Oral Healthcare Upstream: The 'Chain Leader' Behind a Golden Track — Three Mega-Trends Launching a New Journey

Danaher

Product Design and Manufacturer

ANGELAIGN

Dental Medical Consumables Supplier and Service Provider

Amid the prevailing consumer upgrade and the economy of aesthetics, people's demand for dental health and aesthetics is becoming increasingly strong, making the dental track a hot pursuit. Since last year, companies such as Dr. Tooth, China Oral Medical Group, and Longvision have submitted their prospectuses, while ANGELAIGN and Rui'er Group have gone public successively. Meanwhile, numerous investment institutions are betting on the primary market, with 37 financing events occurring in the dental industry. Among them, the upstream of dental medical care has received the most attention from capital and has the highest frequency of financing in the past two years.

Through a series of analytical studies, CYGNUS EQUITY has identified three major trends—domestic substitution, digitalization, and platformization—that are bringing a series of innovation and transformation opportunities to the upstream sector of dental healthcare. The CYGNUS team remains optimistic about the development prospects of the upstream dental healthcare industry, conducts in-depth analyses of the three trends, and proposes three key dimensions for evaluating high-quality enterprises. This article aims to facilitate discussions with entrepreneurs and investors in this field.

Core Argument of This Article:

1. In recent years, the upstream of the oral industry has been highly sought after by capital. It possesses natural attributes such as high entry barriers, strong technical barriers, and powerful scalability, demonstrating multi-dimensional advantages from profitability to concentration and market potential. It is the "chain master" behind the golden track of dentistry.

2. The domestic substitution of upstream equipment and consumables in the dental industry is in full swing. "Cost-effectiveness" remains the main hallmark of domestic substitution at this stage, with some products still in a price war due to homogeneity. At the same time, we are pleased to discover that an increasing number of globally leading products are being reverse-exported worldwide. Looking at the global upstream dental market, the TOP10 is still dominated by overseas companies. High-value, high technological barrier, and differentiated products are expected to achieve continuous breakthroughs. The road ahead is long, but the future is promising.

3. The digitalization of the dental industry is accelerating, and digital-integrated treatment solutions represented by invisible orthodontics have already proven their significant value. Digital-integrated treatment solutions offer substantial underlying optimization logic in terms of precision treatment, doctor efficiency, customization, and aesthetics. From the perspective of both service providers and consumers, embracing digital treatment is an inevitable trend.

4. Platform-based enterprises have significant reuse and synergy in brand, R&D, channels, and digitalization, with stronger risk resistance and higher potential. Nine out of the top 10 global upstream dental brands possess clear platform-based characteristics. However, it is important to note that as these enterprises expand their product lines, management complexity increases significantly. How to build product strength comparable to single-product-focused companies while maintaining the advantages of a platform-based enterprise may become an important challenge and potential barrier.

5. Enterprises with independent R&D and innovation capabilities at the grassroots level, the ability to integrate software and hardware, and platform-based management capabilities have the opportunity to stand out in the upstream wave of the dental industry. The new journey is not only about simply achieving a larger market share for domestically produced alternatives but also about going global and participating in the broader opportunities of worldwide competition.

China's dental healthcare market is entering a period of rapid growth. According to a Frost & Sullivan report, the compound annual growth rate of China's dental healthcare service market reached 9.6% over the past five years, with the market size increasing from 91.8 billion yuan in 2017 to 119.9 billion yuan in 2020. It is expected to reach 173.9 billion yuan by 2022.

Based on the vast market, an increasing number of companies are entering the field. Data from Tianyancha shows that in just the first half of this year, over 3,000 dental-related enterprises were newly established across China, meaning more than 500 new businesses were born each month. These enterprises are distributed across various segments of the dental industry chain.

Specifically:

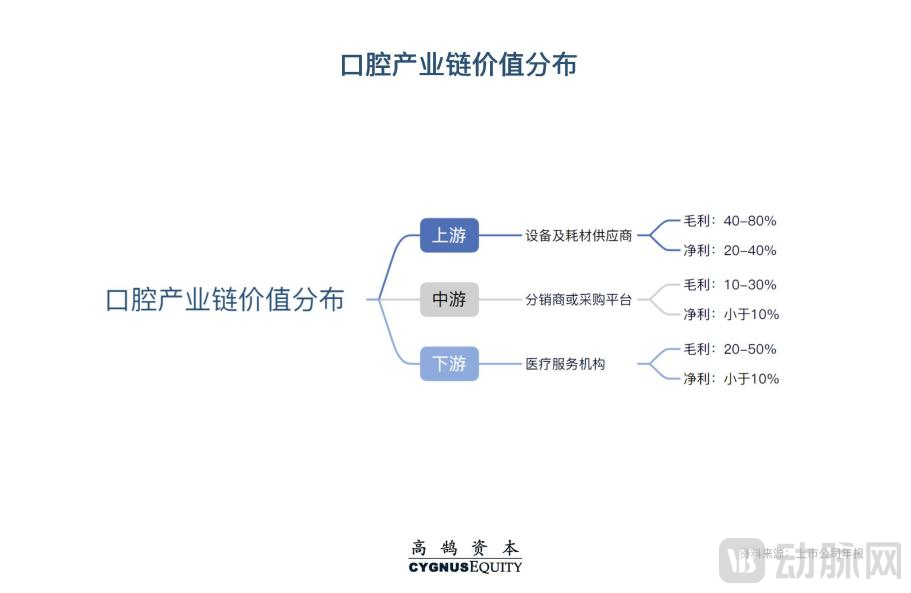

·The upstream mainly consists of consumables and equipment R&D manufacturers, including large equipment such as imaging and dental chairs, small equipment for fillings and whitening, and also the consumables required for dental implants, orthodontics, and dentures.

·The midstream mainly consists of traditional dental equipment and consumables distributors, information software providers, and dental support organizations, etc.;

·The downstream mainly consists of various medical service institutions, including the dental departments of public hospitals, private dental hospitals, and clinics.

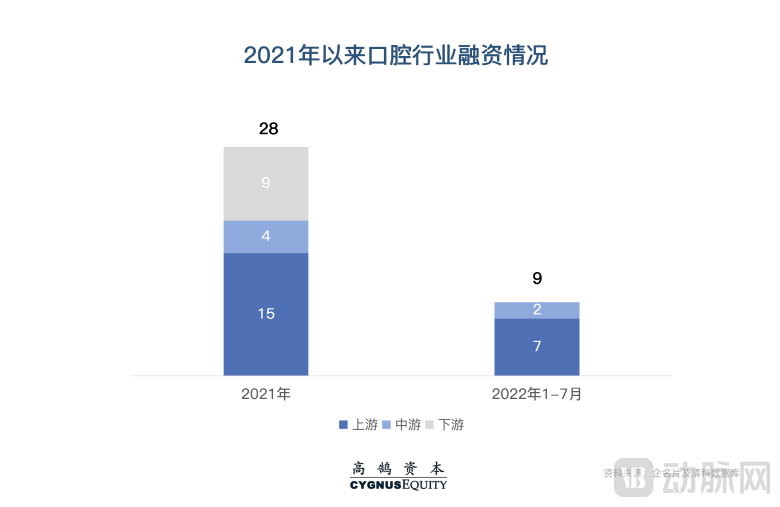

Under the heated competition, the upstream of oral healthcare has become the most capital-focused and highest-frequency financing field in the past two years.Since 2021, upstream enterprises in the oral healthcare industry have maintained a steady pace of financing, with the number of financing events accounting for more than half of the total in the entire industry.

Behind the capital's pursuit, there is a close relationship with the three major characteristics presented by the upstream of the dental industry.

1. The entry threshold is high.The upstream of the oral industry mainly consists of consumables and equipment, all of which require medical product qualifications, such as the Medical Device Manufacturing Enterprise License, Medical Device Operating License, and the registration certificate for medical devices with a "Zhun" character mark. This means that any product that can be marketed must undergo rigorous clinical trials and approval processes, which can take a minimum of 2 years and up to more than 5 years, resulting in a long time cycle and high entry barriers.

Second, the technical barriers are strong.As medical consumables and devices, oral-related products are mostly the result of multidisciplinary integration, which tests the fusion of engineering, biology, physics, and even aesthetics. For example, the technical barriers of dental implants are mainly reflected in materials, design, surface treatment, and other aspects. An ideal dental implant should possess good mechanical properties, biocompatibility, and initial stability, so the materials of dental implants need continuous optimization to pursue better mechanical properties and biocompatibility.

Third, it has strong extensibility.The instruments, consumables, and equipment in the upstream of the dental industry, as a more standardized field, have stronger extensibility. Meanwhile, upstream dental products can expand into the global market and achieve economies of scale. For example, representative upstream companies such as DENTSPLY SIRONA, Danaher, and Straumann are all global enterprises.

These characteristics have built a relatively wide moat for upstream enterprises in the oral healthcare industry and demonstrated two major advantages.

First, profitability is strong enough.Upstream companies in the dental industry chain have a relatively better competitive landscape. Considering factors such as the decentralization of downstream players and dentists' trust in and usage habits of high-quality products, these collectively help upstream companies more easily gain pricing power.

As can be seen from the figure below, in the value distribution of the dental healthcare industry chain: upstream equipment and consumables suppliers have the strongest profitability, followed by downstream medical service institutions, while the profit margin of midstream distributors or procurement platforms is compressed most severely.

In terms of net profit, except for "Tooth茅" TMC (Tongce Medical), whose net profit can reach nearly 30%, the net profit of most dental medical service institutions is within 10%. Some listed companies are still in a loss-making state. The reasons behind this, apart from the doctors, include high marketing and customer acquisition costs, which have squeezed the profit margins of dental service providers. How to build a differentiated reputation will become the key to breaking through for downstream enterprises.

Midstream distributors and procurement platforms, due to the lack of core technology and product capabilities, face low barriers to entry. Their channel resources are severely restricted by regional limitations, and the rise of emerging sales channels such as e-commerce further compresses their profit margins.

In contrast, the upstream sector, with its three major characteristics forming a relatively wide business moat, possesses stronger profitability. The profit margin of upstream companies is often above 15-20%.

Second, the upstream market is more concentrated, and the potential market size of a single enterprise is larger.Due to the high entry barriers, upstream enterprises with technological barrier advantages are more likely to expand their markets and accelerate growth within a relatively reasonable competitive environment. They possess the competitiveness to become leading players in the field within a certain period, especially as the application of new technologies and materials allows upstream enterprises to continuously enhance product iterations, increasing downstream user stickiness. This enables them to achieve high market share and profitability, with greater potential for global expansion and higher growth ceilings, demonstrating excellent business logic.

Although downstream service providers in the oral healthcare industry have accumulated strong brand recognition through direct engagement with end consumers (C-end), they still need to address common industry pain points such as the shortage of dentists, limitations in chain expansion radius, and homogenized services. Breaking through these barriers requires standardized replication to overcome growth ceilings. Currently, the market share of leading companies in the industry has yet to exceed 3%, reflecting a relatively fragmented regional competitive landscape.

It is not difficult to see that,It is precisely due to the excellent profitability and higher market concentration that the upstream of the dental industry occupies a dominant position in the industrial chain, thus attracting capitals to rush for business opportunities.

In this process, in order to identify high-quality targets, it is necessary to understand the evolving trends upstream in the dental industry in order to accurately grasp the development trajectory of the industry.

Based on observations, three major trends are currently emerging in the upstream of the dental industry: domestic substitution, digitalization, and platformization, quietly bringing new growth to the dental sector.

With the continuous economic growth in China and increasing attention from the public on oral health issues, private dental clinics and hospitals in China have been rapidly emerging, driving a surge in demand for upstream consumables and equipment.Compared with demand, although the upstream has gradually achieved domestic substitution, the scale is still small. The high-end and high-value market is still dominated by imported brands, and there are no companies that can compete with overseas giants yet, leaving significant room for growth.

For upstream manufacturers in the oral healthcare industry, the key to achieving greater growth lies in whether they can make breakthroughs in a market traditionally monopolized by imported brands. Therefore, domestic upstream oral care manufacturers are motivated to continuously pursue technological and industrial breakthroughs, actively accelerating the pace of China-produced alternatives. Meanwhile, policies encouraging public hospitals and university dental institutions to choose domestically produced products have also driven the progress of China-produced substitution on the demand side.

We select two relatively representative upstream segments to observe the progress of this trend.

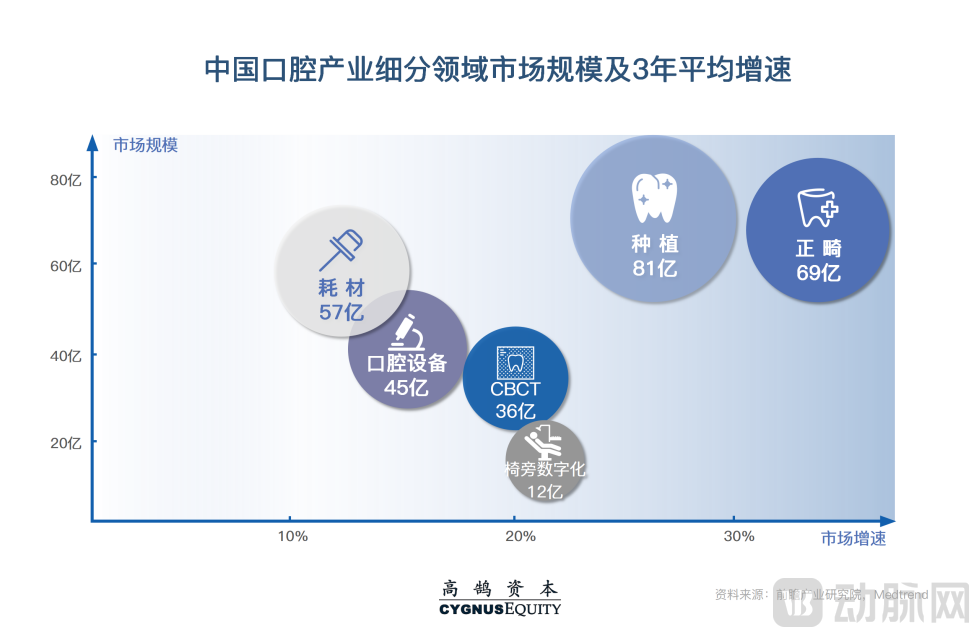

In the field of consumables, taking the dental implant track as an example, the localization rate of implants has long been at a low level, and the market has been mainly dominated by Korean and European brands.

In recent years, domestic manufacturers represented by Weihai Weigao Jielikang, Baichitai, Beijing Leiton Bio, Changzhou Baicont Medical, and others have been making efforts, gradually opening up the market with high cost-effectiveness. Some domestically produced implants have even reached the level of international first-tier brands. In market competition, South Korean implants adopt a relatively aggressive pricing strategy, with basic models priced at 5,000-6,000 yuan at the terminal end of dental hospitals, exerting strong price competition pressure on domestic medical device manufacturers who rely on cost-effectiveness. The centralized procurement of dental implants may become an important breakthrough variable in the localization process.

In terms of equipment, a typical representative is CBCT (Cone Beam CT), which has high technical barriers. Since CBCT offers a lower radiation dose, shorter scanning time, and higher image precision compared to spiral CT, it is more favored by the market.

In the early days, the mid-to-high-end market of CBCT in China was mainly dominated by imported brands, with unit prices around the million-yuan level, such as Germany’s KaVo, Dentsply Sirona, Finland’s Planmeca, and South Korea’s Vatech. Small hospitals and private clinics found it difficult to afford them. In recent years, we are pleased to see domestic brands capturing the market with product performance no less than overseas brands and ultra-high cost-effectiveness. The price of a single unit is only 200,000-400,000 yuan, allowing rapid penetration into institutions like second- and third-tier cities and private dental clinics. Meiya, Rayence, Born Dental, and Fussen are the top four brands in terms of market share, surpassing overseas brands.

Insights from the two fields of consumables and equipment:Although China's upstream dental industry has made certain achievements in the process of domestic substitution, it still faces new opportunities and challenges. In the early stage of this process, a cost-effective strategy may lead to price competition among manufacturers, but in the medium and long term, outstanding companies can achieve a positive cycle of product strength and brand power through continuous R&D investment, gaining higher market share and stable profits, as well as more opportunities to go global and participate in worldwide competition.

Digitalization is rapidly sweeping through the dental industry, focusing on providing consumers with better medical services and improving the treatment efficiency of doctors. Based on the dominant position of upstream industries, their equipment often becomes a data entry point. Comprehensive oral information data is detected through digital means, forming a powerful data analysis system. Digitalization influences the connection and development of all links in the industry chain, having a more prominent and far-reaching impact on the industry. Specifically, its influence is mainly reflected in two aspects.

On the one hand, upstream digitalization can provide consumers with customized precision medical solutions and scientific modeling schemes, improving doctors' diagnosis efficiency and users' treatment experience and outcomes.

On the other hand, upstream enterprises control the core data entry points. Through the accumulation of key dimensional data, they optimize auxiliary diagnosis and treatment solutions, gaining significant advantages in standing out in niche markets or discovering new opportunities, while also providing strong support for continuous product leadership iteration.

Digital diagnosis and treatment solutions represented by invisible orthodontics have been verified to be more comfortable, precise, and aesthetically pleasing compared to traditional silicone rubber and wire methods, with continuously increasing adoption rates. Taking the relatively untapped field of pediatric orthodontics as an example, the development of pediatric orthodontic appliances is more complex, and the shortage of specialized doctors makes treatment in this area more challenging than in other fields. Utilizing comprehensive data collection and processing through CBCT, intraoral scanners, and digital orthodontic systems not only ensures accurate parameter control and design but also facilitates intuitive communication between doctors and patients, providing a more personalized treatment experience and ensuring better orthodontic outcomes. It can be foreseen that in the rapidly growing yet highly competitive pediatric orthodontics market, possessing extensive data resources will provide a significant advantage in capturing this blue ocean.

Currently, most companies have made frequent efforts in digitalization. For example, ANGELAIGN sells its self-developed and produced invisible braces through the "general dentist + intelligent system" model; another example is CYGNUS EQUITY building a one-stop high-value digital platform for doctors, helping medical institutions achieve full-process digital operations while assisting in the growth of doctors through digital products and software/hardware platforms; and another example is Weiyun Artificial Intelligence establishing unmanned smart factories, supply chains, and sales networks to provide industrial solutions for digital dentistry.

From the perspective of the industry, large single products and platformization are two mainstream directions for the development of upstream enterprises.

A "large single product" company refers to a company that owns a certain blockbuster product, while a platform-based enterprise refers to a company with a diversified product line, possessing several absolutely mainstream oral care categories. Through the construction of a digital closed-loop, such an enterprise provides a better experience for its users—both doctors and consumers.

Although accompanied by a huge market demand and the continuous emergence of excellent single-product companies, due to the numerous upstream细分赛道 in dentistry, the actual market space for each product line is limited with a low ceiling. If focusing only on a single product, it is relatively difficult to sustain a great enterprise.

At the same time, a single product line has poor risk resistance. Without extremely strong barriers, companies with a single product often appear very passive when encountering events such as centralized procurement or competitors seizing the market. These events may affect their ability to expand in scale and profitability. For example, the rumored inclusion of implants into medical insurance would significantly impact companies with a single product line, as price reductions would greatly compress profit margins. However, for newly entered domestic brands, this could be an entirely new opportunity.

Currently, among the top ten global dental brands, only Invisalign follows the logic of focusing on a single product.Platformization is becoming the path chosen by an increasing number of upstream dental companies — the advantages of scale and integration brought by a complete set of solutions are becoming more and more obvious.

Platform-based enterprises have significant reuse potential in branding, R&D, and channels, which is conducive to sharing successful product experiences and domestic and international channels, thereby accelerating product development speed and cross-selling (such as sales across different product lines and domestic and international sales). From the perspective of patient experience, the closed-loop of digital treatment also relies on the coordination of multiple product lines. Of course, compared with enterprises focusing on single blockbuster products, platform-based enterprises face greater management challenges and need to pay more attention to controlling the stage and pace of development.

Currently, from the perspective of upstream enterprises in overseas dental healthcare, platform-based companies are also prevalent. Among the top ten dental equipment and consumables companies in 2020, nine were platform-based enterprises, including DENTSPLY SIRONA, Danaher, Straumann, and other well-known companies. Taking DENTSPLY SIRONA as an example, as a global leading supplier of dental equipment and consumables, its product portfolio covers six major areas of dentistry, including X-ray imaging systems, dental treatment units, treatment instruments, CAD/CAM all-ceramic restoration systems, sterilization systems, and consumables required for endodontics, restorative dentistry, dental technology, and implantology. A complete product network has helped the company build a strong brand presence and establish brand momentum. DENTSPLY SIRONA's revenue exceeded $4.2 billion in 2021, with a latest market value of nearly $8 billion.

In summary, the three major trends of domestic substitution, digitalization, and platformization are bringing new opportunities to the upstream dental industry from macro to micro levels. When selecting upstream dental medical enterprises, consideration should also be given to what characteristics will make enterprises stand out under these three trends. Here, the CYGNUS EQUITY team believes that there are three dimensions to be considered when choosing high-quality targets.

1. With independent research and development innovation capabilitiesIn the process of domestic substitution, the first aspect to look at is the speed of a company's R&D, and the second is the depth of its R&D. The speed of R&D determines whether a company can seize the initiative during the domestic substitution process, although channel capabilities cannot be overlooked. The depth of R&D determines whether a company can create products with national or even global competitiveness, which sets the ceiling for the company’s potential over a longer cycle. Both factors together determine the effectiveness and sustainability of a company’s R&D investment.

Secondly, the company's ability to integrate software and hardware.The digitalization trend has imposed new requirements on enterprises: only companies with accumulation in both core products and data can deeply participate in the doctors' diagnosis and treatment process, optimizing overall efficiency, experience, and outcomes.

Third, the platform-based management capability of enterprisesPlatform-based enterprises have clear advantages in terms of market ceiling, risk resistance, and synergy effects. The core focus should be on the product strength of each product line and the company's organizational capabilities, avoiding situations where products become mediocre and management chaotic under multi-front operations.

Focusing on these three dimensions, it becomes relatively easy to discover high-quality targets upstream.

Companies such as ANGELAIGN, Boen Dental, Longvision, and Saire, among others, have seized opportunities in three major trends—or at least one or two of them—and have all performed well.

However, it is important to recognize that for truly innovative companies upstream, the time required for their沉淀往往相对较久,adhering to the essence of medicine. From the perspective of the capital market, innovative enterprises genuinely dedicated to creating world-class products are highly值得关注. In addition to reaping benefits in the process of国产替代, the opportunities for expansion into overseas markets are also worth noting. Strong teams and product capabilities will support Chinese brands in going global.