Bao Pharma passes HKEX hearing at RMB 4.87B valuation, with subcutaneous delivery as key tech

On November 26, Shanghai Bao Pharmaceuticals Co., Ltd. (referred to as "Bao Pharma") successfully passed the main board hearing of the HKEX. CITIC Securities and Guotai Haitong acted as joint sponsors, marking another significant development in the capital markets for China's synthetic biopharmaceutical sector.

Founded in 2019, Bao Pharma did not follow the conventional path of "first building a technology platform, then finding application directions." Instead, it started by addressing structural issues on the clinical side. The team's long-term involvement in the production and application of biochemical preparations allowed Bao Pharma to initially target a category of drugs that are highly sensitive to regulation, supply, and quality stability—traditional bio-extract drugs derived from animal organs, blood, or urine. These products are critical in areas such as assisted reproductive technology, critical care medicine, and autoimmune diseases but have long faced structural limitations such as batch variability, viral contamination, and supply chain volatility.

Over the past few years, Bao Pharma began with lyophilized powder injection technology and gradually developed formulation innovation capabilities centered on large-volume subcutaneous drug delivery. Simultaneously, it has established a systematic product portfolio in areas such as autoimmune diseases, assisted reproductive technology, and recombinant biologics, thereby clarifying its business boundaries.

Subcutaneous Delivery: A Trend Creating Differentiation

In recent years, subcutaneous drug delivery has evolved from localized exploration into an industry-wide trend.

In 2018, over a dozen multinational pharmaceutical companies jointly established the SC Drug Development & Delivery Consortium, which has since continuously promoted the technical standards and research advancements in this field. This trend is driven by higher clinical expectations for "safety, convenience, and long-term repeatability." As a core enabling technology, subcutaneous injection significantly reduces administration time and improves the patient experience.

Globally, industry leader Halozyme (market cap: $8.4 billion), leveraging its hyaluronidase technology, has successfully enabled multiple blockbuster drugs, including J&J's CD38 antibody and Roche's HER2/PD-L1 antibody. The transition is particularly rapid in oncology: the subcutaneous version of MSD's Keytruda has submitted a marketing application in China, and Daiichi Sankyo's DS-8201 has initiated a Phase I clinical trial for its subcutaneous formulation. Both utilize hyaluronidase technology from the Korean company Alteogen.

The shift from traditional IV (intravenous injection) to SC (subcutaneous injection) fundamentally represents a transition from hospital-based to self-administrable settings, with hyaluronidase serving as the key technological enabler. Bao Pharma's entry point in this area is its recombinant human hyaluronidase, KJ017.

Regarding the replacement of traditional biochemical drugs, Bao Pharma is further targeting longstanding industrial challenges that have remained unresolved for years. Whether it's chymotrypsin or ulinastatin, their raw material sources are constrained by extraction from animal tissues or bodily fluids, making it difficult to fully eliminate batch variability and viral contamination risks. Through precise chassis cell engineering, Bao Pharma has achieved stable recombinant expression of complex proteins. Products like KJ101 and BJ044 have already entered clinical development pathways. The core value of this strategy lies not in developing entirely new drugs, but in solving persistent industrial bottlenecks—upgrading historically supply-unreliable product categories into recombinant formulations that are scalable and standardized.

Supporting the advancement of this pipeline is the three-core technology foundation established by Bao Pharma: a drug design platform, a chassis cell platform, and a biomanufacturing platform. Building on this foundation, Bao Pharma utilizes AI to empower sequence optimization and structural design. Combined with bioinformatics techniques, it has successfully reconstructed the urate oxidase sequence lost during human evolution, developing recombinant drug candidates with low immunogenicity and suitability for repeated administration. This provides a potential new treatment pathway for patients with severe gout.

This differentiated capability has also attracted industry collaborations. Bao Pharma has already partnered with companies such as Sumgen Biotech and Qyuns Therapeutics in the area of subcutaneous antibody drug delivery. As of September 30, 2025, Bao Pharma employs 251 R&D personnel, accounting for 72.1% of its total staff. Its CMC (Chemistry, Manufacturing, and Controls) team comprises over 30% of the workforce, establishing a dual-driven business model of "proprietary products + technology services."

Gradient Pipeline Targets 50 Billion Market Space

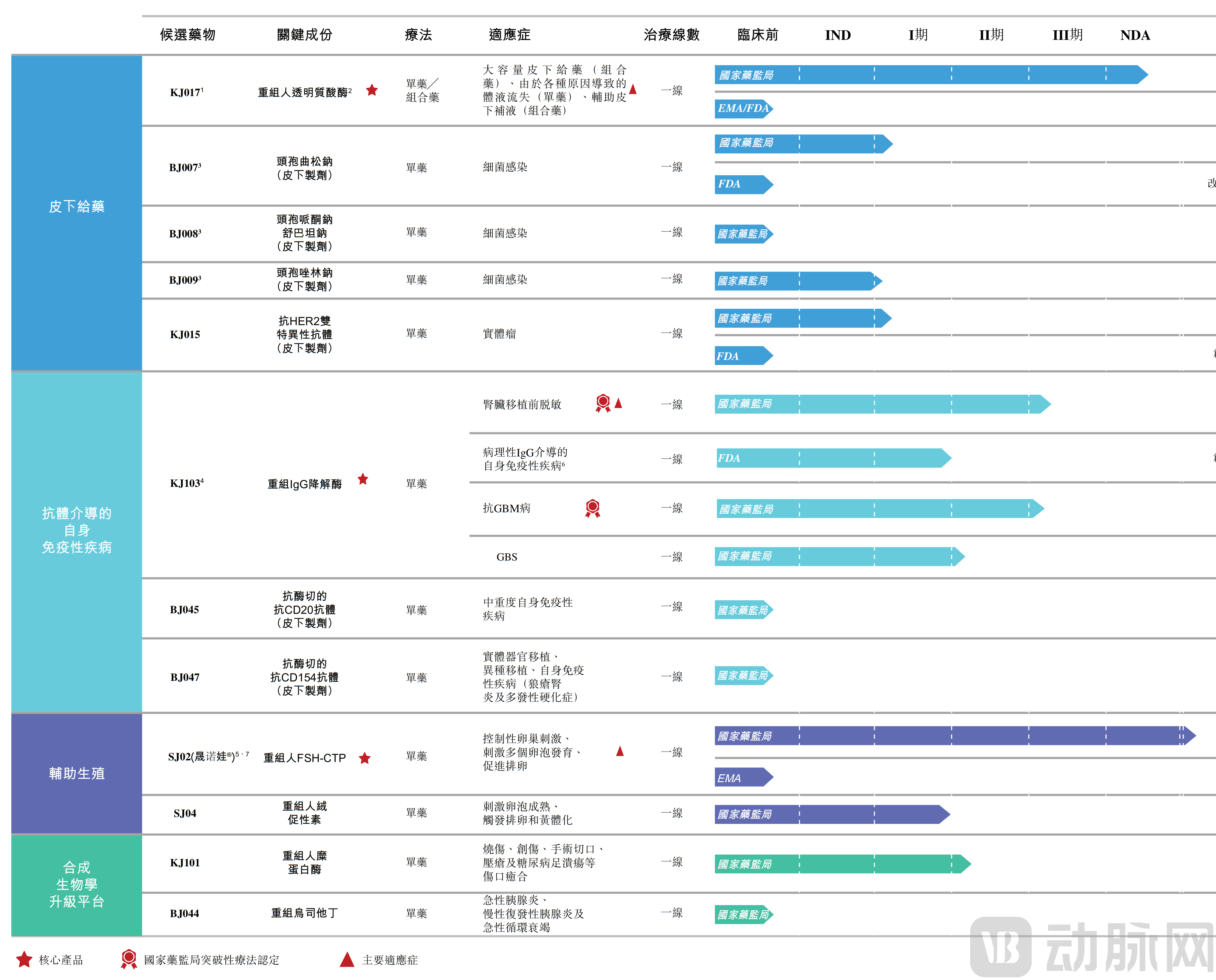

Bao Pharma currently has a total of 12 self-developed drug candidates in its pipeline, among which three core products are in late-stage clinical development or at the New Drug Application (NDA) stage. The markets targeted by these products demonstrate clear size and growth potential, rather than being unproven future-oriented categories. Spanning four major therapeutic areas, the pipeline exhibits a classic tiered structure: late-stage products nearing commercialization, mid-stage candidates accelerating clinical advancement, and early-stage projects serving as innovation reserves.

Bao Pharmaceuticals' R&D Pipeline Status

Behind this portfolio lies an addressable market exceeding RMB 50 billion. According to Frost & Sullivan, the Chinese market size for the four major fields—high-volume subcutaneous drug delivery, autoimmune diseases, assisted reproductive technology (ART), and recombinant biologics—is projected to reach approximately RMB 7 billion, RMB 26.7 billion, RMB 14.9 billion, and RMB 5.3 billion, respectively, by 2033.

1SJ02: The First Marketed Product Entering the Assisted Reproductive Technology Field

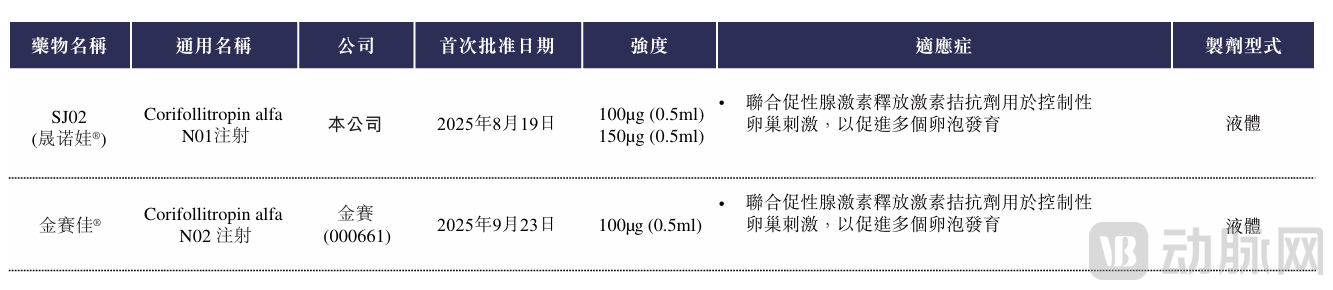

Currently, the most advanced candidate in the pipeline is SJ02, a long-acting recombinant FSH-CTP protein used for Controlled Ovarian Stimulation (COS). The core concept involves extending its duration of action through fusion with a stabilizing peptide, enabling combined use with GnRH antagonists to reduce dosing frequency and improve follicular synchrony. In August 2025, SJ02 received New Drug Application (NDA) approval from China's National Medical Products Administration (NMPA), marking it as Bao Pharma' first marketed product. Presently, only two long-acting FSH-CTP products are approved in the Chinese market, and SJ02 is one of them.

Product Information of China's Long-Acting FSH-CTP Launch

2KJ017: Key Pathway Enzyme for Subcutaneous Injection

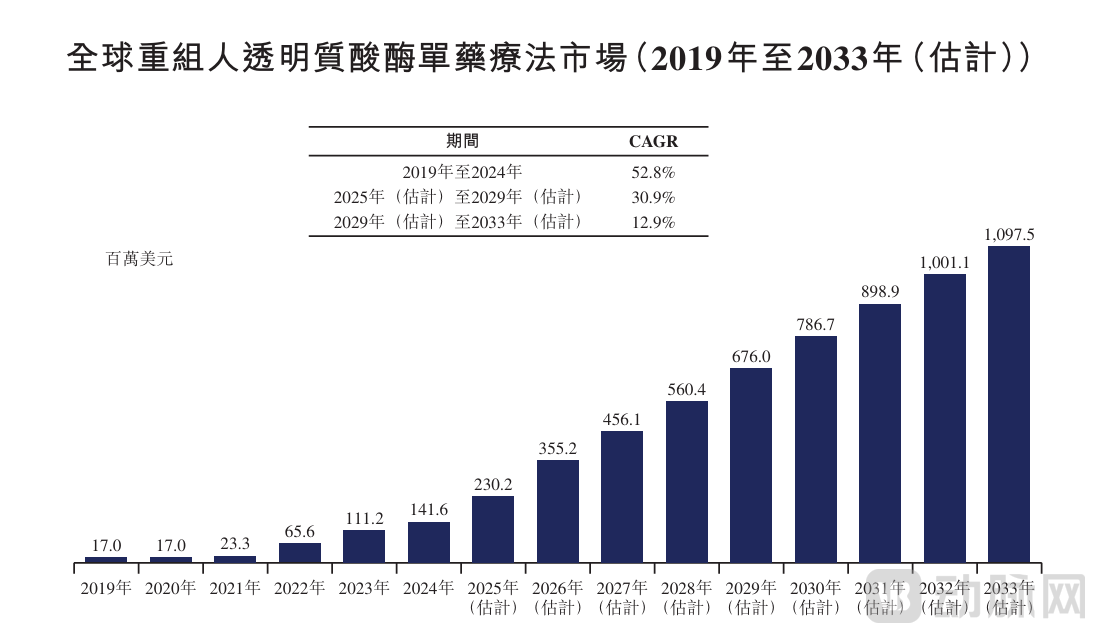

KJ017, a highly glycosylated enzyme, facilitates the localized degradation of subcutaneous hyaluronic acid (HA), reducing tissue resistance. This enables the conversion of various traditional intravenous therapies into formulations suitable for rapid, high-volume subcutaneous administration. This approach not only enhances medication safety and patient convenience but also lays the foundation for optimizing clinical efficacy. Amid the global shift of biologics toward subcutaneous formulations, the market segment for KJ017 is well-defined and experiencing rapid growth. According to Frost & Sullivan, the global recombinant human hyaluronidase market is projected to grow from USD 799 million in 2024 to USD 9.094 billion by 2033, while the Chinese market is expected to expand from RMB 186 million to RMB 6.98 billion during the same period.

Global Recombinant Human Hyaluronidase Monotherapy Market Size (2019-2033)

From a practical application perspective, the strategic entry point for KJ017 lies not only in accelerating drug absorption but also in assisting pharmaceutical companies in reformulating dosage forms. This enables therapies to transition from hospital-based intravenous administration settings to outpatient or even self-administration scenarios, aligning with the global trend of Lifecycle Management (LCM) for biologic drugs.

3KJ103: Overcoming Immune Barriers in Kidney Transplantation

As a globally leading low-immunogenicity IgG-degrading enzyme, KJ103 possesses significant competitive advantages and clear market value within its therapeutic class. According to the latest disclosures, aside from Idefirix (which is already marketed in Europe), only four IgG-degrading enzymes worldwide have entered clinical development. Among these, KJ103's progress is at the forefront—it has reached Phase III for the kidney transplant rejection indication and Phase II for anti-glomerular basement membrane (anti-GBM) disease. In April 2025, it additionally received IND approval for Guillain-Barre syndrome (GBS). Notably, no other drug targeting the same mechanism has been approved or entered clinical trials in China.

Global IgG Degradation Enzyme Pipeline Status

Compared to traditional products, KJ103 offers advantages such as reducing pre-existing anti-drug antibody (ADA) titers, minimizing adverse reactions, extending enzymatic activity duration, and suitability for immunocompromised and other special populations. It also demonstrates potential in gene therapy by lowering viral neutralizing antibodies. From a demand perspective, there are approximately 4.9 to 7.1 million end-stage renal disease patients worldwide awaiting kidney transplantation. Among them, about 40% face challenges such as difficult donor matching and high rejection risks due to anti-HLA antibody sensitization. KJ103 can effectively reduce levels of these antibodies, offering transplantation possibilities for highly sensitized patients unresponsive to traditional desensitization therapies, thereby addressing a clear market gap.

Beyond its three core products, Bao Pharma has also developed several candidates in the recombinant substitution field, including KJ101 (recombinant chymotrypsin) and BJ044 (recombinant ulinastatin). Both target traditional drug markets reliant on extraction from animal organs or urine—categories long plagued by unstable sourcing, impurity risks, and batch variability. As biopharmaceutical regulations tighten, recombinant substitution products are widely regarded as the next wave of replacement opportunities in the industry.

Notably, Bao Pharma's pipeline demonstrates significant synergy. Its subcutaneous injection platform can serve multiple product categories for formulation upgrades, its recombinant substitution technology can be reapplied across critical care therapeutic lines, and its autoimmune disease focus has expanded to include assets targeting anti-degradation antibodies and IgM-degrading enzymes. This "platform reuse + indication synergy" structure transforms the pipeline from single-track advancement into a modular, scalable system while reducing uncertainties in R&D cost structures.

Commercialization Capability Remains to Be Market-Validated

Financially, Bao Pharma remains in a typical "high R&D investment, low revenue" phase, but its financing pace has not slowed down. To date, Bao Pharma has completed six funding rounds, raising a cumulative total exceeding RMB 1.5 billion. Its post-money valuation reached RMB 4.871 billion after the Series C and C+ rounds. Investors include Farglory Real Estate, Prudence Financial Group, Oriental Fortune Capital, Findowin Capital, Haitong Innovation Securities, and Grandway Capital. The significant capital infusion despite continuous losses essentially reflects investors' confidence in its technological barriers and pipeline execution capability.

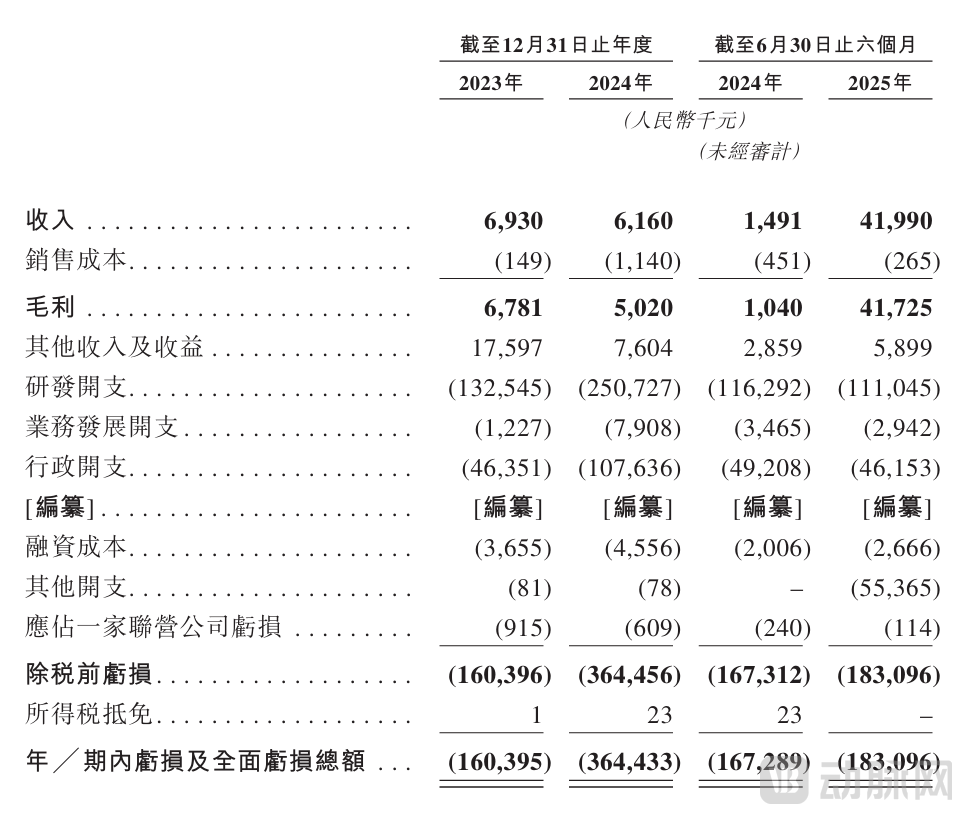

In terms of expense structure, Bao Pharma's "burn rate" is primarily concentrated on R&D. From 2023 to the first half of 2025, R&D expenses were RMB 133 million, RMB 251 million, and RMB 111 million, respectively. Over 30% of these expenditures were allocated to the Phase II clinical trial of KJ103, the NDA submission for KJ017, and process optimization. This R&D-driven model has contributed to widening net losses: net losses for 2023, 2024, and the first half of 2025 were RMB 160 million, RMB 364 million, and RMB 183 million, respectively. However, as of June 2025, Bao Pharma still held RMB 453 million in cash, providing a sufficient buffer for its core pipeline's push toward commercialization.

Bao Pharma 2023-2025 (First Half) Consolidated Income Statement and Other Comprehensive Income

On the revenue side, a transition is underway from a model led by technology licensing to one driven by product sales. Over the past three years, Bao Pharma's revenue remained stable within the RMB 4–7 million range, primarily derived from technology licensing and collaborative development. However, with the approval of SJ02, a substantive shift in the revenue structure is anticipated. In the first half of 2025, Bao Pharma's operating revenue increased to RMB 41.99 million, a year-on-year growth of 2716%, with over 95% attributed to upfront payments from licensing and commercialization agreements.

Notably, Bao Pharma has adopted a "light-asset + specialized outsourcing" strategy in building its commercial system. In July 2025, Bao Pharma signed an exclusive sales agency agreement with Anke Biotechnology (SZSE: 300009), appointing the latter as the exclusive Commercial Sales Organization (CSO) for the Greater China region (including Mainland China, Hong Kong, Macau, and Taiwan), responsible for the market promotion of SJ02. This model leverages Anke's deep channel presence in the field of assisted reproductive technology while allowing Bao Pharma to maintain a relatively lean organizational structure, directing more resources towards advancing its core pipeline.

Yet, the real test lies precisely in commercialization execution.

Firstly, the assisted reproductive market is highly specialized and characterized by brand loyalty, with companies like Livzon Pharmaceutical and Changchun High-tech Industries long dominating the landscape. While SJ02's "long-acting advantage" serves as a market entry point, its actual sales trajectory and peak potential will be determined by strategies for national reimbursement drug list (NRDL) negotiation, clinician education, and channel penetration rates.

Secondly, KJ103 belongs to the category of mechanism-innovative drugs, posing a significantly greater challenge for market education compared to traditional immunosuppressants. Its concept of "directly degrading pathogenic IgG" is quite disruptive, necessitating extensive physician training and support from real-world evidence, which could further extend its commercialization timeline.

In summary, the key variable for Bao Pharma is shifting from R&D efficiency to commercial execution. While the company holds a first-mover foundation and clear product positioning in areas such as assisted reproductive technology, high-volume subcutaneous delivery, and autoimmune diseases, market competition remains intense. Factors such as reimbursement policies, clinical education, and channel penetration will all shape the growth trajectory in the coming years.

From an industry perspective, Bao Pharma represents not merely a synthetic biology concept stock but a more pragmatic direction: replacing traditional biochemical products with engineering approaches, advancing product development around well-defined clinical needs, and enhancing commercial certainty through multi-product synergies. Whether this model succeeds is not only crucial for the company's own growth potential but also warrants long-term observation and reference for the broader synthetic biopharmaceutical sector.