face communication will be replaced to some extent by an increasing volume of digital sales activities, such as those conducted by Digital Medical Science Liaisons (EMSLs); the integration of digital tools will enable more targeted services for physicians and patients;Another aspect lies in the mining of medical evidence—Digital approaches can be employed to enhance efficiency from data collection to evidence generation, thereby reducing the overall cost of drug development.

However, during the digital transformation of pharmaceutical companies, there are some common issues that need attention: such as data fragmentation, difficulty in governance, and lack of integration among business systems. These situations require further exploration and response from pharmaceutical enterprises.

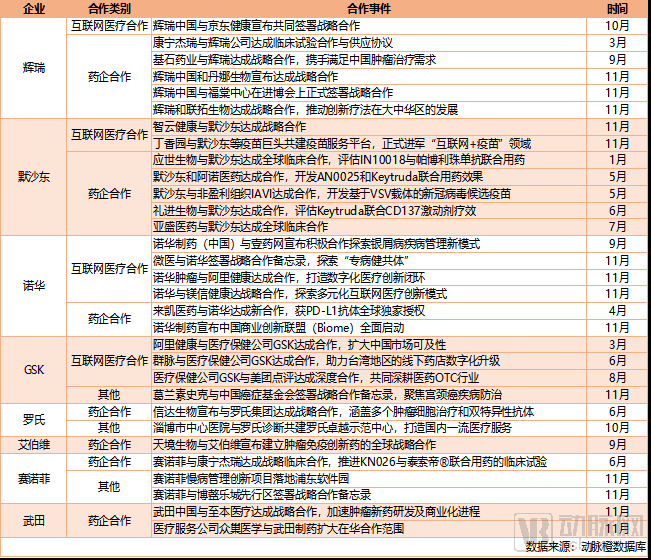

As Internet healthcare sweeps the globe, how do traditional pharmaceutical giants view this transformation? The answer is: Embrace innovation.

Top 10 Pharmaceutical Companies’ Collaboration Strategies in China in 2020 (Key Events from January 1, 2020 to December 9, 2020)

In fact, as early as 2010, or even earlier, pharmaceutical industry leaders had already taken action, and to date, an increasing number of traditional pharmaceutical companies have joined in.

In recent years, the development of internet healthcare in China has continued to grow. Under the impact of the pandemic, residents' offline activities were restricted, making internet healthcare one of the industries experiencing rapid growth strongly driven by the pandemic. As a result, pharmaceutical giants have frequently taken actions in cooperation with domestic internet healthcare platforms, hoping to capture a share of the market.

Taking GSK as an example, on March 30, GSK partnered with Ali Health to announce the launch of Trelegy, a triple-combination inhaler for the maintenance treatment of chronic obstructive pulmonary disease (COPD), on the Ali Health platform. Through this collaboration, GSK aims to leverage Ali Health’s online platform resources to further expand the accessibility of Trelegy in the Chinese market. In June, GSK collaborated with Qunmai to digitally upgrade over 8,000 offline pharmacies in the Taiwan region, thereby fully activating store sales capabilities. Subsequently, in August, GSK entered into a comprehensive partnership with Meituan, aiming to co-establish a pharmaceutical O2O (Online-to-Offline) model based on local life services, providing consumers with a wider variety of products and more convenient medication purchasing services.

It can be seen that,Pharmaceutical giants are actively exploring multidimensional approaches to leverage “Internet Plus” in order to strengthen their competitive edge.

Furthermore, we can also observe thatPharmaceutical giants have also engaged in high-density collaborations with domestic innovative pharmaceutical companies, hospitals, and medical industrial parks in other areas, such as new drug research and development, commercialization licensing of pharmaceuticals, and innovative disease management programs.This not only demonstrates that the R&D capabilities of Chinese biopharmaceutical companies are gradually gaining recognition from global pharmaceutical giants, but also underscores the strategic importance of the Chinese market to these industry leaders. As a coveted high ground fiercely contested by foreign enterprises, the Chinese market harbors vibrant development prospects and countless opportunities for growth.

Based on its performance in the first three quarters, AstraZeneca missed out on a spot in the top 10 list by a margin of just one position. However, VCBeat noted that during the “Double 12” shopping festival, AstraZeneca engaged in a significant acquisition spree, making headlines as another major development before the year’s end.

On December 12, AstraZeneca announced the acquisition of Alexion Pharmaceuticals for $39.4 billion (approximately RMB 257.883 billion), including $13.5 billion in cash and $25.9 billion in AstraZeneca ADSs.

Notably, AstraZeneca’s acquisition price for Alexion was $175 per share, representing a 44.65% premium over Alexion’s closing stock price of $120.98 on December 11. Based on 2019 revenue, AstraZeneca ranked eleventh among global pharmaceutical companies with $24.384 billion; adding Alexion’s $4.991 billion would propel AstraZeneca into the top ten. This means thatUpon completion of this merger, the rankings of the top 10 pharmaceutical companies by global revenue may be reshuffled.