Boston Scientific and Medtronic Make Billion-Dollar Bets on Left Heart Access as Key Growth Frontier

Boston Scientific

Medical Device Manufacturer

Medtronic

Chronic Disease Medical Device and Therapy Developer

In the first half of 2022, Boston Scientific and Medtronic, two giants, extended olive branches to the same field. Boston Scientific spent $1.75 billion, while Medtronic spent $50 million.

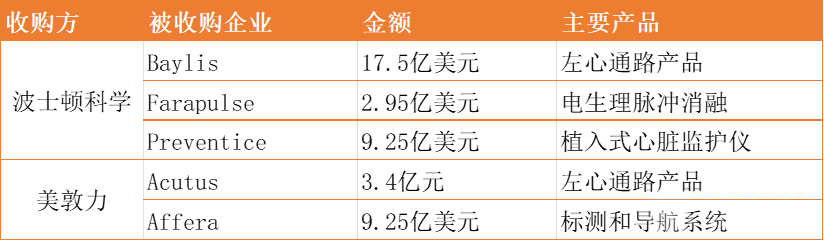

In February this year, Boston Scientific acquired Baylis Medical for an upfront payment of $1.75 billion (approximately RMB 11.2 billion); Medtronic, plc. acquired Actus Medical's left heart access products for $50 million in July this year.

The simultaneous favor of the two giants is because the left heart pathway is associated with three high-growth markets: cardiac electrophysiology, mitral valve intervention, and left atrial appendage closure devices, which play a pivotal role in the structural heart disease market.

Electrophysiological atrial fibrillation ablation, left atrial appendage closure, and trans-septal mitral valve interventions all rely on the trans-septal puncture technique. Only by completing the trans-septal puncture with a left-heart access product can one reach the left atrium to treat related conditions.

When giants make their moves, it is often the time when revolutionary technologies emerge in niche fields. A small change can lead to significant effects, and the two transactions in the left-heart access field will have what kind of impact on electrophysiology and structural heart disease? VCBeat (WeChat ID: vcbeat) has analyzed these two acquisitions.

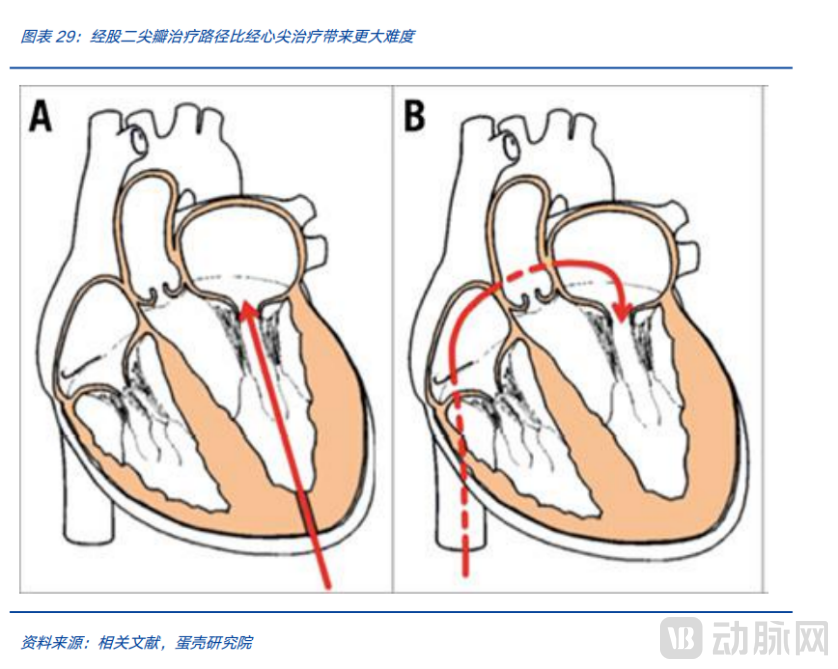

The products of the two enterprises purchased by Boston Scientific and Medtronic are mainly used for atrial septal puncture. The atrial septum is located between the left and right atria, consisting of two layers of endocardium with a small amount of myocardium and connective tissue in between.

The history of transseptal puncture (TSP) dates back to 1958, when it was initially used for left heart catheterization and left ventricular pressure measurement. It gained wider adoption in the 1980s and, with the development of percutaneous mitral valve treatment and catheter ablation for atrial fibrillation (AF), became a routine technique, rapidly spreading in the 21st century.

Transseptal puncture technique is one of the key techniques in cardiac interventional therapy. Many common interventional procedures, such as radiofrequency ablation for atrial fibrillation, mitral valve balloon dilation, and left atrial appendage closure, require transseptal puncture to establish a treatment pathway.

For doctors, the atrial septal puncture technique is a high-risk and highly challenging surgery. The atrial septal puncture is often performed under the guidance of X-rays and transesophageal ultrasound or three-dimensional navigation. Ensuring safety, finding the appropriate puncture site and angle are all challenges for doctors.

Taking the role of atrial septal puncture in electrophysiology procedures as an example, an industry insider stated that the atrial septal puncture in electrophysiology procedures is like learning to reverse park when driving — not knowing how to perform an atrial septal puncture is basically equivalent to not knowing how to perform electrophysiology procedures.

Although atrial septal puncture is not well-known, the number of procedures is considerable. In the United States, more than 300,000 electrophysiology (EP) and structural heart surgeries using trans-septal puncture devices are performed annually. In 2016, there were 70,000 to 80,000 atrial septal puncture procedures annually in China, with an annual growth rate of over 30%.

The atrial septal puncture market consists of three major segments: cardiac electrophysiology atrial fibrillation ablation, left atrial appendage closure, and mitral valve interventional surgery.

Cardiac electrophysiology technology is mainly used to treat tachyarrhythmia. The number of electrophysiology procedures for treating tachyarrhythmia patients in China has continued to grow, increasing from 118,000 cases in 2015 to 212,000 cases in 2020.

Left Atrial Appendage Occlusion for Stroke Prevention

As of 2021, the cumulative number of left atrial appendage closure procedures in China has approached 20,000 cases, with over 9,000 cases performed in 2020, showing a significant increase compared to previous years.

In the interventional treatment of mitral valve, the femoral artery approach in percutaneous mitral valve treatment requires atrial septal puncture. Currently, the only interventional mitral valve product available in China is Abbott's MitraClip, which was approved in 2020, and the number of surgeries has not been disclosed. However, according to Frost & Sullivan, in 2019 there were approximately 210 million patients with valvular heart disease globally, resulting in about 2.6 million deaths. Among them, mitral regurgitation is the most common type of heart valve disease, and if patients with severe mitral regurgitation do not receive effective treatment, the five-year mortality rate can reach approximately 50%. Major global cardiovascular companies are developing mitral valve interventional devices, and with the launch of these products, it will also become a significant growth point for the atrial septal puncture market in the future.

In terms of market landscape, the two major markets where atrial septal puncture plays a crucial role—cardiac electrophysiology and interventional mitral valve treatment—are Abbott's main battlegrounds. Currently, the primary atrial septal puncture systems used in China are also from Abbott.

In the Chinese electrophysiology market, according to the 2020 ranking of three-dimensional cardiac electrophysiology procedures in China, Johnson & Johnson ranked first with a market share of 65.2%, followed by Abbott in second place with a market share of 27.2%.

Abbott is also a leader in the mitral valve market. Abbott's transcatheter mitral valve edge-to-edge repair product, MitraClip, was launched in Europe as early as 2008, in the United States in 2013, and approved in China in 2020. MitraClip remains the only transcatheter mitral valve repair product approved in both China and the United States. In 2019 and 2020, Abbott's MitraClip successively generated nearly $700 million in revenue.

Mitral valve and electrophysiology are both rapidly growing markets. Atrial septal puncture itself has a considerable number of surgical procedures, but this is not the main reason for Boston Scientific and Medtronic's acquisitions. The purchases by Medtronic and Boston Scientific may aim to integrate leading atrial septal puncture systems with their own products to form a competitive product portfolio, especially to enhance the competitiveness of electrophysiology products.

In the three major fields of cardiac electrophysiology, left atrial appendage closure devices, and mitral valves, both Medtronic and Boston Scientific are making strategic investments. However, cardiac electrophysiology has been a细分领域 where the two giants have continuously engaged in acquisitions in recent years. This acquisition of the atrial septal puncture product is evidently aimed primarily at enhancing their competitiveness in the electrophysiology sector.

In the electrophysiology market, Boston Scientific and Medtronic are not the dominant players; Johnson & Johnson is the leader in this field, occupying over 40% of the global market. In recent years, Boston Scientific and Medtronic have begun to challenge Johnson & Johnson's leading position through frequent acquisitions.

Boston Scientific has successively acquired Farapulse, Baylis, and Preventice to strengthen its competitive position in cardiac electrophysiology and structural heart disease.

Boston Scientific is expected to enter the electrophysiology market through pulsed field ablation (PFA) technology. Compared with radiofrequency ablation (RF) and cryoablation, PFA may offer better safety than RF ablation without compromising long-term effectiveness. Boston Scientific's FARAPULSE Pulsed Field Ablation System has entered China's innovative medical device review channel.

The acquisition of Baylis' transseptal puncture products not only completes Boston Scientific's product portfolio in the electrophysiology field, but is also expected to strengthen its competitive position in this area. At the same time, it can be integrated with Boston Scientific's left atrial appendage closure device, consolidating its leading position in the left atrial appendage closure device market and enhancing the competitiveness of its product portfolio.

Medtronic is also increasing its investment in the electrophysiology field. In the electrophysiology field, Medtronic's main technologies include radiofrequency catheter ablation, cryoballoon catheter ablation, and corresponding consumables and equipment, with its core product being the cryoablation product.

In China, Medtronic ranks third in the electrophysiology market, but its market share is much lower than that of Johnson & Johnson and Abbott. In 2020, the top three players in China's electrophysiology device market were all imported brands, with Johnson & Johnson holding a dominant position. In 2020, Johnson & Johnson’s cardiac electrophysiology sales reached approximately 3.03 billion yuan, accounting for 58.8% of the market and ranking first. It was followed by Abbott and Medtronic, with market shares of 21.4% and 6.7%, respectively. The combined market share of the three exceeded 85%.

In addition to cryoablation, Medtronic has also focused on the development of pulsed electric field ablation products, which have similarly entered the National Innovative Medical Device Special Approval Process.

Medtronic's acquisition of Actus Medical's left heart access products also helps to strengthen Medtronic's position in the mitral valve market. In the field of structural heart disease, Medtronic is one of the two global leaders in the TAVR (Transcatheter Aortic Valve Replacement) sector. By acquiring Acutus' left heart access products, Medtronic now has a comprehensive product portfolio in the left heart sector, adding an advantage for future competition in the mitral valve intervention market.

Overall, the two deals mean that both Medtronic and Boston Scientific are preparing to make significant strides with PFA in the electrophysiology field, recruiting resources to challenge Johnson & Johnson's dominant position in this area, while also strengthening their advantages in the structural heart disease sector.

The rush to buy left-heart pathway products, from a market strategy perspective, is to strengthen the product portfolio for cardiac electrophysiology and structural heart disease. From a technical perspective, Boston Scientific and Medtronic are leaders in the global cardiovascular device market, so why do they still need to acquire external technology?

What are the characteristics of Baylis and Acutus' left heart access products?

Transseptal Puncture: A Key Step in Left Atrial Surgery

The innovation of Baylis and Acutus lies in the needle with radiofrequency energy, which can enhance safety and simplify the puncture process.

First, let's look at Baylis, which was acquired by Boston Scientific. Baylis Medical is a company dedicated to providing advanced atrial septal puncture solutions as well as a series of medical guidewires, sheaths, and dilators required for catheter-based left atrial procedures.

Baylis Medical has several star products in the fields of electrophysiology and structural heart, with its most well-known undoubtedly being the atrial septal puncture product.

Baylis Medical's products no longer rely solely on mechanical thrust but instead use radiofrequency energy to perform atrial septal punctures in a predictable and safer manner. This method has been proven to improve puncture efficiency and enhance the safety and effectiveness of atrial septal punctures during left atrial procedures. The new VersaCross platform offers these advantages while eliminating the need to exchange guidewires and sheaths, further simplifying the atrial septal puncture procedure while reducing surgical risks. Clinical evidence shows that the VersaCross platform improves the safety, effectiveness, and efficiency of atrial septal punctures in left atrial treatments such as atrial fibrillation ablation, left atrial appendage closure (LAAC), and mitral valve interventions.

Baylis Medical's net sales in 2022 are expected to reach approximately US$200 million, with year-over-year sales growth in double digits for each of the past five years.

Medtronic Acquires Acutus, Founded in 2011, a Medical Technology Company Focused on Developing Novel Treatment Solutions for Arrhythmia, with Years of Expertise in Cardiac Electrophysiology. Acutus' Star Product is the AcQCross™ Series Universal Transseptal Crossing Device.

Acutus' innovation lies in simplifying the transseptal puncture procedure. AcQCross is the first and only transseptal system with an integrated needle and dilator design, reducing guidewire exchanges, which is also a significant innovation for physicians.

Through AcQCross, doctors can easily reposition without the need to replace the needle and guidewire. Meanwhile, AcQCross is also equipped with radiofrequency energy.

How much can the product innovations of Baylis and Acutus assist Medtronic and Boston Scientific in challenging the electrophysiology market? By leveraging the left heart access products from this acquisition, combined with pulsed field ablation, can Boston Scientific and Medtronic use pulsed field ablation to overtake competitors and gain a larger market share in the electrophysiology market? The future still holds many variables.

In recent years, cardiac electrophysiology has become one of the most watched markets in the field of cardiology, with strong players like Johnson & Johnson and Abbott, as well as no shortage of challengers.

Innovations in electrophysiology mainly focus on four directions: more accurate ablation location, higher ablation efficiency, simplified procedures, and reduced radiation exposure. The benefits brought by the left heart access products acquired by Boston Scientific and Medtronic are more focused on simplifying procedures.

An industry insider summarized: "For electrophysiology surgeries, transseptal puncture is like reversing into a parking space, and previously everyone was using the rearview mirror. The products from Baylis and Acutus are like reverse parking sensors and cameras. Are these two technologies important? For experienced doctors, they can manage without them, but for novice doctors, it makes the process safer, enhancing security and reducing the difficulty of puncture."

On the one hand, Johnson & Johnson's electrophysiology subsidiary has also entered the pulsed field ablation (PFA) market, which is becoming increasingly crowded. However, the 3D ablation capabilities possessed by Johnson & Johnson and Abbott remain scarce. On the other hand, the consecutive acquisitions by Boston Scientific and Medtronic indicate that this is not a simple field; challengers are still in the phase of strengthening their product lines. With the rapid growth in the electrophysiology sector, competition among the major giants is expected to intensify in the future.

References:

After Major Layoffs, Core Product Sold to Medtronic for 330 Million —— Bochuang Medical Technology

【Review】Atrial Septal Puncture Technique: Anatomy, Instruments, and Methods — Chinese Journal of Cardiology