HeartCare Medical's IPO Journey: Navigating Giant Rival Challenges and Aiming for Breakthrough in China's Neurovascular Market

HeartCare

Neurointerventional Medical Device Developer

The vascular intervention sector gains another listed company.

Today, HeartCare officially listed on the Hong Kong Stock Exchange and rang the opening bell. The IPO price was HK$171, and the opening price was HK$141.2. As of press time, HeartCare's share price stood at HK$137.5, down 19.59%, with a market capitalization of HK$5.34 billion.

As a rising star in the medical device market, HeartCareIt took only a brief five from founding to IPO.Year, its growth rate stands as a phenomenal benchmark in the neurointerventional sector. However, on the eve of its IPO, HeartCare faced targeted strikes from industry giants, casting a shadow over its listing.

In the prospectus publicly released in January this year, HeartCare stated,In April 2021, the Company received a notice of infringement claim from the Ningbo Court. The lawsuit was filed by Medtronic, the global leader in medical devices that holds a 60% market share in China’s neurointerventional device sector, with Ningbo Yongheng Medical Device Co., Ltd. also named as a co-defendant.

However, this was merely a "minor hiccup" on the path forward and did not hinder the company's smooth public listing. For HeartCare, the greater challenge lies in how to break through in a fiercely competitive market.

As is well known, for years, 90% of the market share for neurointerventional devices in China has beenMedtronic, StrykerDominated by foreign enterprises, the remaining market space of merely 10% has already become a red ocean where Chinese-produced neurointerventional device manufacturers fiercely compete, and prior to HeartCare's listing,Peijia Medical, Volute MedicalWith peers having already taken the lead in ringing the listing bell, and facing a flood of competitors swarming into the market, how much real competitive value does HeartCare truly possess?

From Founding to IPO in Just Five Years: How Was This Phenomenal Case of Domestic Substitution Forged?

The path to domestic substitution has always been arduous.

Along this path, SANY Heavy Industry led the charge with its "SANY Red Sweeping the World" campaign, ultimately sweeping aside a host of Japanese and South Korean excavators from Doosan and Hitachi; following closely, Mindray Medical deployed its "encircling the cities from the countryside" strategy, tearing a breach in the "GPS medical device iron curtain" established by GE, Philips, and Siemens.

Today, yet another industrial pathway for domestic substitution presents itself to China's manufacturing sector: neurointerventional medical devices. In this track brimming with boundless challenges and limitless possibilities, the portrait of a winner on the domestic substitution path is emerging with striking clarity. Having transitioned from founding to IPO in a mere five years, it stands as a true pioneer in the wave of domestic substitution.

A typical representative of this is HeartCare, a medical device company specializing in the development and commercialization of new minimally invasive interventional technologies for stroke prevention and treatment.

In 2004, upon completing postgraduate studies,Wang GuohuiUpon joining MicroPort, he remained with the company for a full eight years. During this period, MicroPort entered a phase of rapid development and successfully ascended to the leading tier of China’s domestic medical device sector. Meanwhile, Wang Guohui also experienced substantial professional growth over these eight years. During his tenure, he represented MicroPort at the National Technical Committee on Surgical Implants Standardization, where he spearheaded the revision of dozens of industry standards, significantly driving the advancement of the industry at that time.

However, Wang Guohui was not satisfied with this; his burning passion for entrepreneurship has always been surging.In 2012, Wang Guohui left MicroPort and founded China’s first company to manufacture renal denervation products for the treatment of resistant hypertension—AnTong Medical.

Through the founding of Apt Medical, Wang Guohui was able to fully leverage the professional expertise he had accumulated at MicroPort, while further honing his management and operational capabilities. During this process, Apt Medical experienced rapid growth, securing the first European market approval for an Asian product within just one year. Subsequently, the company entered into a strategic partnership with Terumo, Asia's largest medical device company, and initiated clinical trials in China.

The success of Antong Medical did not stop Wang Guohui from advancing further. Following this,Wang Guohui also founded Biosynergy Biotech, which similarly focuses on the coronary artery field., this company, dedicated to bioresorbable coronary drug-eluting stents, has now grown to rank third among domestic bioresorbable stent manufacturers in China, with its products having entered the final stage of clinical trials.

As Antong Medical and Baixinan Biotechnology gradually stabilized their operations, Wang Guohui felt that company management no longer demanded so much of his energy. As an entrepreneur, his restless drive was stirred once again. In early 2016, attending a neurointerventional forum by chance revealed to him that neurointerventional devices in the Chinese market were almost entirely monopolized by imports. These products were expensive and in short supply, and many diseases lacked dedicated interventional devices.

“The high-value medical consumables market in the cardiac field has already witnessed the emergence of multiple listed companies, whereas the market share of domestically produced neurointerventional products remains relatively low. I believe that what domestic manufacturers have achieved in coronary intervention can equally be accomplished in the neurointerventional sector. Those of us in the vascular field should contribute to advancing domestically made neurointerventional products.” With this initial aspiration,In 2016, Wang Guohui founded HeartCare, specializing in developing products for integrated cardiovascular and cerebrovascular management to address stroke.

This decision quickly attracted significant attention from the capital markets. Less than a year after its establishment, HeartCare secured tens of millions of RMB in angel funding. Following this, the company continued to garner strong favor from investors, successfully completing five rounds of financing between 2018 and 2020. Notably, in 2020, the year prior to its IPO, HeartCare closed three funding rounds within a single year, raising a total of several billion RMB, which to a certain extent accelerated HeartCare's IPO process.

Golden Track, Racing with "Capital"

According to incomplete statistics from VCBeat,Hillhouse Capital, Chende Capital, SDIC Innovation, Anlong Fund, Honghui Capital, Sequoia Capital China, Huagai Capital, JF Capital, Qianhai Fund of Funds, NewMargin VenturesOver 60 investment institutions have already committed substantial capital to the neurointerventional sector, unanimously expressing continued optimism about the field.

Capital allocation is inherently directional; the neurointervention sector has garnered significant attention due to itsLarge market potential, rapid growth, upstream technology-driven development, and strong national policy support.

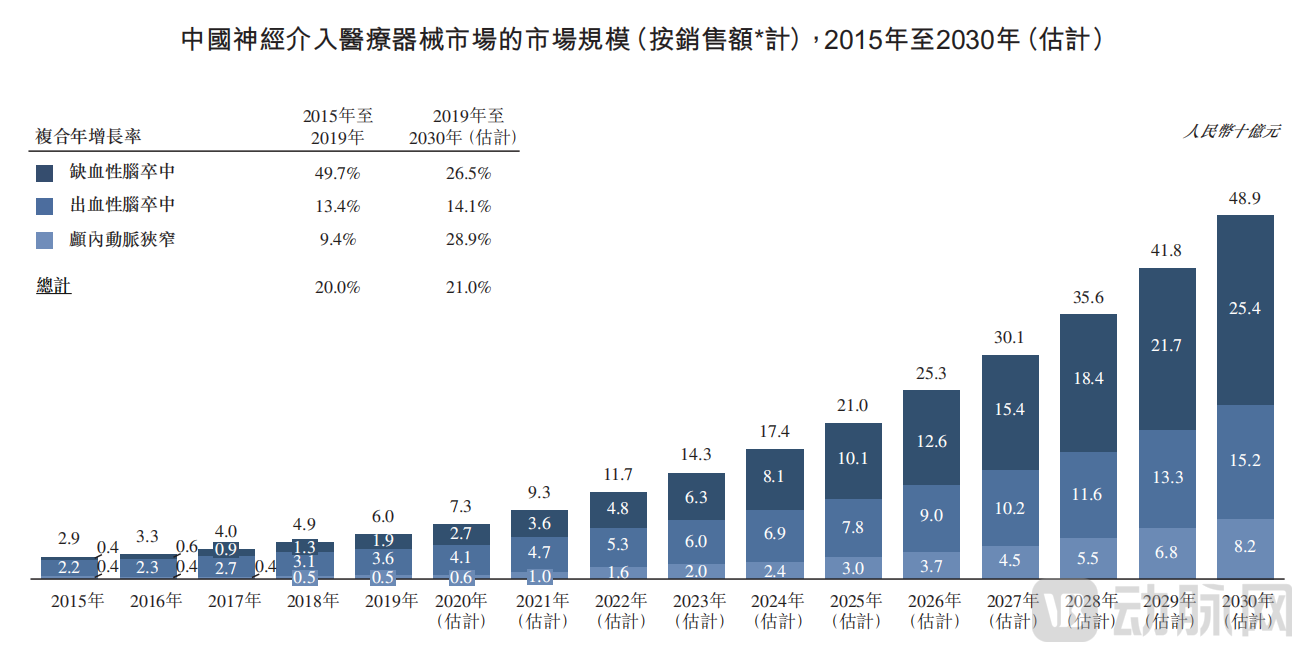

Currently, stroke is the leading cause of death in China.According to data from China Insights Consultancy, in 2019, the number of stroke patients in China reached 14.8 million, including 11.9 million patients with ischemic stroke and 2.9 million patients with hemorrhagic stroke, among which the annual number of new ischemic stroke cases reached 2.3 million.

On the other hand, the penetration rate of neurointerventional procedures in China remains relatively low compared to that in developed countries.In the United States, following the 2015 AHA guidelines that established mechanical thrombectomy as a first-line therapy for ischemic stroke, coupled with technological advancements, the adoption rate of mechanical thrombectomy rapidly increased from 1.4% in 2015 to 11.8% in 2019. In contrast, China's mechanical thrombectomy adoption rate stood at only 1.7% in 2019. However, driven by a combination of favorable factors—including technological innovation, supportive government policies, and the continuous growth of per capita disposable income and healthcare expenditure—the adoption rate is projected to reach 42.9% by 2030.

This data growth is directly reflected in the market size. According to the prospectus,China's neurointerventional medical device market size increased from RMB 2.9 billion in 2015 to RMB 6.0 billion in 2019, at a compound annual growth rate (CAGR) of 20%, and is projected to further expand to RMB 49.8 billion by 2030, representing a CAGR of 21% from 2019 to 2030.

Facing a Vast Blue Ocean, How Is HeartCare Performing?

As an innovative neurointerventional medical device company, HeartCare holds a leading position in China’s neurointerventional market, leveraging its extensive portfolio of commercialized and pipeline products, which encompasses both neurointerventional and cardiovascular medical devices.

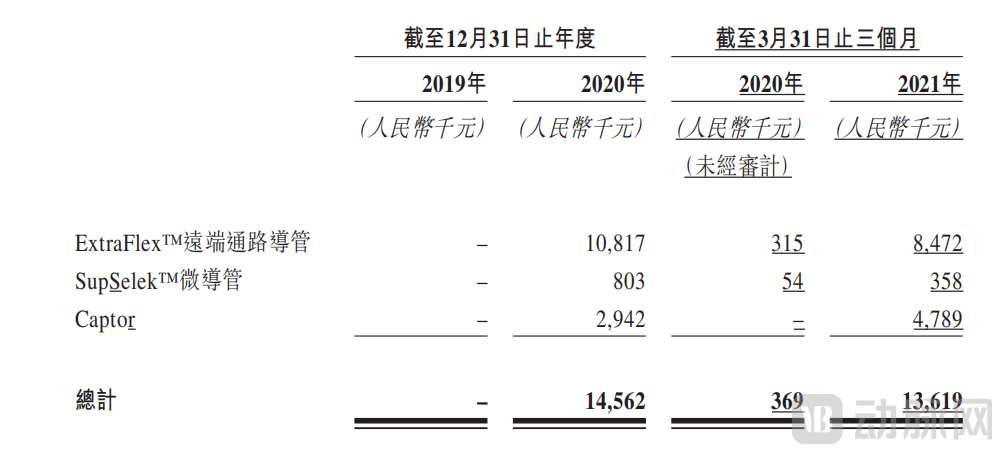

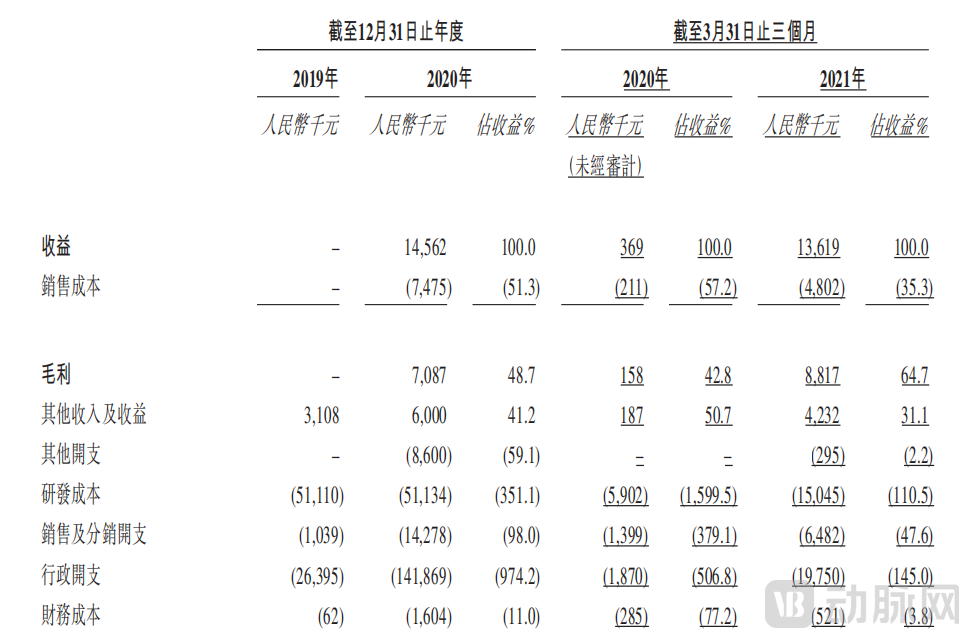

To date, HeartCare has already4 Commercialized Products, among which the CaptorTM thrombectomy device and the extraflex distal access guide catheter are currently the main sources of revenue for HeartCare. The Captor was developed for the treatment of acute ischemic stroke, while the extraflex distal access guide catheter is the first intracranial intermediate catheter in China. According to the prospectus, in 2020, HeartCare's revenue reached RMB 14.562 million, of which the revenue generated by these two commercialized products amounted to RMB 13.57 million, accounting for as high as 93%.

Although its products have been commercialized, HeartCare is currently still facing losses, and the loss amount continues to widen. According to the prospectus,The net losses for 2019 and 2020 were RMB 75.498 million and RMB 216 million, respectively, representing a year-on-year increase of 186.34%.

This is hardly surprising. Loss-making operations and widening losses are a "common ailment" among innovative medical device companies. HeartCare is not alone in this regard; Acandis, which is set to go public next week, shares the same predicament. According to its previously disclosed prospectus, Acandis reported total revenue of RMB 194 million in 2020, with losses reaching RMB 44.292 million.

The primary reason for the losses lies in product research and development.As unprofitable medical device companies, both HeartCare and Acotec Medical reported relatively low total revenues and remain in the R&D investment phase. According to the prospectus, HeartCare's R&D expenditures reached RMB 51.134 million in 2020.

To date, in addition to the four commercialized core products in its product portfolio, HeartCare,plus 19 approved and pipeline products,covering all major stroke subtypes and procedural approaches in the neurointerventional field. According to the plan, HeartCare expects to commercialize nine pipeline products in 2021, and an additional 10 pipeline products between 2022 and 2025, including the world's first rapamycin intracranial drug-eluting balloon catheter for the treatment of intracranial arterial stenosis, to further expand and enrich its product portfolio and meet the growing personalized needs of stroke patients.

Empowered by Multiple Core Capabilities, How Vast Is HeartCare's Potential?

For companies operating in the neurointerventional sector, securing a firm foothold in the market requires sustained "self-sustaining" capability, which entails establishing a robust corporate ecosystem. This not only provides substantial support for business development but, most critically, enables the effective mitigation of market risks.

As a rising star in the neurointerventional field, HeartCare has firmly solidified its competitive "moat" across multiple dimensions despite being founded only five years ago, which is effectively validated by its latest revenue data.According to the prospectus, HeartCare has already achieved significant sales volume growth in Q1 2021, with revenue reaching RMB 13.619 million, nearly matching its full-year revenue for 2020.

Specifically, where is HeartCare's "moat" built?

First, on the talent side.Founder Wang Guohui has accumulated over 16 years of experience in the development and commercialization of neurovascular and cardiovascular devices, having previously worked at MicroPort and APT Medical; Head of R&D Li Zhigang brings 25 years of experience in developing cerebrovascular and cardiovascular interventional devices, having spent many years working at Johnson & Johnson and Medtronic in the United States; Head of Marketing Zhang Ye possesses 20 years of clinical management experience in the cerebrovascular and cardiovascular market in China. In addition, HeartCare has appointed seasoned professionals with extensive relevant experience to all core positions.

Wang Guohui has publicly stated: “Our core competitive advantage still lies in our team, which possesses extensive R&D experience and strong execution capabilities. For a startup, establishing a clear strategy is not difficult; however, implementing it step by step is indeed challenging. Furthermore, our team demonstrates strong learning agility. In the medical device industry, where products update and iterate rapidly, the team must be able to respond swiftly to clinical feedback.”

Secondly, on the platform side.As a technology-innovative enterprise, possessing advanced R&D and production infrastructure will further enhance its competitive advantage in the market. To better support product R&D and manufacturing, HeartCare has designed and developed five technological platforms based on product categories and distinct engineering technologies, namely:Stent manufacturing and processing platform, catheter technology development and manufacturing platform, balloon technology development and manufacturing platform, braiding technology development and manufacturing platform, and interventional product quality platform.

Finally, on the sales side.HeartCare has currently established an in-house sales and marketing team comprising experienced sales personnel. As of March 31, 2021, HeartCare had established an extensive distribution network comprising 41 distributors, collectively covering 1,135 hospitals across 25 provinces in China, including 616 tertiary hospitals and 489 secondary hospitals.

The rapid expansion of commercialized products has broadened HeartCare's distribution network, laying a solid foundation for the sales of the company's subsequently approved products. Furthermore, strong collaborative relationships with third-party distributors will continuously enhance its marketing capabilities, thereby boosting the company's overall profitability. It is reported that as of March 31, 2021, HeartCare had renewed distribution agreements with 22 of these distributors and entered into distribution agreements with an additional 19 distributors.

A Blue Ocean and a Bitter Sea: How Can HeartCare Navigate to Shore?

Undeniably, the future of the neurointerventional field holds great promise.

This is not an unfounded claim, but rather is based on a comprehensive assessment of the market.First, the expansion of market demand.,stroke is a geriatric disease with a high prevalence in the elderly population; given the trend of population aging in China, the number of stroke cases will continue to rise in the future;Secondly, the number and adoption rate of neurointerventional procedures continue to steadily increase., As more innovative neurointerventional procedures are developed for various indications, physicians and patients have more options, leading to a continuous increase in the number of neurointerventional procedures;Then comes the wave of domestic substitution in the medical device sector., as more domestic enterprises increase their investment and launch new products, compared to imported medical devices, high-quality, cost-effective Chinese-made medical devices will gain broader recognition and greater competitiveness.

Finally, Favorable Policies to Advance Stroke Treatment, such policies facilitate innovative development and industrial upgrading in the medical device industry, further driving market growth. Specifically, from 2016 to 2019, the National Health Commission issued numerous detailed policies and guidelines outlining comprehensive plans and measures to advance stroke treatment, including 《Guiding Principles for the Construction and Management of Hospital Stroke Centers (Trial)》 and 《Notice on Further Strengthening the Management of Stroke Diagnosis and Treatment》, among others.

A track brimming with imagination never lacks followers, and behind the vast market and high growth rate lies fierce market competition. According to incomplete statistics from VCBeat, as of now,In China's neurointerventional field, there are already at least 24 innovative companies,Sixty investment institutions are betting on the neurointerventional sector. Additionally, companies in this field are predominantly adopting a "full-pipeline layout," which means that future neurointerventional products entering the market will face numerous competitors and severe homogenized competition.

It is foreseeable that once products from various companies are launched, they will inevitably face fierce competition. An industry insider revealed to VCBeat: "In the future, half of the companies in the neurointerventional field will disappear."

Facing the impending market competition, companies in the neurointerventional sector must prepare for "fierce head-to-head competition." Moreover, given the sector's characteristics of a large market and intense rivalry, enterprises must also brace for the inclusion of neurointerventional products intoCentralized Volume-Based Procurement"Take preventive measures in advance."

Based on previous experience with centralized procurement, neurointerventional products are highly likely to face significant price reductions due to intense market competition. Moreover, once included in the procurement program, manufacturers' profit margins will be substantially compressed, making it difficult to offset price cuts through increased sales volume. Consequently, the research, development, and promotion of innovative products remain the only viable path forward.

Along this core path, HeartCare has already laid out its plans for the future.On the one hand, at the product level, HeartCare planned to submit NMPA registration applications and commercialize nine pipeline products in 2021, including aspiration catheters and aspiration pumps, left atrial appendage occluders, embolic protection systems, carotid and intracranial balloon dilation catheters, hemostatic closure devices, support catheters, and microguidewires.

On the other hand, it is on the sales side.HeartCare plans to recruit additional experienced sales managers and local sales personnel to coordinate the establishment of a specialized local sales and marketing team, laying a solid foundation for expanding future sales channels for its various products.

In addition, HeartCare will further expand the distribution network for its existing and future commercialized products by partnering with other distributors that have a proven sales track record in high-growth regions across China, and plans to coordinate its internal sales and marketing teams to support and train such distributors and establish a localized, professional, and flat sales network.

Overall, China's neurointerventional industry is currently in a rapid ramp-up phase. Various market players are strengthening their product portfolios and distribution networks through diverse strategies. Meanwhile, overseas enterprises that already command a substantial market share are also intensifying their efforts. Industry competition is bound to become increasingly fierce in the future.

HeartCare’s listing can, to a certain extent, effectively ease its financial pressure. However, industry monopolization remains the dominant theme in the current Chinese market. For a sector that relies on technological and financial backing, breaking the existing market monopoly is no easy feat. In the long run, the low penetration rate in lower-tier markets provides Chinese players with a critical window for development. The trend of substitution by Chinese-made products within the neurointerventional industry in China continues to strengthen, and Chinese-made products are poised to eventually compete on equal footing with their foreign counterparts.

In this yet-to-begin battle, HeartCare's performance is highly anticipated.

References:

1. HeartCare and Acandis Medical prospectuses;

2.《HeartCare's IPO Imminent: A Continuation of a Capital Game or the Dawn of the Industry?》, The Paper, August 11, 2021;

3. “HeartCare’s Wang Guohui: Rooted in Zhangjiang for 15 Years, Aiming to Be the Guardian of Cardio-Cerebral Health,” Zhangjiang Toutiao, April 3, 2019;

4. 《Tough Business Targeting 14.8 Million "Stroke" Patients? HeartCare Faces Patent Disputes Pre-IPO, Annual Loss Hits 200 Million Yuan》, Shijie, August 18, 2021.