Nature Forecasts Global Ulcerative Colitis Market to Reach $11–12 Billion by 2026 Amid New Therapeutic Advances

Bristol-Myers Squibb

Biopharmaceutical and Nutritional Product R&D and Sales

European Commission

The European Commission, abbreviated as the EU Commission, is a supranational body under the European Union. Within the EU political system, the European Commission primarily undertakes executive tasks, thus being roughly equivalent to the government in a national system. However, the European Commission has other functions as well. In particular, except for the few circumstances specified in the treaties, the European Commission is the only institution with legislative power in the EU legislative process.

On November 23, Bristol-Myers Squibb (BMS) announced that the European Commission has approved a new indication for its sphingosine-1-phosphate (S1P) receptor modulator, ozanimod (Zeposia): for the treatment of adult patients with moderate to severe active ulcerative colitis (UC) who have had an inadequate response, lost response, or were intolerant to conventional therapies or biologics. Ozanimod is the first and only oral S1P receptor modulator approved in the EU for the treatment of UC, representing a new approach to treating this chronic immune-mediated disease.

UC is a type of inflammatory bowel disease (IBD) that affects the mucosa and submucosa of the colon and rectum, and sometimes a small section of the terminal ileum. Severe UC is characterized by fever, abnormal levels of C-reactive protein and hemoglobin, along with other symptoms of intestinal inflammation. The prevalence of UC is estimated to be between 7 to 246 cases per 100,000 people. Complications of UC can be local, including hemorrhoids, perirectal abscesses, or anal fissures, or may present with extraintestinal manifestations.

In recent years, biologic therapies, including tumor necrosis factor (TNF) antagonists and the anti-α4β7 antibody vedolizumab, have improved the treatment of UC compared to traditional therapies. Newer treatment options have also been developed or are in late-stage development and may prove to be more effective than existing therapies.

On November 23, an article published in Nature Reviews Drug Discovery analyzed the UC market, including current therapies, emerging therapies, and market indicators in this field.

Source: Nature Reviews Drug Discovery

Current Therapy

First-line treatments for mild to moderate UC include oral aminosalicylates or controlled-release budesonide. Acute UC often requires systemic corticosteroid therapy. Mercaptopurine or azathioprine can be used to maintain remission in UC, either as an alternative to TNF inhibitors or in combination with them, and may also be suitable for patients who do not respond to aminosalicylates or require long-term corticosteroids. Intravenous cyclosporine can also effectively treat severe steroid-refractory UC and may delay or prevent the need for surgery.

For patients with moderate to severe UC or those dependent on corticosteroids, extraintestinal treatment options typically involve TNF inhibitors, including infliximab (Remicade; Janssen), adalimumab (Humira; AbbVie), or golimumab (Simponi; Janssen). Additionally, integrin-blocking therapies can also be used to treat patients with moderate or severe UC: vedolizumab (Entyvio; Takeda) is a humanized monoclonal antibody that binds to α4β7 integrin, thereby preventing leukocyte migration to the gut. Vedolizumab is used as a second-line extraintestinal treatment for patients with moderate to severe UC who cannot take anti-TNF drugs due to side effects, lack of efficacy, or loss of response.

Other treatment strategies for moderate to severe UC also include JAK inhibitors and antibodies targeting p40 (a subunit of IL-12 and IL-23). Ustekinumab (Stelara; Janssen) is a monoclonal antibody that binds to p40, blocking cell signaling, cytokine production, and the expression of immune component genes. Tofacitinib (Xeljanz; Pfizer) is an orally active non-selective JAK family kinase inhibitor that affects the production of several interleukins involved in the regulation of B and T lymphocytes, which are associated with mucosal inflammation. However, in one study, compared with TNF inhibitor therapy, tofacitinib was associated with a higher risk of serious adverse events in elderly patients with rheumatoid arthritis, leading to widespread questioning of the safety of tofacitinib and JAK inhibitors. Therefore, the FDA is reviewing the labeling of currently approved JAK inhibitors for inflammatory conditions. The labels of approved JAK inhibitors already carry black box warnings regarding serious infections, malignancies, and thrombosis.

Ozanimod (Zeposia; Bristol-Myers Squibb) is an S1P receptor modulator that prevents lymphocytes from exiting lymph nodes, thereby reducing the number of lymphocytes at sites of chronic inflammation. As mentioned at the beginning of the article, ozanimod is an oral small-molecule drug that has previously been approved in the United States and the European Union for the treatment of multiple sclerosis. It was approved by the U.S. FDA in May 2021, becoming the first oral S1P receptor modulator in the U.S. for the treatment of UC. In the Phase III True North trial, after 10 weeks of ozanimod induction therapy in patients with moderate to severe UC, the clinical remission rate showed statistically significant improvement (18% vs. 6% in the placebo group). Additionally, at week 52, significantly more patients receiving ozanimod maintenance therapy achieved clinical remission (37%) compared to those on placebo (19%).

Emerging Therapies

Emerging therapies for UC are typically applicable to moderate to severe active UC. These therapies include orally administered small molecule drugs and injectable biologics. Compared with current treatments, they offer new mechanistic approaches or have better selectivity (Table 1).

Table 1 | Some drugs under development for ulcerative colitis

Note: IL-6R=IL-6 receptor; LANCL2=LanC-like protein 2; S1P=sphingosine-1-phosphate; RIP1K=receptor-interacting serine/threonine-protein kinase 1 (Source: Nature Reviews Drug Discovery)

In November 2021, the new selective JAK inhibitor filgotinib (Jyseleca; Galapagos/Gilead) was approved in the European Union for the treatment of moderate to severe UC. Another JAK inhibitor, upadacitinib (Rinvoq; AbbVie), is also under development for this indication. Both drugs show higher selectivity for JAK1 over JAK2 and JAK3, inhibiting only certain signaling pathways. As a result, dose-related toxicity is expected to be reduced without compromising efficacy. In the Phase III U-ACCOMPLISH and U-ACHIEVE trials, at week 8, clinical remission was achieved in 4% and 5% of patients in the placebo groups, compared with 33% and 26% in the upadacitinib-treated groups, respectively. Furthermore, at week 52, significantly more patients in the upadacitinib-treated groups achieved clinical remission compared to the placebo group (42% in the 15 mg group, 52% in the 30 mg group vs. 12% in the placebo group).

Two other JAK family inhibitors, Pfizer's ritlecitinib (PF-06651600) and brepocitinib (PF-06700841), have recently completed Phase II development. Ritlecitinib is an irreversible inhibitor of JAK3/TEC, while brepocitinib inhibits TYK2/JAK1. In the Phase II VIBRATO study, by Week 8, patients in the ritlecitinib (70 mg or 200 mg) groups achieved significantly more clinical remission compared to the placebo group (34%, 28.6% vs. 0%).

Etrasimod (Arena Pharmaceuticals) is an oral, once-daily selective S1P receptor modulator currently in Phase III trials (ELEVATE UC 52 and ELEVATE UC 12) for the treatment of moderate to severe active UC. Etrasimod is selective for S1P receptor 1 (S1PR1), S1PR4, and S1PR5 and has a short half-life, which is expected to result in fewer off-target effects compared to ozanimod.

Another orally active small molecule being developed for UC is deucravacitinib (Bristol-Myers Squibb), a selective allosteric inhibitor of tyrosine kinase 2 (TYK2). The drug's mechanism of action differs from other JAK inhibitors as it inhibits TYK2 by binding to the regulatory domain rather than directly to the active site. Allosteric TYK2 inhibition is more selective and has the potential to control side effects typically associated with active site JAK inhibitors. However, in the Phase II LATTICE-UC trial, deucravacitinib failed to demonstrate superiority over placebo at week 12 for the primary endpoint of clinical remission and key secondary endpoints. A second Phase II trial for UC is currently ongoing.

Other orally active small molecules being developed for the treatment of UC include GSK2982772 from GlaxoSmithKline, which is a receptor-interacting serine/threonine protein kinase 1 (RIP1K) inhibitor.

Four specific drugs targeting IL-23 rather than the shared subunit with IL-12 are also being developed for UC treatment. These monoclonal antibodies selectively bind to the p19 subunit of IL-23, thereby inhibiting its interaction with the IL-23 receptor and the resulting downstream signaling. 1) Risankizumab (Skyrizi; AbbVie) has been approved for the treatment of moderate to severe plaque psoriasis and is currently in Phase III clinical trials for moderate to severe UC. 2) Similarly, mirikizumab (LY3074828; Eli Lilly), intended for the same indications, is also in Phase III development. 3) Guselkumab (Tremfya; Janssen), which is approved for treating adult patients with moderate to severe plaque psoriasis and active psoriatic arthritis, is also undergoing Phase III clinical trials for the treatment of moderate to severe UC. 4) The fourth IL-23 inhibitor, brazikumab (MEDI2070) from AstraZeneca, is in Phase II trials for moderate to severe active UC.

Market Indicators

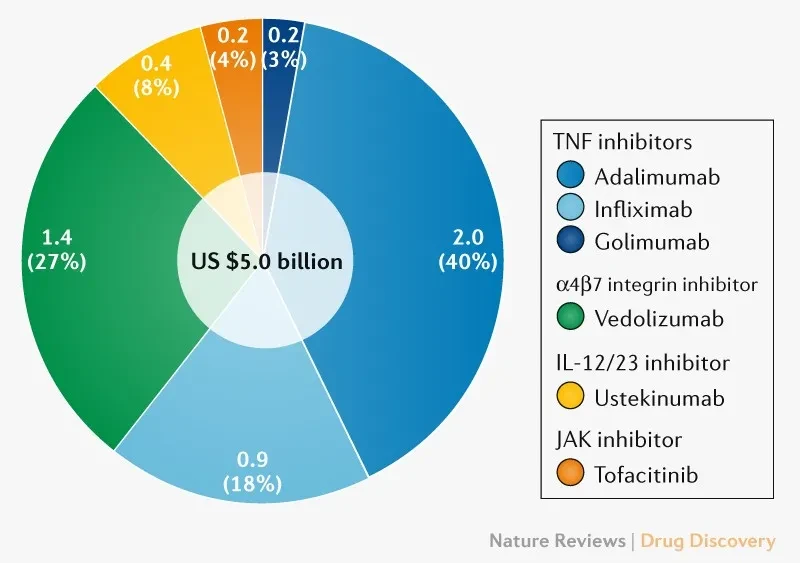

In 2020, the global UC drug market was valued at approximately USD 7.5 billion, accounting for 10% of the entire immunology market. The United States remains the primary market for UC treatment, representing 65% of total sales (Figure 1). Over the past four years, the market size for this disease has shown a compound annual growth rate (CAGR) of 10%, primarily driven by increased diagnosis rates, the introduction of new therapies, and the rising use of biologics among patients with moderate to severe conditions. Adalimumab (Humira in the U.S.) dominates the U.S. UC market with a 40% market share, followed by vedolizumab (Entyvio in the U.S.; 27%), and then infliximab (Remicade and its biosimilars; 18%).

Figure 1 | The U.S. Ulcerative Colitis Market in 2020: $5 Billion in Sales Broken Down by Drug and Target. (Source: Nature Reviews Drug Discovery)

Despite market analysis being muddled by the use of these drugs in other indications, the global UC market outlook is positive post-2020, with an expected CAGR of 5–7%. This growth will primarily be driven by the introduction of several new therapies (mainly IL-23 and JAK inhibitors), and at the current growth rate, the market size is projected to reach $11–12 billion by 2026. However, these new therapies will face challenges from the increasing emergence of biosimilars, as major brands including Humira, Entyvio, and Remicade will lose their "exclusivity" in the U.S. starting from 2023.

References:

1# Bristol Myers Squibb Receives European Commission Approval of Zeposia (ozanimod) for Use in Adults with Moderately to Severely Active Ulcerative Colitis (Source: BMS Official Website)

2# The market for ulcerative colitis (Source: Nature Reviews Drug Discovery)