Largest Domestic Structural Heart Device Deal: Lifetech Acquires Huayi Shengjie for RMB 1.87B to Secure PFO Occluder Leadership

LifeTech

Suppliers of Congenital Heart Defect Occluders

Starway Medical

Research and Development, Production of Cardiovascular Interventional Devices

White Paper + Awards + Forum | 2nd Global Cardiovascular Conference

Heart Future

May 22, 2026,Lifetech Scientific (01302.HK) announced that it intends to acquire approximately 96.46% equity interest in Starway Medical Co. Ltd. for approximately RMB 1.8733 billion., the seller is precisely a shareholding platform under Hillhouse Capital, with the consideration to be settled entirely in convertible bonds, involving no cash whatsoever.

This is a transaction where strategic intent far outweighs financial returns—Lifetech Scientific used a "promissory note" to bring a core competitor in China's congenital heart disease and PFO occluder market under its umbrella, while Hillhouse Capital executed a classic "mature assets for liquidity" exit.

# Who is Starway Medical? What is Lifetech buying?

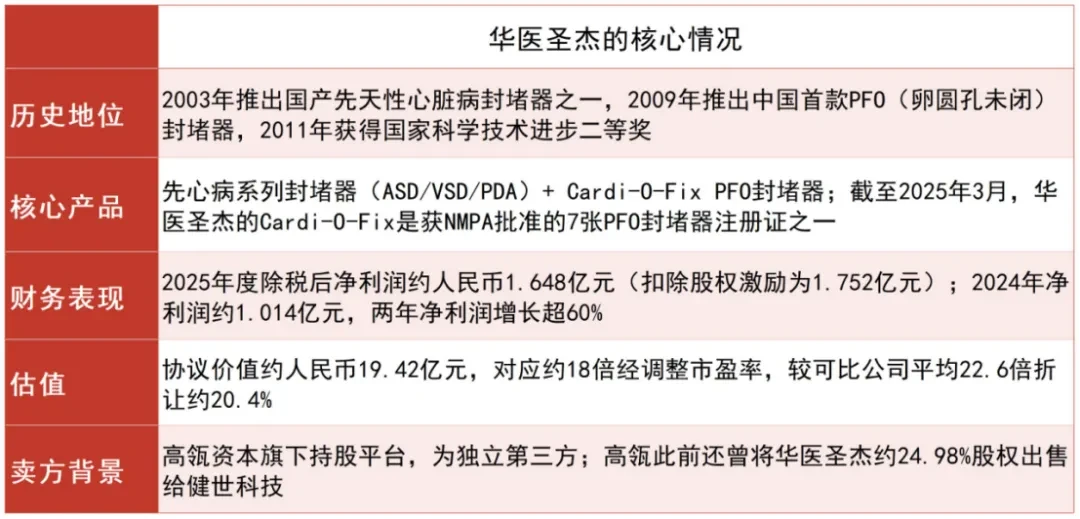

Starway Medical at2002established in Beijing in [year], isChinese Structural Heart OccluderOne of the pioneers in the field, whose history has evolved almost in parallel with the development of this niche market in China:

The core value of Starway Medical lies in China's congenital heart disease occluder market"Third Child"Position. In China's congenital heart disease occluder market,Lifetech Scientific、Starway Medical、Shanghai Shape Memory(Subsidiary of Lepu Medical)The three combined account for90%The above-mentioned share。Lifetech Scientific's acquisition of Starway Medical means that the top two players in this market will merge into a single entity.

# Why now, and why this deal??

(I) Why Hillhouse Is Exiting at This Time

Hillhouse's sale of Starway Medical aligns with its recent consistent investment logic. Since2025Since the second half of the year, Hillhouse has repeatedly executed major divestitures in the mature asset sector, shifting its focus from"Invest Early, Invest in Innovation"Shift focus to continuously revitalizing mature assets.

Starway Medical's annual profit is approximately1.75hundred million yuan, valuation of approximately19100 million yuan, is a mature target with stable operations but plateauing growth potential, presenting a reasonable exit window. Meanwhile, the two structural pressures facing Starway Medical are also intensifying: first, the pricing room in the congenital heart disease (CHD) occluder market continues to narrow due to the impact of centralized procurement policies across various regions; second,PFO`The closure device market, following Abbott`Amplatzer Talisman 2024entered China in [Year], and the competitive landscape is intensifying.

(II) Why Acquire Lifetech?

Lifetech2024full-year revenue was approximately13.59hundred million yuan, three main product lines covering structural heart disease (congenital heart defect occluder+Left Atrial Appendage Occluder), Peripheral Vascular Disease (Covered Stent+vena cava filters), pacing and electrophysiology. Among these, the structural heart disease business is the fastest-growing segment, and the acquisition of Starway Medical precisely strengthens this core strategic direction.

Specifically, what Lifetech can gain from this transaction:

Structural Leap in Market Share:the originally competing domestic congenital heart disease occluders"Second child+The Third One"Through the merger, stronger pricing power and channel control will be achieved in this niche market.

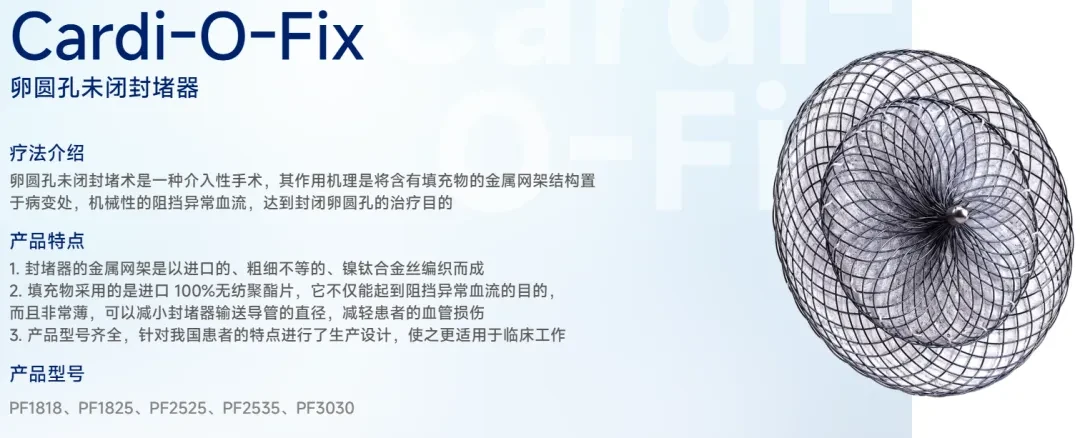

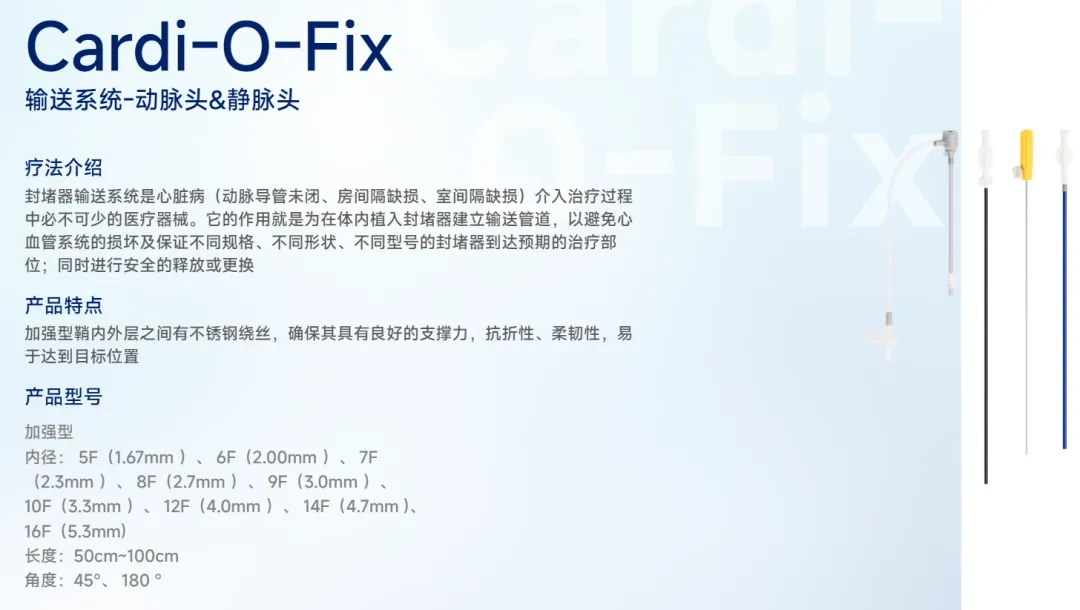

PFORapid Market Entry of the Occluder:Lifetech is currently inPFOThere are no mature commercialized products in the occluder field, while Starway Medical'sCardi-O-Fixare the only few in ChinaPFOOne of the occluder registration certificates.2022ChinaPFOThe number of interventional procedures has reached4At approximately 10,000 procedures, it has ranked first in volume among all structural heart disease interventions, with growth momentum still sustained. This represents a rapidly growing market segment where Lifetech had previously been largely absent.

`Valuation Support from Comparable Companies`:The announcement selected MicroPort Endovastec, Yingtai Medical, ZC Medical, Lepu Cardio, and APT Medical as comparable companies, with an average adjusted P/E ratio22.6times; Starway Medical with18The transaction was closed at a valuation multiple, providing a reasonable margin of safety for the buyer.

(3) CashlessTransaction Structure: Shrewd Strategy or Reluctant Compromise?

What most warrants separate analysis in this transaction is the design of the consideration structure.——Lifetech issued convertible bonds to Hillhouse with no cash payment, at a conversion price of per share.2.5HKD (representing a premium of approximately to the closing price on the announcement date8.2%), Bond Term3Year, Annual Interest3.5%, if not converted upon maturity, it shall be redeemable, at a redemption price of % of the principal1.5fold or produce12.5%The higher of the two Internal Rates of Return shall apply.

This means:

Lifetech Scientific retained all its cash reserves, mitigating the short-term operational impact of the acquisition.

Hillhouse Capital secured stable interest income through the bonds and retained the right to at2.5Hong Kong Dollar/Options to Convert Shares into Lifetech Scientific Shares

If Lifetech's stock price is at3If it rebounds above the conversion price within the year, Hillhouse may elect to convert the bonds into equity to realize additional returns; if it fails to meet expectations, it shall1.5times the principal or12.5% IRRCompensation

Hillhouse also undertakes that, post-closing, at a price not exceeding2.5Hong Kong Dollar/...increase its holdings in Lifetech Scientific's issued shares at the average share price to become the single largest shareholder. This will completely transform Lifetech Scientific's shareholding structure and trigger Hillhouse's nomination of Lifetech Scientific's management.2The rights of the executive directors.

# Value and Risks of the Transaction

Rationality of the Synergistic Logic

Lifetech and Starway Medical are highly complementary in product categories rather than completely overlapping.: at LifetechASDdemonstrates significant advantages in occluders and left atrial appendage occluders, Starway Medical inPFOBoth the occluder and certain congenital heart disease (CHD) occluder categories possess independent brand recognition and clinical reputation. Given that they share procedural settings for structural heart interventions and hospital distribution channels, the frictional costs associated with channel integration are relatively low.

# Product Line Pressures Facing Starway Medical

The announcement candidly acknowledges that,Starway Medical's Structural Heart product line faces ongoing pressure on sales volume and procurement.——This is the common predicament faced by all occluder manufacturers against the backdrop of centralized procurement. Whether CHD occluders will be included in nationwide centralized procurement currently lacks a clear timeline, although precedents for regional procurement already exist. Should such pressures intensify during the three-year bond term, it will impact Starway Medical's net profit, thereby affecting Lifetech Scientific's debt repayment capacity.

Uncertainty in Integration Execution

Starway Medical's Business Integration and Management SuccessionIt was listed in the announcement itself as one of the valuation discount factors. Both companies maintain independent R&D systems, sales teams, and hospital market access networks; the stability of key personnel during the integration process will be the most critical variable at the execution level.

Long-Term Impact of Equity Dilution

If all convertible bonds are converted in full, approximately8.6hundred million new shares, representing approximately of the current issued share capital15.66%。The dilution effect on Lifetech's existing shareholders must be taken into consideration; meanwhile, Hillhouse, through increasing its stake,+The debt-to-equity conversion pathway is expected to result in the relevant party becoming the largest single shareholder of Lifetech Scientific, which will substantially impact its corporate governance structure.

# `Delay`Extended Information and Role-Based Research Recommendations

Supplementary Industry Background: China Structural Heart Disease Occluder Market

Congenital heart disease occluders are the oldest and most mature product category in China's structural heart disease sector. From a global perspective,Abbott(AGA/AmplatzerSeries)accounts for approximately ... of the global55%market share; in China,Lifetech, Starway Medical, Shape Memory (under Lepu Medical)The three combined account for90%With the above market share, the market has become highly localized.

PFOClosure devices are currently a faster-growing sub-sector, in55among adults under [X] years of age,PFOThe prevalence of stroke among patients is as high as50%, with growing awareness of cardioembolic stroke, demand for interventional closure is rapidly expanding. From the perspective of the competitive landscape for registration certificates, as of2025Year3Month, nationwide only7ZhangPFOThe occluder registration certificate has been approved, covering a product category that is still in the early stage of market penetration. Lifetech Scientific’s acquisition of Starway Medical grants it immediate entry into this sector, representing the most forward-looking strategic move in this transaction.

# Key Variables to Monitor Going Forward

Approval Status of the Extraordinary General Meeting of Shareholders: This transaction constitutes a major transaction under the Listing Rules and is subject to shareholders' approval. The circular is expected to be2026Year6Month30Recently dispatched. Barring significant objections, obstacles to approval are minimal.

China Anti-monopoly Review:One of the conditions precedent to closing is obtaining approval from the antitrust review authorities. Given the post-merger increase in market concentration in the congenital heart disease occluder market, whether it will trigger a substantive review warrants close attention.

Developments Regarding Jenscare Scientific: Jieshi Technology had previously held approximately Starway Medical24.98%equity, upon completion of this transaction, TransMed Group will hold the remaining approximately3.54%The equity disposal arrangement has not yet been disclosed, and its shareholder relationship with Lifetech warrants attention.

The Evolutionary Pace of the Centralized Procurement Policy: If CHD occluders are included in China's centralized procurement during the three-year bond term, it will directly impact Starway Medical's profitability and indirectly affect the assessment of Lifetech Scientific's debt servicing capacity.

# How does this affect you?

Correct`Secondary Market Investors`: Key focus should be placed on the comprehensive financial details of Starway Medical disclosed in the circular (currently only profitability data is available, while the asset-liability structure remains to be disclosed), the voting results of the extraordinary general meeting, and the pace at which Hillhouse increases its stake in Lifetech Scientific to become the largest shareholder. The pricing of comparable companies Lepu HeartCare and Acotec provides a reference benchmark for assessing the valuation anchor for Lifetech Scientific following the acquisition.

CorrectStrategies for the Cardiovascular Device Industry orBD# Team: This case provides a zero-cash acquisition+The structural framework of convertible bonds, under conditions of constrained buyer liquidity and relatively stable target asset valuation, constitutes a rational arrangement that balances the buyer's liquidity needs with the seller's exit requirements, making it a sound structural reference for comparable transactions.

CorrectFollowPFO/Clinicians in the congenital heart disease occluder sector orKOL:Should the integration between Lifetech and Starway Medical proceed smoothly, the consolidation of sales channels may lead to competition between the two companies' products within the same sales system, which could temporarily impact the hospital promotion pace for each respective product. In the medium term, a unified clinical support and training system has the potential to enhancePFOThe overall penetration rate of occluders.

CorrectEarly-Stage Investor in the Structural Heart Disease Sector: The signal conveyed by this transaction is——In mature segments such as congenital heart disease (CHD) occluders, the consolidation window has opened, and the M&A valuation of remaining independent players is being repriced. Notably, Shape Memory (a subsidiary of Lepu Medical), another major player in the CHD occluder market, presents the next key M&A issue worthy of analysis: its strategic path toward either independence or industry consolidation.

Comprehensive Cardiovascular Device Solutions for All Indications

Structural Heart Disease → ▌Medtronic

`Vascular Disease` → ▌`VasCare Medical`