Xinwei Medical Reports 1,287% Revenue Surge in H1 2021: Is the Profitability Tipping Point Here?

HeartCare

Neurointerventional Medical Device Developer

On August 30, less than two weeks after its listing,HeartCareAnnounced the financial results for the first half of 2021.

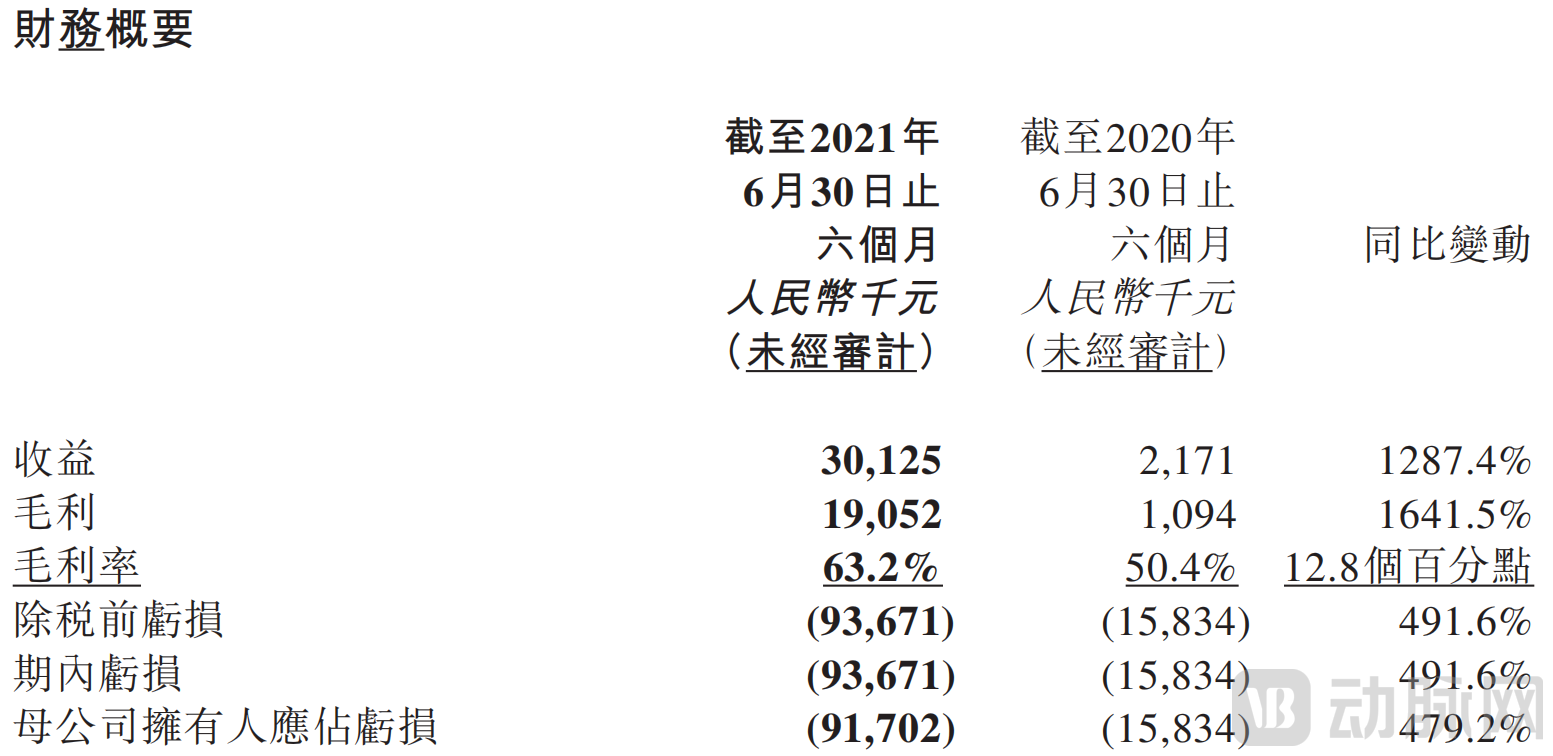

Data shows that,In the first half of the year, HeartCare achieved revenue of RMB 30.125 million, a year-on-year increase of 1,287.4%; gross profit climbed to nearly RMB 20 million, surging more than 16-fold year-on-year; R&D expenses and selling expenses stood at RMB 32.392 million and RMB 18.396 million, respectively, both showing substantial growth compared to the same period last year.

As a rising star in China's medical device sector, HeartCare took merely five years from its establishment to its IPO, with a growth trajectory that stands as a phenomenal benchmark in the neurointerventional field. According to its previously disclosed prospectus, HeartCare only began generating revenue in 2020, yet achieved RMB 14.562 million in its first year through four commercialized products, demonstrating an exceptionally rapid commercialization process.

Entering 2021, HeartCare continued to make significant strides in revenue,First-half revenue has already exceeded last year's full-year revenue by more than twofold., its market potential has been further unlocked.

As a "dark horse" in China's neurointervention sector, what underlying business logic drives HeartCare's rapid revenue growth, and has the company reached its profitability inflection point? On the other hand, by examining key metrics in the semi-annual report, can we uncover HeartCare's potential for future growth? To answer these questions, VCBeat provides a detailed analysis of HeartCare's H1 2021 interim report.

Revenue Surges 1,287.4%, Two Flagship Products Drive Revenue Growth

In terms of sales revenue, neurointervention is the second-largest market segment in the interventional medical device sector; in terms of development stage, neurointervention remains in its early phase, with the core logic of the sector driven by a surge in demand and substitution with products produced in China. Consequently, for medical device companies in China, this generates a synergistic effect between overall volume growth and structural optimization, presenting a massive market opportunity with a ceiling that will be difficult to foresee in the short term.

Based on a clear understanding of the overall neurointerventional sector and its subsegments, HeartCare has established a strategic R&D product layout that is core-focused, comprehensively covers the field, and prioritizes key areas,For stroke management, aggressively treat the condition and comprehensively eliminate all risk factors.

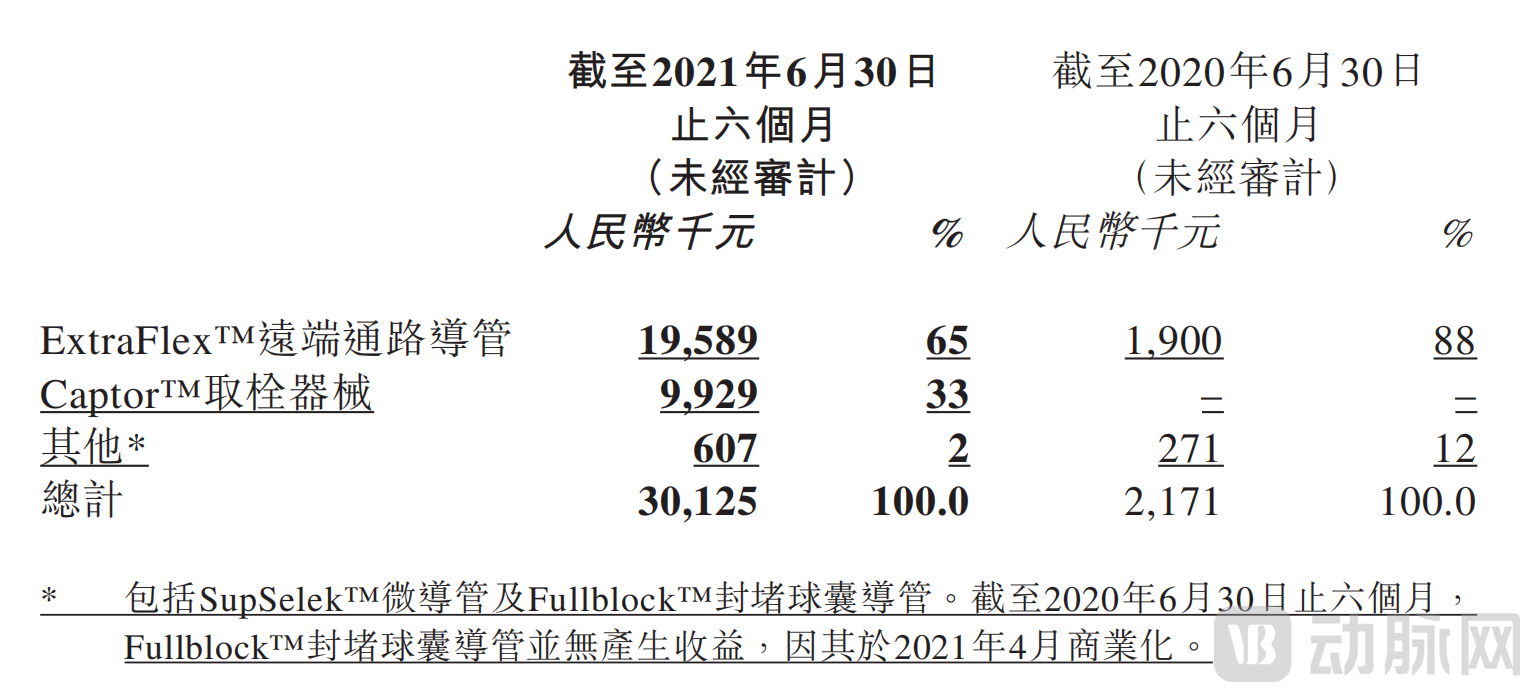

As of now,HeartCare already has 4 commercialized products., among which the CaptorTM thrombectomy device and the extraflex distal access guide catheter are currently the primary sources of revenue for HeartCare. According to the annual report, HeartCare's revenue for the first half of 2021 was RMB 30.125 million, with RMB 29.518 million generated by these two commercialized products, accounting for as high as 98%.

Captor™ Thrombectomy DeviceThe device is used for minimally invasive thrombectomy to remove thrombi or blood clots from the cerebral vasculature of patients with acute ischemic stroke (AIS) caused by intracranial arterial occlusion. Development of this product commenced in November 2016, officially received NMPA approval in August 2020, and began commercial sales in December 2020.

In a comparative clinical trial evaluating the safety and efficacy of patients undergoing stent retriever thrombectomy using the CaptorTM thrombectomy device versus those treated with Medtronic’s Solitaire FR flow restoration device, the CaptorTM device demonstrated non-inferiority, indicating that the product is comparable to top-tier global products.

According to the prospectus, the Captor™ thrombectomy device generated RMB 2.94 million in revenue in 2020, accounting for approximately 20% of total revenue. In the first half of 2021, revenue from the Captor™ thrombectomy device reached RMB 9.929 million, far exceeding its full-year revenue in 2020.

Another flagship product of HeartCare, the Extraflex distal access guide catheter, is currently the first domestically produced large-bore intermediate catheter specifically designed for intracranial use. Its market launch has broken the monopoly of foreign products in the intermediate catheter sector.

The commercial value of its products was quickly reflected in its revenue. As HeartCare's first product to receive approval for market launch, the extraflex distal access guiding catheter is not only a flagship offering but also a key source of revenue. According to the prospectus, the extraflex distal access guiding catheter generated over RMB 10 million in revenue throughout 2020, accounting for as high as 74.2% of total revenue.In 2021, the Extraflex distal access guide catheter generated H1 revenue of RMB 19.589 million, serving as the primary driver of HeartCare's significant first-half revenue growth.

In addition to the surge in revenue, the dramatic leap in gross profit is equally noteworthy. According to the semi-annual report, HeartCare’s gross profit for the first half of 2021 reached RMB 19.052 million, representing a nearly 16-fold year-on-year increase. This growth was driven on one hand by rapidly expanding revenue, and on the other by the relatively high gross profit margin of the Captor™ thrombectomy device.

Charting a New Growth Curve Amid Losses

While financial losses may appear unfavorable for a company, often evoking negative connotations such as poor management, this is actually far from uncommon in the innovative medical device sector. Operating at a loss or reporting inflated losses is a "common phenomenon" among medical device companies that have yet to achieve profitability or have only recently turned a profit.

According to the prospectus, HeartCare's net losses in 2019 and 2020 were RMB 75.498 million and RMB 216 million, respectively, representing a year-on-year increase of 186.34%. In the first half of 2021, HeartCare's net loss reached RMB 93.671 million, maintaining a high-growth trajectory.

However, this should not simply be classified as a "bad thing," because the primary cause of the losses lies in product R&D and market investment. This indicates that HeartCare is currently still in an R&D investment phase, fully dedicated to building its proprietary ecosystem and continuously strengthening its own "moat."According to the semi-annual report, HeartCare's R&D expenses and sales expenses for the first half of 2021 were, respectively,RMB 32.392 millionand18.396 million RMB, all of which recorded significant growth compared to the same period last year.

Specifically in terms of R&D.To date,HeartCare has 7 approved products and 16 products under development., covering all major stroke subtypes and procedural approaches in the neurointerventional field. According to the plan, HeartCare expects to commercialize 9 products under development in 2021, and an additional 10 products under development between 2022 and 2025,including the world's first sirolimus intracranial drug-eluting balloon catheter for the treatment of intracranial arterial stenosis, which has currently entered the Special Review Procedure for Innovative Medical Devices, further expanding and diversifying the product portfolio to meet more personalized needs of stroke patients.

To better support product R&D and production, HeartCare has designed and established seven technology platforms based on product categories and different engineering technologies, namely:Stent manufacturing and processing platform, catheter technology development and manufacturing platform, balloon technology development and manufacturing platform, and interventional product quality platform. In addition,The drug-device combination platform and the active medical device platform will also be rapidly launched in the near future, providing more comprehensive support for R&D and production.

On the other hand, it involves market promotion.It is reported that HeartCare has not independently established its own sales team, with marketing relying entirely on third-party distributors. To date, HeartCare has established an extensive distribution network comprising over 80 distributors,Collectively covers over 1,400 hospitals across 29 provinces (municipalities and autonomous regions) in China capable of performing neurointerventional procedures.

For companies in the neurointerventional sector, establishing a firm foothold in intense market competition requires a sustainable self-funding capability—that is, continuously prioritizing investments in product R&D. As evident, HeartCare currently has 16 products in its development pipeline, making a substantial increase in expenditures inevitable. At the same time, however, it is crucial to recognize HeartCare's tremendous potential for the future.

On the one hand, HeartCare has successfully commercialized multiple products, and its proven commercialization expertise will undoubtedly be effectively applied to other pipeline products, which to a certain extent ensures the quality of these products under development;On the other hand, HeartCare's products have already completed market access procedures in the vast majority of provinces (municipalities, and autonomous regions) in China, and a marketing team comprising experienced sales professionals has been established. These advantages will lay a solid foundation for the future growth of HeartCare's sales revenue.

For HeartCare, the company is currently still in a critical ramp-up phase. Substantial financial resources have been invested in R&D and market promotion, leading to a significant widening of losses. However, it cannot be overlooked that HeartCare’s investments are already yielding rapid returns, which are growing increasingly robust. Its market potential is expected to be further unleashed in the near future.

Standing at a new market opportunity, how much growth potential remains for HeartCare?

According to incomplete statistics from VCBeat,Hillhouse Capital, Chende Capital, SDIC Innovation Capital, Anlong Capital, Better Life Capital, Sequoia Capital China, Huagai Capital, Olympus Capital Asia, Qianhai Fund of Funds, Cowin CapitalOver 60 investment institutions, among others, have already invested substantial capital in the neurointerventional field, unanimously expressing continued optimism regarding the sector.

Capital flows are inherently directional. The neurointerventional sector has garnered significant attention due to its vast market potential, rapid growth rate, upstream technological drivers, and supportive national policies.

Currently, stroke is the leading cause of death among the Chinese population.According to data from China Insights Consultancy, in 2019, the number of stroke patients in China reached 14.8 million, including 11.9 million patients with ischemic stroke and 2.9 million patients with hemorrhagic stroke, with the annual incidence of ischemic stroke reaching 2.3 million cases.

On the other hand, the penetration rate of neurointerventional procedures in China is relatively low compared to that in developed countries.In the United States, following the 2015 AHA guidelines' confirmation of thrombectomy as a first-line treatment for ischemic stroke, coupled with technological advancements, the adoption rate of thrombectomy rapidly increased from 1.4% in 2015 to 11.8% in 2019. In contrast, China's thrombectomy adoption rate remained at only 1.7% in 2019. However, driven by a combination of favorable factors—including technological innovation, supportive government policies, and sustained growth in per capita disposable income and healthcare expenditure—the adoption rate is projected to reach 42.9% by 2030.

Lastly, favorable policies are advancing stroke treatment.These policies help promote the innovative development and industrial upgrading of the medical device industry, further driving the growth of the medical device market. Specifically, from 2016 to 2019, the National Health Commission issued a series of detailed policies and guidelines that outlined specific plans and measures to advance stroke treatment, including the "Guiding Principles for the Construction and Management of Hospital Stroke Centers (Trial)" and the "Notice on Further Strengthening the Management of Stroke Diagnosis and Treatment", among others.

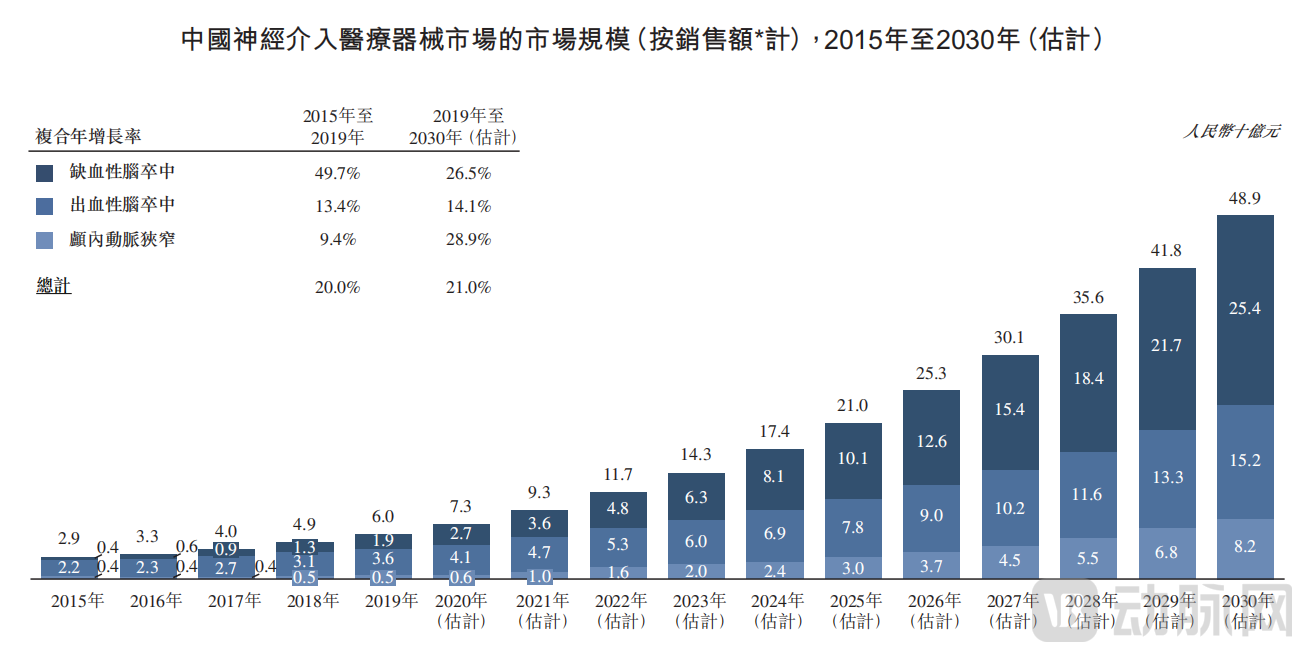

It is reported that,The market size of neurointerventional medical devices in China increased from RMB 2.9 billion in 2015 to RMB 6.0 billion in 2019, at a compound annual growth rate (CAGR) of 20%, and is projected to further increase to RMB 49.8 billion by 2030, with a CAGR of 21% from 2019 to 2030.

While the market undoubtedly represents a blue ocean, competition remains equally fierce. As is widely known, foreign enterprises such as Medtronic and Stryker have dominated 90% of the neurointerventional device market share in China for years. The remaining 10% of the market space has already become a cutthroat red ocean for manufacturers of neurointerventional devices produced in China.

According to statistics, as of now, there are at least 24 innovative enterprises in the neurointerventional sector in China. Prior to HeartCare's listing, Peijia Medical and Truendo Medical had already successfully gone public. On the other hand, companies in the neurointerventional field generally adopt a "full-pipeline layout," which means that future neurointerventional products will face numerous competitors upon launch, with severe homogeneous competition.

Facing the impending "war", companies in the neurointerventional sector must prepare for "close-quarters combat". Moreover, given the sector's vast market scale and intense competition, enterprises must also take "advance precautions" regarding the inclusion of neurointerventional products in volume-based procurement.

Based on previous experience with volume-based procurement (VBP), neurointerventional products are highly likely to undergo significant price reductions due to intense competition. Once included in the procurement program, corporate profits will be substantially impacted, making it difficult to offset price cuts with increased sales volumes. Consequently, the research, development, and commercialization of innovative products remains the only viable path forward.

Along this core pathway, HeartCare has already laid out a strategic roadmap for the future.On one hand, it is on the product side.。HeartCare plans to submit NMPA registration applications and commercialize nine products under development in 2021, including aspiration catheters and aspiration pumps, left atrial appendage occluders, embolic protection systems, carotid balloon dilation catheters and intracranial balloon dilation catheters, hemostatic closure devices, support catheters, and micro guidewires.

On the other hand, it lies on the sales side.HeartCare plans to systematically build a specialized local sales and marketing team by recruiting additional experienced sales managers and local sales personnel, thereby laying a solid foundation for expanding future sales channels for its diverse product portfolio.

In addition, HeartCare will further expand the distribution network for its existing and future commercialized products by partnering with distributors that have a proven sales track record in high-growth regions in China, and plans to coordinate its own sales and marketing teams to support and train such distributors and establish a localized, professional, and flat sales network.

A highly promising track never lacks followers, yet it inevitably yields industry leaders. HeartCare, with its forward-looking product portfolio, high R&D efficiency, and progressively robust channel coverage and service capabilities, deserves close attention from the industry.