"No Cash Spent": Cardiovascular Leader's De Facto Control Shifts Hands Amid $274M Deal

LifeTech

Suppliers of Congenital Heart Defect Occluders

Starway Medical

Research and Development, Production of Cardiovascular Interventional Devices

▲Article Source: Medical Device Hub

▲ Please indicate the above source when reprinting.

May 22, 2026, after the Hong Kong stock market closed,Lifetech ScientificIssued a formal announcement:Proposed at approximatelyRMB 1.873 billionAcquisition of Approximately 96.46% Equity Interest in Starway Medical Co. Ltd for RMB。The consideration consists entirely of convertible bonds, and the company will not pay a single cent in cash.

On that day, Lifetech's stock priceOpened at HK$2.09, reached a high of HK$2.32, closed at HK$2.31, posting a daily gain of 11.59%.——This is the strongest day for the recently sluggish Hong Kong-listed medical device sector.

Image source: Eastmoney.com

However, stock price fluctuations are merely superficial.What truly warrants scrutiny is the hidden shift of power within this transaction.: Tracing up the ownership structure, the seller is Hillhouse Capital; the buyer, Lifetech Scientific, is a long-held portfolio company that Hillhouse invested in six years ago.

This is not a simple transaction, but rather an "asset swap" executed through financial instruments.

Starway Medical was founded in 2002,It is the earliest pioneer in the field of congenital heart disease occluders in China.。In 2003, launched the first batch of domestically produced congenital heart defect occluders, and in 2009, introduced China's first PFO occluder, with a cumulative implantation exceeding 220,000 cases.。

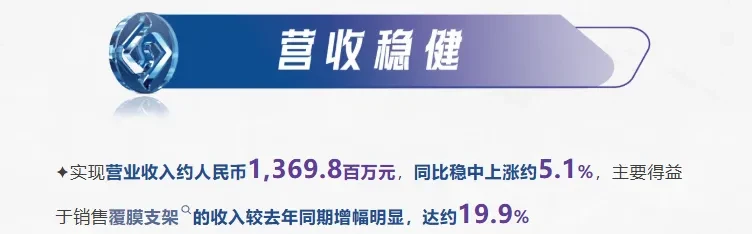

In 2025,Lifetech Scientific Revenue Approximately RMB 1.37 Billion, Up 5.1% Year-on-Year。

Among the three lines,Peripheral Vascular revenue reached RMB 845 million, up 12.4% year-on-year, serving as the growth engine; Structural Heart Disease revenue stood at RMB 512 million, down 3.0% year-on-year—the core business is under pressure.。

Acquiring Starway Medical, Lifetech Scientific Secures Three Key Assets:Market share surges; after the merger of the "No. 1 + No. 3 players," it far surpasses Shape Memory; a ticket to the PFO market, Starway Medical's Cardi-O-Fix holds one of the few PFO device registration certificates in China, with PFO interventional procedures in China reaching approximately 40,000 cases in 2022—a high-growth sector that Lifetech had previously been largely absent from; consolidated profits, Starway Medical's annual profit of approximately RMB 100 million directly accretes to the financial statements.。

Yet the risks are equally real. Each company maintains its own independent R&D system, sales team, and hospital access network; integration friction will not simply vanish. Combining two under-pressure business segments will not automatically translate into high growth.

Hillhouse and Lifetech share a long-standing and deep-rooted relationship. In 2020, a Hillhouse-affiliated fund acquired 462 million shares of Lifetech from Central Huijin and Everbright Holdings, once holding a 9.88% stake. Prior to this transaction, it still held approximately 4.96%.

In 2023, Lifetech Scientific sold an approximately 22.48% equity stake in Starway Medical to Hillhouse Capital for RMB 500 million, at which time Starway Medical was valued at approximately RMB 2.248 billion.

Currently, Lifetech Scientific has repurchased approximately 96% of the equity stake for RMB 1.942 billion at a reduced valuation, but Hillhouse Capital, through the path of "selling minority stake → selling controlling stake → exchanging for the listed company's convertible bonds + potential controlling position,"Completed a typical "mature assets for liquidity" transaction.。

Over the past few years, the narrative in the primary market for medical devices has centered on securing regulatory approvals, raising capital, generating revenue, and gearing up for an IPO. During 2020–2021, valuations for innovative medical devices were exceptionally high. However, the market environment has now shifted—valuations under HKEX Chapter 18A have corrected significantly, and A-share IPOs now place greater emphasis on the underlying quality of revenue, profitability, and cash flow.

The optimal endgame for mature medical device assets is not necessarily an independent IPO, but rather acquisition by a publicly listed company.Starway Medical is a typical example: over two decades of operational history, a clear product line, and regulatory approval barriers, delivering genuine profitability despite slowing growth.A standalone IPO may not necessarily secure an ideal valuation, but it holds clear value in complementing the industry chain for a cardiovascular interventional platform like Lifetech.。

The terms secured by Hillhouse in this deal—a 3.5% coupon, equity pledge, board nomination rights, and 12.5% IRR redemption protection—indicate that top-tier funds at the exit stage are no longer merely divesting equity stakes, but are instead structuring comprehensive asset securitization frameworks.

Lifetech did not acquire the assets for free; instead, it paid with future equity, governance rights, and debt covenants. Nor did Hillhouse make a complete exit; it exchanged its stake in Starway Medical for a ticket to Lifetech’s corporate control. The conversion window in three years will determine whether this ticket is converted into equity or redeemed at 1.5 times the principal.

For Secondary Market Investors, closely monitor: the shareholders' circular prior to June 30, the complete assets and liabilities details of Starway Medical, the voting results of the shareholders' general meeting, the progress of the anti-monopoly review, and the pace of Hillhouse Capital's stake increase to become the largest shareholder.

To Industry Observers, the signal is clear: in mature categories such as congenital heart defect occluders, the window for consolidation has opened. As another major player in the market, the consolidation path of Shape Memory (a subsidiary of Lepu Medical) will be the next M&A proposition worthy of attention.

To Lifetech's Long-Term Holders——For those shareholders reluctant to cut their losses despite a 50% paper loss——this transaction provides a new narrative pivot: hitching a ride on Hillhouse's express train to await the tailwind from the commercial launch of the iron-based stent.

Based inChina, Linking the World

`Zero Inventory Group`Specializing in one-stop supply chain services for medical device centralized procurement and global expansion.

Bringing together an extensive range of high-quality medical devices and consumables (CE/FDA approved).

Sincerely seeking partners or trading enterprises with overseas hospital, clinic, and medical distribution channel resources for collaboration, to monetize these resources and jointly expand into global markets.