With Over 90% Import Dominance, Electrophysiology Faces Centralized Procurement: Can Domestic Players Seize the Opportunity?

APT Medical

Cardiac Electrophysiology and Interventional Medical Device R&D Manufacturer

MicroPort EP

R&D Producer of Cardiac Electrophysiology Interventional Medical Devices

AccuPulse

Developer of products in the field of cardiac electrophysiology

"The possibility of short-term centralized procurement in cardiac electrophysiology is relatively low."

This was a judgment made in a previous securities firm report regarding the possibility of centralized procurement in the electrophysiology sector. However, contrary to expectations, this niche market, where imports account for over 90% and is considered extremely difficult for centralized procurement, will also see such procurement this year.

Recently, according to the information from the National Healthcare Security Administration, a unified deployment and coordination for regional alliance procurement has been made recently. The key product categories for provincial procurement in 2022 and the leading units and procurement categories for the proposed key promotion of alliance procurement have been confirmed.

In the 2022 proposed key recommended alliance procurement, Fujian will lead the electrophysiology and endoscopic stapler procurement alliance. The National Healthcare Security Administration noted that for key product categories, based on the leading intentions and capabilities of each province, the corresponding leading provinces will be identified to encourage other interested provinces to actively join, expand the alliance scope, and optimize the frequency and rhythm of procurement.

In other words, electrophysiology products were included as a key category in the 2022 provincial procurement.High-value consumables in the cardiovascular field, compared to coronary stents which have undergone national centralized procurement, the penetration rate of electrophysiological surgery in China is not high. In 2020, the total number of cardiac electrophysiology surgeries in China was 212,000 cases, while the total number of PCI surgeries in the same year had already exceeded one million.

The market for cardiac electrophysiology is far from mature, with domestically produced products accounting for less than 10% of the market, while the market share of three multinational companies—Johnson & Johnson, Medtronic, and Abbott—exceeds 85%. Moreover, new technologies are also expected to reshape the market landscape. In 2021, a groundbreaking technology in the cardiac electrophysiology field, pulsed field ablation (PFA), became a sensation in the atrial fibrillation ablation sector. Multiple domestic companies have entered the field, sparking a wave of financing.

In this market where the growth rate exceeds 30%, with competition between domestically produced and imported products, and new technologies rapidly emerging, the introduction of centralized procurement as a new variable will lead to what changes in its scale and market landscape in the future?

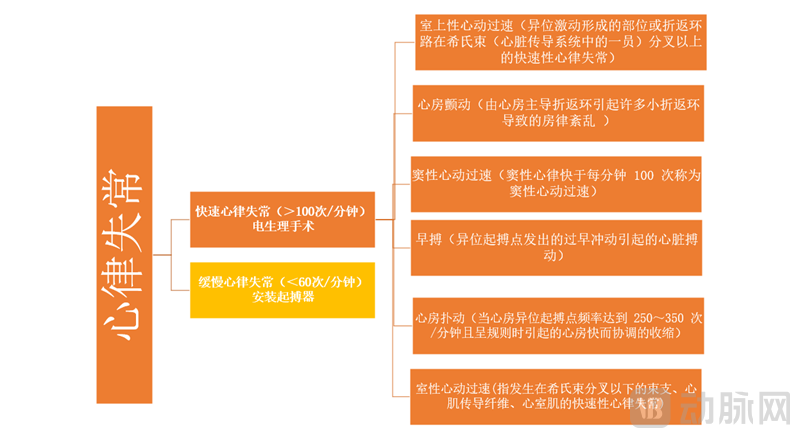

Cardiac electrophysiology technology is mainly used to treat tachyarrhythmia. In 2020, the total number of patients in China exceeded 30 million, most of whom suffered from atrial fibrillation and supraventricular tachycardia.

The cardiac electrophysiology market has been one of the fastest-growing segments in the past decade, which is why cardiac electrophysiology companies have gained significant attention in both primary and secondary markets.

In 2021, the market size of electrophysiology devices in China will reach 8 billion yuan. In the fastest-growing atrial fibrillation (AF) segment, the number of AF electrophysiology surgeries was approximately 10,000 cases in 2011, and by 2021, the number of AF electrophysiology surgeries in China had grown to about 100,000 cases. According to industry insiders, in 2021, imported electrophysiology businesses could achieve an annual revenue of 4.5 billion yuan.

With the rapid development of the cardiac electrophysiology market in China, companies such as APT Medical, MicroPort EP, Xinpul, and Jinjiang Electronics have become the main domestic participants, but the market share of domestically produced products remains relatively low.

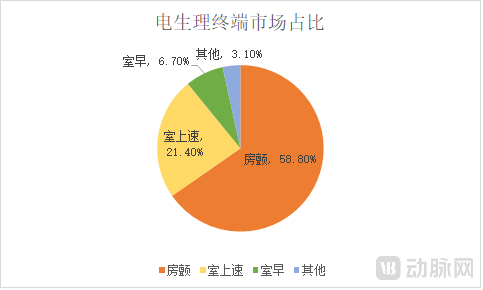

According to the data in the prospectus of MicroPort EP, the market share of domestically produced electrophysiology medical devices in 2020 was 9.6%. Calculated by sales revenue, the top three players in China's electrophysiology device market in 2020 were all imported brands. Among them, Johnson & Johnson held a dominant position with cardiac electrophysiology sales reaching approximately 3.03 billion yuan in 2020, accounting for 58.8% of the market and ranking first. It was followed by Abbott and Medtronic, with market shares of 21.4% and 6.7%, respectively. Together, these three companies accounted for over 85% of the market.

Why is the cardiac electrophysiology market so difficult to crack? The core reason is that the largest piece of the pie has consistently been taken by multinational corporations, making it hard for domestically produced products to break into the largest market segment—the three-dimensional atrial fibrillation ablation market. Domestically produced products are mainly concentrated in the interatrial septal puncture system and simpler mapping catheters.

Electrophysiological procedures are divided into 2D and 3D techniques. The 2D technique uses X-rays for positioning, while the 3D technique employs electromagnetic technology to achieve precise positioning, significantly reducing procedure time and enhancing the success rate and safety of the surgery. 3D ablation procedures can shorten operation and X-ray exposure time, reduce the occurrence of procedure-related complications, improve the effectiveness of ablation, and lower the recurrence rate of postoperative atrial fibrillation.

In the entire cardiac electrophysiology market, the ablation treatment for atrial fibrillation (AF) is the most significant segment. Atrial fibrillation, commonly referred to as "AF," is one of the most prevalent types of tachyarrhythmia in clinical practice. Among tachyarrhythmias, the pathogenesis of AF is relatively complex, and the ablation procedure is more challenging. Therefore, in AF treatments, a three-dimensional mapping system is typically required to create a more precise cardiac model, enabling doctors to perform accurate interventions. Additionally, the cost of AF procedures is the highest in cardiac electrophysiology surgeries.

AccuPulse founder Yin Jie told VCBeat: "Since atrial fibrillation surgery requires the use of a 3D mapping system for operation, the reimbursement price at the medical insurance terminal for all consumables combined is about 80,000 yuan. For non-atrial fibrillation surgeries, the medical insurance terminal reimbursement price is approximately 20,000 yuan, a fourfold difference. Therefore, in the entire electrophysiology market, atrial fibrillation ablation can account for half of the electrophysiology market."

In the field of atrial fibrillation, having a 3D system is the entry ticket to the market, and only companies with their own 3D systems can dominate the main market for treatment consumables. Currently, the products representing the international leading level of 3D cardiac electrophysiological mapping systems are mainly the CARTO 3 system launched by Johnson & Johnson and the EnSite PRECISION system launched by Abbott.

In terms of domestically produced products, the three-dimensional electrophysiology products from Jinjiang Electronics, APT Medical, MicroPort EP, and Xinpulse have been successively approved. Jinjiang Electronics' cardiac electrophysiology mapping product was already approved in 2017.

Why do domestically produced 3D products have a smaller market share? Because electrophysiology manufacturers can only gain sufficient product portfolio competitiveness by building a complete solution of "system + equipment + consumables".

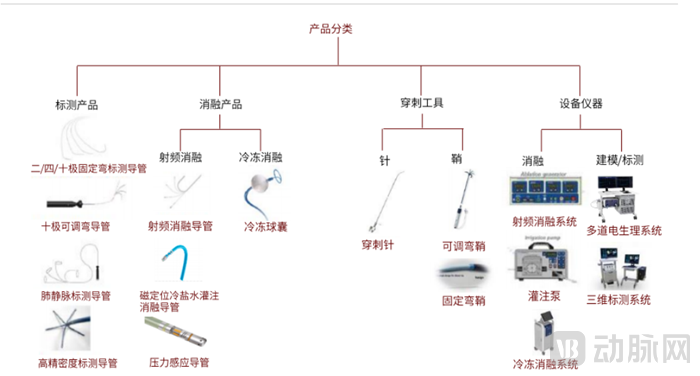

Classification of Cardiac Electrophysiology Products Source: CICC Relevant Report

In the core module, to improve the clinical usability of the 3D cardiac electrophysiology mapping system, internationally advanced products have introduced rapid 3D cardiac chamber modeling modules, high-density mapping modules, and pressure-sensing modules, along with corresponding catheters for commercial use; Chinese manufacturers have yet to commercialize high-density mapping modules and pressure-sensing modules.

Secondly, due to the late start of China-produced electrophysiology development, there is insufficient clinical data, and the core performance stability and core algorithm accuracy need further validation. The international giants launched their 3D cardiac electrophysiology mapping systems earlier, accumulating a large amount of clinical data during the process, covering various types of tachyarrhythmia conditions. They possess a first-mover advantage in terms of core performance and core algorithm levels. Domestic companies still require time to refine their core algorithms, improve core algorithm accuracy, and ensure that the system's core performance meets clinical needs.

At the same time, market education is also one of the difficulties. According to the "Clinical Application Management Standards for Cardiovascular Disease Interventional Diagnosis and Treatment Technology (2019 Edition)," cardiac electrophysiology surgery is classified as a Level IV surgery, which is one of the highest-level surgeries with a high degree of difficulty. Among them, interventional procedures applicable to complex arrhythmias such as atrial fibrillation are even more complicated. There are not many doctors in China who can perform three-dimensional atrial fibrillation ablation. Meanwhile, imported manufacturers like Johnson & Johnson and Abbott have built strong trust relationships with a large number of clinicians during their long-term market education efforts in China’s cardiac electrophysiology market. As a result, clinicians tend to prefer using familiar surgical instruments when performing highly complex surgeries.

In the market landscape where domestically produced cardiac electrophysiology products account for less than 10%, will centralized procurement reshape the market?

In terms of market scale, the domestic alliance procurement affects a larger market scope. The centralized procurement price reduction may promote the penetration rate of electrophysiological surgeries.

China’s market for tachyarrhythmia still has a huge unmet demand. China has a large base of patients with arrhythmia, which is one of the common conditions of cardiovascular diseases. According to Frost & Sullivan, the number of patients is approximately 30 million. Currently, the volume of cardiac electrophysiology procedures in China is about 128.5 per million people, while in the United States, it reaches 1,302.3 per million people.

In the niche market of catheter ablation for atrial fibrillation, China had 11.596 million patients with atrial fibrillation in 2020, but only 82,000 corresponding atrial fibrillation surgeries were performed, with a penetration rate of less than 1%. In contrast, the penetration rate in the United States reached 8%-9%.

Currently, the prices of cardiac electrophysiology consumables are relatively high. The price of domestically produced 2D ablation catheters is around 7,000 RMB per unit, while imported products range from 8,000 to 10,000 RMB per unit. The price of 2D mapping catheters is approximately 2,000 RMB per unit, and a 2D ablation procedure costs about 20,000 RMB. The price of cryoballoons ranges from 30,000 to 50,000 RMB, with accompanying mapping electrodes costing around 20,000 RMB. Therefore, the total cost of a cryoablation procedure is approximately 50,000 to 70,000 RMB. In 3D radiofrequency ablation procedures, the price of high-density mapping catheters exceeds 20,000 RMB, and the price of ablation catheters also exceeds 20,000 RMB. A 3D ablation procedure typically involves the use of 7 to 8 types of consumables. Overall, the cost of a 3D atrial fibrillation ablation procedure is approximately 80,000 RMB.

Reference to the impact of centralized procurement on PCI procedures, centralized procurement has driven a rapid increase in the volume of PCI procedures in the short term, with the growth rate exceeding 40% in 2021. It can be inferred that if the price reduction is significant enough, the price decrease brought by centralized procurement is also expected to boost the volume of cardiac electrophysiology procedures.

From the perspective of the entire market structure, the centralized procurement of mature products in the cardiac electrophysiology field may also accelerate the application of new technologies.In the field of cardiac electrophysiology, the two mainstream ablation technologies are radiofrequency ablation and cryoablation. Radiofrequency ablation is the mainstream technology, while cryoablation accounts for about 10% of the market share. Currently, in China, only Medtronic has products on the market.

PFA Technology: A Thunderclap in the Field of Atrial Fibrillation Ablation. Unlike previous thermal ablation and cryoablation, PFA technology offers advantages in safety and surgical efficiency, with low procedural difficulty and a short learning curve. Currently, the main multinational players in this market are Boston Scientific and Medtronic, while in China, companies such as Jinjiang Electronics, AccuPulse, ZHILIN Medical, and XuanYu Medical have entered the field. The progress of their clinical trials is comparable to that of multinational enterprises.

Regarding how much market space PFA can have in the future, an industry insider stated: "It takes time for a new technology to emerge and form an overwhelming substitution for past technologies. Each technology has its own characteristics and will occupy a certain market share in the future. In the future, PFA may replace the market of cryoablation. If PFA products achieve obvious advantages, multiple manufacturers accelerate certification, and accelerate promotion, PFA is also expected to become the product with the largest market share in the future. In the future, centralized procurement will compress the profits of traditional ablation methods, which will also drive doctors to try new ablation technologies."

But Yin Jie also mentioned: "In PFA technology, the R&D capability of the three-dimensional system is also a core competitiveness, which is a technology that most domestic companies lack."

From the perspective of the market landscape, although China's cardiac electrophysiology centralized procurement has not yet been implemented, the impact of electrophysiology centralized procurement can be analyzed based on the trends observed in previous centralized procurements of other categories.

Currently, the rules for centralized procurement in China can be divided into two types: stent-based centralized procurement and joint-based centralized procurement.

The stent-based centralized procurement has a significant negative impact on the industry, shrinking the market size from tens of billions to just a few hundred million. Under this procurement model, it is difficult for either domestic or imported companies to emerge as winners. Although Chinese-produced companies face lower market entry barriers and gain larger market shares, the sustainability of industry innovation has been compromised.

In addition to the highly impactful stent procurement, last year saw the emergence of more moderate procurement methods in categories such as artificial joints, staplers, and ultrasonic scalpels.

From a regulatory perspective, the subsequent implementation of moderated bulk procurement will generally adopt a grouping model. The share of Group A will be determined based on previous sales volumes. This model has a relatively smaller impact on the existing industry landscape. At the same time, domestically produced enterprises can also secure some shares and new opportunities in Group B. This model is more advantageous for the original market leaders.

The future mode of centralized procurement in the field of cardiac electrophysiology remains uncertain. However, one thing is certain: whether a company owns a 3D system will be the watershed between enterprises and also the threshold for entering the more core atrial fibrillation ablation market.

If it fails to enter the 3D ablation market for atrial fibrillation, the future 2D ablation market will be impacted by centralized procurement, compressing profit margins and further limiting the survival space for domestically produced cardiac electrophysiology products.

In the face of centralized procurement, how will domestic companies respond? Specific bidding strategies will only become clear after the centralized procurement policies are released. Ultimately, only Chinese-produced enterprises that can secure a larger share in the 3D ablation market will emerge as winners.

After the stent centralized procurement, we can see that a rich product line can help companies withstand the impact of centralized procurement. Currently, domestic electrophysiology companies have their own characteristics in terms of product line reserves.

APT Medical adopts a three-pronged approach. In addition to its cardiac electrophysiology business, APT Medical also has a vascular intervention business, which includes coronary pathway and peripheral intervention businesses. In 2021, APT Medical's coronary pathway business revenue reached 382 million yuan, benefiting from centralized procurement to increase market share; the peripheral intervention business revenue reached 119 million yuan in 2021. In 2021, the revenue from electrophysiology products reached 233 million yuan, with net profit attributable to the parent company exceeding 200 million yuan.

APT Medical's 3D product was launched in 2021. It conducted over 30 3D product launch roadshow surgeries at national-level cardiac electrophysiology centers and completed more than 600 3D electrophysiology surgeries in nearly 200 hospitals across China.

MicroPort EP's products focus on the electrophysiology field. Key products under future development include cryoablation systems and cryoablation catheters, high-density mapping catheters, magnetic navigation-enabled cardiac radiofrequency ablation catheters, contact force-sensing magnetic navigation-enabled irrigated radiofrequency ablation catheters, and renal artery radiofrequency ablation catheters. In 2021, MicroPort EP's business revenue reached 190 million yuan, with a net loss of 11.97 million yuan.

Although MicroPort EP did not disclose the sales proportion of its 3D products, according to the prospectus of MicroPort EP, the average price of cardiac electrophysiology catheters sold by MicroPort EP in 2021 was 2,323.71 RMB per unit. Based on the unit price, it can be inferred that the current product mix of MicroPort EP is still dominated by 2D products, with fewer 3D product sales.

Some participants have also started to switch tracks. For example, Jinjiang Electronics' three-dimensional mapping product entered the market relatively early but failed to achieve a significant breakthrough in market share. In 2020, Jinjiang Electronics entered the pulsed field ablation market, and by November 2021, the company had completed patient enrollment for clinical trials of its pulsed field ablation system.

In the past, the concept of "immune to centralized procurement" was often mentioned in medical investments. However, as centralized procurement has been implemented more deeply, being immune to it has become a false proposition, with the scope of centralized procurement expanding continuously. When centralized procurement becomes normalized, what is ultimately tested is still the ability to innovate products.

In the cardiac electrophysiology market, China's cardiac electrophysiology industry is still in the early stages of development, with vast market potential. Against the backdrop of domestically produced products holding less than 10% of the overall market share, the industry still lacks a true leader. Even with the arrival of centralized procurement, companies capable of entering the three-dimensional atrial fibrillation ablation market and those able to deploy next-generation technologies will continue to have room for survival.