Tetanus vaccine leader Olymvax files for HK listing on 35% growth, with an eye on superbug pipeline

olymvax

Human Vaccine Research and Development Manufacturer

On November 25, Chengdu Olymvax Biopharmaceuticals Inc. (Stock Code: 688319, hereinafter referred to as "Olymvax") disclosed that it has submitted an application for the listing and issuance of H shares on the HKEX. This move signifies that Olymvax is transitioning from a single A-share platform to a dual-listed "A+H" structure.

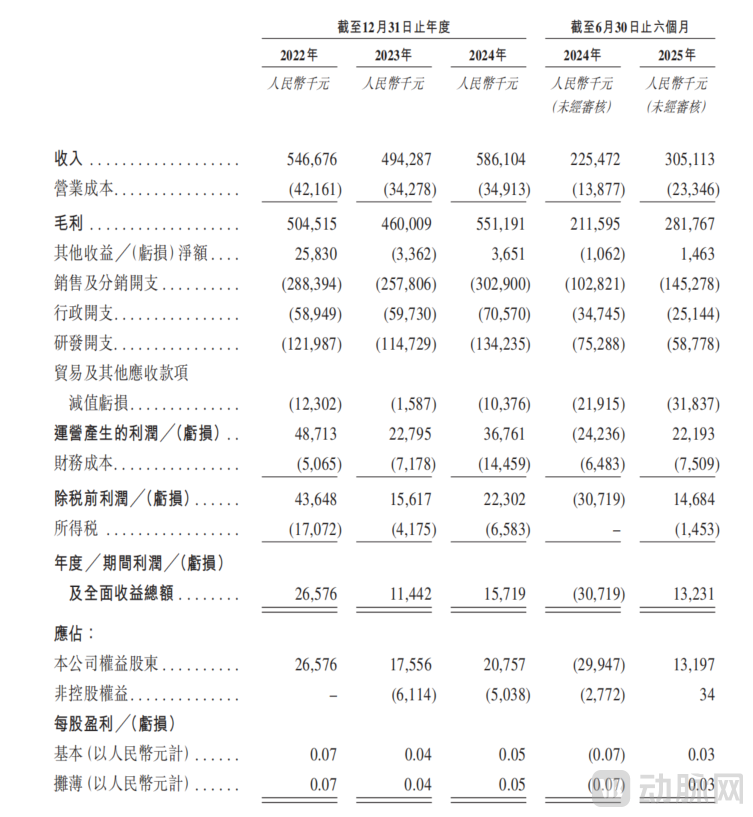

Olymvax has been listed on the A-share market for four years. When it went public on the Science and Technology Innovation Board (STAR Market) in 2021, it was one of the few vaccine companies to achieve profitability in its first listing year. By 2025, Olymvax's fundamentals showed further improvement. Specifically, for the fiscal years ending 2022, 2023, and 2024, Olymvax reported revenues of RMB 546.7 million, RMB 494.3 million, and RMB 586.1 million, respectively. In the first half of 2025, driven by the continued sales expansion of its Tetanus Vaccine, Adsorbed, Olymvax achieved revenue of RMB 305 million, representing a year-on-year increase of approximately 35%. It also reported net profit attributable to the parent company's shareholders of RMB 13.1969 million, marking a return to profitability. After an adjustment in 2023, the Company's revenue scale has resumed its growth trajectory. The significant year-on-year growth rate in the first half of 2025 clearly indicates a business recovery, providing the practical conditions necessary for accessing international capital markets.

Figure 1. Olymvax Consolidated Income and Other Comprehensive Income Statement for 2022-2025 (First Half)

Tetanus Vaccine Builds a Solid Foundation, Superbug Vaccine Anchors New Growth Direction

Olymvax Biopharmaceuticals' product journey did not begin with a high-profile pipeline but rather started with a tetanus vaccine—a product of critical clinical necessity that had long been overlooked.

When Olymvax was founded in 2009, China's tetanus prevention market had long been dominated by passive immunization due to the high volume and low cost of passive immune preparations, coupled with the absence of regulatory mandates specifying preventive methods. As a result, vaccine usage was significantly lower than that of passive preparations. Instead of following the trend toward passive formulations, Olymvax targeted the more technologically demanding but steadily demanded tetanus vaccine, adsorbed segment. After eight years of technological development, the company successfully commercialized the Tetanus Vaccine, Adsorbed in 2017, becoming China's first privately owned enterprise to achieve this milestone.

Compared to traditional passive immune preparations such as tetanus antitoxin, the Tetanus Vaccine, Adsorbed offers longer-lasting protection through active immunization and avoids the allergic risks associated with heterologous antitoxins. With the gradual refinement of its production system, the product's batch release volume has consistently ranked among the industry's highest for several consecutive years, contributing approximately 80% of Olymvax's revenue. This foundational product has provided the company with the capability to sustain investment in innovative vaccine R&D and has become a critical asset as it advances to the next stage of capital market development.

Beyond traditional vaccines, Olymvax is accelerating the diversification of its product portfolio. The company has already commercialized the Hib conjugate vaccine and the AC Meningococcal–Hib conjugate vaccine, covering common infection-related indications in infants and young children.

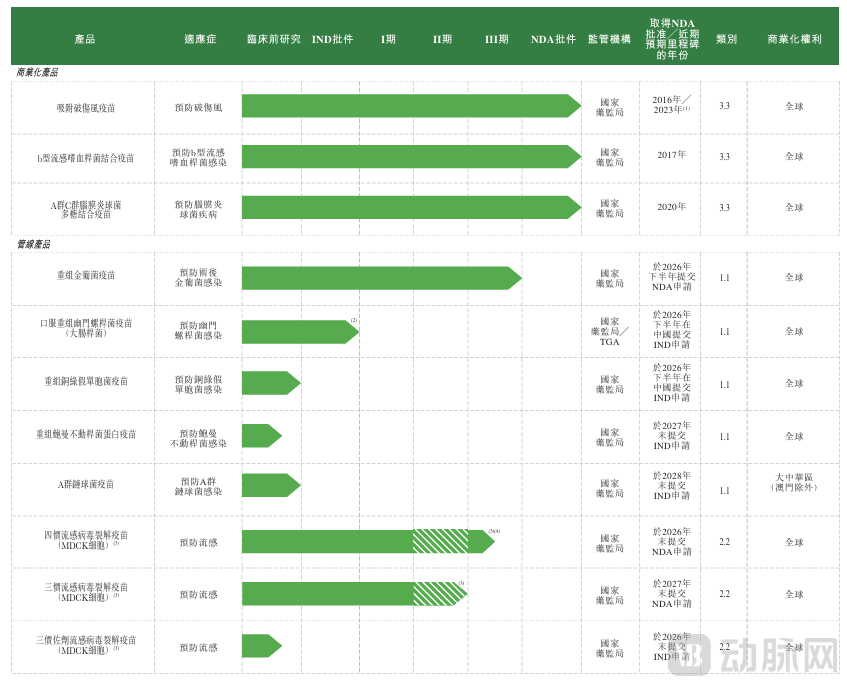

However, Olymvax's strategic direction is better reflected in its two main R&D focuses: the transition in viral vaccine technology and the pursuit of vaccines targeting superbugs.

In the field of viral vaccines, Olymvax has adopted the MDCK cell suspension system to develop trivalent and quadrivalent influenza split vaccines. In early 2025, both vaccines simultaneously entered Phase I clinical trials, with the first group of subjects quickly enrolled. Following the completion of its Phase I trial, the quadrivalent influenza vaccine advanced directly to Phase III clinical trials in October 2025. The trivalent influenza vaccine has completed its interim Phase I trial report and is currently in the Chinese safety follow-up stage.

Compared to China's mainstream chicken embryo cultivation technology, the MDCK system is more suitable for industrial-scale production via bioreactors, enabling shorter production cycles and reduced supply chain dependency. This direction has become one of the global trends in influenza vaccine innovation in recent years.

In the superbug arena, Olymvax has demonstrated notable commitment. Its recombinant Staphylococcus aureus vaccine, developed in collaboration with the Army Medical University, completed enrollment of all subjects in 2025 and has entered the follow-up stage. Among similar projects in China, this pipeline is progressing at a leading pace. Additionally, Olymvax is developing recombinant vaccines targeting pathogens such as Pseudomonas aeruginosa, Helicobacter pylori, and Acinetobacter baumannii. These represent key resistant bacterial targets for which effective vaccines are still lacking globally, underscoring clear clinical demand.

From traditional tetanus vaccines to the technological shift in influenza vaccines, and further to clinical leadership in the field of antimicrobial resistance, this pipeline structure indicates that Olymvax is transitioning from a foundational vaccine enterprise to an innovation-driven company, seeking to establish differentiated competitiveness in globally unresolved areas of severe infection.

Figure2. Olymvax Pipeline Status

International Layout Becomes Key to Breakthrough

The vaccine industry is experiencing a subtle inflection point: demand continues to expand steadily, while supply-side competition intensifies, and research and development phases are becoming longer, more costly, and more challenging. For enterprises relying on innovation as their second growth curve, internationalization is no longer merely an option but increasingly a strategic imperative that must be planned in advance in the coming years.

From the demand perspective, growth remains persistent. According to a research report by Metatech Insights, the global vaccine market (excluding COVID-19 vaccines) is projected to exhibit robust growth, expanding from USD 80.2 billion in 2024 to USD 155.4 billion by 2035, with a compound annual growth rate (CAGR) of 6.2% during this period. The Chinese market also demonstrates growth potential, with data from a Grand View Research report indicating that China's vaccine market size is expected to increase from USD 4.11 billion in 2024 to USD 8.282 billion by 2033, achieving a CAGR of 7.9%. In this context, privately funded vaccines, adult vaccines, multivalent combination vaccines, and innovative vaccines are the primary drivers of growth, shifting the industry's focus from increasing vaccination rates toward upgrading the product portfolio structure.

On the other hand, industry competition has significantly intensified. Traditional vaccine categories have long faced overcapacity, while provincial centralized procurement initiatives have driven substantial price reductions, with some products experiencing price drops exceeding 50%, thereby compressing corporate profit margins. In the innovation arena, the concentration of enterprises in popular vaccine categories (such as HPV, influenza, and COVID-19) is leading to homogenized competition. The segments most likely to penetrate this competitive landscape are typically those involving innovative vaccines with scarce targets, high technological barriers, and clear clinical value.

In the first half of 2025, Olymvax invested RMB 58.77 million in R&D, accounting for approximately 19% of its revenue. For a medium-sized company whose product portfolio is primarily composed of traditional vaccines, the capital pressure associated with innovative R&D has reached an upper limit at this stage. Compared to the annual R&D expenditures of pharmaceutical giants such as MSD and Pfizer, which amount to tens of billions of USD, Chinese companies generally face structural challenges characterized by lengthy pipelines and constrained resources.

Against this backdrop, the expansion of capital platforms becomes crucial. For Olymvax, an H-share listing is not only about accessing a more substantial funding pool but also encompasses enhanced international visibility, more direct pathways for global collaboration, and a regulatory environment more conducive to export registrations.

However, certain risks warrant attention. As indicated in its prospectus, Olymvax acknowledges potential challenges: the increasing penetration of multivalent vaccines may further squeeze the market for single-antigen products such as the Hib standalone vaccine. Additionally, although the company's Staphylococcus aureus vaccine is among the frontrunners in its segment, all innovative vaccines inevitably face multiple variables, including clinical uncertainties, varying regulatory requirements, cost pressures, and post-marketing education efforts. Adjustments to national immunization programs or changes in procurement policies may also impact the profitability of traditional vaccine products.

From an industry-wide perspective, Olymvax's pursuit of an H-share listing reflects a broader trend: traditional vaccines are approaching growth ceilings, innovative vaccines face elevated risks, capital platforms are evolving in scope, and the global burden of infectious diseases is diversifying. The entire industry is transitioning from a phase of "competing on scale" to one of "competing on innovation and execution."

In the coming years, as influenza vaccine production processes evolve, the burden of superbugs intensifies, multivalent vaccines become more widespread, and immunization programs potentially expand, the competitive landscape for vaccine companies is bound to be reshaped. In this process, companies capable of maintaining stability in traditional product categories while continuing to invest in innovation and demonstrating internationalization capabilities will be better positioned to chart a new trajectory of growth.