Source: Instrument Family, no reprinting without authorization, and reprints are allowed 24 hours later.

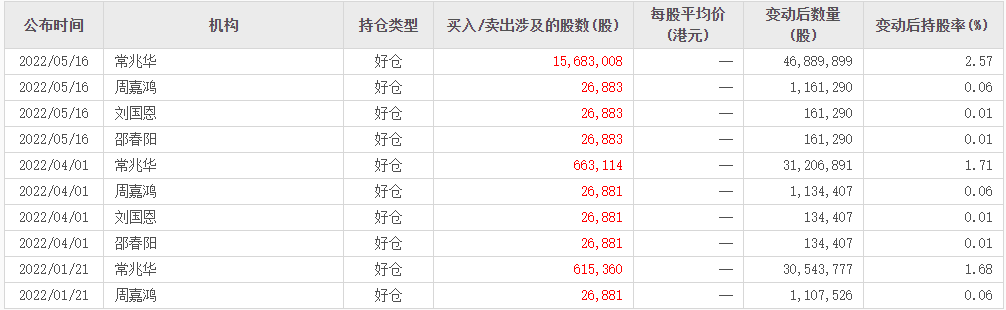

Recently, Medical Device News learned that the shareholding of major shareholders of MicroPort, a Hong Kong-listed company, has changed. Among them, Chairman Zhaohua Chang has continuously increased his shares three times since the beginning of this year. After the change, the number of shares held is 46,889,899, accounting for 2.57% of the total shares.According to public information, Chang Zhaohua and the company's management team, who are in actual control of the second largest shareholder Maxwell Maxcare Science Foundation Limited, currently hold a total of 328.36 million shares, accounting for 18.06% of the equity. Together, they hold a total of 370 million shares, which is only about 7 million shares less than the number of shares held by the largest shareholder, Otsuka Holdings.

This period of time has caused quite a headache for many investors regarding the stock price trend of MicroPort.From the high point of 72.85 last year, MicroPort Medical's stock price plummeted to a recent low of 16.5, with a decline of nearly 77%.This has left investors who were dreaming of the vast universe at the beginning of the year completely stunned, and they have started to reflect on whether investing in MicroPort was an impulsive decision.

From the perspective of the changes in MicroPort's shareholding, some foreign institutions, as the core short-selling forces, are behaving abnormally, while the remaining medium- and long-term institutional investors are showing unusually strong confidence in their holdings. Even after the decline from the peak, the changes in the holdings of the top few dozen shareholders have been minimal. Domestic capital, as a firm bullish force, continues to grow stronger, with MicroPort's CEO, Chang Zhaohua, continuously increasing his stake. What signal is this sending?? According to a prediction by the well-known industry public account "Bone Uncle," in the foreseeable future, perhaps as early as next year, Chang Zhaohua may become the largest shareholder of MicroPort. This could be part of the preparation for MicroPort's smooth return to China's A-share STAR Market.

01

Growth Slows, Stock Price Drops 77%

Two months ago, according to the latest annual performance disclosed by MicroPort, the revenue in 2021 was 779 million US dollars, increasing by 20% year-on-year. If the exchange rate effect is excluded, the growth rate is only 15.0%.In particular, the revenue growth of the two sectors, cardiovascular intervention and orthopedic medical devices, has slowed significantly. Even the domestic revenue in China has seen negative growth due to factors like centralized procurement. Additionally, MicroPort's continued increase in R&D expenditure has led to a further rise in losses.In 2021, the company reported a loss of $351 million, representing a 57.3% increase compared to the same period in 2020. The company's R&D expenses in 2021 amounted to $298 million, accounting for 38.2% of its revenue.

According to the annual report, the reasons for the loss mainly include: the significant increase in expenses brought about by the surgical robot business, heart valve and other businesses leveraging independent financing channels to advance R&D, registration, commercialization, etc.; increased investment in overseas market expansion and product promotion; as well as the impact of China's centralized volume-based procurement policy for coronary stents.

Back in 2020, MicroPort recorded its first loss in five years, amounting to 1.248 billion yuan, nearly twice the total net profit of the previous four years. In particular, the cardiovascular intervention products business, which won the volume-based procurement bid, experienced its first decline, with a drop of nearly 44.6%.

Continuous losses for two years with increasing amounts, the only difference being that the performance loss in 2020 was mainly due to the national volume-based procurement of coronary stents, leading to a direct decline in revenue.However, the losses in 2021 were no longer due to policy impacts but rather returned to the usual reasons of MicroPort's daily R&D and operations.

Firehawk® (Huoying®) stent combines the advantages of bare-metal stents and drug-eluting stents.

Specifically, the three smaller segments of heart valves, neuro-intervention, and aortic and peripheral vascular intervention showed rapid revenue growth, increasing by 93.2%, 72.5%, and 45.6%, respectively. The cardiovascular intervention business under MicroPort Medical was significantly impacted by the centralized procurement policy, which evidently dragged down the company's overall revenue growth rate. In 2021, the company’s global cardiovascular business revenue reached $140 million, representing a year-on-year decrease of 10.8%.

MicroPort's cardiovascular intervention products mainly include four drug-eluting stents and four balloon products.Among them, the two coronary stents, Firebird2 and Firekingfisher, were selected in the first round of high-value consumables procurement launched in November 2020. The relatively high-end stent, Firehawk, missed out on selection due to its quoted price of 7,000 yuan.

MicroPort Medical pointed out that, driven by the centralized procurement of coronary stents, the company's sales volume of coronary stents reached 1.22 million units, a significant year-on-year increase of 132.0%. However, the substantial increase in coronary stent shipments did not lead to an increase in revenue. According to media estimates, MicroPort Medical's domestic cardiovascular intervention business revenue in China was approximately US$120 million in 2021, a year-on-year decrease of 15.5%.

But the overseas revenue from cardiovascular interventions offset the decline in revenue. In 2021, this part of the revenue was 0.2 billion US dollars, a year-on-year increase of 34.5%. Currently, MicroPort's drug-eluting stents have obtained 14 first-time registration certificates in 12 countries or regions, successfully entering markets such as India, Singapore, and Israel.

Orthopedic medical device sector also affected by centralized procurement. In 2021, MicroPort's orthopedic business revenue in China was $0.22 billion, a year-on-year decrease of 31.7%. The centralized procurement of artificial joints led to a reduction in related orders. In the national volume-based procurement of artificial joints in September 2021, MicroPort’s hip and knee joint products were selected. However, domestic revenue from MicroPort's orthopedic medical devices accounted for only 10% of total revenue, with overseas income being the major portion, thus the impact of centralized procurement was relatively mild. In 2021, the company's overseas orthopedic business revenue reached $1.93 billion, a year-on-year increase of 11.8%.

It should be noted that the overseas businesses of MicroPort's cardiovascular intervention and orthopedics have been affected by the pandemic to varying degrees. In 2021, the overall volume of PCI surgeries in overseas markets significantly declined due to the pandemic; meanwhile, the overall demand for orthopedic surgeries overseas has not yet recovered to pre-pandemic levels.

MicroPort Medical's stock price plunged 7.11% on March 31 due to performance falling short of market expectations, closing at HKD 17.78 per share.Since the beginning of this year, the company's stock price has fallen nearly 30%, and it has dropped nearly 77% from its high in June 2021. Some previously steadfast investors have also given up and turned against it, flipping from bullish to bearish in an instant. The company’s market value is now only HK$29.3 billion. Due to MicroPort Medical's continuous spin-offs of subsidiaries, the market has begun to worry about its "hollowing out."The market values of MicroPort Robotics, Heartflow Medical, and Heartpulse Medical are 25.3 billion HKD, 6 billion HKD, and 13.5 billion CNY, respectively, all significantly reduced.

02

Still splitting, companies producing and going public

From its establishment in 1998 to the present, MicroPort has undergone 23 years of development. However, unlike other companies that expand their businesses through reorganization and mergers, MicroPort's growth lies in continuously spinning off and strengthening its subsidiaries while constantly exploring new fields. A closer look at the medical device industry reveals that MicroPort's reach has extended into multiple sectors.

MicroPort Coronary Rapamycin-Eluting Stent System

MicroPort started with heart stents but has not limited itself to just this product line. From the beginning, the company positioned itself for globalization.Starting from the overseas layout with the PTCA balloon dilation catheter's launch in Japan in 2003, the real turning point that allowed MicroPort to make significant strides was around 2010, when MicroPort went public on the capital market.

From the perspective of the company's development process, MicroPort Life Science was established in 2008 to enter the diabetes field, initiating MicroPort's diversified strategic layout; MicroPort Orthopedics was founded in 2009; MicroPort EP was established in 2010; MicroPort NeuroTech, MicroPort CardioFlow, and MicroPort Surgical Instruments were established in 2012; MicroPort Medical Robot and MicroPort Online Medical Technology were founded in 2015; MicroPort UroCare was created in 2017 to enter the urology and women’s health fields; In 2018, the Cardiac Rhythm Management headquarters was set up abroad to pioneer the cardiac rhythm management field.

Currently, the subsidiaries under MicroPort include HeartFlow Medical, HeartGate Medical, MicroPort NeuroTech, MicroPort EP, MicroPort NeuroTech Robotics, MicroPort Orthopedics, MicroPort Cardiac Rhythm Management, MingYue Medical, MicroPort UroCare, MicroPort CardioPower, MicroPort EndoWise, MicroPort Aesthetic Medicine, MicroPort Vision, MicroPort Ziya, RuiKe Medical, ShenTai Medical, ShenDun Medical, ShenYi Medical, ShenTu Medical, MicroPort Longmai, ChuangMai Medical, MaiTong Medical, and NuoJie Medical. Just from its subsidiaries, it is evident that MicroPort has laid out a presence across almost the entire medical device industry.

These subsidiaries are linked hand in hand, supported by the core company, MicroPort, behind them.The enlargement of any single point can expand the entire web surface; as the web surface expands, the core grows; when the core grows, the points expand further. This tightly interconnected web, where "you are in me and I am in you," has enabled MicroPort to reach the highest level of integration between internal and external forces.

From a business model perspective, as one of the only two medical device platform companies in China, MicroPort still maintains its competitive barriers. While other major single-category medical device companies are under pressure from centralized procurement and struggle to invest significant funds into researching new product categories, MicroPort's approach of spinning off subsidiaries for public listings has carved out its own path for development.

Due to its exceptional ability to "spin off subsidiaries," MicroPort is considered a unique presence in the Hong Kong stock market. Previously, it has spun off HeartFlow Medical and HeartValve Medical, which were listed on the STAR Market and H shares respectively. In November last year, MicroPort (Shanghai) Medical Robot Co., Ltd. (hereinafter referred to as "MicroPort Medical Robot") was listed on the Hong Kong Stock Exchange. Currently, the MicroPort group has four listed companies.

In addition, there are two quasi-listed companies,On March 31, the Shanghai Stock Exchange announced that Shanghai MicroPort EP MedTech Co., Ltd. ("MicroPort EP"), a portfolio company of Pudong Sci-Tech Innovation Group, has successfully passed the review for its STAR Market IPO.

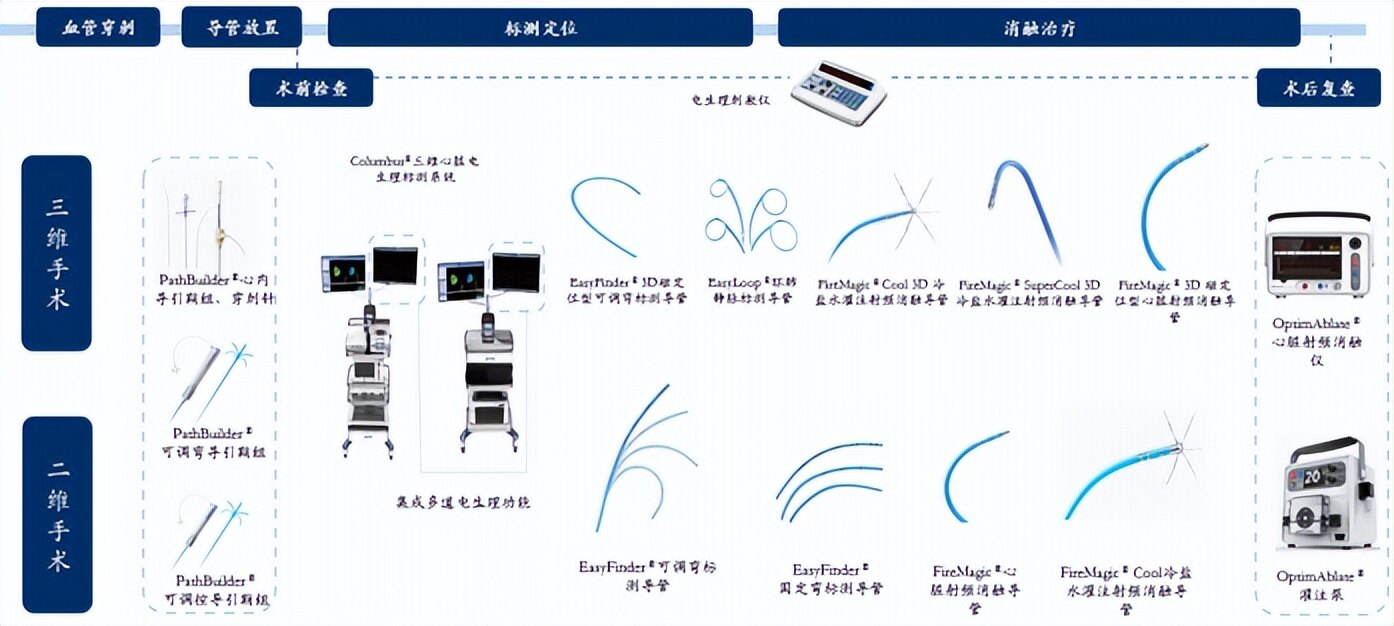

Application of the Company's Main Products in 3D Cardiac Electrophysiology Procedures and 2D Cardiac Electrophysiology Procedures

In addition, on December 28, 2021, MicroPort announced the spin-off of MicroPort NeuroTech Limited ("MicroPort NeuroTech") for an independent listing and officially submitted the prospectus to the Hong Kong Stock Exchange.MicroPort NeuroTech's main business is the research and development, production, and sales of neurointerventional medical devices. According to data from CIC, MicroPort NeuroTech is the largest company in this field in China.

It must be said that MicroPort is a "professional" expert in spin-off listings. If MicroPort NeuroScience successfully goes public, the "MicroPort family" will add another listed company, potentially reaching a total of six. All along, MicroPort has been benchmarking itself against the international medical device giant Medtronic. To achieve this goal, it has steadfastly implemented a strategy of diversified expansion.But the final harvest remains uncertain. What is certain is that the "trillion-dollar market value" Chang Zhaohua expects still has a long way to go.

03

Chairman Continuously Increases Shares, Preparing for Return to A-Share Market?

On the evening of June 1, MicroPort Robot (2252.HK), a subsidiary of MicroPort Medical (0853.HK), announced that it had proposed to the board to list on the STAR Market. The confirmation of its return to the A-share market directly stimulated a significant rise in the stock price of MicroPort Robot's Hong Kong shares—by the close of trading on June 2, the stock price surged by 12.93%, with a total turnover of HK$0.31 billion, nearly equal to the combined turnover of the previous five trading days.

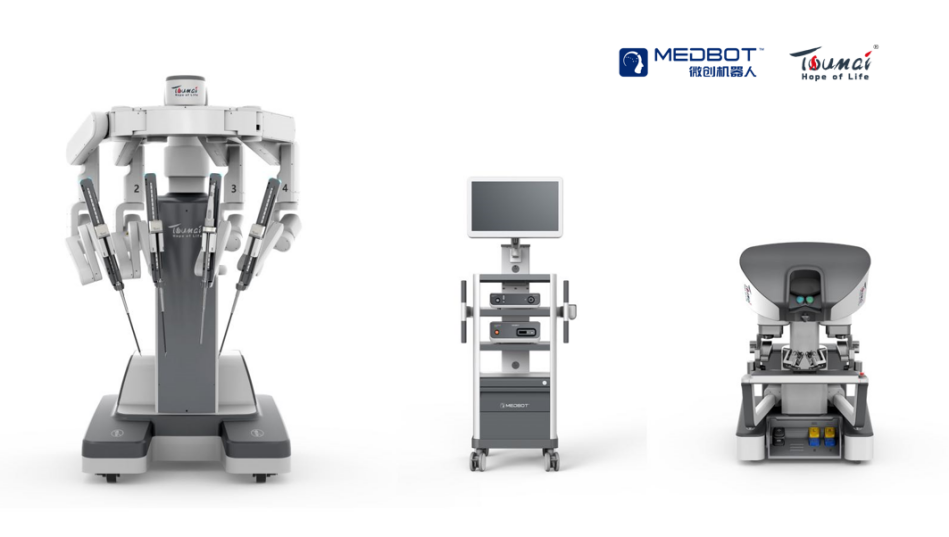

As a surgical robot company, the three flagship products under MicroPort Robot — Tumie Laparoscopic Surgical Robot, Dragonfly Eye 3D Electronic Laparoscope, and Honghu Orthopedic Surgical Robot — have all been approved for marketing by the National Medical Products Administration (NMPA). In this initial public offering plan, MicroPort Robot intends to issue no more than 116 million shares to raise 2.8 billion yuan, which will be used for the construction of three major projects: "Surgical Robot R&D," "Surgical Robot Industrialization," "Marketing System Establishment and Academic Promotion," as well as for supplementing working capital.

This is already the third case of MicroPort's subsidiary making a push for an A-share IPO.Previously, MicroPort Medical had already spun off its subsidiaries, MicroPort CardioFlow Medtech and EP Solutions, for listing on the STAR Market. If MicroPort Robot and EP Solutions successfully go public on the STAR Market, and MicroPort NeuroTech successfully lists on the Hong Kong Stock Exchange, MicroPort Medical — originally founded by Zhaohua Chang and currently in a state without an actual controller — could simultaneously own five listed companies. The question remains whether it will continue to promote independent capital operations for its other divisions.Similarly drawing significant market attention, on January 21, April 1, and May 16 this year, Chang Zhaohua frequently increased his shares, bringing him just one step away from becoming the largest shareholder—a move that undoubtedly sends positive signals.

MicroPort Robot Once Again Initiates Plan to Return to A-Share Market, Possibly Related to Latest Progress in Product Applications. According to the official website, as of 2021, only the Dragonfly Eye 3D Electronic Laparoscopic Endoscope from MicroPort Robot had received approval from the National Medical Products Administration (NMPA) for marketing in China. Meanwhile, the Toumai Laparoscopic Surgical Robot and the Honghu Orthopedic Surgical Robot were both approved in 2022. All three flagship products under the company have now obtained market approval.For MicroPort Robotics' recent attempt to go public on the STAR Market IPO, it undoubtedly plays an important role. Analysts believe that MicroPort Robotics may apply for a STAR Market listing under the fifth set of listing standards.

In 2021, the revenue and loss of MicroPort Robotics were 0.02 billion yuan and 5.58 billion yuan respectively. The income was derived from the sales of Dragonfly Eye 3D Electronic Laparoscopic Endoscope, which marked the first revenue since the establishment of MicroPort Robotics. As the first to fourth listing standards of the STAR Market all impose rigid indicators on revenue, which MicroPort Robotics currently finds difficult to meet, it is more likely that the "fifth standard," which is more suitable for the pharmaceutical and healthcare industry, could become the applicable standard for its listing application.

Toumai® Endoscopic Surgical Robot

According to the regulations, the "Standard Set V" only sets requirements for market value and R&D progress:"The estimated market value is no less than RMB 40 billion, and the main business or products need to be approved by relevant national departments, with a large market space and currently having achieved phased results. Pharmaceutical industry enterprises must have at least one core product approved for Phase II clinical trials, and other enterprises that meet the positioning of the STAR Market must possess obvious technological advantages and meet corresponding conditions."

Some analysts are optimistic about the development prospects of MicroPort Robot, especially since Beijing and Shanghai included some surgical robots in the medical insurance reimbursement scope starting from 2021, which might create more opportunities for the company’s related products. Currently, MicroPort Robot still has a relatively abundant capital reserve, providing the resources needed for further commercial expansion—by the end of December 2021, MicroPort Robot had approximately 1.941 billion yuan in cash and cash equivalents.

MicroPort currently owns or is planning to spin off no less than five subsidiaries for independent listings in the A-share and Hong Kong stock markets. A "MicroPort Group," which flexibly utilizes capital means to independently securitize its sub-businesses, is nearing completion.MicroPort Robot Plans "A+H" Push for STAR Market IPO, Aiming at Three A-Share Companies; "MicroPort Family" Likely to Emerge?

04

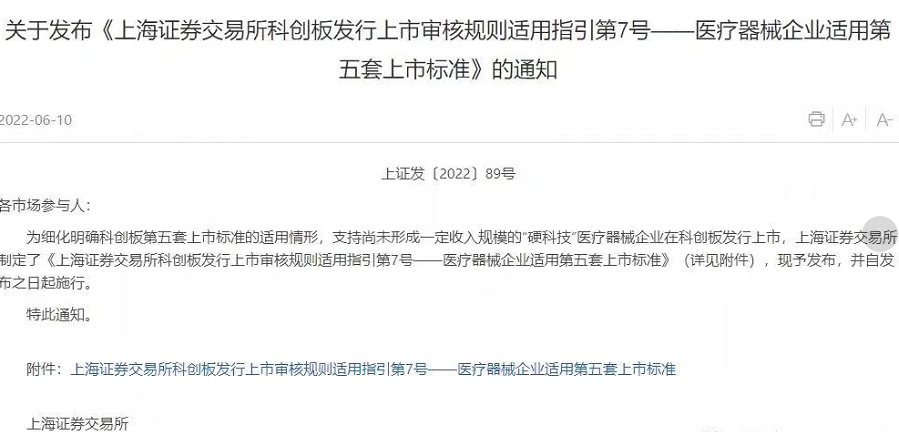

STAR Market Refines "Fifth Set of Standards"

Medical Device Financing Achieves Significant Breakthrough, Welcomes Policy Benefits

Recently, the Shanghai Stock Exchange issued the "Application of the Fifth Set of Listing Standards for Medical Device Companies," adjusting the requirements for medical device companies to be listed on the Sci-Tech Innovation Board, supporting companies in the research and development stage that have not yet generated a certain level of revenue to go public.According to Lin Senyong, President of the Medical Device International Cooperation Branch of the China Chamber of Commerce for Import and Export of Medicines and Health Products, this adjustment represents a significant breakthrough by lowering the profitability requirements for publicly listed medical device companies, boosting enterprises' confidence in accelerating innovation. It is reported that in the past, the Sci-Tech Innovation Board required medical device companies to have a profit of 200 million yuan, which was difficult for some small and medium-sized high-end medical device enterprises to achieve.

Rules Allow Companies to Raise Funds on the Market Before Commercialization After Approval, Opening New Avenues for Early-Stage, Profitless, Technologically Groundbreaking Small and Medium Innovative Medical Device Enterprises in China. Prior to the introduction of these rules, most high-end small and medium-sized medical device companies in China, unable to meet the listing requirements of China’s A-share market or Growth Enterprise Market (GEM), opted to list on the Hong Kong Stock Exchange via Rule 18A (which allows biotech companies without revenue or profit to file for an IPO). However, data from a report by Evercore showed that the Hong Kong stock market saw a sharp downturn in the second half of 2021, with poor financing and liquidity, causing some medical device companies planning to go public via Rule 18A to slow down their Hong Kong listing plans.

It is reported that China's medical device industry has entered a period of rapid development, currently occupying nearly 20% of the global medical device market. It is expected that the medical device industry will continue to maintain a high level of prosperity in the coming years, and the market size is expected to officially exceed one trillion yuan in 2022.

China's domestic medical device companies have transformed from previously focusing on 'import substitution' products to pursuing independent research and development and globally innovative products, thanks to the national policies supporting independent innovation over the past decade. The rise of China's material science, engineering, software and chip technology, AI, as well as the establishment of comprehensive supply chain capabilities, has laid an industrial foundation for the future development of medical device companies.

According to industry insiders, medical device companies transitioning from a past "imitation and following" development model to a "source innovation" development model will assume significant risks during the transformation process and require greater cooperation from the capital market. First, the time investment is much longer. Unlike in the past, source-innovative medical device products take 4 to 5 years from research and development to approval for market entry, and another 5 years or so after launch to achieve commercialization. Second, substantial continuous funding is still required during the commercial promotion phase.

The Shanghai Stock Exchange pointed out that since the opening of the board, a number of innovative drug research and development companies have successfully listed on the STAR Market using the fifth set of listing standards, initially forming an agglomeration effect and demonstration effect among pharmaceutical R&D companies.In addition, leading domestic device companies such as United Imaging, Wego Orthopedics, Infervision, and MGI are already on or are in the process of IPO on the STAR Market, indicating that the medical device R&D has reached a considerable scale.This adjustment rule further improves the mechanism for supporting "hard tech" medical device companies to go public on the STAR Market, which is an important measure to better leverage the STAR Market's role in serving the innovation-driven development strategy.