Spinal Implant National Tender Awards Announced: Weigao Emerges as Top Winner; Which Segments Remain Safe Havens from Volume-Based Procurement?

WEGO ORTHO

Orthopedic Medical Device Manufacturer

WEGO

Medical Device and Pharmaceutical R&D Manufacturer

On September 27, the national centralized bulk procurement of orthopedic spinal consumables was launched. This is the second nationwide orthopedic procurement following the national artificial joint procurement in the field of orthopedics.

The orthopedic market in China is divided into four major categories: spinal consumables, artificial joints, trauma, and sports medicine. National centralized procurement has been completed for artificial joints and spinal products, trauma-related consumables have been covered by the twelve-province alliance procurement, and the suture anchors used in sports medicine have recently been included in Beijing's provincial procurement plan. Orthopedics has become the most comprehensively covered area in centralized procurement.

According to revelations from manufacturers at the spinal procurement site, the spinal sector is WEGO's area of strength. This time, WEGO was again the biggest winner, with 17 Group A wins, one Group B win, and multiple entity wins. In the previous artificial joint procurement, WEGO ORTHO greatly increased its market share of artificial joints post-procurement due to favorable bid prices and a large volume of successful bids.

What impact does this spinal collection have on the orthopedic market? In addition to full orthopedic coverage, the rapidly advancing collection in recent years has completed its coverage of multiple sectors such as vascular intervention, orthopedics, minimally invasive surgery, ophthalmology, low-value consumables, and dentistry. With the collection becoming a major backdrop across the entire medical device industry, what segments within the medical device field remain in the "collection safe harbor"? VCBeat has conducted an analysis.

Spinal Implant Centralized Procurement Called the Most Complex Procurement in History, with Rules Documentation Exceeding 1800 Pages.

This centralized bulk procurement of medical consumables for orthopedic spinal surgery is divided into 14 product system categories, 29 bidding units, and 872 systems based on surgical types, surgical sites, and approach methods. According to the National Healthcare Security Administration, 6,426 medical institutions across China have reported procurement needs reaching 1.2084 million sets, involving 173 bidding companies.

The products in this procurement are used for the treatment of cervical and lumbar diseases, spinal compression fractures, intervertebral disc protrusions, and other conditions, meeting 95% of the needs for spinal surgeries. The market for spinal implant devices included in this procurement accounts for approximately 30% of the entire orthopedic market. From 2015 to 2019, the sales revenue of the spinal implant device market increased from 4.7 billion yuan to 8.7 billion yuan, with a compound annual growth rate of 16.58%.

The price reduction of previous artificial joint centralized procurement exceeded 80%, while the expected price reduction of this spinal centralized procurement is lower than that of artificial joints. The official did not announce the price reduction, but a simple calculation shows that the price reduction of this centralized procurement is about 60%-70%.

Before the centralized procurement, the price of an interbody fusion cage reached 6,000–12,000 yuan. However, in the procurement documents for the anterior cervical screw-plate fixation and fusion system, the highest valid bid was set at 11,360 yuan, while the highest valid bid for the fusion cage was 3,500 yuan. Most of the winning bids were in the range of 4,000–4,500 yuan, with the lowest winning bid being 3,972 yuan from WEGO ORTHO.

The "official guidance price" for the posterior cervical pedicle screw fixation system was 10,000 yuan, with the winning bid prices ranging from 3,690 to 4,000 yuan. The lowest winning bid price was 3,696 yuan from Sanyou Medical, and the highest winning bid price was 4,000 yuan from WEGO.

Many enterprises won the bids in this spine collector procurement, but some small and medium-sized enterprises said that although their companies won the bids at low prices, the overall profit was very thin, making it difficult to continue to survive.

The expected price reduction this time is relatively low, mainly because the rule setting allows enterprises more room for being selected as the winning bid.

In the rule-setting for this spinal collection procurement, companies were first divided into three groups—A, B, and C—based on supply capacity and the intended purchase volume of medical institutions. Companies with large intended purchase volumes from medical institutions entered Group A for bidding, while companies with complete main components but unable to supply across China entered Group B. Additionally, a "revival" rule was introduced: if a valid bidder’s price does not exceed 40% of the highest valid bid price in its product system category, it can obtain provisional winning status. This rule design protects leading enterprises with stronger supply capabilities while also offering more opportunities for smaller businesses to win bids.

Therefore, this spinal collection procurement is hailed as the most moderate procurement, and at the same time, it is also considered the most complex procurement. Compared with artificial joints, the characteristic of spinal implants lies in the diversity of products.

The product system categories alone are divided into 14 types, including anterior cervical screw-plate fixation and fusion systems, posterior cervical screw-rod fixation systems, anterior thoracolumbar screw-rod fixation and fusion systems, posterior thoracolumbar open screw-rod fixation and fusion systems, bone cement for spinal use, and more.

Among many products, which ones are the core products?

The mainstream products of spinal implants are mainly divided into two categories: one is the spinal internal fixation system composed of bone plates, fixation rods, screws, etc., either individually or in combination; the other is the interbody fusion cage.Mainly used to treat three major categories of diseases: degenerative spinal diseases (such as cervical spondylosis, lumbar disc herniation, cervical-lumbar syndrome, chronic low back pain, etc.), spinal trauma and tumors, and spinal deformities.

The entire spine, as the central axial bone of the human body, includes the cervical vertebrae, thoracic vertebrae, lumbar vertebrae, sacral vertebrae, and coccygeal vertebrae. Spinal implants can be divided into posterior cervical internal fixation systems, anterior cervical plate systems, posterior spinal internal fixation systems, interbody fusion cages, minimally invasive posterior spinal internal fixation systems, and vertebral body augmentation systems.

Among numerous products, the posterior spinal internal fixation system using pedicle screws and rods is currently the most widely used internal fixation system in spinal surgery, accounting for approximately 70% of spinal surgeries in China.

With the aging population and changes in lifestyle, the number of people working long hours at desks has increased. In recent years, the prevalence of cervical spondylosis and lumbar disc herniation has been on the rise, with a trend toward younger age of onset. The high prevalence forms a solid foundation for the rapid growth of the spinal implant market.

The complexity of physiological structures determines the complexity of spinal implants, and also sets the difficulty for centralized procurement, which is why spinal implant procurement is called the most complex procurement.

Unlike cardiac stents, the localization rate of orthopedic spinal implants is relatively low, with a significant price gap between domestically produced and imported products. A moderate centralized procurement plan is a boon and protection for domestic companies.

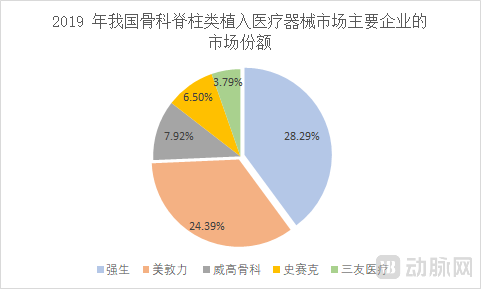

The spinal implant market in China is dominated by imports. In the spinal market, foreign medical device companies represented by Johnson & Johnson, Medtronic, and Stryker account for more than 60% of the domestic market share. The localization of orthopedic spinal implants in China is lower than that of trauma implants but higher than that in the joint implant sector.

According to the prospectus of WEGO ORTHO, Johnson & Johnson, Medtronic, and Stryker respectively account for 28.29%, 24.39%, and 6.50% of the spinal implant market share. Among Chinese manufacturers, WEGO ORTHO holds 7.92% of the market share, while Sanyou Medical holds 3.79% of the market share.

Centralized procurement often accelerates the replacement with domestically produced alternatives. In this spinal centralized procurement, who is the bigger winner, imported or domestically produced products?

A manufacturer at the centralized procurement site said, "In this spinal products procurement, the price cuts for imported products are larger. Among domestic manufacturers, WEGO ORTHO might be the biggest winner."

On the first day of the spinal bidding opening, the closing prices of related orthopedic enterprises in the A-share market rose, with WEGO ORTHO experiencing the highest increase among them.

According to a report by Zhiyan Consulting, the market size of high-value medical consumables in China reached 129.2 billion yuan in 2019. Of this, orthopedic implant consumables accounted for 34.5 billion yuan; vascular intervention consumables for 46.1 billion yuan; neurosurgical consumables for 4.2 billion yuan; ophthalmic consumables for 9 billion yuan; dental consumables for 8.5 billion yuan; blood purification consumables for 8.2 billion yuan; non-vascular intervention consumables for 4.8 billion yuan; electrophysiology and pacemakers for 8.5 billion yuan; and others for 5.2 billion yuan. The vascular intervention and orthopedic implant markets are the largest segments in China's high-value medical consumables sector, accounting for 35.74% and 26.74%, respectively. Vascular intervention, dental, and blood purification sectors have shown the highest growth rates, exceeding 20%.

In the main细分 markets mentioned above, most have already been covered by centralized procurement. Centralized procurement will inevitably reduce product gross margins, increase industry concentration, and trigger a major reshuffle in the industry. Previous centralized procurements for coronary stents and artificial joints have also shown that not all winners of bids are truly winners—low-price bidding can easily lead to losses in both volume and price.

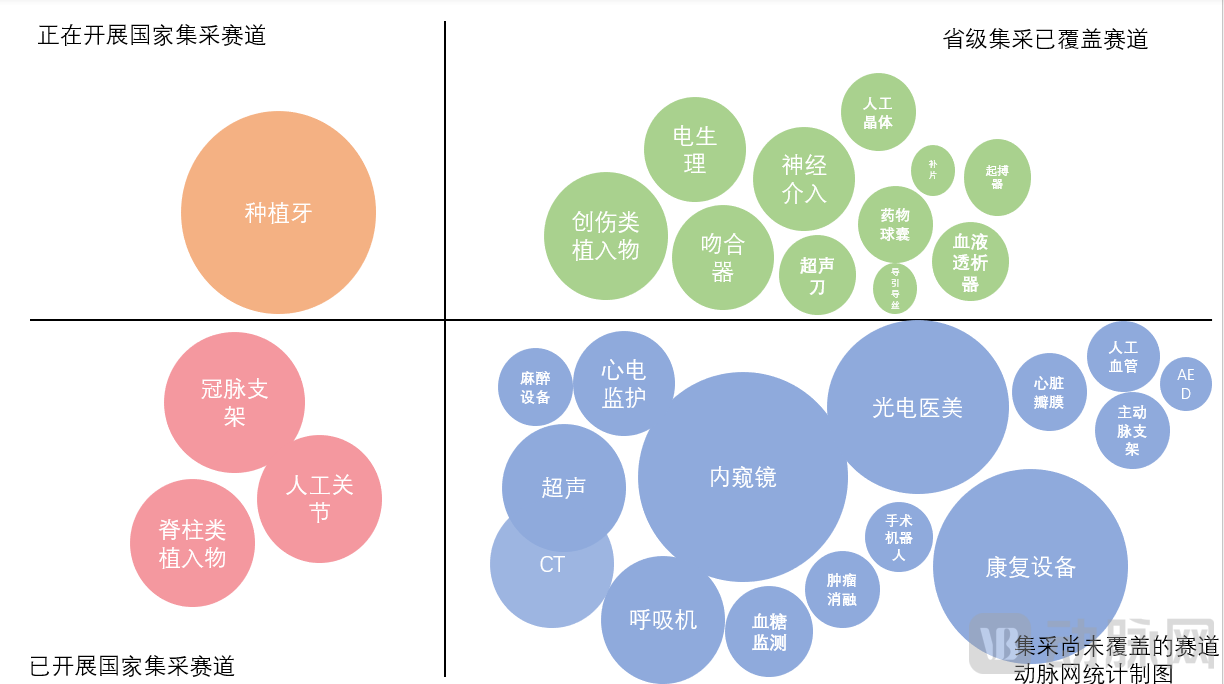

Under the new era background, what tracks have not been covered by centralized procurement? What kind of tracks can withstand the impact of centralized procurement?

From the existing statistics of bulk procurement, the market size of the tracks focused on by national-level procurement is close to 10 billion yuan. These tracks are clinically mature, have large clinical usage, individual product prices exceed ten thousand yuan, and involve many domestic participants. The market size of the细分 tracks focused on by provincial-level procurement is 5 billion yuan or less. Provincial-level procurement covers more tracks with a broader scope, including both low-value and high-value consumables.

From the distribution of major high-value medical device centralized procurement, the field most preferred for procurement currently is high-value consumables. Among high-value consumables, the vascular intervention and orthopedic fields are the most extensively procured, followed by the minimally invasive surgery field.

There are also sectors with similarly high prices, mature clinical techniques, and a large number of domestically produced products that have not been included in centralized procurement. In the overall medical device landscape, there are still many sectors that have not been subject to centralized procurement. These sectors can mainly be divided into two categories.

One category is high-value consumables with relatively low surgical volume. Take aortic stents, for example: the market price of aortic stents is relatively high, with domestically produced stents costing around 20,000 yuan and imported stents around 30,000 yuan.

However, the number of aortic stent surgeries in China is not very high. In 2017, the number of endovascular aortic stent surgeries in China was 25,621. According to the "2021 White Paper on Cardiovascular Surgery and Extracorporeal Circulation Data in China," there were 37,179 major vascular surgeries, an increase of 7,370 cases (24.7%) compared to 2020. Major vascular surgeries accounted for 13.4% of total heart surgeries, the same proportion as in 2020. The number of major vascular surgeries has shown a rapid growth trend for many consecutive years. Not all surgeries involve endovascular aortic stents; in 2017, the number of endovascular aortic stent surgeries in China was 25,621, which is less than 30,000.

At the same time, there are not many domestically-produced enterprises in this field. The main participant, Endovastec™, has shown relatively rapid growth in China. In Endovastec™'s 2022 semi-annual report, the Castor® Branched Aortic Stent Graft and Delivery System has been on the market for over five years, with more than 12,000 cumulative implantations. In the first half of 2022, it achieved sales revenue of 183 million yuan, representing a year-on-year increase of 37.82%. The Minos® Abdominal Aortic Stent Graft and Delivery System achieved sales revenue of 75 million yuan during the reporting period, marking a year-on-year increase of 78.95%.

The second category is medical devices. Since the annual procurement volume for devices is unclear, it is impossible to achieve price reductions through bulk purchasing. Therefore, device products have always been in a safe harbor from centralized procurement.

Taking endoscopes as an example, due to their high technical threshold, large-scale centralized procurement has not yet been carried out. Endoscopes have always been in a safe harbor from centralized procurement, and listed companies in the endoscope field, such as HAITAI New Light and AOHUA Endoscopy, have not been affected by centralized procurement.

In the endoscope sector, Chinese manufacturers are not at an advantage and lack competitiveness. In the rigid endoscope market, global players such as Karl Storz, Stryker, and Olympus dominate. In the flexible endoscope market, Olympus, Fujifilm, and Pentax almost occupy all of the market share. Without the pressure of centralized procurement, domestic endoscope companies can still enjoy a prolonged period of rapid revenue growth. In the first half of 2022, HAITAI New Sight achieved operating revenue of 190 million yuan, representing a year-on-year increase of 44.74%; net profit attributable to shareholders of the listed company was 79.8694 million yuan, up 35.80% from the same period last year.

The external environment is constantly changing, and future centralized procurement will continue. What kind of companies can resist the risks of centralized procurement and perform more calmly before it?

First is the ability to master底层技术. Mastering core底层技术, differentiated innovation enables enterprises to avoid homogeneous competition and possess stronger cost control capabilities before集采. Innovation is the deepest moat for enterprises.In the entire high-value consumables and medical device industry chain, core raw materials and components in multiple细分fields still rely on a single overseas supplier, indicating that domestic companies still have significant room for improvement.

Taking orthopedic materials as an example, there are still no qualified domestic suppliers for medical ceramics, PEEK, cobalt-chromium-molybdenum, ultra-high molecular weight polyethylene, and other materials. PEEK, a core raw material used in spinal products, is almost exclusively sourced by several major domestic companies from a single British company.

Previously, the National Healthcare Security Administration clearly stated in its response to Proposal No. 4955 of the Fifth Session of the 13th National People's Congress that innovative medical devices will not be included in centralized procurement.

It was mentioned that during the centralized bulk procurement process, medical institutions determine the procurement volume based on historical usage, combined with clinical application and advancements in medical technology. Due to the immature clinical application of innovative medical devices and the temporary difficulty in estimating their usage, it is still challenging to implement a bulk procurement approach. During the centralized bulk procurement process, the National Healthcare Security Administration will reasonably determine the bulk procurement ratio based on factors such as clinical application characteristics, market competition landscape, and the number of selected enterprises, leaving some market space outside the centralized bulk procurement for innovative products to expand their market.

The National Healthcare Security Administration (NHSA) has clarified that innovative medical devices will not be included in bulk procurement. Previously, the standard for innovative medical devices defined in the medical device approval process was that they must have a Chinese invention patent, be domestically首创in China, internationally领先, and possess significant clinical application value.

The standard for innovative devices defined by the National Healthcare Security Administration (NHSA) includes those with immature usage volume. This indicates that the NHSA prioritizes truly original devices rather than imitations of existing, mature imported products, further highlighting the competitiveness of original innovation.

Secondly, the diversification of product lines, with the ability to provide comprehensive solutions.Whether in vascular intervention, orthopedics, or minimally invasive surgery, each细分领域contains multiple single products. Focusing on large-volume products and markets is one approach, but an overall solution enables companies to mitigate the impact of centralized procurement.

Challenges in centralized procurement also breed opportunities. When the storm comes, there will always be ships that fall behind in the outgoing fleet, but those that adapt to the times can navigate through the storm and welcome the sunshine after the rain.