MicroPort NeuroTech, MicroPort's Fourth Spin-off, Files for Hong Kong IPO Amid Aggressive Subsidiary Listing Strategy

MicroPort

High-end Medical Device R&D and Manufacturer

On July 15, MicroPort's fourth subsidiary, MicroPort NeuroScience, was listed on the Hong Kong Stock Exchange.

Previously, MicroPort has successfully spun off three listed companies: HeartRay Medical, HeartValve Medical, and MicroPort Robotics. Another subsidiary, MicroPort EP, has submitted its listing application on the STAR Market.

MicroPort Chairman Chang Zhaohua once said: MicroPort is a company with the genes of a trillion-dollar market value.

These four listed companies are just the tip of the iceberg in MicroPort's trillion-dollar market value plan. Through its twelve major groups, MicroPort has prepared subsidiaries with a business scope covering cardiovascular and structural heart disease, electrophysiology and heart rhythm management systems, bone and soft tissue repair, aortic and peripheral vascular diseases, medical robotics, in vitro diagnostics and in vivo imaging, and solid tumor treatment.

The continuous spin-offs have not pushed up the market value of MicroPort, whose market value has dropped from a peak of 100 billion yuan to only over 36 billion yuan now. The market value of the subsidiaries after the spin-offs is also around 10 billion yuan.

Another leading medical device company in China, Mindray Medical, has chosen not to pursue a spin-off listing, with a market value approaching 400 billion yuan.

Although the spin-offs have brought higher management costs, they also enabled MicroPort to quickly cover multiple potential markets in a short period of time. Does the listing of MicroPort BrainScience prove the replicability of the spin-off plan? What impact does it bring to MicroPort's spin-off strategy? How are the three listed companies performing? VCBeat (WeChat ID: vcbeat) conducted an analysis and interpretation.

MicroPort Brain Sciences, as the fourth company of MicroPort Medical, opened at 24.7 yuan, slightly fell on the first day, with a total market value of 14.333 billion yuan.

Although MicroPort Brain Science is named in relation to brain science, which Elon Musk also focuses on, its business does not involve brain-computer interfaces or chips. Instead, it primarily treats blockages, ruptures, strokes, and cerebral hemorrhages of cerebral blood vessels, originating from the neuro-intervention field.

According to the "Report on Cardiovascular Health and Diseases in China 2021," there are 13 million cases of stroke. As neurointerventional treatment has developed relatively late in China, products have been mainly dominated by imported brands. However, with domestic companies beginning to engage in independent research and development, the localization of neurointerventional products has become a focal point in the primary market, attracting over 20 companies. Leading enterprises have also secured substantial financing.

On November 11, 2021, MicroPort NeuroScience completed a $150 million financing round, with a pre-IPO valuation of up to 11.2 billion RMB.

The neurointerventional market has a large number of participating companies. Someone once described the neurointerventional market in one sentence: "They all dislike each other, but none can eliminate the other." This statement actually reflects that domestic neurointerventional companies cannot pull away from each other in terms of either products or revenue.

What are the characteristics of MicroPort Brain Science in the nearly identical neurointervention market?

In terms of revenue, MicroPort Brain Sciences has achieved profitability in the neurointervention market, ranking among the leading Chinese neurointervention companies, which are generally in a loss-making state.

MicroPort NeuroTech's revenue in 2019, 2020, and 2021 was RMB 184 million, RMB 222 million, and RMB 382 million respectively, with a 73.3% increase in revenue in 2021. MicroPort NeuroTech's adjusted profits for 2019, 2020, and 2021 were RMB 46.98 million, RMB 47.55 million, and RMB 91.91 million respectively.

Although MicroPort NeuroTech has shown leading performance among domestically produced enterprises in China, its commercialization in the past few years has not been impressive compared to the true leaders of the neurointerventional market—imported enterprises. In terms of product market share, MicroPort NeuroTech's products have been on the market for quite some time, yet they hold a relatively low market share.

MicroPort NeuroTech has successively developed and industrialized the first cerebral vascular stent in China's neurointerventional field, the apollo™ Intracranial Artery Stent System, as well as the first domestically produced intracranial covered stent, the willis® Intracranial Covered Stent System, and the first blood flow diverter in China, the tubridge® Vascular Reconstruction Device.

Among them, the intracranial stent Apollo was approved in China as early as 2004, the Willis covered stent was approved in 2013 in China, and the Tubridge flow diverter stent was approved in 2018.

Although it was approved early, leaving more time for MicroPort NeuroScience's domestically produced alternatives, the market share captured by MicroPort NeuroScience in those years was not significant.

Compared with global players in the neurointerventional market, MicroPort Brain Science is still at a disadvantage.In terms of sales revenue of neurointerventional medical devices in 2020, the top four players in China's neurovascular medical device market—Medtronic, Stryker, MicroVention, and Johnson & Johnson Medical—still accounted for over 85% of the market, while MicroPort Brain Science held a 4% share of the entire neurointerventional market in China.

According to CIC Consultancy, the scale of China's neurointerventional medical devices market is expected to expand from RMB 5.8 billion in 2020 to RMB 17.5 billion in 2026, with a compound annual growth rate (CAGR) of 20.1%. In 2020, 160,000 neurointerventional surgeries were performed in China.

The future market is expected to reach billions, indicating that the market space for neurointervention is sufficiently large, and the space for domestic substitution is also significant. However, the development of MicroPort Neuromodulation has confirmed that domestic substitution is not an easy path. It is not as simple as achieving a surge in sales once the product hits the market, especially in the field of neurointervention where there are high demands for products.

MicroPort NeuroTech needs to strengthen its product line and commercialization to support its high valuation.

MicroPort NeuroTech went public in July 2022; MicroPort Robotics went public in November 2021; MicroPort Cardiopath went public in April 2021; MicroPort Endovascular went public in July 2019.

MicroPort maintains an average pace of listing one company per year. This spin-off plan was initiated by MicroPort as early as 2012. The first company to be spun off was Shanghai MicroPort Heart Technology, which was established in 2012.

MicroPort Chairman Chang Zhaohua once said, "We have been preparing for the spin-off of Heartpulse Medical for a long time, and it was very difficult in the early stages. With the advent of the STAR Market, the listing process for Heartpulse Medical has been shortened from three years to three months. The arrival of the STAR Market has also given MicroPort more confidence in its spin-off plans. I believe the path for spin-offs will become broader as long as the registration system is implemented, starting from the STAR Market to the ChiNext and then to the main board. I think there is great hope."

Why Did MicroPort Plan for a Spin-off IPO So Early?

On the one hand, it is to provide more incentives for MicroPort executives and retain more talent.

Minimally Invasive High-Value Consumables: A Complex Field with Multiple Independent Segments

Chang Zhaohua also once stated at the shareholders' meeting: Without subsidiaries going public, it would be impossible to complete the incentives for senior executives. MicroPort has a large number of managerial talents, with 70-80 people at the VP level or above, as well as many R&D talents. Everyone hopes to have a continuous career and achieve financial freedom at MicroPort. A small pond cannot accommodate so many talents; only multiple ponds can.

The spin-off listing of MicroPort's subsidiary has indeed provided some shareholders with high returns.

Taking MicroPort Cardio as an example, the company's initial shareholder, Honghao Investment, was an investment entity established to address the insufficient funding of MicroPort Cardio at that time by raising capital from shareholders and internal employees of MicroPort. Its shareholders include the main shareholder of MicroPort, the Jinsanjinmei Foundation, institutional shareholders with indirect holdings, and executives and employees of the MicroPort group such as Dong Yunxiao, Peng Bo, Xu Yimin, Sun Hongbin, CHENGYUN YUE, HONGYAN JIANG, Cai Linlin, and others. In August 2021, Honghao Investment planned to reduce its holdings by 779,900 shares in MicroPort Cardio, cashing out 263 million yuan. Although the reduction plan was terminated, it highlights the high returns brought about by the listing of subsidiaries.

The purpose of the spin-off, on the other hand, is to raise more funds for research and development. MicroPort Medical does not just want to be a company in the field of coronary intervention; it aims to become a giant covering multiple fields. Relying on past profits alone cannot cover the extensive R&D pipelines and projects.

In the past, the main profit of MicroPort Medical came from the profits generated by coronary drug stent revenue. In 2019, the net profit attributable to the parent company of MicroPort Medical was 323 million yuan, compared to 164 million yuan in 2018.

The subsidiaries spun off by MicroPort have also been favored by investment institutions. Behind entities like Endovastec, VascuTron, MicroPort Robotics, and MicroPort Electrophysiology, there are several well-known investment institutions placing their bets, including Huaxing, Hillhouse, CPE Yuanfeng, and CICC.

When MicroPort Robot went public, Hillhouse Capital indirectly held 8.05% of the shares, making it the largest external institutional shareholder; Huaxing Capital is the largest shareholder of Xinmai Medical; CICC Healthcare is the largest shareholder of Xintong.

But the method of spinning off subsidiaries for external financing and IPOs also has risks. A major characteristic of MicroPort's subsidiaries is that almost all of them lack an actual controller.

At the time of its IPO, MicroPort EP had a shareholding structure where the voting rights of two major shareholders, Jiaxing Huajie (affiliated with Huaxing Capital) and MicroPort Investment, were relatively high but neither exceeded 50%. The issue of lacking an actual controller drew regulatory attention and was highlighted in both rounds of inquiries.

MicroPort's spin-off plan has been implemented for several years. Judging from the performance of the previous four subsidiaries, there are differences among them. Endovastec, Heart Technology, MicroPort Robot, and MicroPort NeuroScience have developed different trends.

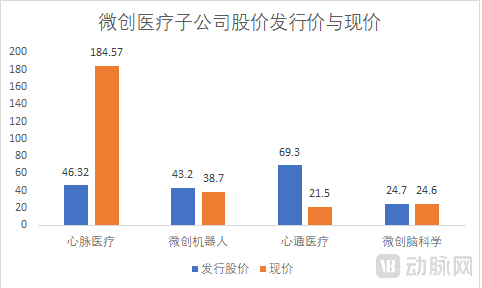

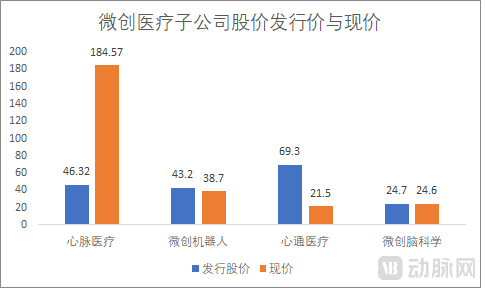

In terms of market value, Cardionovum is valued at 13.2 billion yuan, with an issue price of 46.32 yuan and a current stock price of 184.57 yuan; MicroPort Robotics is valued at 37.3 billion Hong Kong dollars, with an issue price of 43.2 Hong Kong dollars and a current price of 38.7 Hong Kong dollars; MicroPort CardioFlow is valued at 6.93 billion yuan, with an issue price of 21.5 Hong Kong dollars and a current stock price of 2.8 Hong Kong dollars. MicroPort NeuroTech is valued at 14.3 billion yuan, with an issue price of 24.7 Hong Kong dollars.

Apart from MicroPort, the other three have already fallen below their issue price.

Among the four subsidiaries, the most profitable and the one with the best stock price performance is Shanghai MicroPort CardioFlow Medtech, which originated from the earliest spin-off in the aortic stent and peripheral vascular business fields.In the field of aortic stents, aortic diseases are highly dangerous. Although the number of aortic stent surgeries in China has not exceeded 50,000 cases, the unit price of aortic stents is high. MicroPort CardioFlow, relying on its aortic stent product Castor, generates hundreds of millions in revenue annually. In Q1 of 2022, MicroPort CardioFlow achieved a revenue of 258 million yuan (+30.59%).

MicroPort Robot is currently the subsidiary with the highest market value and the most investment in R&D.MicroPort's robotic business covers five major tracks: endoscopy, orthopedics,泛vascular, natural orifice, and percutaneous puncture. Through R&D investment, MicroPort's surgical robot progress has been rapid.

Among them, the laparoscopic surgical robot, Tumai Robot, is对标to the Da Vinci Surgical Robot. Tumai has made rapid progress in clinical trials, completing the registration clinical trial in urology in May 2021, initiating multi-disciplinary and multi-center clinical trials in general surgery, thoracic surgery, and gynecology in October 2021, and obtaining NMPA approval for marketing in 2022.

The joint replacement surgical robot Honghong completed the registration clinical trial for total knee arthroplasty in July 2021 and submitted a registration application to the NMPA. In July this year, MicroPort's minimally invasive joint replacement surgical robot received FDA certification, becoming the first Chinese surgical robot to obtain FDA certification.

The R-ONE® Vascular Interventional Surgical Robot, jointly introduced by MicroPort Robotics and the French company ROBOCATH S.A.S., completed the first case enrollment for NMPA registration clinical trials in November 2021.

MicroPort Robot's Rapid Progress in Multiple Surgical Robot Pipelines Owes Much to IPO Financing. After going public, the company secured substantial funding for MicroPort Medical's R&D, with investments in robot R&D reaching 390 million yuan in 2021, a threefold increase from 130 million yuan in 2020. Currently, MicroPort Robot is still incurring losses, with a deficit of 580 million yuan in 2021.

MicroPort CardioFlow Medtech is in the stage of accelerating commercialization. Transcatheter aortic valves face commercialization challenges in China.To accelerate the commercialization of TAVR products, MicroPort CardioFlow has adopted a low-price strategy compared to similar products, with its TAVR product priced approximately 50,000 yuan lower than other domestically produced products. The annual revenue of MicroPort CardioFlow increased by 93.2% year-on-year from 103 million yuan in 2020 to 200 million yuan in 2021.

Although the performance of subsidiaries after spin-offs varies, it might be beneficial for the parent company either way. A high-growth product spin-off can bring more momentum, while underperforming businesses can have less drag on the parent company when developed independently.

In contrast, another leading domestic medical device company, Mindray, which is developing globally, has taken a different path.

From the annual report revenue, the company achieved operating income of 21.02 billion yuan, an increase of 27.00% over the same period last year; total profit was 7.43 billion yuan, an increase of 38.56% over the same period last year; net profit attributable to shareholders of listed companies was 6.65 billion yuan, an increase of 42.24% over the same period last year. The proportion of Mindray's overseas market in 2021 dropped to 39.61%. Mindray stated that it plans to increase the proportion of overseas business income to 70% in the future.

The problems faced by the two companies are different, and the solutions provided are also different. Mindray is currently focusing on more stable global development to address the uncertainties in the development of the global market environment.

Against the backdrop of increasing uncertainty in global market development, ensuring the stability of the supply chain has become a major challenge. Over the past two years, Mindray has been addressing the issue of domestic substitution for upstream raw materials and components. To secure a stable supply of key raw materials required for Mindray's chemiluminescence business and to enhance the quality of luminescent reagents, Mindray completed the acquisition of HyTest Bio for 4 billion yuan.

From the development paths of Mindray and MicroPort, it is evident that no single development model can be continuously replicated and imitated. Mindray and MicroPort have different core businesses, distinct advantages, and varying growth trajectories. A single tree does not make a forest, and we look forward to both companies bringing more vitality to China's medical device industry.