Thirty Years of U.S. Biotech: Lessons from Four Market Cycles

Genentech

Pharmaceutical R&D Manufacturer

In 2022, everyone was talking about "cycles" and the "investment window" in the biotechnology field.

"The 'window' can be opened, which means it will also close at some point."

If we evaluate the performance record of the biotech sector in the U.S. stock market, we will find that the "window" has opened and closed many times. Investment windows in the biotechnology field often last 6 to 9 months. The frequency of its value cycles is also higher than expected. Even considering only the major cycles, starting from 1992, Biotech in the U.S. stock market has already experienced four distinct upward and downward cycles over the past 30 years.

These value cycles remain an excellent guide to understanding human behavior, as always.

Reviewing the historical ups and downs helps to understand the thoughts and actions of biotech investors today. Although past experiences may not accurately tell us when the market might face a major shift,It cannot tell us when the cold winter will end or when the bubble will burst, but it can certainly guide more rational behavior.

1992 was a critical turning point, widely regarded as the end of the golden decade for U.S. biotech stocks and the conclusion of the first upcycle in the American biotechnology industry.

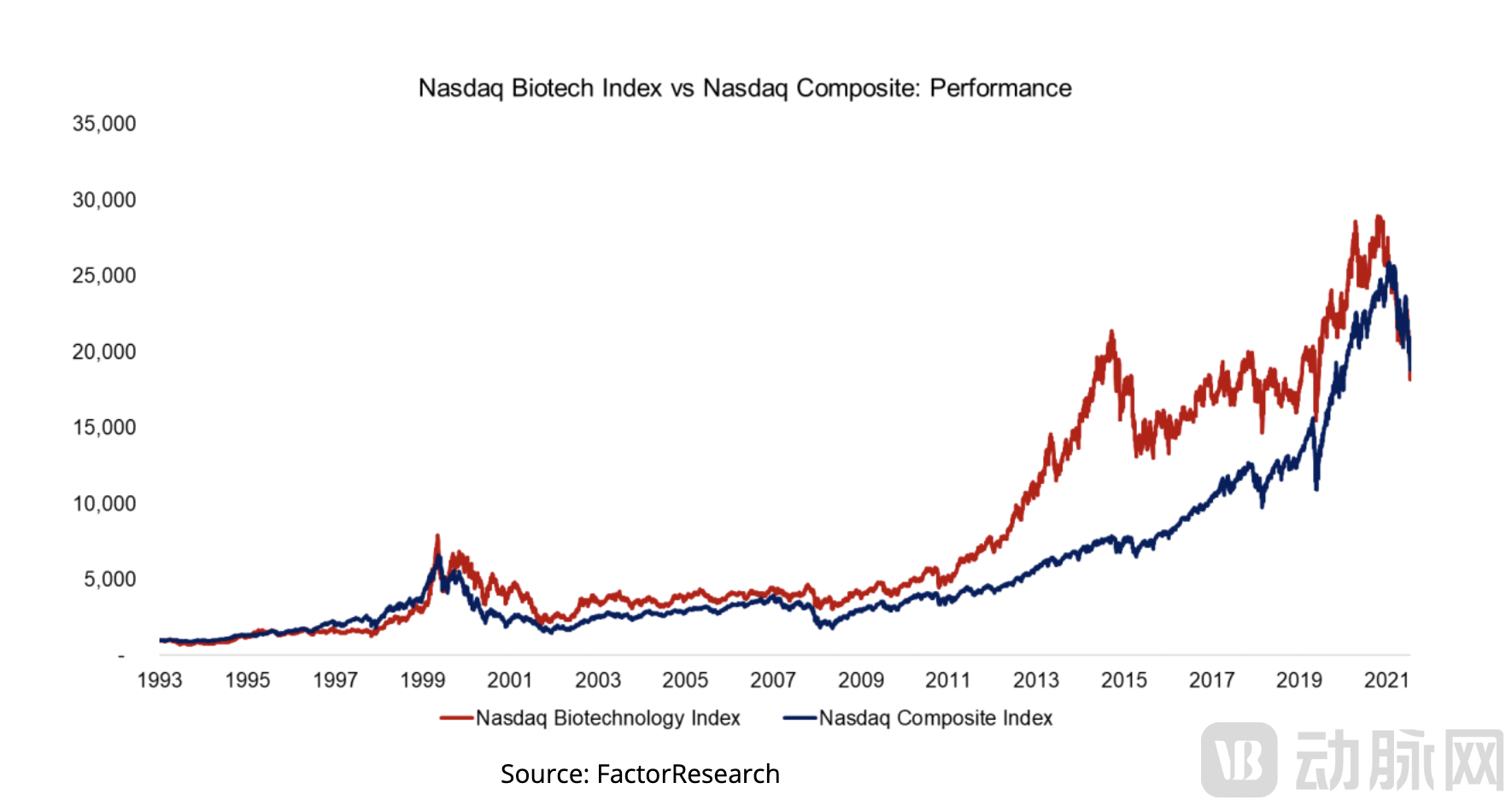

The Biotechnology Index (BTK Index) of the American Stock Exchange faithfully recorded the bubble of 1992 and the subsequent major crash.

In October 1991, the benchmark value of the BTK Index was 200. This index consists of 15 companies, including the then well-known Amgen, Chiron, Biogen, and Immunoex, among others, reflecting the overall performance of the entire industry.

In January 1992, the BTK reached a peak of 223.92 points. Afterwards, as several biotechnology companies' new drugs for sepsis failed, investors lost faith in biotechnological miracles. In the spring of 1992, the bubble burst, and investment and financing in the biotechnology sector fell into a winter. By March 1995, the BTK had plummeted to a low of 77.56.

After hitting the bottom in March 1995, the biotechnology industry experienced a brief recovery. Biotech companies in the U.S. Bay Area, such as Gilead Sciences, seized the opportunity to go public. However, the rebound in 1995 was weak, and the BTK Index never exceeded 160 points—still below its starting point in 1991.

After experiencing several years of downturn,This wave of "winter" lasted until the end of 1999,"The BTK index has finally exceeded the level of January 1992,It took 7 years to return to the starting point.——At the end of 1999, when biotechnology once again became a hot topic on Wall Street, the BTK index fluctuated around 200 points.

However, this round of eruption after seven years of silence was powerful. The recovery began in October 1999 and started to accelerate in January 2000. Before people realized what had truly happened, the value of biotechnology companies in the stock market had already tripled, and the capital market experienced another frenzy like that of 1991.

The BTK Index once again faithfully recorded this market cycle, which was later referred to as the "Genomics Bubble."——By the end of February 2000, the BTK index had risen 487% within 52 weeks, and surged 273% just in January and February. Within those two months, 20 companies filed for IPO applications, already equal to the total number of biotech companies listed in both 1998 and 1999.

At the end of 1999 and throughout 2000, more than 60 biotechnology companies in the United States went public. The genomics boom inspired Bay Area companies — such as Tularik, Caliper Technologies, and Maxgen — to enter the capital market. These companies emerged around buzzwords like genomics, bioinformatics, and proteomics.

At that time, the capital market had already begun to grow weary of internet companies and the prospects they described. Those who had become accustomed to extreme market volatility and speculative investments in young "dot-coms" started to place their bets on biotechnology. A flood of capital from the internet sector created a kind of irrational exuberance.

For much of the year 2000, biotech stocks were a bright spot in an otherwise rather gloomy market. But as the Internet bubble burst, the tech stock disaster eventually spilled over into the biotech sector, and the "genomics bubble" burst.

Take Caliper Technologies as an example. In February 2000, when biotechnology was the hottest topic on Wall Street, the company's stock price was close to $200 per share. By January 2003, Caliper's stock price had fallen to $3. Large biotech stocks also performed poorly, with Genentech's stock price dropping by 38%. The BTK index plummeted by about 40% in 2002.

Moreover, in many aspects, biotech companies have been stigmatized like internet companies—despite their extremely high valuations at their peak, neither type of company has generated noteworthy revenue.

The bursting of the Internet bubble triggered a stock market crash that had a huge global impact, ushering in a bear market period. In fact, it could be said that the "winter" lasted for about a decade — many companies went bankrupt, and many high-quality startup projects lacked the funding needed for survival and growth. Even today, some still believe that the bursting of the bubble marked the worst period in the history of biotech stocks, with the Nasdaq index taking 15 years to return to its peak.

In 2003, biotech companies experienced a slight rebound. According to statistics, data at the end of 2003 showed that the biotech industry secured $16.4 billion in new financing, representing a 56% increase from 2002. Eight new biotech companies went public on NASDAQ, breaking a streak of five consecutive quarters without any initial public offerings. The Nasdaq Biotechnology Index (NBI) rose by 46% in 2003.

But it wasn't until the 2010s that everything truly changed, with a series of events reigniting biotech investment. The good times were finally back, and it was believed that the window for biotech companies to secure funding, as well as the exit window for venture capital firms, had both opened.

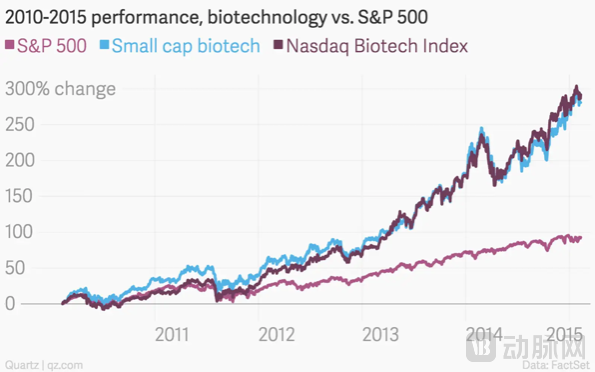

From 2011 to 2015, the biotech sector led the rise in the U.S. stock market and sparked another wave of technological innovation.At the same time, a large number of biotechnology companies have flooded the market through initial public offerings (IPOs) — 33 companies went public in the first half of 2015 (accounting for nearly one-third of the total), compared to 74 companies for the entire year of 2014.

Biotech stocks continued to rise, and by 2014, concerns about a bubble had been growing. Then-Federal Reserve Chair Janet Yellen noted in July 2014 that valuation metrics for biotech stocks "appear substantially overstretched" — a warning about a potential bubble. In March 2015, Fierce Biotech conducted an informal survey of its readers and found that more than half believed the industry had entered a bubble phase.

On September 29, 2015, Time magazine published an article pointing out: Over the past four years, a large number of biotech startups went public, outperforming almost all other industries. However, this feast may have ended, and the biotech bubble could finally be bursting. Since peaking on July 20, 2015, the Nasdaq Biotechnology Index fell by 27% by the end of September that year. Typically, a bear market refers to prices dropping by 20% or more over several months. By the end of June 2016, within a span of 12 months, the NBI index had fallen by 39%.

The last cycle began around 2020, known as the "COVID-19 bubble."In 2020, amid a global economic recession, financing activities in the entire biotechnology sector surged ahead, with a comprehensive and strong rise in the biotech stock index. Venture capital reached a historic high of over 23 billion US dollars, increasing by more than 60% compared to the already robust financing amount in 2019. The appeal of Initial Public Offerings (IPOs) was nearly three times that of the previous year, with over half being preclinical or phase one clinical companies.

The NBI index climbed throughout 2020 and remained stable in the first half of 2021. However, between September and mid-November, this figure dropped by approximately 10%. Throughout 2021, biotech stocks faced historic sell-offs, with the industry’s equities falling more than 50% on average.

In February 2021, warnings had already been issued: the current stage bears a striking resemblance to the final phase of the internet bubble burst, where investors are merely betting on rising stock prices without paying any attention to fundamental valuations—a behavior indicative of high-level speculation.

Referred to as the "COVID-19 bubble" has finally become directly synchronized with China's biopharmaceutical industry, which has now stepped onto the global stage.One data point is that in 2020, nearly one-third of private financings exceeding 100 million US dollars were raised by Chinese companies, while in 2019, this proportion was only one-seventh.

To understand the four up-and-down cycles of the U.S. biotech industry in the past 30 years, there are two key words,News-driven and Bio-crazy.

Reviewing the several Bio-crazes in history reveals that while technology evolves and the world changes rapidly, human cognition and behavior remain unchanged in many aspects.

In 1991, biotech stocks quadrupled or even tripled in just a few months, with biotechnology dominating Wall Street. Analysts believe that Amgen directly triggered the "boom" of 1991 with a series of positive news, capturing Wall Street's attention. First, in March 1991, Amgen won a patent battle and gained control of EPO, one of the most profitable new drugs on the market at the time. Second, Amgen's Neupogen received FDA approval for preventing infections in people undergoing chemotherapy.

The genomics bubble that began in the autumn of 1999 was triggered by several successful IPOs of biotechnology companies, which suddenly stimulated the market. Additionally, the extensive media coverage of the Human Genome Project added the strongest fuel to the fire.

By the end of 1999, investors began to take an interest in genomics. By that time, human chromosome 22 had been fully sequenced, becoming the first completed chromosome; the one billionth base of the human genome had been sequenced; and Celera Genomics was about to publish the fruit fly genome sequence in record time through its collaboration with academia. Individual investors had just been introduced to concepts such as "genomics," "gene expression," or "single nucleotide polymorphisms," but they were already making big bets on the future of these complex technologies.

Not surprisingly, at the time, genomics — the study of how genes control disease and development — was seen as a new era for drug discovery. Investors drove up the stocks of companies like Celera, Incel, and others that were discovering and patenting genes. Companies involved in various aspects of genomics, studying the structure and function of human genes, had soared to particularly high levels. Scientists said that mapping the human genome — the entire sequence of 3 billion chemical pairs that make up human DNA — would give them a genetic blueprint to understand why humans are susceptible to certain diseases. Ultimately, scientists believed this knowledge could help them develop innovative treatments for a variety of diseases.

Since the early 1990s, every change in biotechnology has been exciting. Buzzwords like genomics, high-throughput sequencing, and gene editing are thrilling, and potentially revolutionary drugs are under development, making industry professionals eager to take action.

Just as recombinant DNA technology and monoclonal antibodies propelled the nascent biotechnology field in the 1980s; genomics dominated Wall Street in 2000; and in the 2010s, affordable high-throughput sequencing, along with the emergence of cell and gene therapies, supported a new technological era.

The explosive growth in the number of biotech startups, coupled with a surge in the industry's annual revenue, has bolstered optimism for the biotech sector, driven by excitement over emerging technologies. The prevailing outlook is that technology will save the world and the pharmaceutical revolution will succeed, even if it takes longer and requires more capital than anticipated. For the past 30 years, this industry has been built on such promises.

The capital market places big bets on the future of these complex technologies.. At the height of the frenzy, investors seemed to be unaware that it might take quite a long time before they could see many of the economic benefits brought about by the explosive growth in genomics research and gene therapy.

Overzealous investors may overestimate the feasibility of the technology and underestimate the complexity of the industry. During the most frenzied investment period in genomics, no one asked whether genomics would ultimately improve the efficiency of drug discovery. How many years would it take? Would it eventually lead to the emergence of new drugs? How long would it take for new drugs to gain FDA approval?

But frustratingly, most technological changes are evolutionary, and the much-anticipated revolution in new drug development seems not to have occurred. The regularity of biotech failures has gradually led to the realization that biotechnology is an extremely complex field, far from fulfilling its early promises. A new technology cannot, as expected, create infinite value (or do so in the short term).

Failure is inevitable. Whether there is significant positive news in the biotechnology field driving the market's upward phase; a prolonged absence of positive events, coupled with one or two major failures, triggers the onset of a downturn.

This is often where the bubble starts to burst—not necessarily due to some major, market-shaking change, but rather the straw that breaks the camel's back in an overvalued industry.

Of course, major positive news follows a certain pattern, as major breakthroughs originate from basic research, forming a large cycle every 6 to 8 years. In recent years, due to the faster iteration of new technologies, industrial cycles have become more frequent.

The value cycle in the biotechnology industry occurs more frequently than imagined, and of course, they are not always linked to market sentiment.

Some proponents of biotechnology have long opposed the notion of a "bubble." They argue that today's biotech industry is much more mature, with a stronger foundation than ever before. Relying on novel therapies and the FDA’s inclination to approve more innovative drugs, an increasing number of new drugs are coming to market, and more promising drugs are undergoing Phase II and III clinical trials. Some of these will eventually receive FDA approval and generate significant sales.

Moreover, unlike the biotech bubble of 1991-1992, when investors were buying into the hope of new drug development, many companies today have shown real results. Back then, the only real successes were Genentech and Amgen. Now, there are many companies that have achieved great success.

If we look at the 30 years of Biotech as a whole, the changes have been tremendous and even fundamental. A vision based on harnessing the power of biology and technology to change the world has been circulating ever since the Human Genome Project in the 1990s. It was also from the 1990s that people started to accept this idea. Now, there is a consensus that the 21st century is the "century of biology," just as the 20th century belonged to physics.

In the 1990s, the pharmaceutical and biotechnology industries were completely independent. Today, they form a deeply interconnected community. Back then, small molecules still dominated, and large pharmaceutical companies were almost entirely focused on this model. Proteins remained highly challenging, and the humanization technology for antibodies was under development but still imperfect. Now, new modalities include small molecules, proteins (especially monoclonal antibodies), oligonucleotides (antisense and various forms of RNA), gene therapy and genome editing, nanoparticles, and more.

Correspondingly, the predicament of the modern pharmaceuticals industry is becoming more prominent. Those large pharmaceutical companies, worth hundreds of billions of US dollars, are in urgent need of new drugs. Before 2015, patents for a group of blockbuster drugs have already expired. The "patent cliff" has hit the industry's profits, and the cost of pushing new drugs to market is getting higher and higher.

Therefore,Even if investors have distanced themselves from the biotechnology industry, large pharmaceutical companies will not. This driving force played a crucial role in the 2010-2015 cycle.

From 2010 to 2014, the rise in biotech stocks surpassed any other sector in the U.S. market. In 2014, the healthcare industry set new records for both IPOs and merger and acquisition spending, driven not only by new technologies but also by the urgent need for innovative drugs among many global large pharmaceutical companies as existing patents expired and R&D costs continued to soar.

In the previous major upswing of biotech companies, after the tide receded, the sector's excess returns essentially returned to where they started. However, in the wave from 2010 to 2015, the difference was that although the industry’s excess returns also saw a significant pullback after 2015, overall they did not completely revert as before and remained at a relatively high level. The main driving force behind this wave of biotech companies was the approval of new drugs by numerous biotech firms and the resulting M&A effects.

Cautious and optimistic voices believe that,Wall Street will always burst bubbles. That's not the issue. The question is, when and how severe the ensuing downturn will be.A pullback is inevitable, and the market will continue to experience fluctuations. However, due to the solid foundation that has been established in the industry, there will no longer be significant or sharp pullbacks, such as the severe crash that occurred in 1992.

30 Years: Rather than a Revelation of Four Up-and-Down Cycles of U.S. Biotech, It Is a Revelation of Human Behavior.

Driving these cycles is an effective combination of greed and creativity. Memory, however, is short-lived:Most investors working in this industry today have not experienced major up and down cycles, and some investors know nothing but bull markets.

The market's madness lies in everyone thinking they can become the next Genentech, the next Biogen, the next Moderna.

When the market falls, investors turn to safe assets to reduce risk, so it's no surprise that biotech stocks are being heavily sold off. This negative sentiment flows back into private markets — for venture capitalists (VCs), exiting through an IPO in the public market becomes more difficult. Therefore, if investors are concerned about their ability to exit, it becomes even harder for biotech startups to secure initial financing.

How can investors avoid more volatility that comes with the tech boom? The answer is they probably can't. They must realize that markets don't operate smoothly and gradually, but rather in sudden bursts of enthusiasm and despair.Investors rush to profit from new technologies and then scramble for shelter when a crisis hits.

Exciting new technologies promise to change the world, but you need to act quickly before opportunities vanish — make hay while the sun shines. In an environment of optimism and frenzy, people tend to become even more optimistic and frenzied; rationality hardly plays a role, giving way instead to zeal, chaos, and greed. It is only after hitting a wall that people regain their rationality, but they may then become overly pessimistic and cautious.

The biotechnology industry always experiences sudden excitement, followed by booms and bubbles, then disappointment and a downturn, in a recurring cycle.

However, people can learn lessons from the experiences of the past few years and avoid making some obvious mistakes.One starting point is to understand the biotechnology industry and the Internet revolution, as well as its differences.

After 2000, the Internet bubble and the biotech bubble always followed closely.After investors' money flowed out of the internet, they needed to find the next exciting field. The aftermath of the 1999-2000 internet bubble quickly gave way to the genomics bubble of 2000-2001.

An obvious common feature is the entrepreneurial culture. Smart biologists are motivated by the market just as smart computer scientists are. Moreover, both industries share a similar willingness to take significant risks in pursuit of high returns.

However, these two industries are also very different. Silicon Valley entrepreneurs like to boast about their "internet time," where the lifespan of their products is measured in "months" rather than "years." In contrast, the biotechnology field is completely different. Drug discovery remains an art that relies on judgment, instinct, and experience, with decisions made amidst the fog of limited knowledge and experience. It takes a company ten years of research and development to achieve a breakthrough in the lab and eventually develop a commercially viable drug.

We should understand that biotechnology will not generate any immediate "killer apps." In this industry, no one can get rich overnight. Those who join this industry should be long-term investors.

This might be the simplest truth that these 30 years have taught us.

Another simple truth is: history has its own laws of operation, it won't simply repeat itself, but humans will repeat their behaviors.