Major Benefits in 2026! The Introduction of National Standards for Tiered Pricing of Surgical Robots Ignites the Industry

Intuitive

Surgical Robot Developer

Surgical Robot Market Welcomes Significant Policy Boost!

In January 2026, the National Healthcare Security Administration officially released the "Guidelines for the Establishment of Medical Service Price Projects for Surgical and Therapeutic Auxiliary Operations (Trial)" (hereinafter referred to as the Establishment Guidelines). The release of these guidelines further fueled the growing popularity of surgical robots. Although the establishment of medical service pricing does not equate to inclusion in medical insurance reimbursement, it is still highly significant for the industry.

This milestone policy's impact on the industry can be viewed from two aspects.On the one hand, it marks the standardization of surgical robot charges.Previously, the charging standards for surgical robots were mainly set by hospitals independently, lacking a unified standard. The pricing guidelines issued by the National Healthcare Security Administration (NHSA) have made the charges for surgical robots "legally compliant."

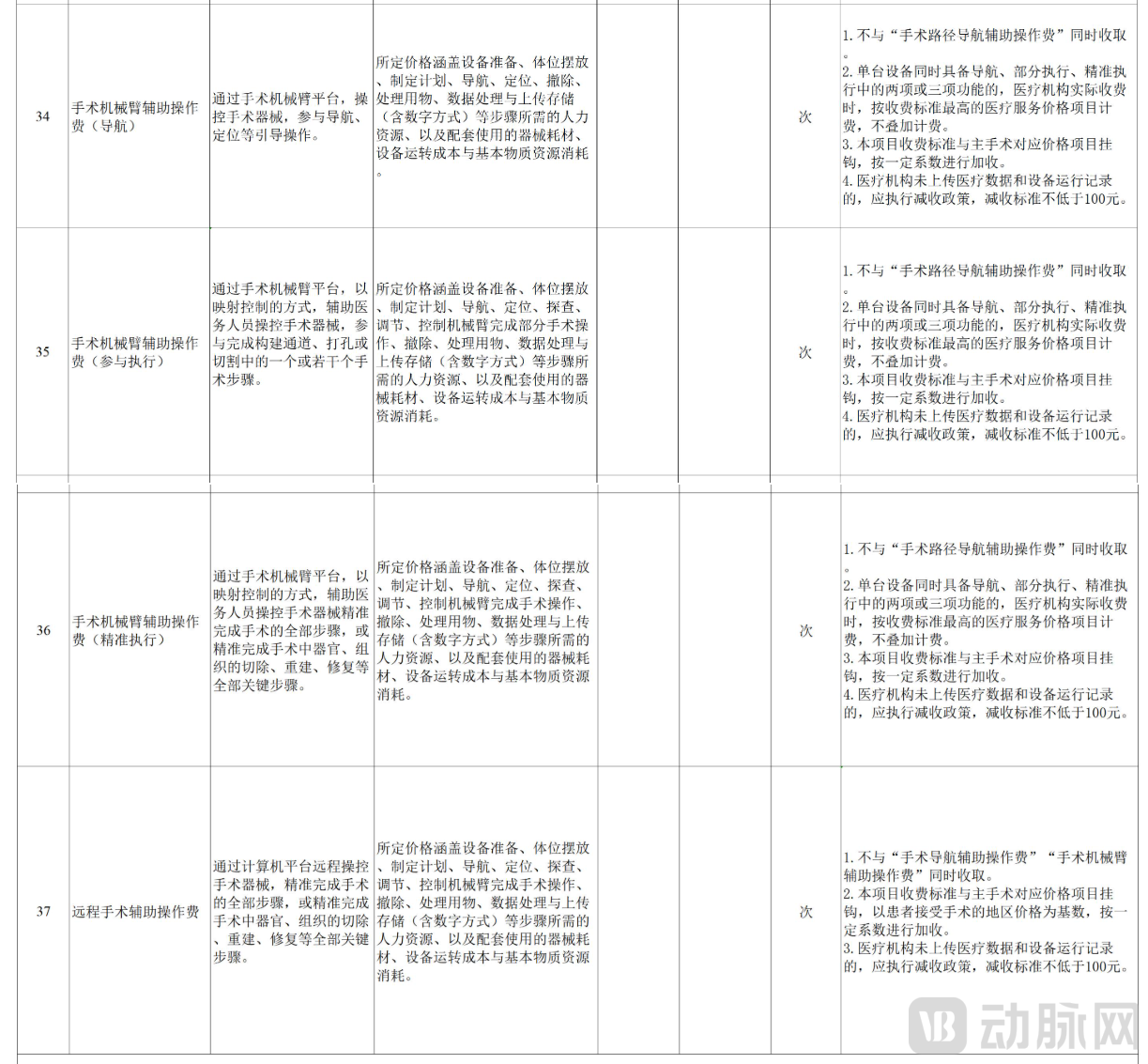

On the other hand, the project guidelines stipulate tiered charging, with the surgical robotic arm assistance fees divided into three functional tiers: navigation, participation in execution, and precise execution.The charging system focuses on clinical value, tilting towards products that participate in more surgical procedures and accomplish more precise operations.

EJ Capital has long been deeply engaged in and served innovative sectors such as surgical robots. Founding partner Pengcheng Liu stated: "Currently, domestic surgical robot companies are showing a flourishing and rapidly iterative development trend in terms of surgical method selection, technological innovation, registration progress, and more. However, the issue at the payment level has remained unresolved, causing most companies, except those utilizing endoscopes, to rely on financing for survival. The release of the 'Project Approval Guidelines' represents the finalization of national-level charging standards, bringing the industry out of the 'darkest hour before dawn.'"’Crossing into 'the sun moves above the horizon'’"The stage."

How will the surgical robot charging policy impact the industry? VCBeat interviewed several leading surgical robot companies.

Part of the Project Guidelines

This project initiation guideline impacts the entire surgical robotics industry. According to VCBeat statistics, the surgical robotics industry has over 93 registered certificates, with more than 60 companies holding these certificates.

When mentioning the impact of the project guidelines, multiple companies believed that the standardization of charging is a milestone progress for the industry.The project guidelines have put an end to the hospital self-pricing model, providing a reference standard for surgical robot charges. This move has narrowed the pricing gap between hospitals and standardized the charging criteria for surgical robots.

A regional sales director of a laparoscopic surgical robot company told VCBeat: "The current pricing of laparoscopic surgical robots is mainly determined by hospitals independently, and there are differences in pricing between different hospitals. Even within the same city, the prices of different hospitals may vary greatly. Some hospitals set very low prices to promote robots, even performing surgeries at a loss, while others set very high prices. In some provinces and cities, there is uniform pricing. For example, in Hubei Province, the uniform startup fee for laparoscopic surgical robots is 9,234 yuan, while in other provinces and cities, there is none. The issuance of these guidelines provides a reference for charging items for surgical robots, making the charging for surgical robots 'legally compliant.'"

An orthopedic surgical robot company also stated: "Previously, the charges for surgical robots mainly included startup fees and consumable costs, with a lack of uniform standards; in some provinces and cities, there was no charge catalog. After the policy was introduced, a unified charging standard was established."

Unified charging standards lower the threshold for hospitals, reduce obstacles in the commercialization process, and are beneficial for the large-scale promotion of surgical robots across multi-level hospitals nationwide.

Industry insiders believe:The focus of this adjustment lies in the systematic reconstruction and standardization of the surgical robot charging system. In the past, various regions mostly addressed robot charging issues by referencing instruments, bundling, or adding fees, resulting in non-uniform projects and unclear standards. The new project guidelines, at the national level, categorize endoscopic surgical robots as "precision execution technology."’Formally included in the medical service price project system, establishing a clear and logically consistent charging framework.

From a results-oriented perspective, unified project initiation helps make the charging structure more transparent and rational, and overall facilitates the return of prices to a reasonable level. For patients, this generally shows a downward trend, making it an important measure that benefits both the country and its people. At the same time, incorporating remote-related capabilities into chargeable items is necessary and forward-looking. Remote surgery essentially represents the extension of expert surgical capabilities, offering widespread benefits. Combined with China’s cost-effective network infrastructure, adopting accessible pricing could promote its widespread application.

In addition to the unification of charging standards, multiple companies mentioned an easily overlooked point in the guidelines: the project approval guidelines include "the storage and uploading of medical data and equipment operation records" as part of the cost structure. This means that chargeable items are required to upload backend data, making charging supervision more standardized.

The specific charging price is still being formulated by the National Healthcare Security Administration. On the one hand, considering the relatively high amortization cost during the initial clinical use of surgical robots, the National Healthcare Security Administration will guide regions to research and establish reasonable baseline charging standards. On the other hand, taking into account patients' accessibility to surgical robots, the National Healthcare Security Administration will also guide regions to set ceiling charging standards simultaneously. The detailed standards will be reasonably formulated by local healthcare security departments based on factors such as regional economic and social development.

The introduction of the project guidelines has made tiered pricing for surgical robots a focal point of industry discussion.

According to the project guidelines, the surgical robotic arm's assisted operation fee is divided into three functional charging categories: navigation, participation in execution, and precise execution.The project initiation guidelines charge fees based on the role surgical robots play in the surgical process. The charges are matched according to whether the surgical robot serves as a navigation tool, participates in partial execution, or performs full-process precision execution. Important consumables in the surgical robot business model have also shifted from hospital-led pricing to uniform pricing.

Tiered pricing will have a profound impact on the direction of industry development.TINAVI mentioned in investor communications that the guidelines follow the overall principle of "project establishment based on service output," focusing on the actual participation level of robots in surgeries and their clinical value contribution to precision surgery., which will guide and incentivize companies to develop high-value technologies that can participate more deeply in core surgical steps and improve clinical outcomes., will also guide the surgical robotics industry into a new phase of high-quality, standardized development driven by real clinical value.

A leading robotic-assisted laparoscopic surgery company also stated: "After the establishment of a unified pricing system, industry competition will increasingly return to the core of clinical value itself. When pricing standards become more rational, the key to a company's development will no longer be price flexibility but whether it can continuously create clear and verifiable minimally invasive value. The core factor determining whether a company can benefit is whether it genuinely enhances minimally invasive techniques and improves patient outcomes."

The implementation of the charging catalog will undoubtedly accelerate the development of the industry, boosting the growth of the surgical robot market.Looking back at 2025, the surgical robot market achieved strong overall growth in the number of surgeries despite being in a market environment without insurance reimbursement and primarily self-funded.

Laparoscopic surgical robots are operating efficiently, with the number of surgeries performed by a single unit growing rapidly.According to Fosun Intuitive data, more than 500 da Vinci surgical robots have been deployed in China, serving over 810,000 Chinese patients cumulatively.The average annual number of surgeries performed by a single device exceeds 400.According to Frost & Sullivan data, the average annual number of assisted surgeries per single laparoscopic surgical robot in China was over 250 in 2021. The growth in this data reflects the widespread demand for laparoscopic surgical robots in clinical settings in China.

Chinese companies have also seized this development opportunity, capturing half of the new installation market.According to RoboticTech statistics, the number of bids for China's domestic endoscopic surgical robot market in 2025 is 110 units, with leading companies such as MicroPort Robot, Jinfeng Medical, Suribot, and Sizhe Rui taking the lead in winning bids. At the same time, domestic endoscopic surgical robot companies have also opened up a second front. Throughout 2025, they newly secured overseas orders exceeding 130 units, achieving dual-track rapid growth in both domestic and international markets.

The orthopedic surgery robot market has also started to gain momentum.According to VCBeat data, the number of orthopedic surgical robot procurement bids exceeded 100 units in China by 2025, with market size (measured by quantity) experiencing significant growth and a year-on-year increase of approximately 35%. TIANYIZHANG maintains its position as the leading market share holder in China's orthopedic surgical robot sector. Amidst record-high installations of surgical robots, the volume of orthopedic robotic surgeries in China reached 48,500 cases in the first three quarters of 2025, of which over 35,000 cases were performed using TIANYIZHANG's Tianji orthopedic surgical robot, accounting for more than 70%.

At the same time, 2025Breakthroughs in Multiple Specialized Surgical Robot Fields in ChinaIn the field of ophthalmology, Antai Weijing's ophthalmic surgical robot completed its registration clinical trials in 2025, officially entering the critical phase of registration and market launch; Micro Eye Medical successfully performed the world’s first remote robotic subretinal injection surgery, marking the transition of remote surgery from the "centimeter level" to the "micron level" era. Subretinal microsurgical robots can perform high-precision surgeries that are typically impossible for general doctors. With the establishment of a payment framework specifying charges for 'precise execution,' their clinical necessity aligns with policy support, offering a competitive advantage in commercialization.

In the field of structural heart disease, Peijia Medical's self-developed TAVR surgical robot, Reach Tactile, has entered the "Special Review Procedure for Innovative Medical Devices"; in the natural orifice field, MicroPort®Minimally Invasive® Robotic Bronchoscopy Surgical Robot — UniPath®/Dudao® Electronic Bronchoscopy Surgical Navigation System Approved for Marketing in China; In the field of percutaneous intervention, the renal interventional intelligent surgical robot developed by Weide Precision based on intraoperative ultrasound technology has passed the special review for innovative medical devices by the state and entered the innovation pathway.Dao。

Liu Pengcheng, founding partner of Yijia Capital, continued to add: "The successful commercialization and rapid development of innovative medical devices tests the comprehensive capabilities of the founding and management teams. Technology is just the threshold and ticket to enter the market, while clinical trials, registration, policies, channels, and more all determine the life or death of a company. Strategic foresight for enterprise development is a key factor. The release of the 'Project Guidelines' is undoubtedly a huge boon for well-prepared companies, but for those 'who haven't done their homework...'’"It's a devastating blow to the companies. Currently, the national guidelines have made a good start, and the next key step is to actively coordinate the mapping of medical insurance in various provinces and the construction of channels, which is the preparatory work that enterprises need to complete at least one year in advance to obtain product marketing approval."

Driven by the multiple forces of favorable policies, industrial innovation, and clinical demand, the surgical robot market in China is entering a golden age of development. Companies with continuous innovation capabilities, efficient expansion of indications, and the ability to build evidence-based barriers through academic promotion while validating product value with high-quality clinical data, are poised to capture a larger market share.