Emerging Hotspots in Domestic Substitution of Medical Devices: Industries Poised for Breakthrough

Singular Medical

Developer, Manufacturer, and Seller of Cardiac Rhythm Management Products

MicroPort

High-end Medical Device R&D and Manufacturer

Mindray

Medical Device R&D Manufacturer

Achieving domestic substitution has long been an enduring topic in China's medical device industry, and has consistently served as a development plan and goal across numerous sub-sectors.

Recently, a notice regarding the 《Guiding Standards for the Review of Government Procurement of Imported Products (2021 Edition)》, jointly issued by the Ministry of Finance and the Ministry of Industry and Information Technology, has been leaked. The notice clearly stipulates the proportion requirements for government agencies (public institutions) to procure China-produced medical devices and instruments.

Among them, 137 types of medical devices require 100% procurement of products produced in China; 12 types require 75% procurement of products produced in China; 24 types require 50% procurement of products produced in China; and 5 types require 25% procurement of products produced in China. The procurement scope covers multiple categories, including patient monitors, imaging equipment, in vitro diagnostics (IVD), and high-value medical consumables.

In recent years, relevant policies have consistently supported the domestic substitution of medical devices. On the one hand, certain policies primarily aim to enhance the innovation capacity of domestic medical enterprises, with a focus on improving the quality and efficiency of the medical device approval process, thereby laying the foundation for achieving domestic substitution.

On the other hand, policies are also progressively tightening regulations on the procurement of imported medical devices. Multiple provinces and municipalities across China have explicitly stipulated in their published government procurement policies to strictly restrict imported medical devices, aiming to increase the market share of domestic medical equipment in healthcare institutions.

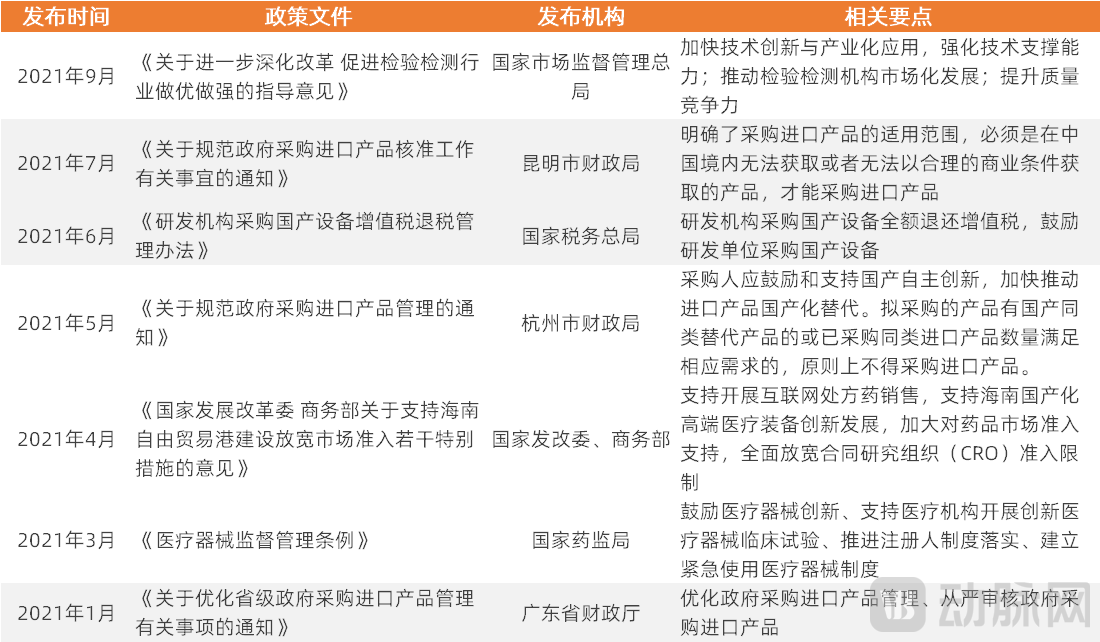

Selected Policies on the Development of Domestic Medical Devices Since the Beginning of This Year

Selected Policies on the Development of Domestic Medical Devices Since the Beginning of This Year

As early as 2007, the Ministry of Finance issued a notice on the "Measures for the Administration of Government Procurement of Imported Products", primarily to promote and facilitate the implementation of government procurement policies for independent innovation, and to regulate the government's procurement practices regarding imported products.

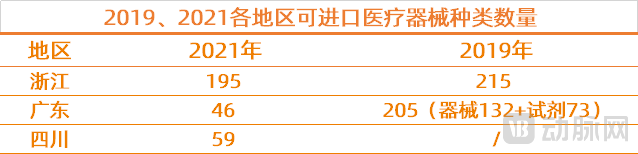

Since the beginning of this year, Zhejiang, Guangdong, and Sichuan provinces have successively released their latest procurement lists for imported medical devices. Notably, the number of imported devices included in Guangdong's procurement list has experienced a precipitous decline.

From Mid-to-Low End to High-End: The Next Step in Domestic Substitution

Driven by continuous policy support, an increasing number of high-quality domestic medical devices are entering the market, and the market share of domestic brands continues to expand. Basic medical device products that previously relied heavily on imports have now largely been localized, while domestic substitution is gradually advancing from the mid-to-low-end market to the high-end market.

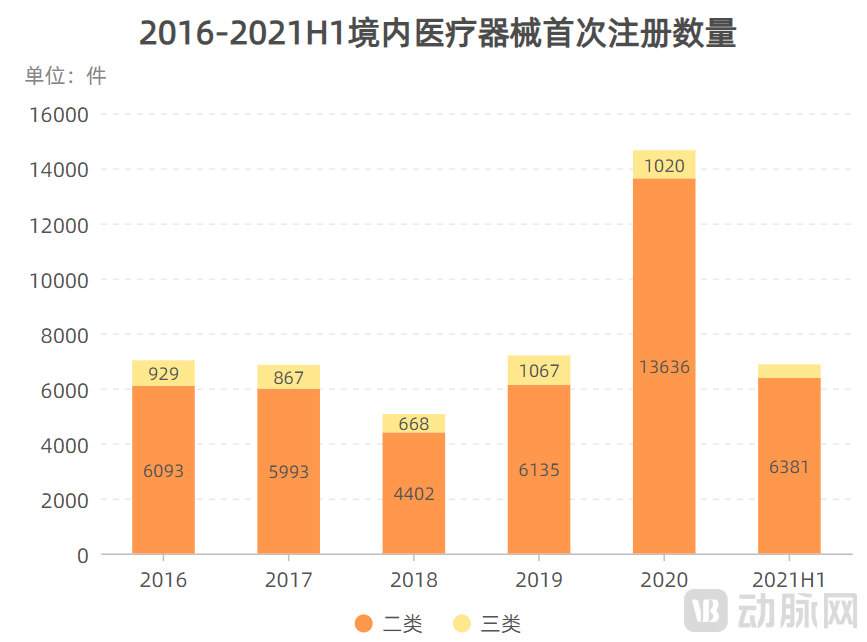

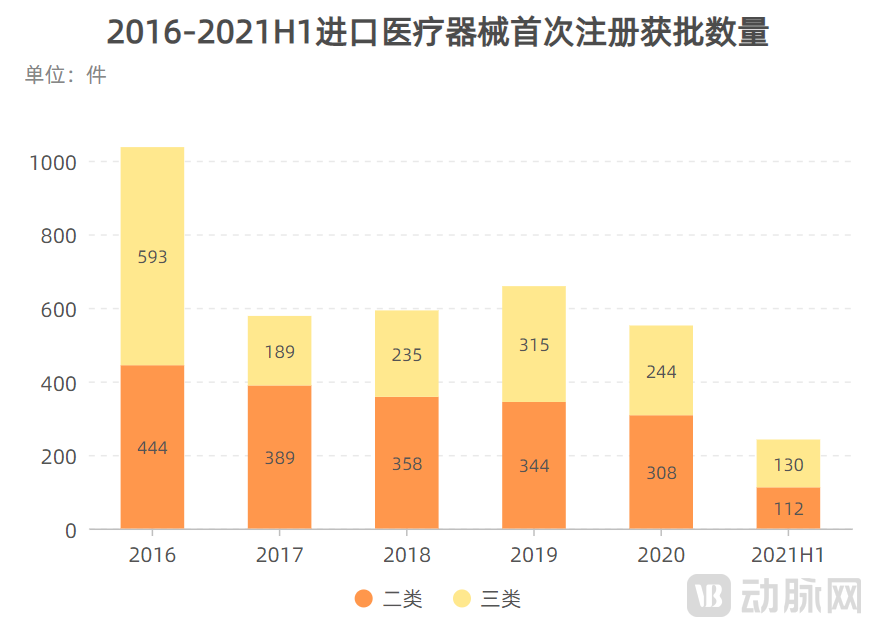

As shown in the chart above, the number of domestically approved Class II and Class III medical devices has generally been on an upward trend in recent years. Impacted by the pandemic in 2020, the number of approved devices experienced explosive growth. Conversely, over the past six years, the number of imported medical devices receiving initial approval has exhibited an overall year-on-year declining trend.

As can be seen, the number of approvals for domestic Class II medical devices far exceeds that for imported Class II devices, indicating that import substitution has been largely achieved in the mid- to low-end medical device sector. Meanwhile, the number of approvals for domestic Class III devices is not only steadily increasing but has also surpassed the total for imported Class III devices, which, to a certain extent, signifies that the pace of domestic substitution in the high-end medical device market is beginning to accelerate.

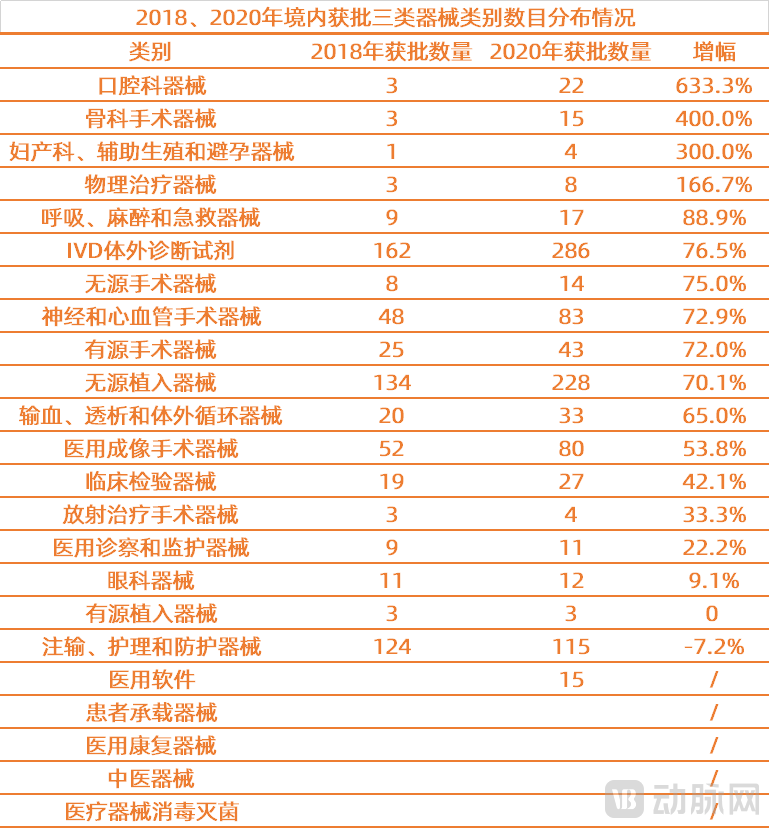

In terms of approved product categories, a comparison of the full-year approval data for domestic Class III medical devices in 2018 and 2020 reveals that over this two-year period, the growth in the number of approvals for dental devices, orthopedic surgical devices, obstetrics and gynecology/assisted reproductive and contraceptive devices, physical therapy devices, and respiratory, anesthesia and emergency devices ranked in the top five. However, the absolute approval volumes for these five categories remained at a relatively low level.

These five major categories—in vitro diagnostic (IVD) reagents, non-active implantable devices, devices for infusion, nursing and protection, neurological and cardiovascular surgical devices, and medical imaging devices—have consistently ranked among the top five in terms of approvals. This trend continued in the first half of 2021 (the approval status of Class III medical devices in H1 2021 will be further analyzed in the following sections).

Which fields have achieved domestic substitution?

Based on approval data, domestic substitution has begun to accelerate or has even been achieved in most sub-sectors of China's medical device industry. Specifically, which sectors in China have already overcome technological barriers and essentially achieved import substitution (with domestically produced products accounting for over 50%)?

Biochemical diagnostics is one of the earliest sub-sectors of the in vitro diagnostics (IVD) industry to emerge in China and has long served as a routine diagnostic test in hospitals. Currently, domestic brands in China's biochemical diagnostics sector have achieved a market share of 70%, effectively completing the import substitution process.

Compared to other sub-sectors within IVD, biochemical diagnostic reagents have relatively low technical barriers. Furthermore, when imported brands entered China in the late 20th century, imported biochemical diagnostic reagents were generally priced higher due to production costs, customs inspection, and tariffs. Consequently, biochemical diagnostic reagents became the entry point for numerous domestic companies to enter the in vitro diagnostics sector and achieve import substitution.

With continuous technological advancements and accumulated experience in biochemical diagnostic reagents, Chinese enterprises, aligning with industry development trends, have also begun to ramp up their efforts in biochemical analyzers. They are steadily catching up with imported brands in terms of technology and performance, gradually achieving domestic substitution in the biochemical diagnostics market.

Currently, China's biochemical diagnostics sector is largely dominated by domestic brands, yet market concentration remains relatively low. Major players include Mindray, Kehua Bio-engineering, Jiuqiang Biotechnology, etc.

The development process of domestic patient monitors, to some extent, also parallels the growth history of Mindray.

In the 1990s, China's patient monitor market was monopolized by foreign companies. Leveraging the experience accumulated from its early distribution of imported products, Mindray gradually transitioned to independent research and development, subsequently launching the first domestically produced pulse oximetry monitor and the first domestically produced multi-parameter monitor to the market, thereby breaking the monopoly of foreign giants.

Subsequently, Mindray continuously increased its R&D investment and consistently optimized its products according to actual clinical needs, with patient monitors undergoing a transition from "MCU-centric to PC-centric to network-centric." Currently, Mindray ranks third in the international market and first in the domestic market for patient monitors, with a domestic market share exceeding 60%.

In 1998, coronary stents began to be widely adopted in China. Over the subsequent years, both the volume of percutaneous coronary intervention (PCI) procedures and coronary stent utilization experienced exponential growth. However, China's research and development of cardiovascular stents started relatively late. In the early stages, the relevant market in China was largely dominated by multinational giants such as Johnson & Johnson, Medtronic, and Boston Scientific. This situation changed in 2004.

In 2004, MicroPort launched the first drug-eluting coronary stent produced in China. Subsequently, new products from Lepu Medical and JW Medical were introduced in succession. Leveraging superior technical performance and relatively competitive pricing, coronary stents produced in China began to rapidly scale up in volume. According to statistical data from the Surgical Implant Professional Committee of the China Association of Medical Devices Industry, the market share of stents produced in China reached 59%, 65%, and 70% in 2006, 2007, and 2008, respectively. Coronary stents produced in China "successfully turned the tables," achieving import substitution.

Beyond the aforementioned fields, areas such as Digital Radiography (DR) and cardiac occluders have also achieved remarkable success in domestic substitution. Summarizing the experiences of medical device sub-sectors in China that have already realized import substitution reveals that technological capability, cost-effectiveness, and brand strength are the key success factors for domestic enterprises. Furthermore, throughout this process, most companies have chosen to launch their products before the domestic competitive landscape has fully taken shape, thereby securing a first-mover advantage, rapidly capturing market share, and ultimately ascending to the top tier of domestic manufacturers.

Domestic Substitution: What Are the Next Anchor Points?

Although China's medical device market has sustained its robust growth momentum in recent years and has become the world's second-largest market, it is undeniable that imports still dominate multiple sub-sectors within the domestic medical device industry.

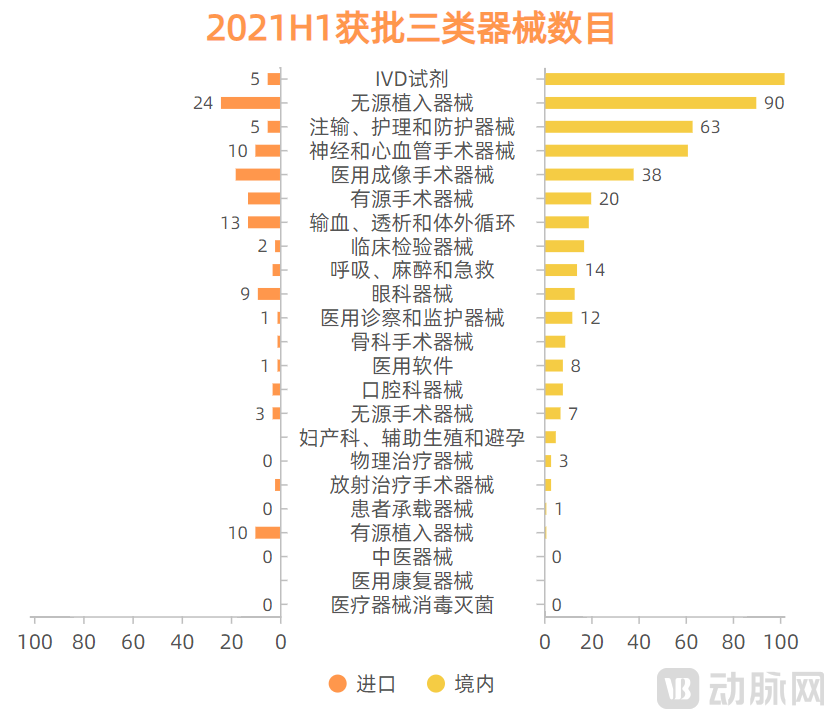

To this end, VCBeat analyzed the number of approved Class III medical devices produced in China and those imported in the first half of 2021, along with the main categories of imported products, to assess the status of domestic substitution across different sectors and identify the next track likely to achieve localization in the future.

An analysis of the Class III medical devices approved domestically and via import in the first half of 2021 reveals that imported products still account for a significant proportion in sectors such as active implantable medical devices, ophthalmic devices, medical imaging surgical devices, and active surgical devices. In the active implantable medical device sector, imported products significantly surpass domestic ones.

Among the 10 imported active implantable medical devices approved in the first half of this year, approximately half are ICDs. By definition, an ICD is an electronic device implanted into the patient's thoracic cavity that connects to the heart via transvenous defibrillation leads and is capable of automatically detecting and promptly terminating malignant ventricular arrhythmias.

The ICD integrates both defibrillation and pacing capabilities. When a patient experiences tachycardia, the ICD delivers high-energy electrical pulses to restore a normal heart rhythm; conversely, when bradycardia occurs, it utilizes low-energy electrical pulses to normalize the rhythm. Appropriate use of ICDs can correct ventricular tachyarrhythmias, reduce the incidence of sudden cardiac death, and prolong patient survival. Multiple clinical studies have confirmed that ICD therapy is the optimal treatment for preventing sudden cardiac death.

However, from a technical perspective, the ICD represents a high-tech achievement that seamlessly integrates modern clinical cardiac electrophysiology and pacing technology with advanced microelectronics. Characterized by highly complex system integration, it demands exceptionally rigorous standards for timeliness, efficacy, and safety, while also incorporating the pacing capabilities of a pacemaker. Consequently, it is widely recognized as one of the Class III active implantable medical devices in the industry with the highest technical barriers and the greatest R&D risks.

Although the clinical application value of the product is evident, the penetration rate of implantable cardioverter-defibrillators (ICDs) in China remains low. According to data reported by the Arrhythmia Intervention Quality Control Center of the National Health Commission, the number of ICD implantations in mainland China in 2018 was 4,471, which is significantly lower than the implantation volumes in some European and American countries.

High Costs Pose a Major Barrier to the Widespread Adoption of ICDs

Cost is a major factor contributing to the low adoption rate of ICD devices in China. Currently, two types of ICDs are commonly used in clinical practice, with prices typically ranging from RMB 60,000 to 80,000, and some models costing as high as RMB 100,000 to 150,000. Although a portion of the expenses can be reimbursed through medical insurance, it still imposes a substantial financial burden on ordinary families.

Furthermore, the absence of clear treatment reference guidelines in China's ICD sector, coupled with inadequate market education, are also significant factors limiting the growth of ICD implantation volume in China.

Furthermore, potential safety risks remain in the long-term application and promotion of ICDs. In April this year, Medtronic initiated a voluntary Class I recall of its ICD products due to battery-related issues. Previously, companies such as Boston Scientific and St. Jude Medical (acquired by Abbott) have also conducted voluntary recalls of ICD products. As Class III implantable medical devices, the safety of ICDs is of paramount importance.

Which Chinese companies are entering the high-barrier ICD sector?

In terms of the market, China's ICD sector remains monopolized by imported products, with no domestically manufactured ICDs currently commercially available.

According to the "2019-2023 China Implantable Cardioverter Defibrillator (ICD) Market Analysis and Feasibility Study Report", the current domestic ICD market in China is primarily dominated by brands such as Boston Scientific, Medtronic, Biotronik, and St. Jude Medical.

Under the monopoly of imported products, some domestic brands have begun to venture into this highly R&D-intensive field, striving to capture market share with original products.

As early as 2014, MicroPort Medical and Sorin (the rhythm management business of LivaNova) established the joint venture "MicroPort Sorin CRM" to jointly develop, manufacture, and market cardiac rhythm management devices (including pacemakers, ICDs, and CRTs).

In 2015, LivaNova CRM launched the PLATINUM™ series of implantable cardioverter-defibrillators (ICDs). Featuring the world's longest battery longevity of 14.3 years, the product reduces the risks associated with frequent ICD replacements and has been well received in overseas markets. In 2018, MicroPort announced the completion of its joint acquisition of Sorin alongside Yunfeng Capital. Since then, MicroPort has gained a comprehensive product portfolio in cardiac rhythm management (CRM).

Another company with a strategic presence in the ICD sector is the Suzhou-based Singular Medical. Since its establishment in 2017, Singular Medical has consistently focused on the R&D and commercialization of Class III active medical devices in the Cardiac Rhythm Management (CRM) field, with ICDs serving as its strategic entry point. It is reported that Singular Medical’s first-generation ICD product has entered the registration testing phase and has applied for the Innovative Medical Device designation.

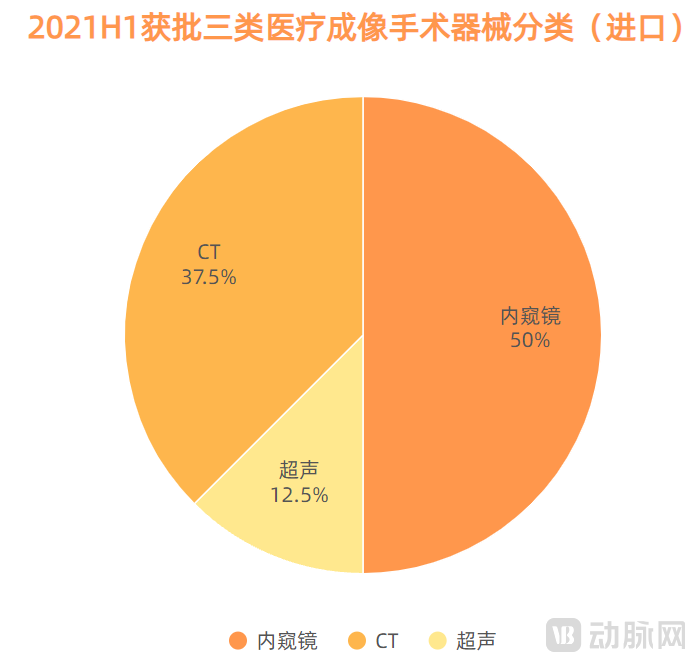

In the field of medical imaging and surgical devices, the number of approved domestic products actually exceeds that of imported ones; however, approved products are more heavily concentrated in the CT and MRI sectors. Among the 18 imported Class III medical imaging and surgical devices approved in the first half of this year, endoscopes account for a significant proportion.

Since its inception in the 19th century, the endoscope has undergone continuous development and is now widely applied in clinical departments such as gastroenterology, respiratory medicine, general surgery, otorhinolaryngology, orthopedics, urology, and gynecology, becoming a vital medical device for diagnosis and treatment. To date, endoscope technology has advanced through four generations: rigid endoscopes, semi-flexible endoscopes, fiberoptic endoscopes, and electronic endoscopes. Owing to their superior imaging quality, electronic endoscopes have become the mainstream in the market.

Currently, driven by the growing clinical demand for minimally invasive treatments, endoscopes used in minimally invasive surgery are once again experiencing significant development opportunities. According to data published by Evaluate MedTech, the global endoscope market reached $20.9 billion in sales in 2019, and is projected to continue growing at a compound annual growth rate (CAGR) of 6.3% over the next five years, reaching $28.3 billion by 2024.

However, the introduction of endoscopic examination and minimally invasive therapy in China occurred relatively late, which has hindered the development of domestic endoscope enterprises to a certain extent. Currently, China's endoscope market remains dominated by imported brands. 《China Medical Device Industry Development Report 2019》 shows that overseas giants such as Karl Storz, Olympus, and Stryker account for over 90% of the rigid endoscope market share, leaving enormous room for domestic substitution.

Gradual Mastery of Core Technologies Creates Opportunities for Endoscope Domestic Production

For devices with high technological barriers such as endoscopes, achieving breakthroughs in core components and technologies is clearly the top priority for domestic localization.

It is understood that the core components of an endoscope include lenses, image sensors, image processors, and light sources. Currently, Chinese enterprises have achieved breakthroughs in core components such as image processors and light sources, providing strong support for the domestic production of endoscopes.

Regarding image sensors, with the rise of CMOS image sensor technology, traditional CCD image sensor technology is gradually being replaced. Compared to CMOS, CCDs are more difficult to manufacture, their core technologies are restricted by foreign giants, and they carry a higher cost. In contrast, CMOS not only features relatively lower technical barriers but also offers low power consumption and reduced noise. Its application has created opportunities for the production in China of endoscopes.

With the continuous advancement of technology, endoscopes are increasingly integrating with numerous innovative technologies, materials, and manufacturing processes. Evolving toward miniaturization, multifunctionality, and high-quality imaging, this convergence has given rise to a variety of innovative product categories. Currently, 3D endoscopes, single-use endoscopes, and capsule endoscopes rank among the product categories attracting the highest market attention.

3D Endoscope: More Intuitive Imaging

In terms of imaging, 3D and 4K endoscopes offer more intuitive and clearer visualization compared to conventional endoscopes, making them the current focal point of technological R&D for most manufacturers. Among these, 3D endoscopes can, to a certain extent, restore the advantages of natural vision. The images synthesized by the image processor deliver a stereoscopic effect, making the anatomical layers in the surgical field more distinct and thereby facilitating improved surgical efficiency.

Just this year, Weigao Robotics' 3D laparoscope was successfully approved. Subsequently, Surui Medical and MicroPort successively obtained NMPA approval for their 3D electronic laparoscopes, demonstrating that China has made preliminary progress in the field of 3D endoscopy.

Disposable Endoscopes: Endoscopes Become Consumables, Five Companies Receive NMPA Approval

Due to their complex structure, traditional endoscopes are difficult to thoroughly clean and disinfect, which also leads to a risk of cross-infection when the same endoscope is reused across different patients.

Single-use endoscopes have thus emerged as an effective solution to this problem. They not only demonstrate excellent performance in preventing cross-infection, but also eliminate wear and tear on the device due to their single-use nature, ensuring that every endoscope remains in optimal condition upon unboxing. This, to a certain extent, enhances surgical efficiency.

According to incomplete statistics, five companies in China's single-use endoscope sector have currently obtained NMPA registration certificates, and their products have gained recognition from market regulators.

NMPA Approval Status of Disposable Endoscopes in China (Partial)

Capsule Endoscopy: Convenient Operation, Addressing the Pain Points of Traditional Gastrointestinal Endoscopy

For a long time, the incidence of gastrointestinal diseases in China has remained consistently high. However, due to the significant discomfort caused by the invasive nature of traditional gastrointestinal endoscopy, patients' willingness to undergo the examination has been low. In contrast, capsule endoscopy requires no anesthesia, is comfortable and safe, and achieves diagnostic accuracy comparable to conventional endoscopy, making it increasingly favored by patients.

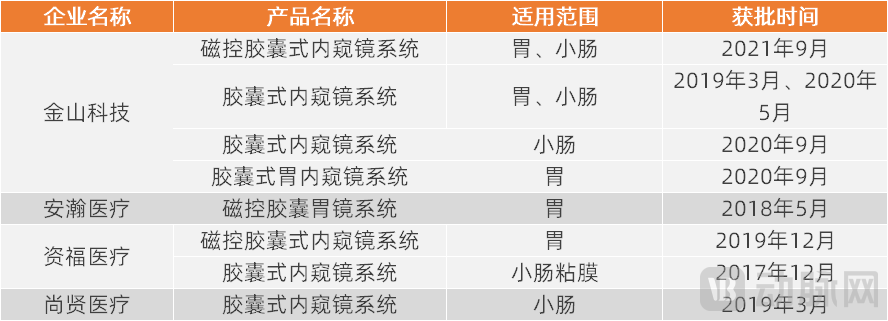

Furthermore, capsule endoscopes also demonstrate excellent performance in preventing cross-infection. It is reported that Ankon Technologies, Jinshan Science & Technology, Zifu Medical, and Shangxian Medical have all launched capsule endoscopy products, which are distributed globally.

NMPA Approval Status of Capsule Endoscopes in China (Partial)

Beyond the aforementioned categories, endoscopic ultrasound (EUS)—a gastrointestinal examination technology that integrates endoscopy with ultrasonography—also represents an innovative direction in the endoscopy field. Currently, Olympus, Fujifilm, and Pentax have already launched commercial products in the EUS sector. In China, SonoScape has already established a strategic presence in this area; however, overall, no Chinese-made EUS systems have yet been commercially launched in China, leaving substantial room for domestic substitution as well.

Among the imported passive implantable medical devices approved in the first half of this year, neurological and neurosurgical implants, joint replacement implants, and orthopedic filling and repair materials constituted the major import categories. Notably, the neurointerventional market associated with neurological and neurosurgical implants is one of the key sectors in China that urgently requires domestic substitution.

According to the prospectus of Zhuoyu Medical, foreign enterprises such as Medtronic, Johnson & Johnson, and Stryker currently account for 93% of China's neurointerventional market, while domestic companies are building a complete product line from scratch.

The neurointerventional market primarily comprises ischemic devices for ischemic stroke and arterial stenosis, hemorrhagic devices for aneurysms, and access devices that assist in establishing vascular access. Among them, ischemic devices command a larger market potential due to a higher patient volume; hemorrhagic devices face higher technical barriers owing to disease complexity and greater procedural difficulty; whereas access devices, with relatively lower technical barriers, have already achieved partial production in China.

In terms of capital, the neurointervention sector has been highly favored by investors. According to non-exhaustive statistics from VCBeat, there have been eight financing and M&A deals in the neurointervention field since the beginning of this year. Compared to the coronary intervention sector, which has already successfully achieved domestic substitution, it can be said that neurointervention currently faces a more favorable capital environment.

In terms of product quality, neurointerventional products produced in China have shown significant improvement, with certain performance indicators of some products even surpassing those of imported counterparts. However, the number of balloons, covered stents, flow diverter stents, and arterial stents produced in China that have been launched to market remains relatively limited, and these related sectors still require further penetration.

The reasons for the low penetration rate of Chinese-produced neurointerventional products are multifaceted. Factors such as product pricing, patient awareness, cerebrovascular disease screening, and the number of stroke centers have all exerted a certain impact, representing the key areas where future neurointerventional devices need to achieve breakthroughs.

Final Thoughts

In addition to the ICD, endoscope, and neurointervention fields mentioned earlier, imports also dominate in China for heart valves, artificial blood vessels, and core components of medical imaging equipment.

Over the past decade, China's medical device industry has experienced rapid and sustained growth, establishing itself as the world's second-largest medical device market. However, the overall localization rate remains relatively low. The vast import substitution market is poised to become a fiercely contested battleground for domestic medical device companies in the future.

The path to domestic substitution is long and arduous. Particularly at this stage, the areas most urgently requiring domestic replacement are predominantly high-end medical devices with significant technical barriers. However, on one hand, the vast population in China translates into substantial healthcare demand; on the other hand, continuous favorable policies support the development of domestically produced medical devices. These factors collectively provide valuable opportunities for the growth of domestic enterprises.

It is anticipated that in the future, as an increasing number of enterprises intensify their innovation and R&D efforts, more sectors within China's healthcare industry will achieve domestic substitution, and a large number of innovative entities will emerge rapidly.

Reference: 【100-Page In-Depth Report on Medical Devices - Part II of the Series】The Golden Decade: Who Will Take the Lead? —— Industrial Securities Healthcare