Local Governments Rush to Attract Digital Therapeutics Talent Amid Booming Sector

SLANHEALTH

Digital Therapeutics CDMO and Full-process Service Developer

If you ask what track is hot in the current medical and health field, digital therapy is undoubtedly one of them. As an interdisciplinary cutting-edge science, digital therapy has the opportunity to combine various advanced digital technologies with medical care, thereby creating new or more sophisticated therapies that complement existing traditional treatments. In fact, digital therapy has indeed demonstrated unique advantages in the real world, empowering all parties involved in the healthcare system.

At the same time, the rapidly developing digital economy is becoming an important factor in changing the global competitive landscape. According to statistics, in 2021, China's digital economy accounted for as high as 39.8% of GDP, with the digital industry scale reaching 8.4 trillion yuan. As part of the digital economy, the popularity of digital therapeutics has naturally drawn the attention of local governments.

More crucially, digital therapeutics remains an emerging field where various rules and frameworks are yet to be perfected, and the industry landscape is still chaotic and not solidified. While early movers have certain advantages, no insurmountable competitive barriers have been formed. Precisely because of this, regions across the board are rolling out preferential policies in hopes of not falling behind on this gradually heating track.

The successive policy incentives have gradually intensified the "talent grab" battle in digital therapeutics. So, which regions have already gained the upper hand? And what kind of impact will this have on the future industrial landscape?

It needs to be clarified that although digital therapeutics are still in their infancy in China, there are some differences in the industry regarding the definition and framework of existing digital therapeutics. However, it is basically clear that the full embodiment of digital therapeutics will definitely be a kind of medical device, specifically falling under the category of SaMD (Software as a Medical Device). Therefore, the policies of local governments naturally appear in the form of supporting medical devices.

The first to notice digital therapeutics and take action was Hangzhou. On July 9, 2021, the General Office of the Hangzhou Municipal People's Government issued the "Several Opinions on Accelerating the High-Quality Development of the Biomedical Industry," proposing the ambitious goal of reaching a trillion-yuan scale for the city's biomedical and health industry by 2030, with digital healthcare (pharmaceuticals) included as a key focus area.

Hangzhou's "Opinions" first give strong support to the research and development of medical devices. For instance, for innovative Class II and Class III medical devices that have obtained a medical device registration certificate and are produced in Hangzhou, after evaluation, they will be granted financial support of up to 20% of R&D investment, with a maximum of 2 million yuan and 4 million yuan per variety respectively (including local clinical trial fee reductions).

Hangzhou has also supported the local application of Hangzhou-produced medical devices, mainly focusing on the two aspects of procurement and payment.

In terms of procurement, the "Opinions" propose that local medical institutions purchasing the first (set) of medical devices recognized by provincial and municipal departments will be rewarded with 20% of the procurement amount. At the same time, the use of recognized innovative pharmaceuticals and medical devices, as well as high-quality Hangzhou-produced pharmaceuticals and medical devices, will not be included in the assessment scope of the proportion of medicines and consumables in medical institutions, and a reward of up to 3% of the actual product usage amount will be given.

Of course, this support policy is aimed at medical devices that meet the requirements, and digital therapeutics are only a part of it. At the same time, the policy has set an upper limit, which is that the total annual reward for a single medical institution shall not exceed 3 million yuan.

Article 18 of the "Opinions" mentions "encouraging the application of medical artificial intelligence and new digital health services,"Support local medical institutions in participating in the pilot program for purchasing digital therapeutics products." This is also the first policy in China to explicitly encourage the procurement of digital therapeutics.

In terms of payment, Hangzhou also hopes to enrich the supply of commercial supplementary medical insurance products by leveraging local commercial insurance and other financial services, thereby strengthening the support of the medical insurance system for the application of innovative products, including digital therapeutics.

Finally, the "Opinions" also proposed the implementation of the "156 Action" for the biomedicine and health industry. It proposed to focus on five key areas: innovative drugs, medical devices, biotechnology + digital technology, pharmaceutical distribution, and medical health, and to carry out key tasks such as improving the R&D innovation system, perfecting the ecological service system, creating an enterprise cultivation system, building a digital empowerment system, establishing a modern distribution system, and strengthening the element guarantee system, with the ultimate goal of creating a trillion-yuan-level industrial cluster.

As we all know, Hangzhou has always been recognized as the leader in China's digital economy. According to statistics, in 2020, the core industries of Hangzhou's digital economy achieved operating revenue of 1.29 trillion yuan, a year-on-year increase of 15.4%; the added value reached 429 billion yuan, a year-on-year increase of 13.3%, accounting for 26.6% of that year's GDP. Its software and information technology services industry ranks among the top comprehensive competitiveness in major cities in China.

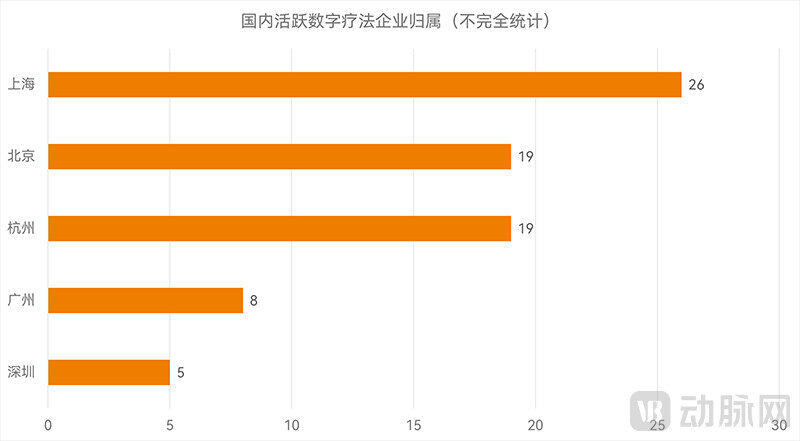

Attribution of Active Digital Therapy Companies in China (Incomplete Statistics, Chart by VCBeat)

With this strong foundation, coupled with policy support, Hangzhou has already formed a preliminary industrial cluster in digital therapeutics — among the more than a hundred active digital therapeutics companies in China, Hangzhou is home to as many as 19 such companies. In December 2021, China's first digital therapeutics industry park — Hangzhou Digital Therapeutics Industry Park — was established under the guidance and support of the government of Hangzhou's High-tech Industrial Development Zone (Binjiang).

It can be said that, with the dual efforts of policy and industry foundation, Hangzhou has already gained an edge in the fiercely competitive "talent grab" battle in the field of digital therapeutics.

In addition to Hangzhou, Hainan Province has also given policy preference to digital therapy. Announced in January 2022,The "14th Five-Year Plan for Digital Health Development in Hainan Province" includes "exploring the pilot use of digital therapeutics" as one of the main tasks for digital health development in Hainan Province during the 14th Five-Year Plan period. This is also the first time that digital therapeutics have been included in a provincial plan.。

Despite Hainan Province's lack of corresponding foundation in the past, its advantages in institutional integration and innovation remain impressive: For instance, the registration and access policies for Hainan's pilot program on the application of real-world clinical data, as well as the policy advantages of zero tariffs, low tax rates, simplified tax systems, relaxed market access, and the establishment of high-level data platforms such as the electronic prescription center in the Hainan Free Trade Port are still quite attractive.

However, compared to Hangzhou, Hainan has a much weaker foundation in the digital economy industry. The effects of these policies still require some time to observe. Nevertheless, according to VCBeat, a considerable number of digital therapeutics companies have shown strong interest in Hainan, and some enterprises have already settled locally.

At least on the surface, these regions that have been given policy preferences have already gained an advantage in the "talent grab" competition.

As mentioned earlier, digital therapeutics should actually be a type of SaMD. In foreign countries, the mature regulatory systems for digital therapeutics are all based on this. In other words, whether gaining regulatory approval through providing clinical evidence and obtaining a medical device license is an important development milestone for digital therapeutics companies.

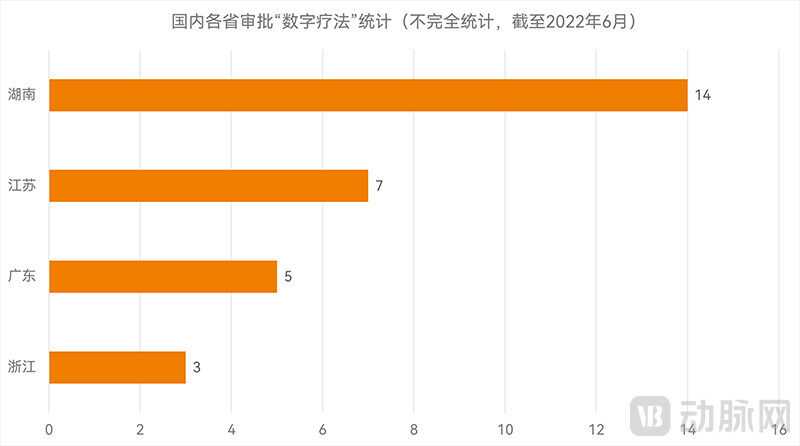

The vast majority of digital therapeutics should fall under the category of Class II medical devices, approved by the provincial bureaus of the NMPA. Therefore, the inclination towards digital therapeutics is also evident from the current status of approvals across regions. According to statistics from VCBeat, as of June 2022, among the SaMDs that have been approved and meet the definition of digital therapeutics, 14 were approved in Hunan, accounting for nearly 40% of the total number of digital therapeutics in the statistics.

As of June 2022, Statistics on the Approval of "Digital Therapeutics" in Various Provinces (Incomplete Statistics, Chart by VCBeat)

Hunan Approved Digital Therapies Mainly Divided into Two Categories: One is Cognitive Function Digital Therapy, with a Total of 7 Products. Among All 11 Cognitive Function Digital Therapies Counted, "Xiang Medical Device Approval" Accounts for Over 60%. The Second Category is Ophthalmic Digital Therapy, with a Total of 7 Products, Mainly Involving Training and Treatment for Symptoms Such as Strabismus and Amblyopia.

If we look at the approval timeline, 2022 is a significant turning point. Before this, Hunan approved five digital therapies, which was comparable to other regions. However, after entering 2022, Hunan rapidly approved nine digital therapies, showing a clear acceleration in the approval process. Among these, there were five cognitive function digital therapies and four ophthalmology digital therapies.

In a public speech, relevant persons from the regulatory department of Hunan Province also mentioned that Hunan hopes to make efforts in the registration of medical devices. Following the "five best" principles of product registration—“the simplest documentation, the fewest steps, the shortest time, the most optimal cost, and the best attitude”—Hunan aims to become a policy lowland and innovation highland for the development of China's medical device industry.

For Class II innovative medical devices, Hunan Province has also introduced a series of preferential policies, including "priority processing procedures," "early intervention and dedicated personnel responsibility," "exemption from product registration fees (50,400 yuan for Class II medical device registration)," "financial subsidies (up to 500,000 yuan for single varieties of domestically首创, patented Class II innovative medical devices)," and "contract manufacturing."

In December 2021, Hunan also released"Hunan Provincial Drug Administration Announcement on the Release of Business Processes for Class II Medical Devices/In Vitro Diagnostic Reagents Registration" has taken the lead in reducing the time from application to final certification for Class II certificates from the original statutory period of 80 working days to 40 working days, increasing the approval speed by 50%.。

This may also be one of the reasons why the number of digital therapy approvals in Hunan has surged.

These preferential policies have also attracted some digital therapy companies whose headquarters are not in Hunan to set up subsidiaries locally. Perhaps their initial purpose was to obtain certification quickly, but no one can deny the possibility that they may subsequently increase investment in their subsidiaries, thereby driving local industrial clustering.

After all, Hunan also boasts the prestigious "Xiangya System" academic and clinical resources.

Other regions have also followed suit, entering the "involution" mode. From 2021 to present, Hubei, Jiangsu, Shandong, Shanghai, and Guangdong have successively introduced policies to shorten the certification time for Class II medical device licenses. Among them, Shandong has even proposed further reducing the time to 30 working days.

From the perspective of approval status, the number of digital therapies approved in these regions also ranks at the forefront. From 2021 to now, the number of digital therapies approved in Jiangsu (4), Zhejiang (3), and Guangdong (3) is second only to Hunan. It can be foreseen that as these preferential policies become known to more people, the number of digital therapies approved in various regions will also increase rapidly.

In addition to compressing the approval speed, obtaining reasonable clinical trial exemptions is also a common approach to accelerate the registration of medical devices. Currently, according to relevant regulations, clinical exemptions for Class II medical devices are mainly divided into two categories. The first category involves comparison with similar medical devices, utilizing clinical trial or clinical usage data obtained from similar medical devices for analysis and evaluation, thereby proving the safety and effectiveness of the product.

Another category of situations involves products listed in the NMPA's "List of Medical Devices Exempt from Clinical Evaluation." In the latest version of the clinical exemption list, several Software as a Medical Device (SaMD) products are exempt from clinical trials. Registered products can be compared with the list of exemptions, and if they meet the relevant descriptions, they can quickly obtain certification through the exemption from clinical evaluation.

However, the latest version of the "List of Medical Devices Exempt from Clinical Evaluation" includes SaMD that can be exempted from clinical evaluation, such as "trace analysis software," "clinical management software," "radiotherapy record and verification system software," "radiotherapy contouring software," "medical imaging storage and transmission system software," "medical image processing software," and "data processing software." Theoretically, these categories deviate somewhat from the definition of digital therapeutics.

As a leading digital therapeutics CDMO and full-process service provider in China, Fang Qiuxue, Marketing Director of SLANHEALTH, believes that for the industry to further develop, the first issue to address should be clinical effectiveness. It is essential to ensure that the treatment outcomes of digital therapeutics products are based on rigorous clinical research conducted in real-world settings, allowing doctors to prescribe without any concerns. "After all, the essence of digital therapeutics is serious medical care, and scientifically rigorous clinical treatment effects are the most important," she stated.

Regulatory agencies are also rapidly exploring more appropriate regulatory pathways for digital therapeutics. Fang Cong, the founder of Shudan Medical, who previously worked at Yitu Healthcare, is one of the few experts in the digital therapeutics industry to have experienced both the initial stages of artificial intelligence and digital therapeutics. She stated that any medical innovation poses a new challenge for regulatory approval.

"Reviewing the FDA's approval strategy for digital therapeutics, I think it is very similar to the regulatory approval of medical artificial intelligence products in recent years, that is, 'compatible with the process and responsible for the results'. For example, the classification definition is based on the analogy of functionally similar products in traditional classifications, and is determined according to their involvement in clinical applications. This way of controlling key parameters and outcomes might help China establish its own digital therapeutics approval system as soon as possible," she said.

Precisely because of the popularity of digital therapeutics, regulatory agencies are also gradually improving the corresponding regulatory framework. In March 2022, the NMPA simultaneously released three important digital health guidance principles: "Guiding Principles for the Registration Review of Medical Device Software (2022 Revised Edition)," "Guiding Principles for the Registration Review of Medical Device Cybersecurity (2022 Revised Edition)," and "Guiding Principles for the Registration Review of Artificial Intelligence Medical Devices."

Among these,The revised "Guiding Principles for the Registration Review of Medical Device Software (2022 Revised Edition)" has significant changes compared to the 2015 version. It is explicitly stated that this will form the foundation of the medical device digital health guidance principle system and serve as the general guiding principle for SaMD.; In conjunction with cybersecurity and artificial intelligence guidelines, basic coverage of digital healthcare will be achieved.

On the one hand, as localities gradually follow up with policy incentives and the understanding of digital therapeutics deepens, the future regulatory approval landscape for digital therapeutics may become more decentralized; on the other hand, foreseeable regulatory provisions will clearly be more targeted and practical. Therefore, merely tilting the scale in favor of obtaining certification and approvals may not be sustainable—it is also necessary to further strengthen other essential elements to achieve industrial clustering.

So, what are the most critical elements for digital therapeutics companies? Many companies have indicated that the most crucial factor is still talent. As an interdisciplinary field, digital therapeutics requires teams capable of closely integrating digital technology with medicine.

Simply put, digital therapies that pass the approval process must be part of SaMD (Software as a Medical Device), and they also fall under the scope of software development. In terms of underlying logic, technical processes, and technical pathways, the requirements for developing general software are essentially identical to those for developing SaMD.

However, as a medical device, SaMD also needs to focus on the core medical principles. "For instance, in the entire presentation process, what elements play the strongest therapeutic role and which are useless? There needs to be corresponding scientific evidence, research findings, and clinical applications. Moreover, attention must be paid to whether there are any adverse reactions or even serious medical accidents during the product's use. This part is a significant difference," said Chen Hang, Medical Advisor for Bock Shukang Vision Technology (Hangzhou) Co., Ltd.'s pediatric digital therapy for amblyopia and strabismus, and Founder & CEO of ClearView Bio, emphasizing that digital therapy professionals need to balance both technology and medicine.

Ningdong Wansheng Medical Technology (Wuhan) Co., Ltd.'s digital therapy for specific phobias was recently approved. Its founder and CEO, Boya Dong, also stated that digital therapy is an entirely new interdisciplinary field requiring a comprehensive talent team with a deep understanding of both digital technology and medicine: "If we go into more detail, it requires talents with multidimensional capabilities in areas such as human-computer interaction, algorithm software development, regulatory registration, and clinical applications. There are no corresponding talent resources available in the market for companies to tap into."

"Therefore, we believe that the most important factor is actually talent. Regions with excellent scientific research talent reserves, high-quality medical expert resources, and highly professional civil service teams are very attractive to digital therapeutics startups like ours," said Dong Boya further.

In this aspect, first-tier cities represented by Beijing and Shanghai have unique advantages.

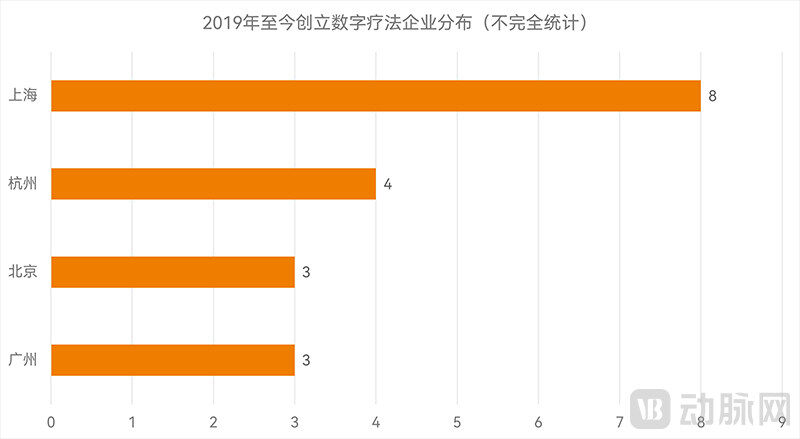

Regional Distribution of Digital Therapeutics Companies Established from 2019 to Present (Incomplete Statistics, VCBeat Mapping)

Although the policy inclination in these two regions is not particularly prominent, they have still become the main hubs for digital therapeutics. Take Shanghai as an example: it leads by a wide margin with 27 digital therapeutics companies, and from 2019 to the present, eight new digital therapeutics companies have been established, making it the most active region for startups during this period. As for Beijing, it also has as many as 19 digital therapeutics companies.

At the same time, these two regions also have the highest concentration of high-quality medical resources in China. According to the latest "2020 China Hospital Rankings" released by the Fudan University Hospital Management Research Institute, Beijing has 23 hospitals on the list, while Shanghai has 19 – together, they account for forty percent.

However, first-tier cities also have their own troubles. The high operating costs are undoubtedly one of the biggest concerns, which puts enormous pressure on digital therapeutics startups. Meanwhile, compared to other regions, first-tier cities tend to support larger enterprises, paying relatively less attention to smaller businesses like those in digital therapeutics.

Take the approval of certification as an example: only one ophthalmic digital therapy has been approved in each of Beijing and Shanghai. Compared with the status of the two places in the medical device industry, this is really disproportionate. Because of this, many companies headquartered in these two cities prefer to obtain certification in other regions.

At the same time, the high cost of living and the initial formation of industries in second-tier cities have also led to a talent outflow from first-tier cities back to second-tier cities. Some of these second-tier cities possess medical resources that are no less impressive than those in first-tier cities — in the "2020 China Hospital Rankings," Wuhan, Hangzhou, Chengdu, Chongqing, and Nanjing each had four or more hospitals selected.

In view of this, some digital therapeutics companies in first-tier cities have also indicated that they may relocate from these high-cost cities in the future, retaining only nominal headquarters functions.

From the current situation, digital therapeutics, which are in the early stage of development, are increasingly gaining attention in various regions. These regions are also gradually starting to attract companies through various means in order to gain an edge in this "talent grab" battle, ultimately achieving industrial clustering.

Based on different situations, the policy entry points vary from region to region, and the effects are also different. Places such as Beijing, Shanghai, Guangzhou, Hangzhou, Hunan, and Hainan have gained an early advantage. However, it is certain that over time, policies will gradually converge, and latecomers may still have the possibility to catch up or even surpass. At the same time, the rapid development of the industry will inevitably lead to more targeted and operational supervision. The boost from policies will ultimately return to the competition of internal strengths, such as the accumulation of talent resources and the establishment of industrial foundations.

Therefore, this "talent grab" battle can be considered a marathon, and it may be difficult to see results in the short term. Nevertheless, this is itself a positive signal for the industry. VCBeat will continue to follow industry trends and bring fresh reports to everyone, and we also welcome the industry to provide us with relevant reporting leads.

References:

CAICT: "China Digital Economy Development Report (2022)"

"The 14th Five-Year Plan for the Development of Hangzhou's Digital Economy"