Recently, Liaoning Yinyi Biomedical Materials R&D Center Co., Ltd. (referred to as "Yinyi Biotech") updated its prospectus and plans to be listed on the ChiNext Board of the Shenzhen Stock Exchange. The company intends to raise 1.678 billion yuan for projects including the capacity upgrade of vascular interventional medical devices, the construction of a research and development center, the upgrade of the marketing network and information technology projects, as well as the supplementation of working capital.

Yinyi Biotech mainly engages in the research, development, production, and sales of high-end medical devices for vascular intervention. Its core product is a coronary drug-eluting balloon catheter. For many years, stent implantation has been the mainstream method for coronary heart disease intervention. However, while acting as a drug delivery tool to prevent restenosis, stents remain in the body as foreign objects. With the recent promotion of the "intervention without implant" concept, the usage of drug-eluting balloons has grown rapidly.

However, as the price of drug-eluting balloons has significantly dropped after being included in the centralized procurement program, the company's gross margin has also declined. More concerning is that the sales volume growth driven by centralized procurement failed to offset the impact of the price reduction, and the company expects its operating revenue for 2022 to decrease sharply by 30.94% to 34.96% compared to 2021. Additionally, the company has long adopted a "sales-focused, R&D-light" model, with R&D investment lagging far behind comparable companies. Paradoxically, the company’s gross margin remains much higher than industry peers, prompting the exchange to inquire twice about the reasonableness of this phenomenon.

Price Reduction of Core Products During the Reporting Period75%

Yinyi Biotech was founded in October 2004 and has been deeply engaged in the field of coronary intervention treatment for nearly two decades. The company's currently approved and marketed products are all Class III medical devices, including drug-eluting balloons, balloon dilation catheters, drug-eluting stents, bare metal stents, and angiographic catheters.

Recently, the company's products have expanded into the neurointerventional and peripheral vascular fields. In December 2022, its self-developed and produced intracranial balloon dilation catheter and PTA balloon dilation catheter were approved for marketing.

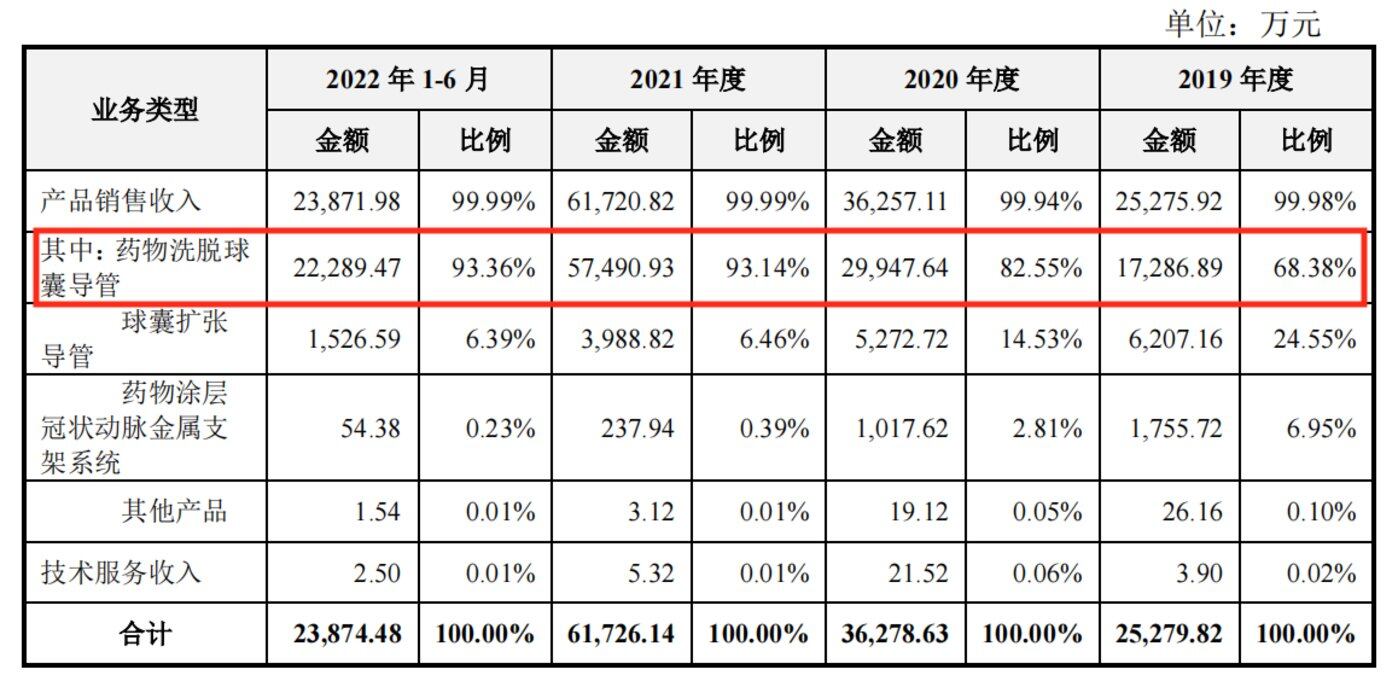

During the reporting period, more than 90% of Yinyi Biotech's revenue came from two products: drug-eluting coronary balloon catheters and balloon dilation catheters, with the majority of revenue coming from drug-eluting balloon catheters. The prospectus shows that from 2019 to the first half of 2022, the combined revenue of these two products accounted for 92.94%, 97.08%, 99.6%, and 99.76% of total main business revenue, respectively. The revenue from drug-eluting balloon catheters accounted for 68.38%, 82.55%, 93.14%, and 93.36% of total main business revenue, respectively.

Data source: Prospectus

Drug-eluting balloon catheter products are drug delivery devices used in percutaneous coronary intervention (PCI) procedures. The drug coating on the balloon surface, which inhibits cell proliferation, is pressed into the vessel wall during balloon expansion, serving to suppress vascular hyperplasia. After the drug is released, the balloon is withdrawn from the vessel, leaving no foreign objects behind in the body. Balloon dilation catheters, on the other hand, are used in PCI procedures to pre-dilate areas of vascular stenosis and to perform post-dilation after stent placement.

It is worth noting that centralized bulk procurement has been basically implemented nationwide for these two main products, and the impact of such procurement has already been reflected in the gross profit margin of the products.

During the reporting period, the gross profit margin of the company's drug-eluting balloon catheter products was 96.70%, 95.80%, 95.42%, and 90.86%, respectively, showing a downward trend. The company stated that the main reason is that since December 2020, local alliances have successively organized centralized volume-based procurement of coronary drug-eluting balloon catheters, leading to a decrease in terminal bidding prices. According to the prospectus, the selling price of this product dropped from 8,010.98 yuan/unit in 2019 to 2,022.82 yuan/unit in the first half of last year, with a reduction of 74.76%.

Data source: Prospectus

Under the impact of centralized procurement, the gross profit margin of another major product of the company, the balloon dilation catheter, has seen a more significant decline, reporting 80.82%, 76.12%, 62.53%, and 33.42% during the reporting period. The company stated that from 2020 to 2021, 31 provinces, municipalities, and autonomous regions across China successively implemented centralized volume-based procurement for balloon dilation catheters, with the company's products being selected in 18 provinces, municipalities, and autonomous regions. Meanwhile, the price of this product has dropped from 1,111.97 yuan/unit in 2019 to only 261.34 yuan/unit, marking a decrease of 76.51%.

Data source: Prospectus

Regarding whether the centralized procurement will continuously have an adverse impact on the company's profitability, Yinyi Biotech told Titanium Media APP, "Based on the current implementation of centralized procurement and the policy's protection of innovative products, the risk of a further significant short-term price drop for the company’s drug-coated balloons is relatively low, and future sales volume is expected to maintain rapid growth."

The company also stated in the prospectus that the sales volume of its drug-eluting balloon catheters increased by 106.79% in 2020 and 181.11% in 2021. According to data from Frost & Sullivan, its sales volume ranked first in the Chinese market in 2021, with a market share of 41.5%, surpassing B. Braun's 27.1%.

However, judging from the performance in 2022, the impact of centralized procurement on the company is far from optimistic. In its reply letter to the Shenzhen Stock Exchange, the company mentioned that it expects its total revenue for the whole year of 2022 to be approximately RMB 401 million to 426 million, representing a decrease of about 30.94% to 34.96% compared with the same period in 2021. This is mainly due to the implementation of centralized volume procurement of drug-eluting balloons, where the increase in product sales failed to offset the impact of price cuts from centralized procurement.

Heavy on Sales, Light on R&D: High Gross Margin Reasonableness Questioned

With the promotion of the concept of "intervention without implant" in recent years, the usage of drug-coated balloons has grown rapidly and is expected to continue at an increasing rate. According to forecast data from Frost & Sullivan, the usage of drug-coated balloons surged from 7,500 units in 2016 to 290,000 units in 2021, and is projected to further rise to one million units by 2025, with a compound annual growth rate of approximately 36.27%. Meanwhile, the market size also increased from 135 million yuan in 2016 to 2.009 billion yuan in 2021, and is expected to further grow to 4.386 billion yuan by 2025.

After the rapid expansion of the market, there is no shortage of competitors in the industry vying for market share. As of now, there are 11 coronary drug-eluting balloon products that have been approved for marketing in China, with participants including both local companies and multinational corporations. Among them, local enterprises started relatively late, with technical levels and innovation lagging behind multinational corporations, but they have better R&D achievements transformation and faster development speed. Representative companies include Yinyi Biotech, Grand Pharmaceutical, Shanghai Shenqi, and Lepu Medical, etc.; multinational corporations occupy a dominant position due to their deep technical accumulation and product quality assurance, such as B. Braun from Germany, Boston Scientific, and Medtronic. In the future, with more competitors and rival products entering the market, market competition will undoubtedly intensify further.

To enhance market competitiveness and increase market share, Yinyi Biotech has chosen to expand its production capacity. Among the projects funded by this IPO, the company plans to invest 672 million yuan in upgrading the production capacity of vascular interventional medical devices. The construction period for the project is one year, and upon reaching full production, it will achieve an annual production capacity of 600,000 drug-eluting balloon catheters and 600,000 balloon dilation catheters.

However, in terms of the drug-eluting balloon catheter products, the company's sales volume was 125,400 units in 2021, which still has a certain gap compared to the production capacity of 600,000 sets. Whether there will be an overcapacity situation, the company did not mention.

Moreover, future capacity expansion will likely lead to a continued rise in promotional expenses. In recent years, due to the increase in customer acquisition and maintenance costs as well as more promotional activities, Yinyi Biotech's promotional service fees have risen year by year from 2019 to the first half of 2022, reaching 79.1843 million yuan, 91.9128 million yuan, 127.3709 million yuan, and 30.0886 million yuan respectively. These figures accounted for 74.1%, 69.34%, 68.81%, and 72.29% of each period’s sales expenses respectively. The prospectus reveals that, due to heavy investment in promotion, the company’s sales expense ratio from 2019 to 2021 was higher than that of its peers.

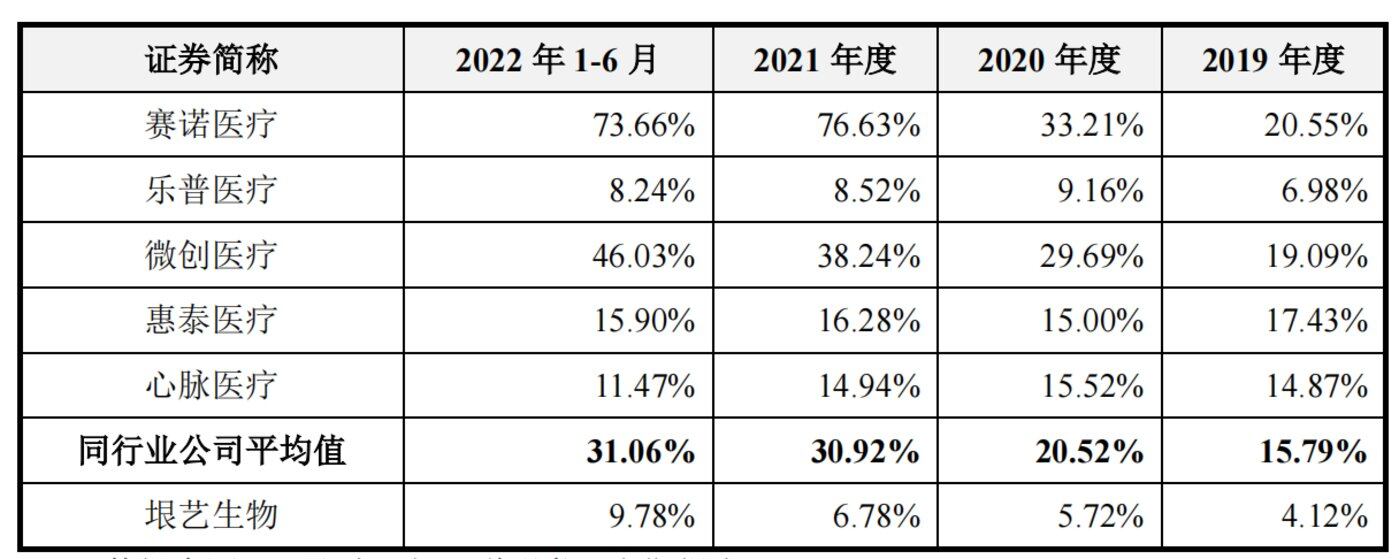

However, compared with the promotion service fee, the company's investment in R&D appears somewhat "stingy." During the reporting period, the company's R&D expenses were 10.4088 million yuan, 20.7468 million yuan, 41.8306 million yuan, and 23.3529 million yuan, respectively, accounting for 4.12%, 5.72%, 6.78%, and 9.78% of operating income. The company's R&D expense ratio is not only lower than its own sales expense ratio but also far below the average of comparable companies.

Comparable Companies' R&D Expense Ratio Data Source: Prospectus

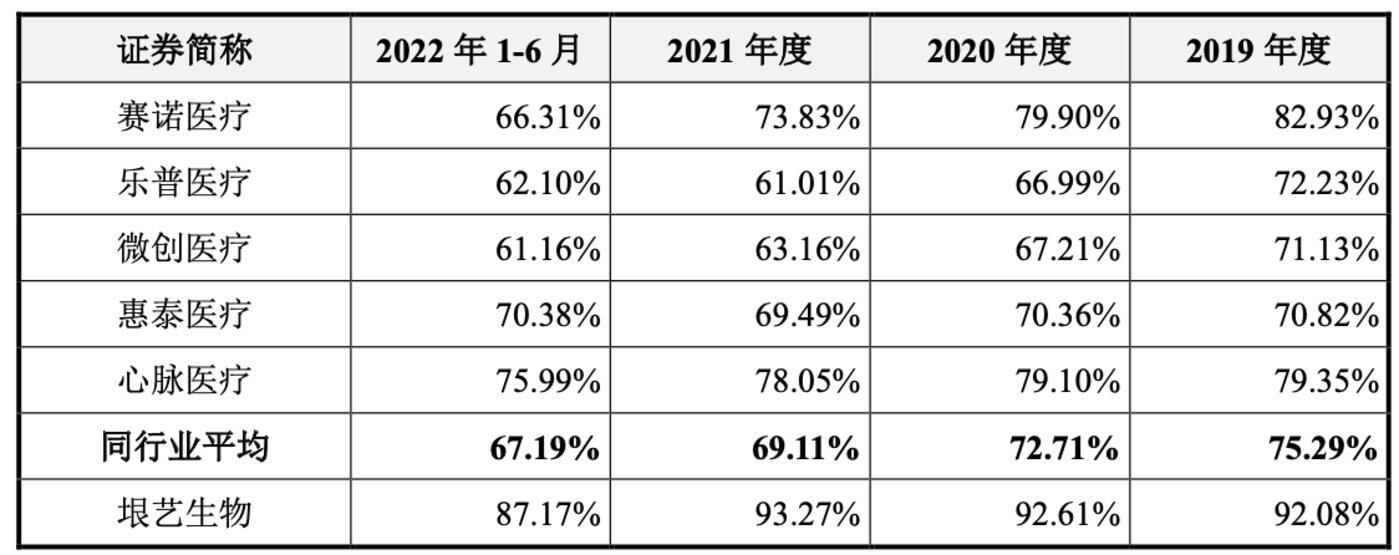

Strangely, although Yinyi Biotech spends the least on R&D, its gross profit margin is much higher than the industry average. Even though its gross profit margin dropped to 87.17% in the first half of last year, it was still 20 percentage points higher than the industry average.

Comparable Companies Gross Profit Margin Data Source: Prospectus

In response, the Shenzhen Stock Exchange raised questions in its inquiry. The company explained that the differences in product segmentation from comparable companies in the same industry resulted in a higher comprehensive gross profit margin compared to those companies. As for the lower research and development (R&D) expense ratio compared to the industry peers, the reasons are: firstly, the issuer is at a disadvantage in terms of financial strength, thus being more cautious about R&D investments in attracting top talents, advanced technologies, and equipment; secondly, peer companies have more product pipelines, leading to higher R&D investments, whereas the issuer focuses specifically on drug-coated balloon catheter products.

However, the company's response did not dispel the regulators' doubts. In the second round of inquiries, the Shenzhen Stock Exchange (SZSE) again explicitly requested the company to provide supplementary explanations regarding the rationality of its gross profit margin being higher than the industry level despite its R&D expense ratio being lower than that of peer companies.

Dividend payout during the review period

The prospectus shows that Yinyi Biotech submitted an application for the initial public offering of shares and listing on the ChiNext Board to the Shenzhen Stock Exchange on June 23, 2022. During the review period, the company held a board meeting and a shareholders' meeting on September 5 and September 22 of the same year, respectively, to review and approve the "Proposal on the Company's 2022 Semi-Annual Profit Distribution Plan," agreeing to distribute a cash dividend of 3.6 yuan (including tax) per 10 shares to all shareholders, totaling 54.3652 million yuan.

The company stated that the amount of this cash dividend accounts for 50.01% of the net profit attributable to the parent company's owners in the first half of 2022. In the same period, the net cash flow from operating activities was 72.9685 million yuan, which is also sufficient to cover the dividend amount. Therefore, although the asset scale and debt repayment capacity decreased after this dividend, it does not affect the normal operation of the company. Meanwhile, the company still retains a high amount of undistributed profits to be shared by both new and existing shareholders after the IPO, without adversely affecting the interests of new and existing shareholders.

In fact, Yinyi Biotech was not short of money originally. As of the end of June last year, the company had 314 million yuan in cash on hand, with no interest-bearing debt, a debt-to-asset ratio of only 8.56%, and a current ratio as high as 8.21. Therefore, given that the company has "idle funds" for dividends and a strong debt repayment ability, the necessity of raising 200 million yuan in this IPO for replenishing working capital is questionable.(This article was first published on the Titanium Media APP, Author/Zhai Biyue)