Nearly 30 Million Coronary Artery Disease Patients’ Demand Drives InSight Lifetech's Successful IPO: What Are the Future Development Trends of the Industry?

InSight Lifetech

Cardiovascular Interventional and Implantable Device Manufacturer

Today, Insight Lifetech Co., Ltd. (hereinafter referred to as "InSight Lifetech") officially went public on the STAR Market, marking another company in the cardiovascular intervention field going public. With the listing of InSight Lifetech, we can't help but ask: why is it them? And where is the next opportunity in the industry track?

InSight Lifetech's IPO is related to the capital market's long-term attention to cardiovascular interventions, particularly in the coronary intervention sector.

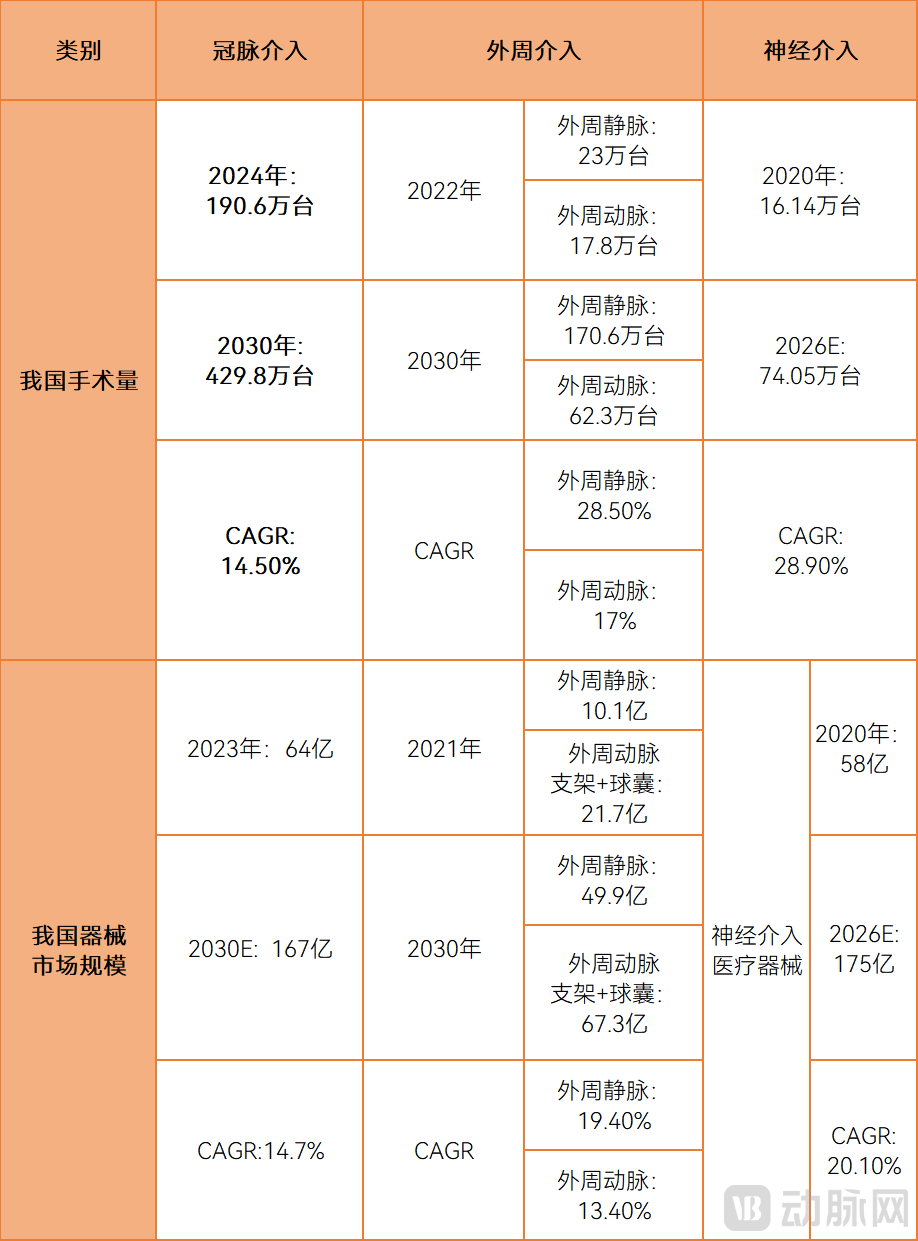

Firstly, in the field of pan-vascular intervention, the annual number of surgeries in the coronary intervention track laid out by InSight Lifetech has exceeded 2 million, indicating a huge market volume.

Data Sources: Frost & Sullivan, CIC Consulting, Southwest Securities; VCBeat整理;

Data Sources: Frost & Sullivan, CIC Consulting, Southwest Securities; VCBeat整理;

Note: Data from different statistical sources may vary. The National Cardiovascular Disease Medical Quality Control Center shows that the number of PCI procedures in 2024 is 2.21 million.

According to Frost & Sullivan, the number of patients with coronary artery disease in China is expected to increase from 270 million in 2022 to 320 million in 2030, with a compound annual growth rate of approximately 2.2%. Meanwhile, patient demand has driven the growth in the volume of PCI (percutaneous coronary intervention) procedures, a major treatment method for coronary artery disease. The volume of PCI procedures in China is expected to reach 4.298 million by 2030, with a compound annual growth rate of approximately 14.5%.

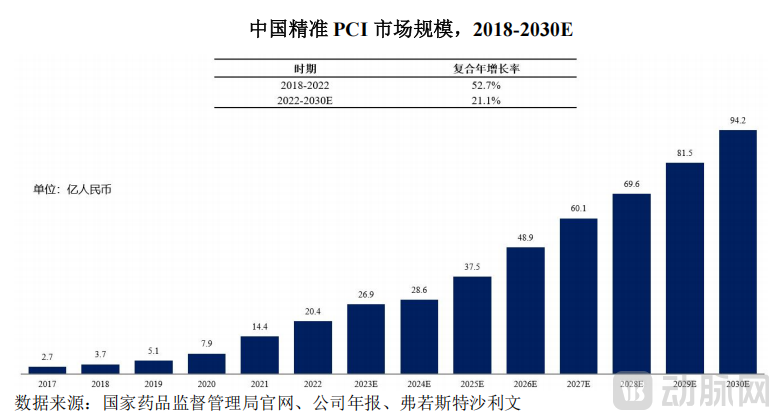

Secondly, InSight Lifetech focuses on the high-growth potential area of precision PCI within the coronary intervention sector.As core PCI procedure products like stents and balloons are gradually included in centralized procurement, the cost of PCI treatment has further decreased. Combined with the increasing awareness of health, PCI treatment is moving towards more clinically valuable precision PCI. Frost & Sullivan predicts that the market size of China's precision PCI will grow from 2.04 billion yuan in 2022 to 9.42 billion yuan in 2030, with a compound annual growth rate (CAGR) of approximately 21.1%, significantly higher than the growth rate of PCI procedures.

Source: InSight Lifetech Prospectus

Once again, InSight Lifetech, as an industry benchmark enterprise in coronary intervention solutions, has core products such as the FFR system and IVUS system, both of which are domestically首创products in China, successfully promoting the localization process in the field of precise diagnosis in China's coronary intervention treatment.

It should be noted that the commercialized products currently marketed by InSight Lifetech not only cover the coronary intervention field but also the peripheral intervention field. From the perspective of industry development trends, the coronary intervention field is characterized by strict clinical standards, a well-established evidence system, and mature surgical procedures, making it the core scenario for validating the safety, efficacy, and commercial feasibility of new interventional technologies. Companies often choose this as a breakthrough point to build core technical barriers and market foundations, and then rely on the same technology platform to expand into other areas of pan-vascular intervention. Given the importance of the coronary intervention track and its widespread attention from capital, what is the current state of the track's development, and which细分fields deserve more industry attention?

Through catheter technology, the narrowed or even occluded coronary artery lumen is dredged to improve myocardial blood perfusion. This process mainly includes important steps such as radial/femoral artery puncture, coronary angiography, establishing access, and stent implantation.From the overall market perspective, treatment products such as coronary stents and balloons still dominate. However, technology products for lesion assessment, like FFR, IVUS/OCT, are rapidly developing and are being more widely applied throughout the entire PCI procedure.: In a complex PCI procedure, it may be applied in various stages including preoperative assessment, evaluation of the effect of complex lesion preprocessing, assessment of stent/drug-coated balloon treatment efficacy, and evaluation of post-dilation treatment outcomes. As one of the most rapidly advancing fields, we will also provide an in-depth analysis of this topic in the article.

Market Size and Growth Rate of Innovative Devices in the Coronary Intervention Segment, Data Sources: Frost & Sullivan, CIC Consulting, Southwest Securities, Public Company Announcements, Yilin Research Institute, etc.; Compiled and Charted by VCBeat

According to the PCI surgical procedure, we roughly divide the innovative products in the coronary intervention field into the following categories:

1. Access Establishment — Increasing emphasis on complex lesion adaptation, reducing blind operations through imaging.

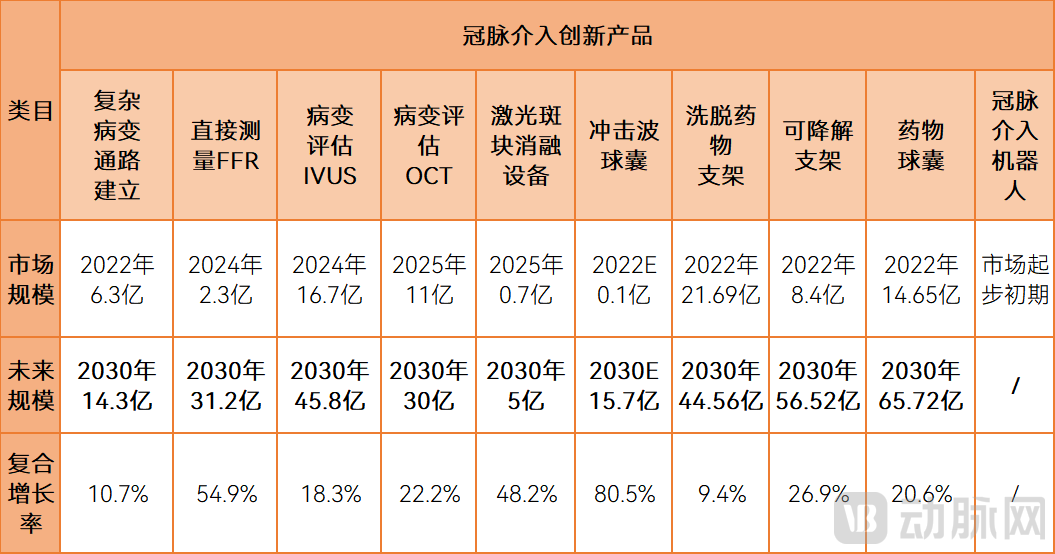

Access Establishment refers to the creation of a safe channel from outside the body to the site of coronary artery lesions through sheaths, guiding catheters, guidewires, and microcatheters. Currently, complex PCI accounts for approximately 50% of all PCI procedures. In complex PCI surgeries, more cases involve complicated lesion conditions such as tortuosity, tandem lesions, diffuse lesions, bifurcation, and severe stenosis, requiring specialized vascular access products for complex lesions. This market is predominantly occupied by imported manufacturers such as Terumo, Asahi Intecc, and Boston Scientific, with the market share of imported brands being approximately 80.5% in 2022. Domestic manufacturers mainly include companies like Apert (HT Medical). Currently, products for access establishment primarily focus on advancements in trackability (smaller diameters), pushability and flexibility, operability in special scenarios, and intelligence (imaging, reducing blind operations).In terms of market size, according to Frost & Sullivan, the market size of China's coronary complex lesion vascular access products is expected to grow from 630 million yuan in 2022 to 1.43 billion yuan in 2030, with a compound annual growth rate of approximately 10.7%.

2. Lesion Assessment — Imaging and Other Evaluation Techniques Become Essential Tools, Spanning the Entire Diagnosis and Treatment Process

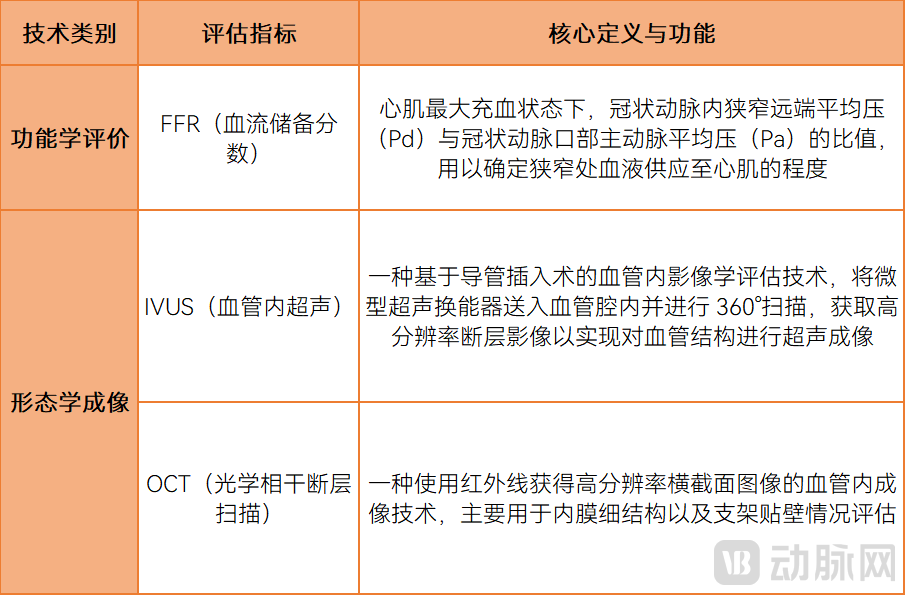

Main Diagnostic Techniques in Endovascular Intervention, Chart Compiled by VCBeat

Main Diagnostic Techniques in Endovascular Intervention, Chart Compiled by VCBeat

Functional FFR and morphological imaging techniques such as IVUS and OCT provide more valuable clinical indicators for guiding treatment in precise PCI, and are gradually becoming essential tools for precise PCI.

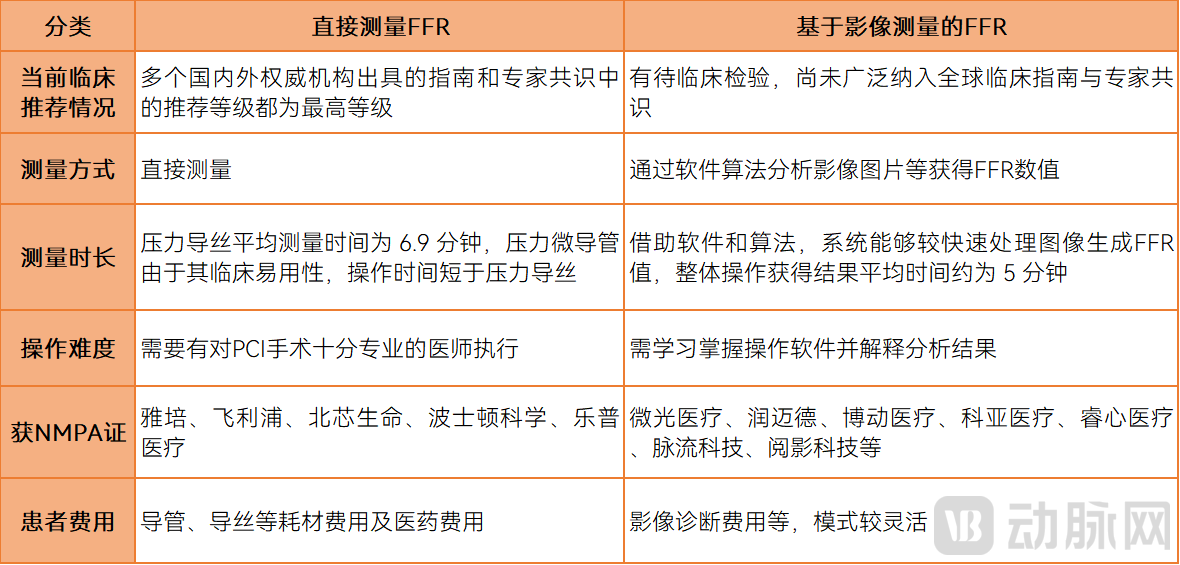

Comparison of Directly Measured FFR and Image-Based FFR, Data Source: InSight Lifetech Prospectus, Chart Prepared by VCBeat

Currently, FFR technology is widely used in PCI postoperative evaluation, PCI for ST-segment elevation myocardial infarction, unstable angina (UA), non-ST-segment elevation myocardial infarction (NSTEMI), drug-coated balloon treatment, and all scenarios involving coronary angiography. At present, there is competition between direct FFR measurement and image-based FFR measurement: among them, direct FFR measurement is the gold standard for FFR. Its advantages lie in the fact that major manufacturers like Abbott and Philips have been deeply rooted in the market for many years, with strong clinical education and application foundations, and their penetration rate continues to increase. Image-based FFR, including CT angiography-based FFR and angiography-based FFR, has the advantage of obtaining FFR values primarily through software algorithm analysis of imaging data. In the future, with improvements in algorithms, technological advancements, better imaging quality, and sufficient accumulation of evidence-based medical evidence, it may pose a substitution threat to the former. Computational fractional flow reserve represented by Pulse Medical's QFR has already gained widespread clinical application. Previously, domestically produced devices were mainly approved for angiography-based computational FFR. The latest information shows that at the end of January, MicroLight Medical’s product, which calculates quantitative flow ratio (OCT-FFR) based on optical coherence tomography (OCT) imaging, received approval. Local manufacturers are accelerating the implementation of their products.

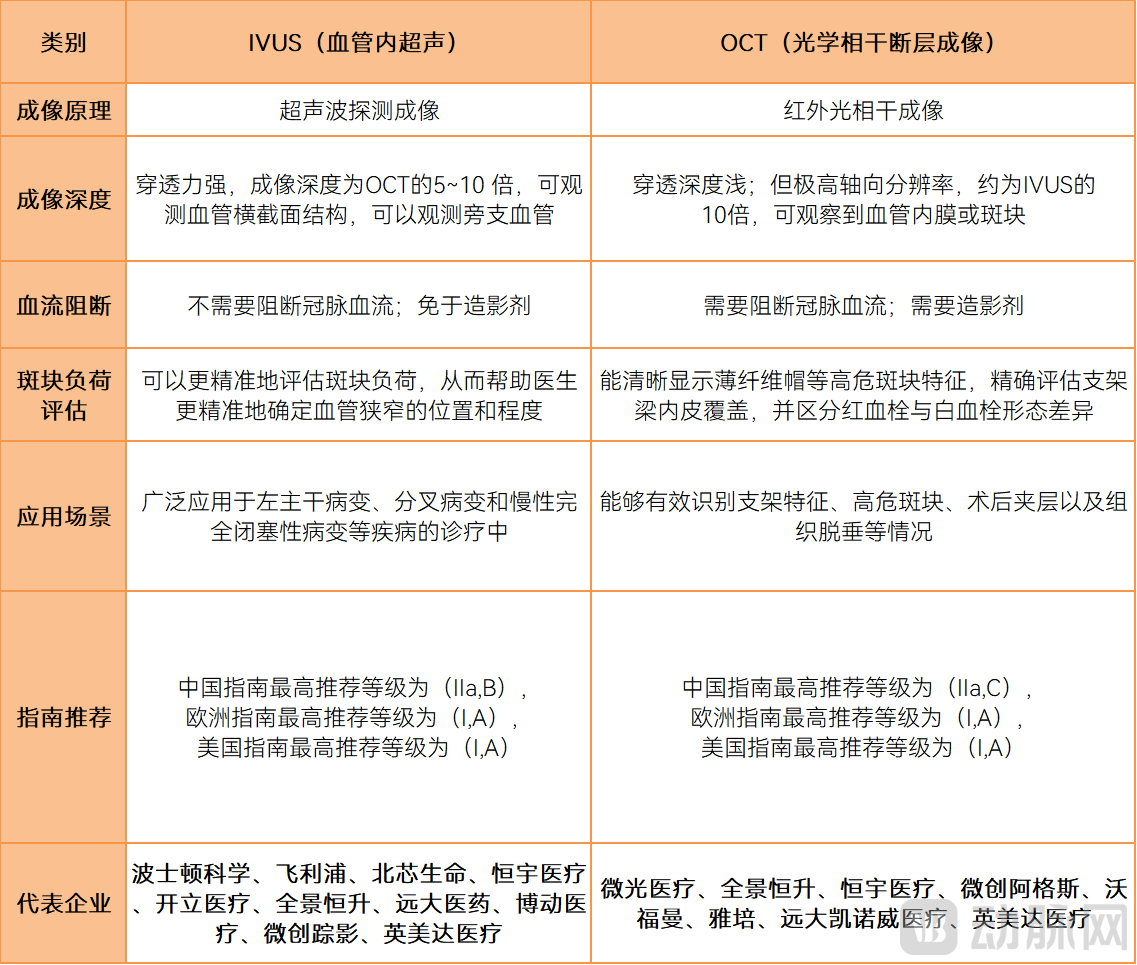

As important diagnostic tools for assessing patient conditions and treatment outcomes in PCI procedures, IVUS and OCT complement coronary angiography. Angiography is responsible for vascular mapping and intraoperative navigation, while OCT and IVUS focus on tomographic imaging and quantitative evaluation of the vessel wall. With the listing of InSight Lifetech, the value of IVUS has increasingly come to light.According to Frost & Sullivan, the market size of the IVUS coronary field is expected to be approximately 1.67 billion yuan in 2024 and is anticipated to reach 4.58 billion yuan by 2030, with a compound annual growth rate (CAGR) as high as 18.3%. However, the value of OCT technology still has yet to be fully explored, and it is expected to become the next technological breakthrough.

Comparison of OCT and IVUS Technologies, Data Source: InSight Lifetech Prospectus, DeviceMagic, VCBeat

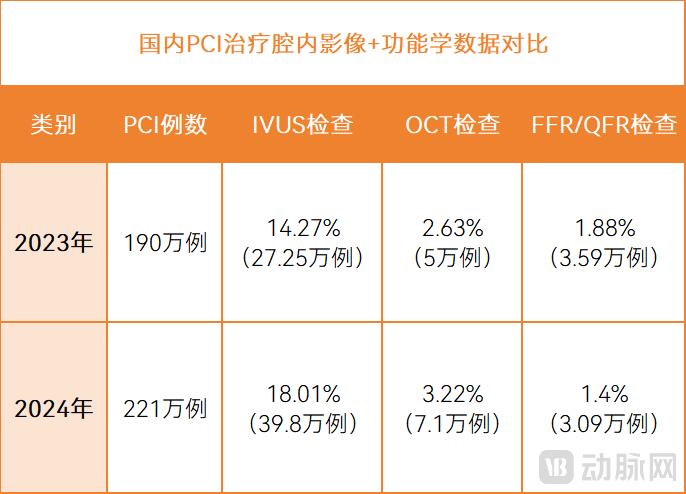

From the perspective of centralized procurement, IVUS systems have been partially included in centralized procurement to achieve volume expansion, while OCT systems are expected to achieve volume expansion through centralized procurement in the future.Intravascular Ultrasound (IVUS) kicked off a nationwide large-scale centralized procurement following the inter-provincial alliance procurement led by Zhejiang Province at the end of 2023. There are 10 products approved in the Chinese market, including Novasight Hybrid Catheter from Grand Pharmaceutical, and Outsight from MicroPort.®(Li Jian®) Single-use intravascular ultrasound diagnostic catheters, and Innereye single-use intravascular imaging catheters by AngioMind, except for all commercialized IVUS products that have been included in the medical insurance directory, with some products being incorporated into the centralized procurement scope. Centralized procurement has driven domestic companies to rapidly achieve substitution and increase production. According to data from the National Quality Control Center for Cardiovascular Disease Medical Treatment System, the number of IVUS examinations increased rapidly from approximately 272,500 cases in 2023 to 398,000 cases. In the OCT sector, with the approval and listing of domestically produced enterprises, rapid iteration has similarly achieved a breakthrough in the market monopolized by foreign enterprises. Referring to the market expansion in the IVUS field, the future OCT market is also expected to further expand.

Data source: National Quality Control Center for Cardiovascular System Diseases, VCBeat; VCBeat mapping

From the perspective of technological development, the current penetration rate of OCT technology is still lower than that of IVUS technology, but its long-term development may not be inferior to IVUS technology.The prospectus of InSight Lifetech pointed out that the current penetration rate of IVUS technology is higher. Data from the National Medical Control Center for Cardiovascular System Diseases shows that the market penetration rates of both IVUS and OCT examinations have increased. Even without centralized procurement, the usage of OCT still showed a rapid year-on-year growth of 42%. The reason is related to the longer time cycle for companies to transition from layout to harvest with OCT technology as an innovative technology—past clinical applications were mainly dominated by IVUS, while OCT lacked evidence-based support. However, with the growing availability of more favorable evidence-based data, OCT technology is expected to accelerate its penetration. For instance, South Korea's OCTIVUS study (2024), which aimed to compare OCT with IVUS, has been published: a prospective, multicenter, randomized, open-label study conducted across nine research centers in South Korea showed that the primary procedural complications in the OCT group were lower than those in the IVUS group (2.2% vs. 3.7%). Compared with the IVUS group, the total amount of contrast agent used was higher in the OCT group, but the total PCI time was shorter.

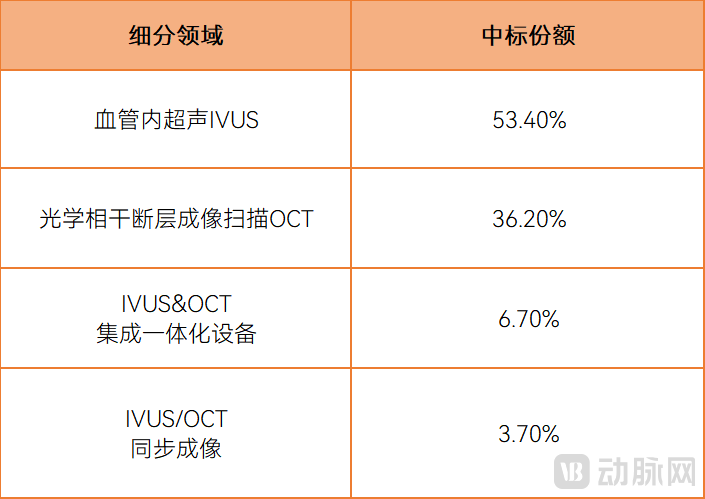

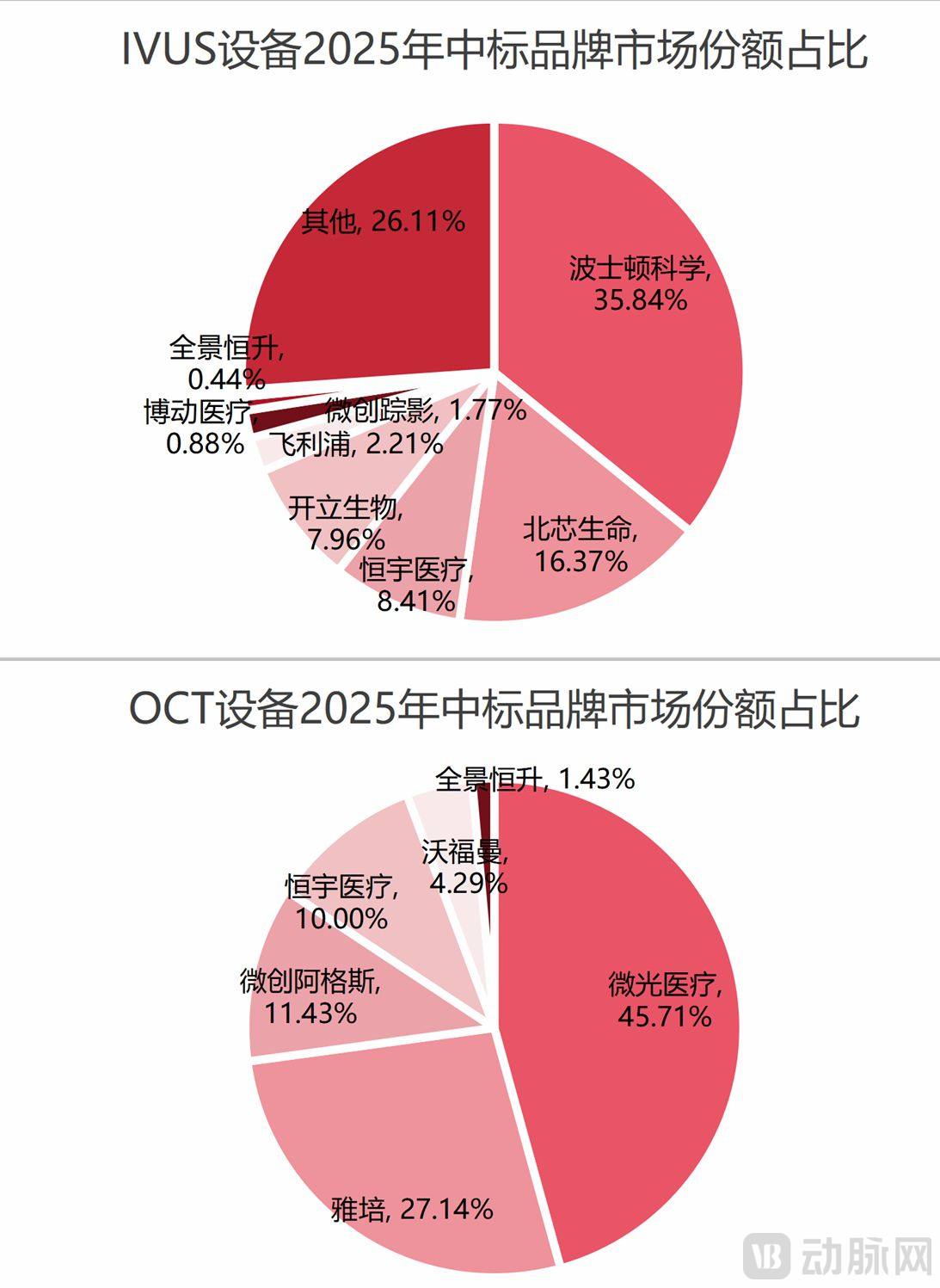

IVUS/OCT Local Companies in China Are Accelerating Development, Even Surpassing Foreign Enterprises' Market Share in Niche Fields.From the data of Party B's bidding platform, looking at the entire market,In the IVUS field, Boston Scientific still dominates, followed closely by companies like InSight Lifetech and Hengyu Medical. In the OCT field, Chinese manufacturers have broken the market monopoly previously held by overseas companies. As a leading company in the OCT sector, MicroLight Medical ranked first in the OCT market share in 2025, surpassing Abbott (27.14%) with a market share of 45.71%, securing an absolute leadership position.

Market Share of Intravascular Imaging Devices in 2025 by Segment, Data Source: DeviceMagic, Chart by VCBeat

Market Share of Various Equipment Brands in 2025; Data Source: Party B Treasure Platform; Chart Prepared by VCBeat

Market Share of Various Equipment Brands in 2025; Data Source: Party B Treasure Platform; Chart Prepared by VCBeat

3. Lesion Preprocessing - Increasing Clinical Attention: Treatment methods such as laser plaque ablation and shock wave balloons are gaining attention.

Laser plaque reduction devices provide a safer, more efficient, and convenient treatment option for the opening of coronary atherosclerotic stenosis and occlusive lesions. In this field, companies like Philips still dominate. Leading domestic companies, such as MicroPort, Ciecho, and Weiguang Medical, are in the process of obtaining certification. Currently, Weiguang Medical's cold laser plaque ablation system has entered the registration review stage, and barring any unforeseen circumstances, it may become China’s first laser plaque reduction device. Meanwhile, in early 2025, Weiguang Medical initiated the clinical enrollment for China’s first coronary cold laser ablation catheter and developed laser shockwave technology for calcified lesions and large-size plaque reduction technology.

Some plaques in the arterial walls of certain patients may evolve into calcium deposits. Before surgery, it is necessary to adequately prepare for vascular calcification to achieve perfect stent apposition. When treating mild, moderate, or severe vascular calcification, products such as ultra-high-pressure balloons, cutting balloons, scoring balloons, or procedures like rotational atherectomy are often used. However, complications, indications, health economics, and other issues limit the widespread adoption of these techniques. For example, ultra-high-pressure balloons can easily cause intimal tears; cutting balloons and chocolate balloons have larger outer diameters, which often affects their deliverability; and rotational atherectomy requires highly experienced physicians. Intravascular lithotripsy (IVL), represented by shockwave balloon catheters, is currently the only technology effective for deep calcified lesions. In China, manufacturers such as Jian Shi Medical, Sai He Medical, Lepu Medical, Pu Chuang Medical, Blue Sail Medical, Jian Wei Medical, MicroPort Melody, and Jia Mu Yao Medical have coronary shockwave balloon treatment products that have been approved for marketing.According to the prospectus of InSight Lifetech, in terms of market size, the shockwave balloon is still in the introduction stage, and it is expected to reach a market size of 1.57 billion yuan by 2030, with a compound annual growth rate of 80.5%.

VCBeat Chart

VCBeat Chart

In the future, technologies such as "laser" combined with shock wave balloons will better address ultra-high difficulty calcification issues in patients.

4. Treatment Products - Drug-eluting Stents Progress Towards Bioresorbable Scaffolds, Usage of Drug-coated Balloons Further Increases

Coronary stents and balloon products are core consumables in PCI procedures.

Drug-eluting stents are currently the mainstream product. They primarily utilize biocompatible polymers to coat proliferation-inhibiting drugs on the stent surface, which are slowly released to suppress cell proliferation, thereby reducing the probability of restenosis. However, design and process limitations of drug-eluting stents can easily lead to endothelialization healing disorders. In recent years, there has been increasing exploration into biodegradable polymer-coated drug stents, polymer-free drug stents, and bioresorbable vascular scaffolds (BVS). This field has seen the emergence of a large number of innovative companies, such as Meizhong Shuanghe, Ju Zheng Medical, Mai Quan Medical, Amedical, and Baixin’an, among others. According to Frost & Sullivan, by 2030, the number of fully degradable stents used in China is projected to increase to 1.289 million, accounting for approximately 30% of all stents.According to Southwest Securities, by 2030, the market size of drug-eluting stents is expected to reach 4.456 billion yuan, while the market for bioresorbable scaffolds is projected to reach 5.652 billion yuan. Notably, the annual compound growth rate of bioresorbable scaffolds is as high as 26.9%.

Data source: Southwest Securities; Chart compiled by VCBeat

Currently, the usage of drug-coated balloons is also continuously increasing. According to CCIF&CCPCC2023, the proportion of drug-coated balloons used in PCI has risen from 6.4% in 2019 to 17.6%. The advantages lie in the complete release of the drug, after which the balloon can be withdrawn from the blood vessel, leaving no foreign objects behind. Additionally, it offers benefits such as a shorter postoperative antithrombotic treatment time, lower risk of bleeding, and better preservation of vascular elasticity. However, its current main applications are for patients with in-stent restenosis, ostial lesions of vascular branches, small vessel disease, and those at high risk of bleeding, and it cannot be used for patients with severe vascular disease.According to data from Southwest Securities, the drug-coated balloon market reached 1.465 billion yuan in 2020 and is expected to reach 6.075 billion yuan by 2030, with a compound annual growth rate (CAGR) of 20.6%.

5. Adjunctive Therapy —— Coronary Intervention Surgical Robot Approved, Enhancing Surgical Intelligence

As the first coronary interventional surgical robot is approved in 2025, this field has increasingly come into the public eye. Currently, mainstream products adopt a master-slave control architecture, with core value lying in the precise delivery of guidewires/catheters/stents, reduction of radiation exposure for doctors, and enhancement of operational stability for complex lesions. Several products have already been approved for marketing or entered clinical trial stages in China. Representative companies include Weimai Medical and Jieruo Medical, both of which obtained Class III certificates for coronary interventional surgical robots in 2025. Notably, Weimai Medical’s ETcath® is the first domestically developed coronary interventional surgical robot to enter and gain approval through the National Medical Products Administration’s “Special Approval Procedure for Innovative Medical Devices.” According to estimates by Jindalai,Based on the 2014-2024 data of DSA equipment repurchases in China, it is estimated that there will be approximately 12,000 operating rooms capable of installing vascular interventional surgical robots in the future. By 2030, the global vascular robotics market size is projected to reach approximately $4.48 billion, with the Chinese market valued at around 5.82 billion RMB.Vascular interventional surgical robots are still in the market introduction phase.

Looking back at the development of the coronary intervention field, it is essentially patient-centered, with a continuous pursuit of smaller trauma, faster recovery, and better postoperative outcomes. The focus has shifted from relying more on doctors' experience in the past to relying more on imaging technology and evidence-based evidence, and from solving short-term vascular patency issues to ensuring long-term patient prognosis.

Currently, the field of coronary intervention treatment mainly presents the following trends:

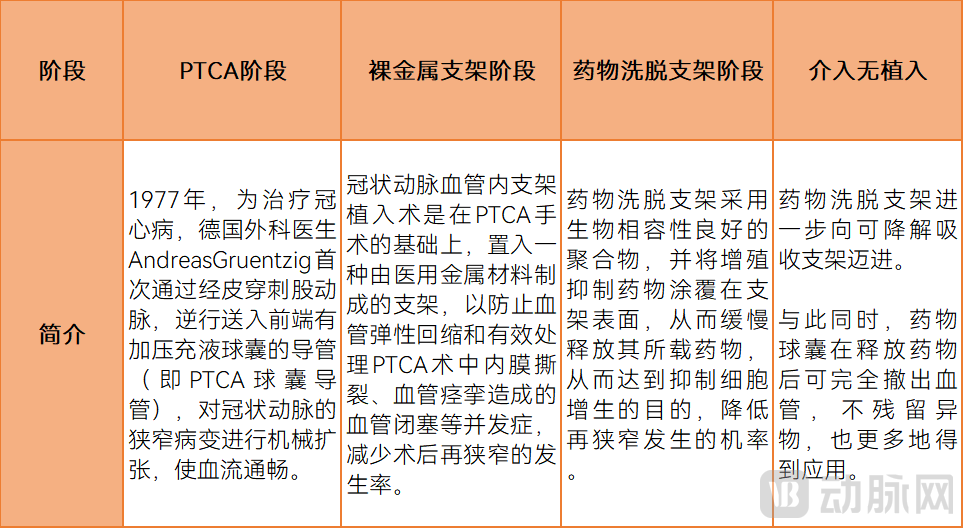

1. The development trend of "intervention without implantation."Coronary interventional treatment has gone through the stages of PTCA, bare-metal stents, and drug-eluting stents, further evolving into the "intervention without implant" phase — utilizing products such as drug-coated balloons for targeted drug delivery and bioresorbable scaffolds to promote natural vascular healing and reduce the risk of long-term complications. Against this trend,The demand for precise understanding of intravascular structures and physiology has also driven the market for precision imaging diagnosis and evaluation tools in coronary treatment to become another significant market, second only to coronary stents and drug-coated balloons.

Data source: Southern Securities, compiled and charted by VCBeat

Data source: Southern Securities, compiled and charted by VCBeat

Secondly, the industry has shifted from past single technological innovations to systematic innovations guided by technologies such as imaging diagnostics, with IVUS/OCT technology gradually upgrading to become an essential tool.Whether it is functional diagnosis FFR or imaging diagnosis IVUS/OCT, precise identification of anatomical stenosis and ischemia can lead to more accurate targeted treatment, avoid overtreatment, and reduce the burden on medical insurance. Among these, in the field of diagnostics, the trend of multi-modal fusion in medical imaging products is becoming increasingly evident.

Third, the industry is gradually moving towards intelligence, with the integration of AI and surgical robots for diagnosis and treatment becoming one of the trends.Currently, AI technology is not only used for the auxiliary control of surgical robots but also applied in medical imaging measurements such as IVUS/OCT to simplify physician operations. At the same time, artificial intelligence is utilized to algorithmically generate VFR (Virtual FFR) for screening ischemic lesions, reducing unnecessary PCI procedures and assisting doctors in decision-making. In the future, with the integration of intelligent technologies, the precision of diagnostic evaluation and treatment is expected to improve significantly.

Fourth, the coronary intervention market will shift more from foreign dominance to the rise of local enterprises.In the coronary intervention market, domestic companies are comprehensively breaking the monopoly of overseas enterprises and gradually transitioning from followers to leaders. This transformation is occurring in two aspects: First, experts in China's coronary intervention field are increasingly taking the global stage, sharing academic insights and presenting clinical outcomes enabled by cutting-edge technologies. Second, products associated with PCI procedures in China are achieving market breakthroughs and expanding globally. For instance, in the field of imaging diagnostics, InSight Lifetech’s IVUS product is not only the first domestically self-innovated 60MHz high-definition and high-speed IVUS product in China but also the first domestically produced IVUS product to receive approval overseas (EU MDR). After its launch, it broke the monopoly of foreign companies. Similarly, in the OCT field, under the market dominance of international giant Abbott, Weiguang Medical, a local company, received FDA approval in the U.S. for its multimodal OCT in 2025. As the first Chinese intravascular imaging company to obtain FDA certification, it is expanding into more than 10 countries and regions worldwide, with an overseas growth rate as high as 100% in 2025.

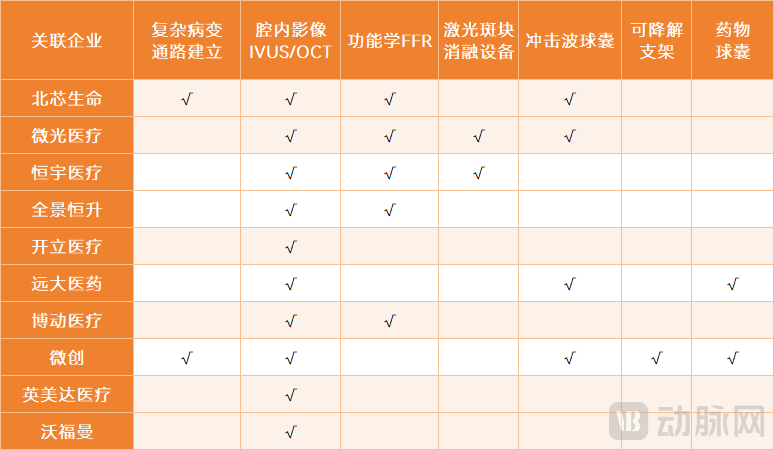

Enterprise Layout Field, Based on Data from Corporate Official Accounts and the National Medical Products Administration, etc., Chart by VCBeat

Enterprise Layout Field, Based on Data from Corporate Official Accounts and the National Medical Products Administration, etc., Chart by VCBeat

In the future, in the field of coronary intervention and even pan-vascular intervention, there will be opportunities not only for domestic substitution but also for globalization. More importantly, it depends on who can better grasp the industry demands and technological development trends, and more rapidly launch and iterate innovative products. In this process, Chinese innovative companies are bound to play a more significant role in the global market, bringing higher-quality medical innovation solutions to patients in China and around the world.