Shandong Branden Medical's IPO Withdrawn: Domestic Leader in PICC Devices Halts Sci-Tech Innovation Board Listing

Branden

Medical Device Manufacturer

Source: Wutong Shuxia V

On September 4, the Shanghai Stock Exchange (SSE) announced its decision to terminate the review of Shandong Branden Medical Devices Co., Ltd.’s initial public offering (IPO) on the STAR Market. The direct reason was the withdrawal of the IPO application and sponsorship by the company and its sponsor, Guojin Securities. The company’s IPO application was accepted on October 19, 2022, and it had completed two rounds of inquiry responses as of August 3, 2023. The company had planned to raise RMB 760 million through this IPO.

I. Net profit was average, government subsidies were relatively high, and the net profit after deducting non-recurring gains and losses in 2023 was less than RMB 25 million.

The company is a national high-tech enterprise dedicated to applying medical material modification technologies to implantable and interventional medical devices. It is the first domestic company to obtain the Class III medical device registration certificate for a domestically produced Peripherally Inserted Central Catheter (PICC).

The company’s main products are medical devices in the fields of vascular access and neurosurgery. According to the "Classification of Strategic Emerging Industries (2018)," the company falls under "4.2 Biomedical Engineering Industry" within the category of "4.2.2 Manufacturing of Implantable and Interventional Biomaterials and Devices."

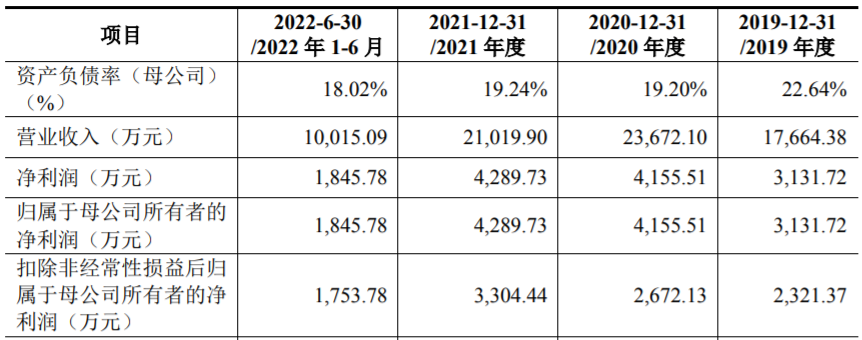

From 2020 to 2021, the company's main business revenue was RMB 176.2625 million, RMB 175.5354 million, and RMB 208.2556 million, respectively.

According to the latest reply disclosure, based on the lower of the net profit attributable to owners of the parent company before and after deducting non-recurring gains and losses, the company's net profit attributable to owners of the parent company in 2023 was RMB 23.5565 million, and its operating revenue in 2023 was RMB 201 million.

The actual controllers of the Company are Zhang Haijun and Guo Haihong. Zhang Haijun and Guo Haihong are spouses, and they collectively hold 49.03% of the shares in the Issuer, both directly and indirectly.

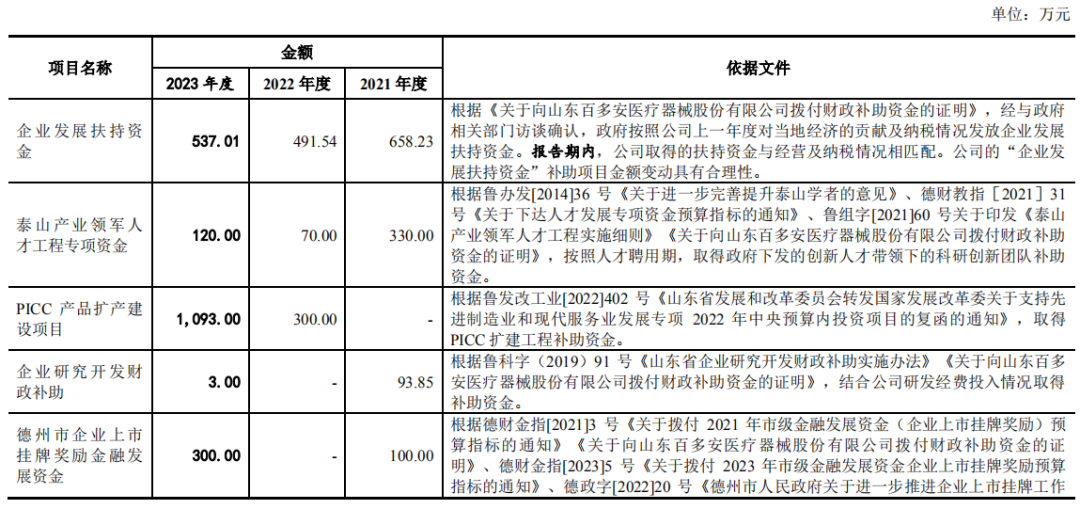

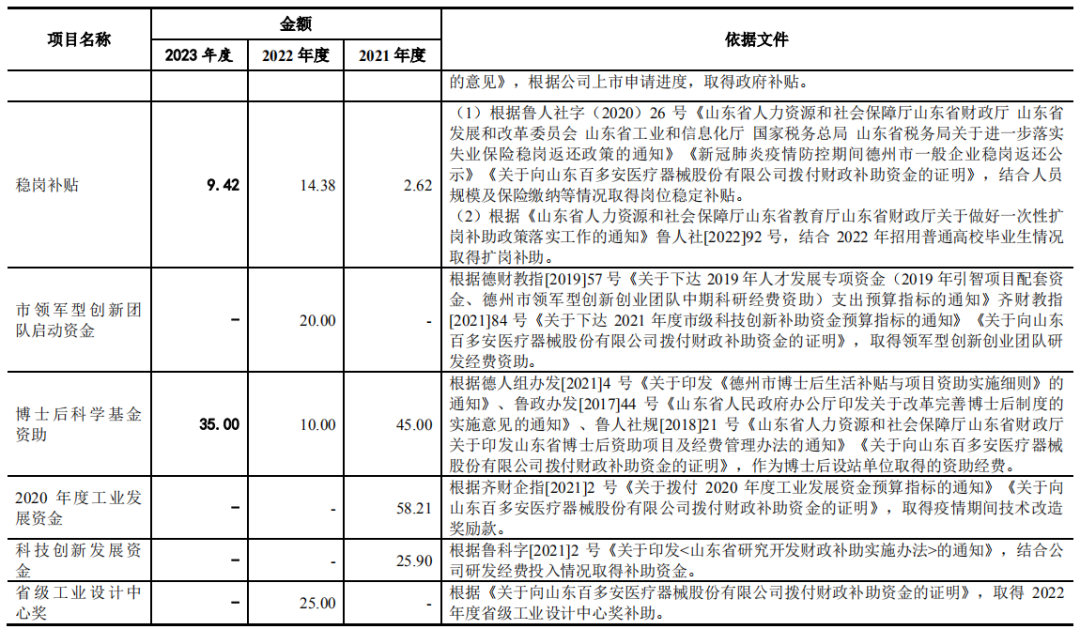

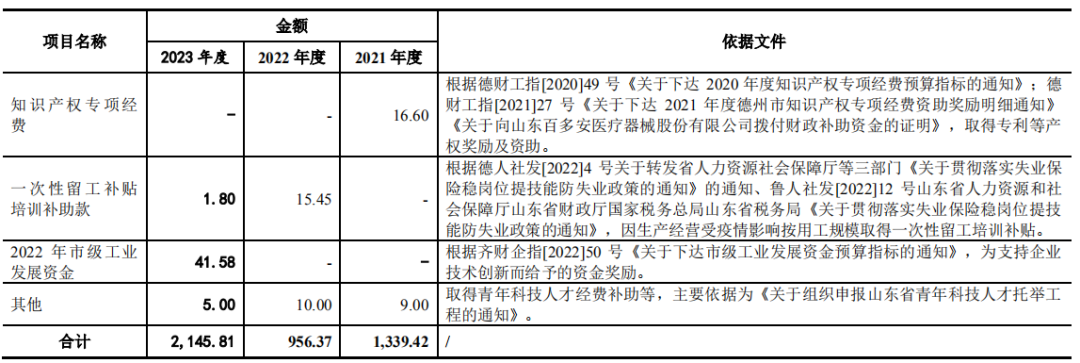

2021-2023, the government subsidies obtained by the company are as follows:

II. PICC Products: Ranked No. 1 Domestically, but with a Limited Market Size

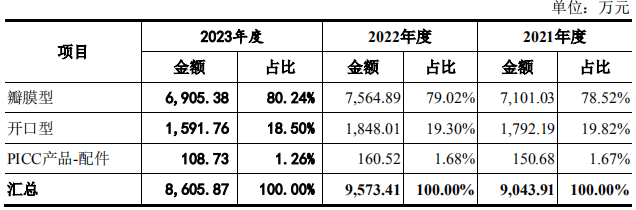

During the reporting period, the revenue composition of the Company's PICC products was as follows:

As one of the Company’s core products, PICC products generated sales revenues of RMB 90.4391 million, RMB 95.7341 million, and RMB 86.0587 million during the reporting period, with sales volumes of 135,600 sets, 152,700 sets, and 147,300 sets, respectively.

According to QYResearch’s “Global and China Peripherally Inserted Central Catheter (PICC) Market: Current Status and Future Development Trends, 2023–2029,” since 2018, the Company has achieved steady growth in market share alongside increased product sales, with its market share rising from 16.54% in 2018 to 21.02% in 2022. Meanwhile, the domestic PICC market remains predominantly dominated by foreign enterprises represented by Bard Medical. Leveraging its prominent technological advantages and cost-effective products, the Company has gained widespread clinical recognition and ranks first among domestic enterprises in terms of market share.

Based on the statistics of PICC usage volume in China as reported by QYResearch, combined with factors such as the increased product penetration rate driven by post-centralized procurement price reductions and the utilization of tunneling needles following the popularization of tunneled PICC technology,It is projected that by 2030, the usage volume of PICCs in China will reach 2.8406 million sets, corresponding to a market size of approximately RMB 2.18 billion.

In addition to the research report issued by QYResearch, which proves that the company's PICC market share ranks first among domestic brands, according to the survey conducted by the Medical Plastics Committee of the China Plastics Processing Industry Association, the company's market share in the national PICC segment is second only to Bard Medical, ranking first among domestic brands.

According to QYResearch’s “Global and China Cranial External Drainage System Market Status and Future Development Trends 2023-2029,” China’s sales volume of cranial external drainage systems reached approximately 518,600 units in 2022. Among them, Medtronic, Branden, and Dazheng Medical sold 167,200 units, 72,300 units, and 62,400 units respectively, with corresponding market shares of 32.24%,13.94%, 12.03%. The company's market share remained generally stable.

The Company’s self-calculated market share of 13.81% does not differ materially from the 13.94% reported in research data provided by an independent third party, demonstrating that the Company’s market share calculation is objective and reasonable.

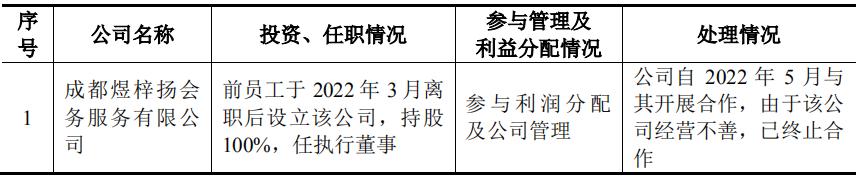

III. Some marketing service providers are held or managed by employees, former employees, or their relatives

According to the prospectus: (1) Selling expenses and administrative expenses increased significantly in 2021; (2) Selling expenses mainly consisted of compensation for sales personnel and promotion fees, with market promotion conducted either by the issuer itself or through entrusted promotion service providers; (3) A relatively high proportion of the issuer’s employees and their relatives held equity interests or positions in market promotion service providers, and rectification measures were implemented in respect of these matters in the first quarter of 2022.

According to the response to the first round of inquiries, some of the Issuer’s marketing service providers are held or managed by employees, former employees, or their relatives, with the related expenses accounting for a relatively high proportion; the Issuer engages marketing service providers to carry out promotional activities and settles the marketing service fees based on the number of attendees.

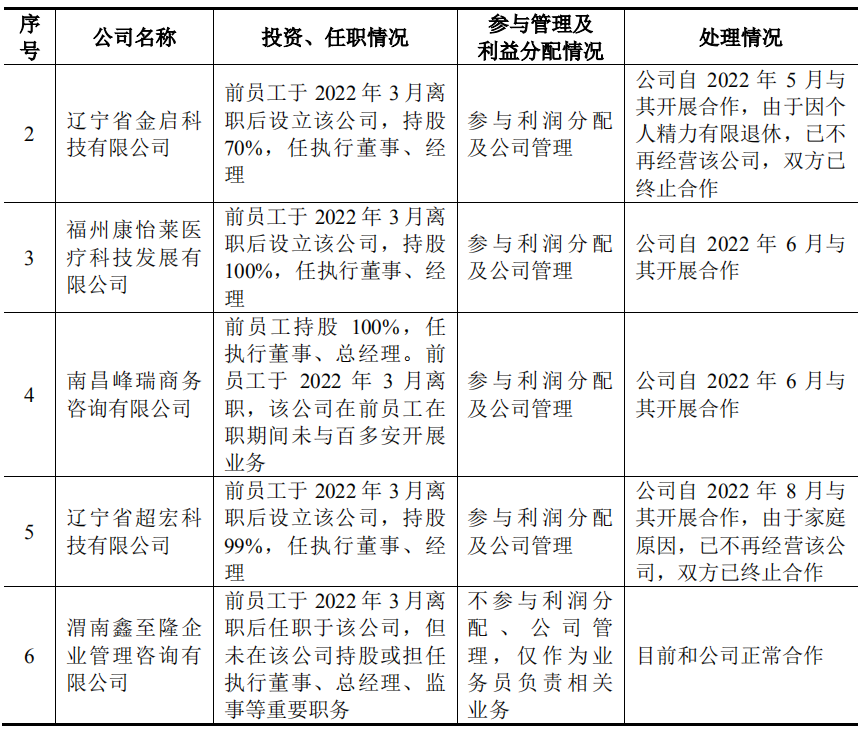

1. During the reporting period, there were isolated cases where individual employees held equity interests or positions in promotional service providers. Upon discovery, the Company immediately terminated its cooperation with the relevant service providers or required the employees to divest their equity interests or resign from their positions. The main circumstances are as follows:

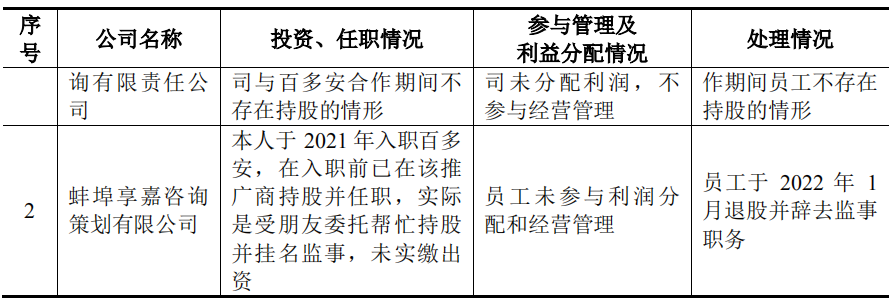

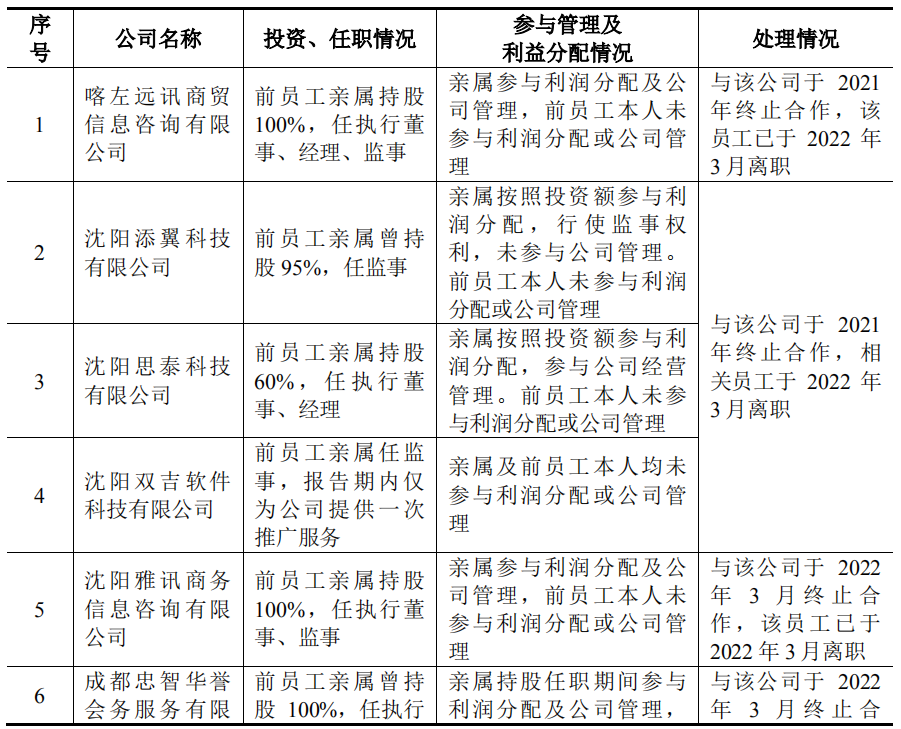

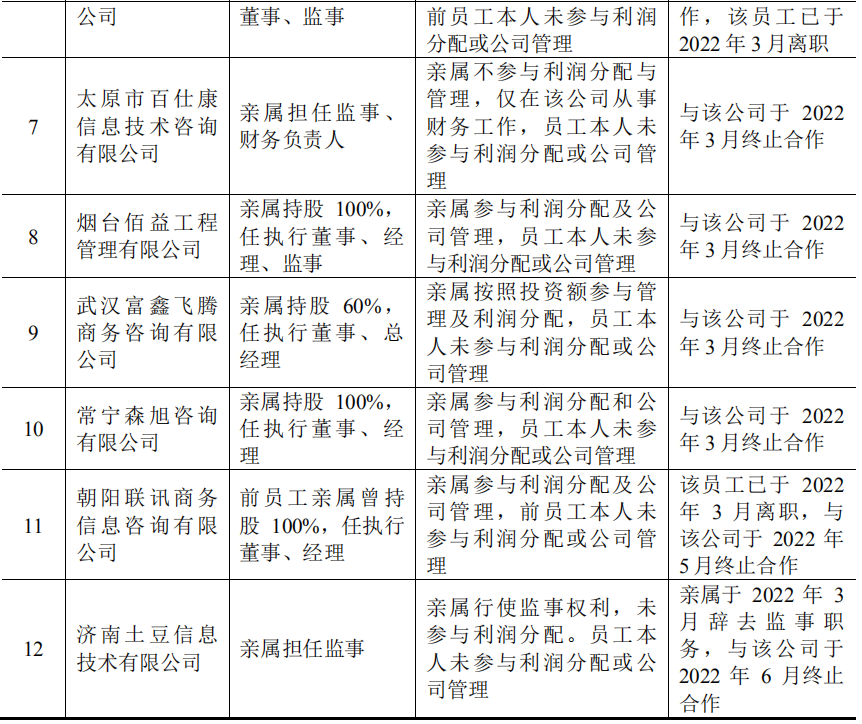

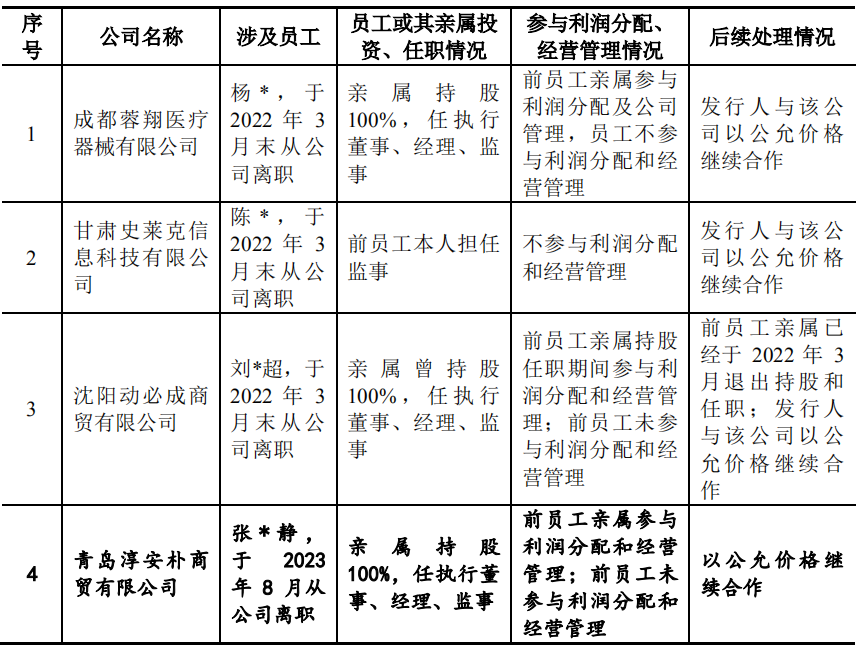

2. During the reporting period, there were instances where relatives of the Company’s employees held equity interests or positions in promotional service providers. The Company conducted a self-inspection and implemented corrective measures in the first quarter of 2022. Since April 2022, no such circumstances have existed. The main details regarding the involved promotional service providers are as follows:

3. Some former employees, after leaving the Company, established promotional service providers or joined such entities to provide promotional services to the Company. The Company cooperates with these related entities in accordance with unified management standards for promotional service providers, and the transaction prices are fair and reasonable. The main details of these related entities are as follows:

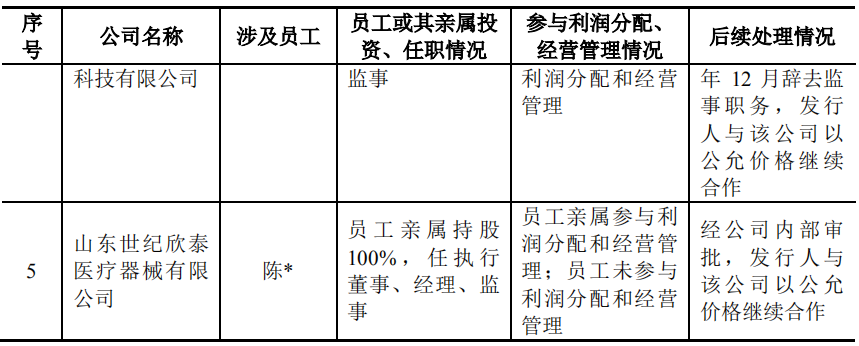

IV. Former or Current Employees Previously Held Equity Interests in Certain Distributors of the Issuer or Had Affiliated Relationships

1. Details of distributors in which former employees or their relatives held investments or positions during their employment and after their departure are as follows:

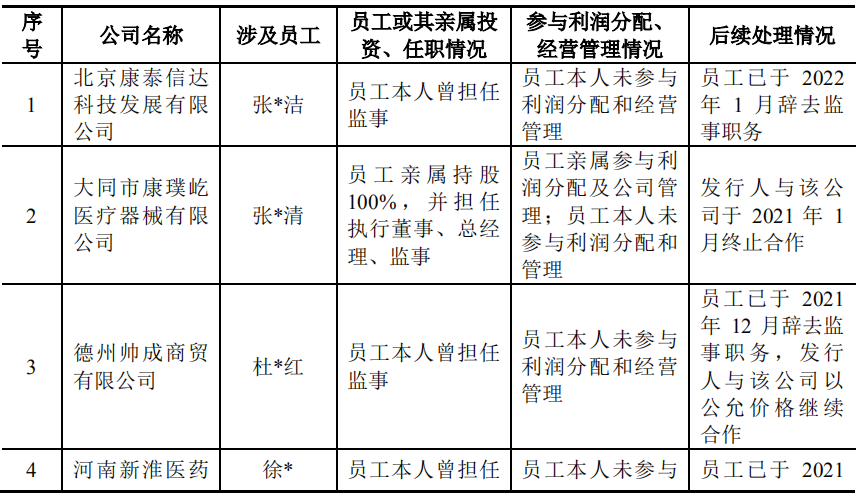

2. The distributors in which current employees or their relatives have invested or hold positions are as follows:

As of the date of this response, except for Shandong Shiji Xintai Medical Devices Co., Ltd., which continues to cooperate with the Company following internal approval, all other distributors affiliated with the Company’s employees have been regulated through measures such as the resignation of employees or their relatives from such distributors, the resignation of employees from the Company, or the termination of cooperation between the Company and such distributors. Since April 2022, the Company has not added any new distributors affiliated with its employees.

5. Distribution model accounts for approximately 99%, with dealer inventory balances drawing attention

According to the prospectus and application materials: (1) During the reporting period, approximately 99% of the Issuer’s revenue was generated through its distribution model, with revenue from the agency-based distribution model accounting for 14.67%, 14.87%, 10.43%, and 6.65% of total operating revenue, respectively; (2) Among the Issuer’s major customers during the reporting period, there were entities that served as both customers and suppliers, as well as individual natural persons.

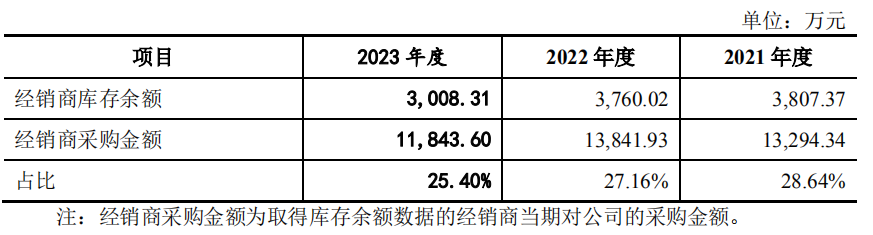

Based on the inventory balance data provided by distributors (the proportion of revenue corresponding to distributors who provided detailed purchase, sales, and inventory records accounted for 71.60%, 64.87%, and 69.04% of the total operating revenue, respectively), the overall inventory balances of distributors during each period of the reporting period were as follows:

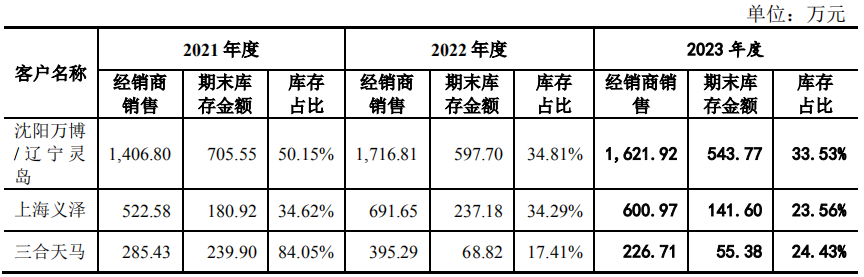

During the reporting period, the distributors with ending inventory balances exceeding RMB 2 million in a single period included: Shenyang Wanbo Tonghui Medical Devices Co., Ltd. and Liaoning Lingdao Trading Co., Ltd. (hereinafter collectively referred to as “Shenyang Wanbo/Liaoning Lingdao”), Shanghai Yize International Trading Co., Ltd. (hereinafter referred to as “Shanghai Yize”), and Beijing Sanhe Tianma Medical Devices Co., Ltd. (hereinafter referred to as “Sanhe Tianma”). The ending inventory and end-user sales situations of these distributors are as follows:

During the reporting period, distributors determined their year-end safety stock levels based on the current year’s sales volume and expected growth. Given the strong end-user sales performance of these distributors, they typically maintained higher inventory levels at year-end. In 2022, influenced by fluctuations in hospitalization numbers and surgical volumes, distributors appropriately reduced their year-end inventory levels. By the end of 2023, the aforementioned distributors achieved robust external sales; however, due to uncertainties surrounding the implementation timeline of the centralized procurement policy, their year-end inventory levels declined.

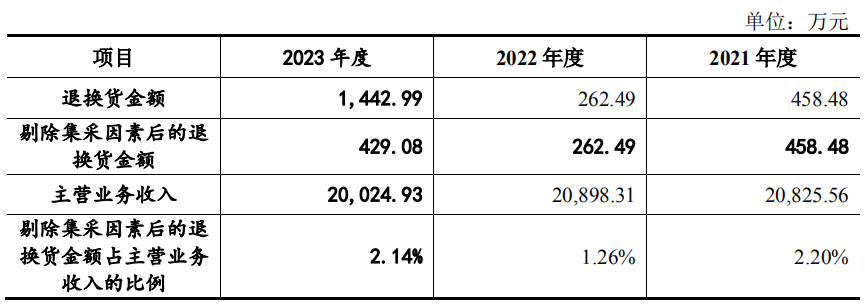

During each period of the reporting period, the issuer's distributors' return and exchange situations were as follows:

The amount of returns and exchanges was relatively high in 2023, primarily because the issuer, to ensure market stability during the transition period of centralized procurement and to maintain long-term cooperative relationships with end customers and distributors, coordinated with certain distributors to adjust their inventory products. After excluding the impact of centralized procurement, the company’s return and exchange amounts and their proportions were both small.

VI. Other Matters of Concern

1. According to the prospectus and application materials: (1) The Issuer and Rui'an Tai, which is controlled by one of the actual controllers, Zhang Haijun, both belong to the sub-sector of implantable and interventional medical devices, but there are significant differences in terms of treatment or application areas, etc., so they do not constitute horizontal competition; (2) According to the Medical Device Classification Catalog, the Issuer's central venous catheters and Rui'an Tai's balloon dilation catheters both belong to cardiovascular interventional devices within the category of neurological and cardiovascular surgical instruments; (3) During the reporting period, there was personnel movement between the Issuer and Rui'an Tai, and related-party transactions existed, such as leasing factory buildings and office spaces to Rui'an Tai, collecting and paying electricity bills on its behalf, purchasing materials, and making payments for goods on its behalf. There were overlaps in customers, raw material suppliers, engineering equipment suppliers, and service providers.

2. According to the application materials: The issuer distributed cash dividends of RMB 30 million, RMB 45.39 million, and RMB 20.3148 million in 2019, 2021, and January–June 2022, respectively, accounting for a relatively high proportion of the net profit for the corresponding periods.

3. According to the prospectus: (1) To facilitate expansion into international markets and enhance brand awareness, the Company was established as a Sino-foreign joint venture. At its inception, there were defects in capital contribution, instances of nominee shareholding, and failure to complete appraisal procedures for debt-to-equity conversions during its historical evolution; (2) During the reporting period, the Company failed to make social insurance and housing fund contributions for certain employees, and engaged Chengtong Human Resources Co., Ltd. to handle such contributions for some employees working in other locations; (3) During the reporting period, there were returns and exchanges of the Company’s core products, and in 2021, product certification renewals resulted in the batch scrapping of products; (4) The Company has not obtained title certificates for certain properties, resulting in defects in ownership rights. The Company holds multiple registration certificates for Class II and Class III medical devices. Publicly available information indicates that routine unannounced inspections by regulatory authorities identified general deficiencies related to the Company’s PICC products.

Pharmaceuticals | Biologics | ADC | mRNA | CAR—T | PD-1 | Medical Devices | Imaging | IVD | Cardiovascular | Orthopedics | Oral Cavity | Ophthalmology | Surgical Robot | Internet Healthcare| Hospital | CXO | Life SciencesStudy

In-depth Originality | Annual Review | Trend Analysis | Cross-Cycle Series | Stock Market Trends | Corporate News | Executive Updates | Pharmaceutical Financial Reports | Medical Device Financial Report | Blockbuster M&A | Strategic Spin-off | Executive Interview | Compensation | Policy Analysis | National Reimbursement Drug List (NRDL) Negotiations | DRG/DIP | Centralized Procurement | JPM | Latest News | CIIE | CMEF

Medical Device Rankings | Medtronic | Abbott | Johnson & Johnson Medical | Siemens Healthineers | BD | Stryker | GE Healthcare | Roche Diagnostics | Philips | Boston Scientific | Mindray Medical | United Imaging Healthcare | MicroPort | Lepu Medical | Weigao | Danaher | Thermo Fisher

Pharmaceutical Rankings | Pfizer | AbbVie | Roche Pharmaceuticals | Johnson & Johnson Pharmaceuticals | Merck & Co. | AstraZeneca | Bristol-Myers Squibb | Sanofi | Novartis | GlaxoSmithKline | Hengrui | BeiGene | CSPC | Innovent Biologics | Junshi Biosciences | Legend Biotech | I-Mab | CStone Pharmaceuticals | RemeGen | Zai Lab | WuXi AppTec | Qiming Venture Partners | Eli Lilly Asia