How Domestic Neurovascular Device Companies Break Through Amid Product Homogenization, Volume-Based Procurement, and Multinational Localization

Wallaby Medical

Developer and Producer of Therapeutic Products in the Neurointervention Field

HeartCare

Neurointerventional Medical Device Developer

Zylox-Tonbridge

Innovative R&D, Production, and Sales of Medical Devices in the Vascular Intervention Field

Peijia Medical

Developer of Cardiac and Cerebrovascular Interventional Medical Devices

In last year's year-end review, we observed trends such as the capital market in the neurointervention field becoming more rational, innovative products entering the payoff period, neurointervention companies gradually exploring overseas markets for new growth points, and neurointervention products beginning to be included in centralized procurement.

Based on these observations, we have made the following judgments: innovative enterprises lacking capital advantages still have development opportunities; market competition will become increasingly fierce; the penetration rate of neurointervention will rapidly increase, and the market size will continue to grow; the scope of centralized procurement will further expand, making it essential for domestically produced neurointervention products to enter overseas markets; with the support of "medicine, research, enterprises, government, and capital," product innovation in the neurointervention field will accelerate.

Looking back at 2022: In the neurointervention field, there were only three financing events—Rapex Medical, Lepu Neurotech, and XinKaiNuo Medical—indicating that the capital market has gradually shifted its focus. Throughout 2022, more than 120 neurointervention products were approved, making the sector highly crowded.

At the same time, the penetration rate of neurointerventional surgeries in China is accelerating, and the neurointerventional businesses of various related companies saw significant growth in 2022. For instance, Minimally Invasive Brain Science's revenue for 2022 is expected to reach 520 million to 540 million yuan, representing a year-on-year increase of 36% to 41%. Peijia Medical's revenue for 2022 is projected to be between 240 million and 260 million yuan, marking a year-on-year growth of 75.8% to 90.4%. HeartCare Medical's revenue in the first half of 2022 reached 76.7 million yuan, reflecting a year-on-year increase of 154.6%. Zylox-Tonbridge's neurovascular intervention business revenue in the first half of 2022 amounted to 112 million yuan, with a year-on-year growth of 160.1%.

Wallaby Medical, Minimally Invasive Brain Science, and Zylox-Tonbridge strengthened their exploration of overseas markets in 2022, with significant growth in overseas revenue. For instance, Minimally Invasive Brain Science's overseas business income exceeded RMB 20 million for the first time in 2022, increasing more than 32 times compared to the previous year; Zylox-Tonbridge’s revenue from overseas markets achieved a 49% year-on-year growth in 2022.

Also in 2022, products from various neurointerventional companies in China were successively approved. Among them were a large number of homogenous products, but also several innovative ones, such as the dense mesh stent launched by AccuMedical, the self-developed balloon-expandable delivery catheter by Peijia Medical, and the delivery-assist microcatheter by Zhongtian Medical…

It can be seen that the changes and developments in neurointervention in 2022 generally aligned with the predictions we made at the end of 2021. Now, at the beginning of 2023, looking ahead to the future, where will the development of the neurointervention field go? What new challenges will companies face? What new trends will emerge in the neurointervention field in 2023?

Since 2021, neurointerventional products have been approved at an accelerated pace.

According to incomplete statistics from VCBeat, more than 25 neurointerventional products were approved in 2021, and over 120 products were approved in 2022.

However, although many neurointerventional products were approved in 2022, most of them are homogeneous products, and the competition is extremely fierce. According to industry insiders, among the approved products in the neurointerventional field in 2022, there were 24 balloon-related products, accounting for 20%; 23 intermediate catheters, accounting for 19%; 17 microcatheters, accounting for 14%; and a total of 63 access products, accounting for 52%.

(VCBeat incomplete statistics, approval status of neurointerventional products made in China in 2022)

Among them, innovative companies such as Zhongtian Medical, Libai Technology, Maichuang Medical, and Pugao Medical have received approvals for a relatively large number of products, with 6, 5, 5, and 5 products respectively.

Reviewing the approval status of domestically produced neurointerventional products in 2022, it can be observed that: the number of neurointerventional products approved for domestic brands has far exceeded that of imported brands. Moreover, the types of domestically produced neurointerventional products are diverse, covering stent retrievers, aspiration catheters, coils, microcatheters, intermediate catheters, distal access catheters, and intracranial balloon dilation catheters, among others.

The listing of various domestically produced neurointerventional products represents that Chinese neurointerventional companies are now able to meet the clinical needs of most relevant patients and fulfill the diverse demands of different patients.

But it has to be admitted: the overall market pattern of neurointervention is still dominated by multinational medical device companies such as Medtronic, Stryker, and Johnson & Johnson. For example, the localization rate of China-produced devices in the neurointervention ischemic market is about 30%, while the remaining 70% of the market is occupied by multinational medical device companies. In terms of products, the performance and quality of neurointervention products from various China-produced brands are uneven.

On the other hand, the approval of similar products has increased, intensifying market competition. A search on the National Medical Products Administration's official website using the keyword "intracranial balloon dilation catheter" shows 32 products; a search with the keyword "coil" shows 20 products; and a search with the keyword "distal access catheter" shows 21 products.

(Image source: Official website of the National Medical Products Administration)

In 2021, thrombus aspiration was still considered a high-barrier market. In May 2021, China's first domestically produced intracranial thrombus aspiration catheter system received NMPA approval. Prior to this, the market was mainly dominated by the ACE aspiration catheter from Penumbra, introduced by Genesis. However, in 2022, the National Medical Products Administration (NMPA) successively approved seven intracranial thrombus aspiration catheters, making this niche market quickly become lively.

In addition to aspiration catheters, 12 intracranial balloon dilation catheters, 10 microcatheters, and 10 distal access catheters were approved in 2022... Moreover, according to the product registration information from manufacturers in the Henan procurement, there are over 40 intermediate catheters and nearly 20 thrombectomy stents.

From the above figures, we can see the intensity of competition in the neurointervention field. Moreover, this raises another question: with so many products already in the neurointervention field, is there still room for innovation? — Of course, there is. At the very least, there are still many clinical pain points that have not been addressed in clinical practice, and this is the direction where companies need to focus their innovation and efforts.

For example, in previous endovascular surgeries for treating intracranial atherosclerotic stenosis (ICAS), the procedure generally required twelve steps. Peijia Medical has independently developed a delivery-type balloon dilation catheter, making this surgical method simpler and easier to perform.

Compared with other products on the market, the delivery balloon dilation catheter integrates the functions of both balloon catheters and microcatheters. With this innovative product, clinicians will eliminate the need for multiple exchanges during surgery, reduce complications caused by intraoperative manipulation, lower surgical risks, and improve safety.

Therefore, there are still many unmet clinical needs in the field of neurointervention, waiting for enterprises to overcome.

From the perspective of market competition, for companies like Minimally Invasive Brain Science, Genesis, and Zylox-Tonbridge, which already occupy a significant market share, they face the impact of competing products, and their market share may be affected. However, with the substantial increase in the penetration rate of neurointervention, the revenue of these companies is expected to maintain steady growth.

For companies with newly approved products, how to stand out among a large number of competing enterprises and achieve expected sales output is also a challenge that must be faced. Undoubtedly, the pressure involved is enormous.

At the end of December 2022, Jilin Province announced the winning results of the 21-province coil procurement alliance, putting the winning companies at ease.

However, Jilin Province did not disclose the prices and reduction幅度 of this round of centralized procurement, which inevitably makes more people curious and anxious. However, according to the principle of "trading price for volume," and based on previous experience with coil procurement, the industry expects a significant price reduction in this round.

On the one hand, the 21-province alliance covers a wide range, accounting for about two-thirds of the market in China; on the other hand, the procurement cycle is long, lasting for 2 years. If they fail to win the bid, related enterprises will lose most of China's coil market for nearly 2 years. Therefore, each enterprise will carefully fill in the price to win the bid.

In addition, coil springs have previously been included in bulk procurement by Hebei, Jiangsu, and Fujian respectively. In Hebei, the average selected price of coil springs dropped from 12,000 yuan to around 6,400 yuan, with an average decrease of 46.82% and a maximum decrease of 66%. In Jiangsu, the average decrease for neuro-dedicated coil springs was 54%, with a maximum decrease of 69%, bringing mainstream products down from 10,000 yuan to around 3,500 yuan. According to the "volume-for-price" principle, it is expected that a larger market and longer procurement cycle will lead to lower prices and greater reductions.

It is worth mentioning that compared with the previous two years, more coil products have been approved for marketing, and the competition among enterprises has become more intense. Enterprises that have already occupied a certain market share, such as Minimally Invasive Brain Science, Genesis, Zylox-Tonbridge, Peijia Medical, and HeartCare, hope to stabilize or even increase their market share. Meanwhile, companies with newly approved products aim to quickly open up the market and boost sales through centralized procurement. Therefore, this will also affect the bidding prices of various enterprises.

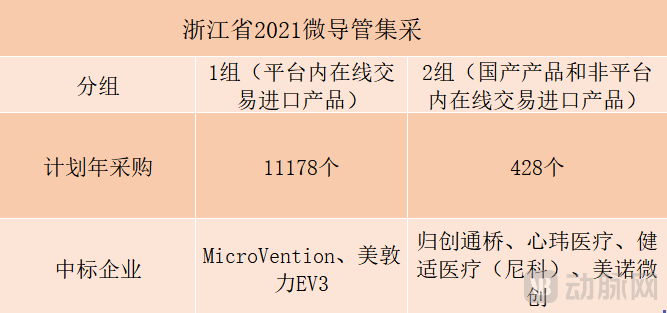

In addition to coils, neurointerventional microcatheters have also been included in the centralized procurement by Zhejiang Province. This procurement is divided into Group 1 and Group 2. Group 1 consists of imported products traded online within the platform, with an annual planned procurement of 11,178 units; Group 2 includes domestically produced products and imported products not traded online within the platform, with an annual planned procurement of 428 units.

(VCBeat Mapping)

It is clear that the main procurement of microcatheters in Zhejiang Province's centralized procurement focuses on imported products, with domestically produced products accounting for only about 4%. Nowadays, microcatheters have become "oversaturated," with 10 microcatheter products approved just in 2022. It is expected that subsequent centralized procurements will significantly impact the market share of multinational medical device companies.

At the same time, after multiple rounds of bulk procurement, the centralized procurement rules have been gradually optimized and adjusted. For instance, the 21-province alliance led by Jiangsu Province and Jilin Province has increased the procurement volume of domestically produced coil springs.

For centralized procurement, industry insiders said: Centralized procurement helps Chinese domestic companies increase production volume. After products are included in large-scale centralized procurement, revenue may initially show a certain degree of decline. However, when price reductions lead to an increase in the number of surgeries and market concentration improves, companies will achieve volume growth through lower prices and improve revenue.

Another person in charge of a neurointerventional company stated: Compared with imported products, domestically produced products have more advantages in terms of cost. Therefore, keeping up with policy changes, ensuring high product quality while reducing production costs as soon as possible, is one of the ways out for enterprises.

Based on this, a group of companies have begun to reduce product manufacturing costs. For example, the neurointerventional products introduced by Genesis have all achieved technology transfer and localized production in 2022. Localization and scale will enhance the cost-performance ratio of the products.

With the advancement of centralized procurement, the penetration rate of neurointervention will increase rapidly. However, due to factors such as fierce competition and significant price reductions, domestic neurointervention companies may also need to seek other paths.

In 2021, when neurointervention was extremely popular, the two core reasons why investment institutions were optimistic about this field were: first, there are many patients with cerebrovascular diseases and they cause significant harm, making it a market with strong demand and broad prospects; second, the neurointervention market is monopolized by imported products, leaving large space for domestically produced alternatives.

However, at present, the logic of domestic substitution is being challenged. Multinational medical device companies such as Medtronic, Stryker, and Johnson & Johnson, which dominate the majority of China's neurointerventional market, are implementing localization strategies and strengthening local construction.

On November 15, 2022, Medtronic's medical technology industrial base was launched in Lingang. According to reports, Medtronic will build a localized R&D and production base for high-end cardiovascular medical technology in the "Life Blue Bay" park, which is expected to officially begin operations in 2023.

Compared to Medtronic, Johnson & Johnson places greater emphasis on the Chinese market. This is because the Chinese market has become one of Johnson & Johnson's fastest-growing markets globally, with its share of global sales increasing annually.

Therefore, Johnson & Johnson has built and put into operation supply chain production bases in multiple locations in China. For example, in 2019, Johnson & Johnson invested an additional $180 million to build a new Ethicon factory on the basis of its existing orthopedics plant in Suzhou; in 2021, Johnson & Johnson established a new customer logistics warehouse in Suzhou; in June 2022, Guangzhou Bioseal Biotechnology Co., Ltd., a wholly-owned subsidiary of Johnson & Johnson in China, invested 150 million yuan to upgrade and expand production.

At the same time, Johnson & Johnson's three major businesses have established R&D centers or departments in China. It has also set up an Asia-Pacific Innovation Center, an innovation incubator, and a professional education center in China. Today, Johnson & Johnson has established bases in Suzhou, Xi'an, Guangzhou, and other places for R&D, production, and capacity expansion. These regions have become important components of Johnson & Johnson's global supply chain system.

Besides this, another medical device giant, Stryker, is also implementing a localization strategy. Currently, Stryker has three product distribution channels in the Chinese market: first, global R&D by Stryker, which involves introducing advanced overseas products to China to help Chinese patients; second, collaborating with local innovative companies such as Hightech Newlight to quickly bring products to market; and third, local R&D, where its R&D team designs products based on clinical insights to meet the needs of the Chinese clinical environment.

It is reported that Stryker's China Innovation Center is under preparation and construction in Shanghai, and is expected to be officially put into use in the first half of 2023. As Stryker's first innovation center in China, the center will be equipped with advanced orthopedic laboratories, open surgery laboratories, catheterization rooms, and other professional medical education facilities.

Overall, multinational medical device companies (Medtronic, Johnson & Johnson, Stryker), which collectively account for over 70% of China's neurointerventional market, are establishing research and development centers and manufacturing bases in China. If the location of production is used as the criterion to distinguish between imported and domestically produced products, then domestic brands may no longer be able to develop under the logic of "domestic substitution," but instead must engage in fierce competition with other companies in the market.

In addition, multinational medical device companies are also strengthening skills training, promoting doctor education, and popularizing neurointerventional technology in China. For example, in August 2022, the "Torch Plan" supported by Johnson & Johnson was officially launched, aiming to provide standardized basic surgical skills training for young clinical surgeons. Over the next three years, the "Torch Plan" is expected to cover 2,000 grassroots hospitals across China, reaching millions of healthcare workers.

The localization strategies and market promotion capabilities of multinational medical device companies will pose greater challenges to domestically produced brands. The future competition in the neurointerventional market will also put the comprehensive capabilities of companies in the industry to a greater test, such as product capability, commercialization capability, and innovation capability. Companies with certain weaknesses may be acquired or directly eliminated by the market.

How the market will change in the future and how companies will respond, VCBeat will continue to track and wait to see.