Why Did the Commercial Insurance Catalogue Fail in Its First Battle Despite the Million-Dollar Health Insurance Frenzy Over Innovative Drugs?

As we enter 2026, the implementation of the first "Commercial Health Insurance Innovative Drug List" (hereinafter referred to as the "commercial insurance list") is undoubtedly the top event of the new year for both the innovative drug industry and the commercial insurance industry.

However, the anticipated large-scale iteration wave of commercial insurance products has not emerged. Although惠民保 (HuiMinBao) programs in various regions have quietly responded to the commercial insurance innovative drug list by adjusting coverage rules, the side with a larger user base — million-dollar medical insurance plans — has remained surprisingly calm. VCBeat found that leading million-dollar medical insurance products such as 好医保 (Good Medical Insurance), 蓝医保 (Blue Medical Insurance), and 尊享e生 (Respectful Enjoyment e-Life) have not updated their related drug lists recently. In other words, the much-anticipated commercial insurance innovative drug list cannot be considered a success in its first attempt.

Commercial insurance has covered most of the catalog drugs.

Of course, the fact that网红险种 (popular insurance types) did not respond immediately does not mean that all innovative drugs in the commercial insurance catalog cannot be reimbursed.

In December 2025, the National Healthcare Security Administration and the Ministry of Human Resources and Social Security jointly released the first version of the commercial insurance catalog, which included five CAR-T cell therapy drugs such as Yikaida, six rare disease medications such as Gorining, two Alzheimer's disease treatments such as Leye Bao, and six anti-cancer drugs with novel targets within the reimbursement scope of commercial insurance.

Notably, the introduction of the first edition of the commercial insurance directory actually separates innovative drugs that are routinely admitted to hospitals and covered by medical insurance from some special innovative drugs. These two categories will follow different payment pathways in the future.

On the one hand, compared with conventional innovative drugs, the innovative attributes of listed innovative drugs are stronger, mostly featuring breakthrough innovations in mechanisms of action and drug modalities. In current clinical practice, these drugs are considered life-saving medications, primarily used for last-line treatments of serious diseases such as cancer. For instance, the five CAR-T cell therapy drugs that have drawn the most public attention represent a typical next-generation innovative treatment solution in the field of cancer therapy. While their efficacy is remarkable, their side effects are also very pronounced, and they are only approved for last-line treatment of specific blood cancers. On the other hand, before conventional innovative drugs enter the medical insurance system, they usually accumulate extensive long-term safety and real-world efficacy clinical data, and are mainly used in first-line or second-line disease treatments.

On the other hand, drugs listed in the catalog are constrained by complex preparation processes or limited applicable populations, resulting in very high pricing with little room for significant price reductions in the short term. For example, Revestive, used to treat short bowel syndrome, has an annual treatment cost as high as 350,000–500,000 RMB per year, while Leqembi, a wonder drug for early-stage Alzheimer's disease, also reaches an annual treatment cost of 180,000 RMB. The number of patients suitable for these drugs is limited, and if pharmaceutical companies lower the price, it will be difficult to cover the early R&D costs. In contrast, innovative drugs commonly included in China’s medical insurance system are mostly for common and frequently occurring diseases, allowing for a trade-off between price and volume to meet the inclusive and sustainable principles of medical insurance.

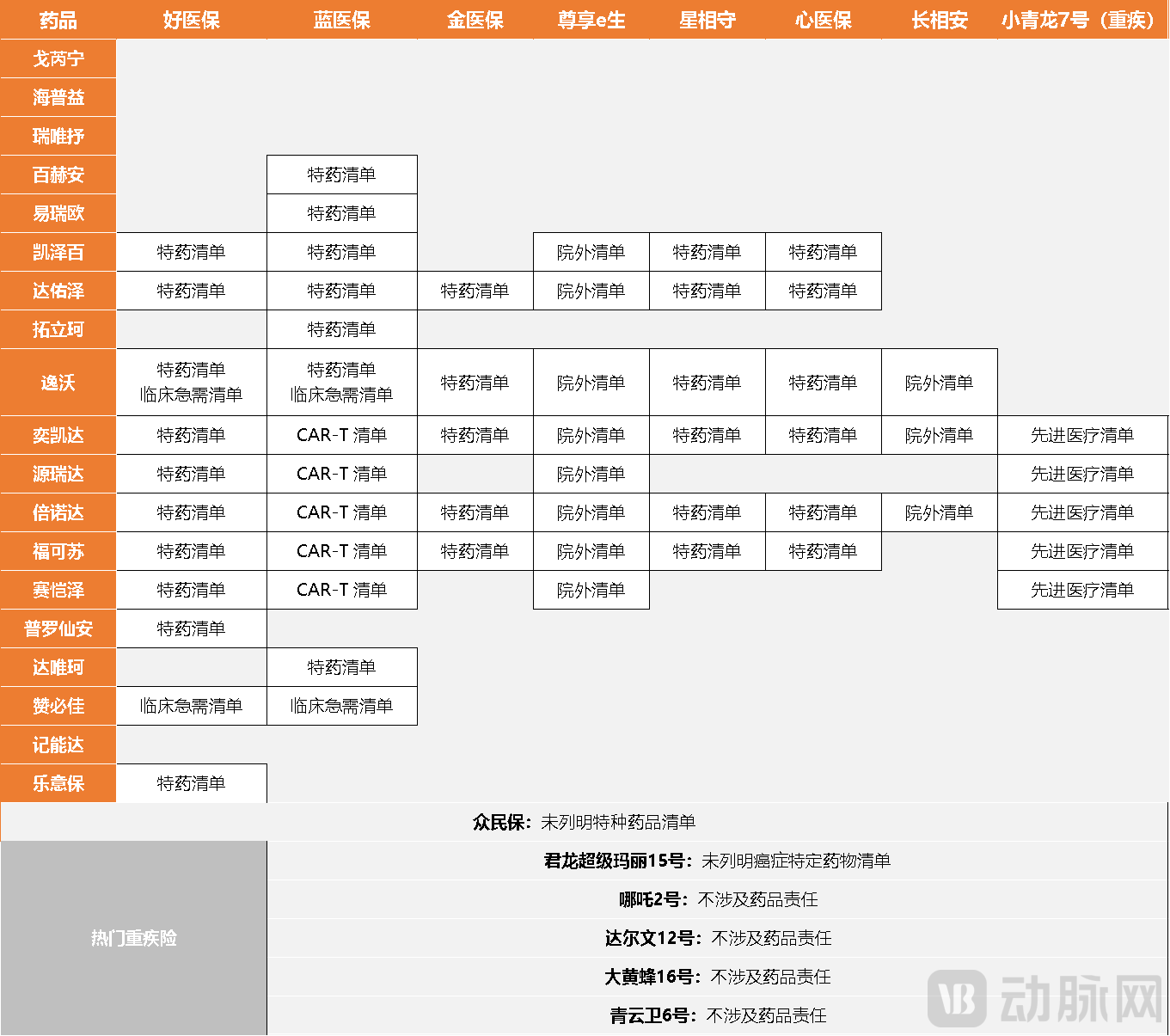

Although it is difficult to be covered by basic medical insurance in the short term, for the reimbursement of this part of the drug costs, commercial insurance has formed an independent liability category, namely, specific drug liability (hereinafter referred to as "special drug liability").VCBeat's inquiry into product manuals found that most drugs in the commercial insurance directory have been included in the reimbursement scope of previous versions of top-tier million-yuan medical insurances such as Good Medical Insurance, Blue Medical Insurance, Gold Medical Insurance, Enjoy E-Life, Star Guardian, Heart Medical Insurance, Long-term Peace, and some critical illness insurances.

Among the 14 popular commercial health insurance products surveyed by VCBeat this time, Blue Medicare covers 13 out of 19 innovative drugs in the directory, making it the insurance type with the most drug coverage. Good Medicare comes second, covering 11 drugs. Even EverPeaceful, which covers the least number of innovative drugs in the directory, proactively includes 3 out of 5 CAR-T drugs listed in the commercial insurance directory. Additionally, some critical illness insurances, such as Little Qinglong No. 7 and JunLong Super Mario No. 15, also incorporate certain commercial insurance directory drugs into their reimbursement scope through optional clauses, in addition to lump-sum payouts. For example, Little Qinglong No. 7 includes Yikaida, Yuanruida, Bennoda, Fuke Su, and Saikaize, five cell therapy drugs, in its reimbursement responsibility via an advanced medical list.

In practice, different million-dollar medical insurance policies categorize special drug coverage under various names of medical insurance benefits. For example, the special drug coverage of Good Medical Insurance is covered by specific pharmaceutical and device cost insurance benefits, external purchase pharmaceutical and device cost insurance benefits, etc., while the special drug coverage of Enjoy Life is covered by specific drug medical cost insurance benefits, advanced cancer therapy medical insurance benefits, etc. Although the reimbursement rules of specific insurance types vary, each million-dollar medical insurance policy has formed a relatively unified reimbursement principle for special drug coverage: zero deductible, full reimbursement, low out-of-pocket expense, and relatively strict claim requirements.

Amid the fierce homogenization competition in the million-dollar medical insurance market, the special drug coverage with constantly relaxed reimbursement rules has long become a battleground for insurers.

Innovative Drugs Trapped in Traffic

The inclusion of special drug coverage in million-yuan medical insurance for the first time occurred in 2018, when leading products first added "special drug coverage for malignant tumors," specifying dozens of common cancer drugs such as trastuzumab and paclitaxel on the special drug list, allowing reimbursement for the cost of purchasing these drugs outside of hospitals.

At that time, due to the concentrated emergence of innovative drugs such as targeted tumor therapies and immunotherapies, coupled with factors like the "drug cost ratio" assessment, the pain point of not being able to purchase specific new drugs in hospital pharmacies gradually became prominent. Premium medical insurance products like Zunxiang e-Sheng and Lan Yibao were quick to optimize their product designs, introducing the concept of special drug coverage, and reaped the first wave of traffic brought by these special drugs. Data shows that from 2018 to 2020, the number of participants in million-yuan medical insurance plans had a compound annual growth rate exceeding 50%.

In fact, when the million-yuan medical insurance was first introduced, it came with the label of "unrestricted by the social security directory," allowing reimbursement for out-of-pocket medications and imported drugs. However, the concept of "special drugs" in the early days was vague and included under "inpatient medical expenses," making it difficult to cover the costs of purchasing drugs outside the hospital. Subsequently, the special drug coverage of the million-yuan medical insurance continued to expand, and the constraints on reimbursement were gradually relaxed.

In recent years, with the advancement of China's national medical insurance DRG/DIP payment reform, hospitals have been more motivated to shift expensive drugs and consumables outside their premises in order to control costs. This has led to a surge in patients' demand for purchasing drugs outside the hospital, rendering early special drug lists insufficient. By 2025, on top of the special drug coverage, leading million-yuan medical insurance plans have competitively introduced outpatient drug purchase responsibilities without a restricted drug list.

The responsibility for purchasing drugs outside the hospital has overturned the rules of limiting drug lists and restricting medication use during hospitalization in specialty drug coverage. It proposes that as long as the prescribed drugs are reasonable and necessary, whether or not they are on a specific list, there is an opportunity for reimbursement, greatly enhancing the flexibility and scope of coverage.Breaking the restriction on purchasing drugs outside the hospital during hospitalization means that outpatient and emergency scenarios will allow reimbursement through million-yuan medical insurance for off-site drug purchases, whether for postoperative follow-up medications, or long-term outpatient medications for chronic or critical illnesses. At the same time, most million-yuan medical insurance plans still maintain a special drug list, primarily to clarify coverage responsibilities for some extremely expensive innovative treatment technologies; for instance, CAR-T cell therapy is widely included in the special drug lists of million-yuan medical insurance.

From special drug coverage to out-of-hospital drug purchase responsibilities, million-yuan medical insurance seems to comprehensively cover the costs of using some expensive but highly effective innovative drugs, which is undoubtedly highly attractive to modern people who are extremely worried about falling into poverty due to illness. Data shows that by 2025, the nearly saturated million-yuan medical insurance market achieved approximately 15% growth in the number of insured individuals.

However, whether it is the special drug coverage with a restricted list or the off-list outpatient drug purchase responsibility, million-dollar medical insurance policies have set many claims requirements. Among them, the special drug coverage with a restricted list is slightly more lenient. Besides strictly defined diseases, it usually also requires prescriptions issued by specialized doctors in hospitals, compliance with indications and usage specified in the drug instructions, being essential for the insured's current treatment, and purchases must be made at pharmacies designated by the insurer, etc. Additionally, the insured person must submit relevant materials according to the designated process of the insurer and pass the prescription review before purchasing the specific drugs listed in the prescription; otherwise, reimbursement will not be provided.

In the actual medical environment, obtaining a prescription issued by a specialist doctor, purchasing it at a designated pharmacy, submitting materials in advance and getting them reviewed has greatly increased the difficulty of reimbursement. Proving in the materials that the prescribed medication is essential for the insured person's current treatment, with no established process to follow, is an almost impossible task for most insured individuals who are already struggling to seek medical treatment. The claim requirements for off-prescription drug purchases outside the hospital without a restricted list are even more stringent, often requiring the insured to prove that the hospital pharmacy where they are being treated does not provide the prescribed medication. In fact, having a doctor issue a prescription, proving that the medication is necessary for the current treatment, and proving that the medication cannot be purchased at the current treatment hospital may constitute an "impossible triangle."

In a sense, due to the high threshold for claims, the various special drug responsibilities set in current million-dollar medical insurance policies still have more promotional effect than actual help provided to the insured. The "White Paper on Diversified Payment for China's Innovative Pharmaceuticals and Medical Devices (2025)" shows that in 2024, the scale of China's innovative pharmaceuticals and medical devices market is expected to reach 162 billion yuan, increasing by 16% compared to 2023. Among this, personal out-of-pocket payments in the innovative pharmaceuticals and medical devices sector still account for a high 49%, medical insurance fund expenditures account for about 44%, and commercial health insurance claims account for only approximately 7.7%.

Innovative drugs overwhelmed by million-dollar medical insurance are still trapped in the flow.

Special Drugs Move into Hospitals

If we focus on the particularly innovative drugs listed in the commercial insurance catalog, which are more expensive and highly efficient, the sales boost provided by existing million-dollar medical insurance is even more negligible.

Taking CAR-T cell therapy, which is most widely covered by million-dollar medical insurance, as an example: In 2024, the domestic sales of Yikaida amounted to approximately 500 million yuan, making it the best-selling among all disclosed CAR-T therapies. Over five years since its launch, Yikaida has accumulated total sales of 1.2 billion yuan. Benoda achieved sales of 158 million yuan in 2024, representing a 9% year-on-year decrease, with sales reaching 81.239 million yuan in the first half of 2025. Meanwhile, Saikaze sold only 39.424 million yuan worth in 2024. Considering that the per-dose prices of Yikaida, Benoda, and Saikaze are as high as 1.2 million yuan, 1.29 million yuan, and 1.15 million yuan respectively, even if all treated patients had their costs reimbursed through million-dollar medical insurance, the number of beneficiaries would be only in the thousands—forming a stark contrast to the hundreds of millions enrolled in such insurance schemes.

In fact, the coverage of expensive and highly efficient innovative drugs by million-dollar medical insurance is limited. The deeper reason lies in the fact that these drugs can only be squeezed out of hospitals, directly increasing the difficulty of reimbursement.

However, the "three exclusions" policy given in the first edition of the commercial insurance directory, aside from the drug bills, is expected to push these drugs from within hospitals to outside.According to the regulations, the medical insurance fund will not cover the costs of drugs listed in the commercial insurance directory, and they will not be included in the basic medical insurance self-payment rate indicators for designated medical institutions or in the monitoring scope for alternative varieties selected in centralized procurement. Cases involving the use of innovative drugs from the commercial health insurance-covered innovative drug directory may be excluded from the medical insurance payment scope based on disease categories, subject to payment after review and evaluation procedures.

First, it is not included in the assessment of the self-payment rate index for basic medical insurance.In the past, due to the "self-payment rate/self-paid proportion" indicator in hospitals' medical insurance assessments, doctors often tried to avoid prescribing high-cost self-paid medications when writing prescriptions. This was to prevent raising the hospital’s self-payment rate, which could affect the hospital's rating, performance evaluation, and medical insurance quota. This increased the difficulty for patients to obtain the corresponding prescriptions, making it impossible to meet the special drug claims requirements of million-dollar medical insurance policies. However, drugs listed within commercial insurance directories are not restricted by the self-payment rate indicator, greatly enhancing the flexibility of doctors’ prescriptions.

Secondly, it is not included in the centralized procurement and selection of substitutable varieties for monitoring.As the selected drugs from centralized procurement are implemented, the medical insurance department will monitor the usage ratio of "substitutable varieties in the same therapeutic area," encouraging the preferential use of low-cost drugs selected through centralized procurement while restricting the use of high-priced non-centralized procurement drugs. However, innovative drugs listed in commercial insurance directories are not considered "substitutable varieties" for centrally procured drugs and are exempt from substitution monitoring and usage ratio assessments. As a result, hospitals are more willing to purchase high-priced innovative drugs, and pharmaceutical companies, under relatively free pricing constraints, are also more motivated to promote the inclusion of these drugs in hospitals. For patients using million-yuan medical insurance for reimbursement, the claims difficulty for using in-hospital medications is significantly lower than that for out-of-hospital medications.

Finally, it may not be included in the scope of medical insurance payment by disease category (DRG/DIP).At this stage, the medical insurance DRG/DIP payment model based on disease categories has been rolled out nationwide in China. The use of high-cost innovative drugs may lead to "over-expenditure losses" for hospitals, so hospitals tend to restrict their use. However, according to the exemption policy in commercial insurance directories, if patients have purchased corresponding commercial insurance and use listed drugs within the scope of commercial insurance coverage, after review and evaluation, such cases will not be included in the fixed DRG/DIP payment. Instead, medical insurance will settle payments based on actual reasonable costs or other market-oriented rules. This will further promote the in-hospital use of expensive yet highly effective innovative drugs.

It can be said that the logic behind the commercial insurance catalog alleviating the flow dilemma of innovative drugs does not lie in whether the catalog itself is covered or expanded, but in whether innovative drugs can return from outside hospitals to inside hospitals under the promotion of supporting policies. The process of specialty drugs moving into hospitals requires close collaboration among pharmaceutical companies, insurance firms, and hospitals. Currently, if insurance companies rashly adjust product designs to fully cover the drugs listed in the commercial insurance catalog, it may suddenly expand the risk of claims. This might be the direct reason why, after the implementation of the commercial insurance catalog, various million-dollar medical insurance plans have remained inactive.

From being covered by million-dollar medical insurance to truly reducing the economic pressure on patients seeking medical care, the commercial insurance catalog has just begun to take its first steps forward.