Top Angel Investors Are Launching Their Own Startups—Here’s What They’re Building

Anlong

Gene Therapy Drug Developer

Nowadays, an increasing number of former institutional investors are stepping into the spotlight, embracing a role that is both familiar and unfamiliar to them—entrepreneurs.

The transition from Party A to Party B is not easy, but these individuals, who are most adept at the intricacies of capital operations, are becoming a vital force among China's high-quality entrepreneurs. From investors to today’s entrepreneurs, how many can rise to become great business leaders? What inspiration will their practices bring to the management and operation of modern healthcare enterprises? We reached out to some of them, sitting down to hear them talk about their dreams, past investment experiences, and future business strategies.

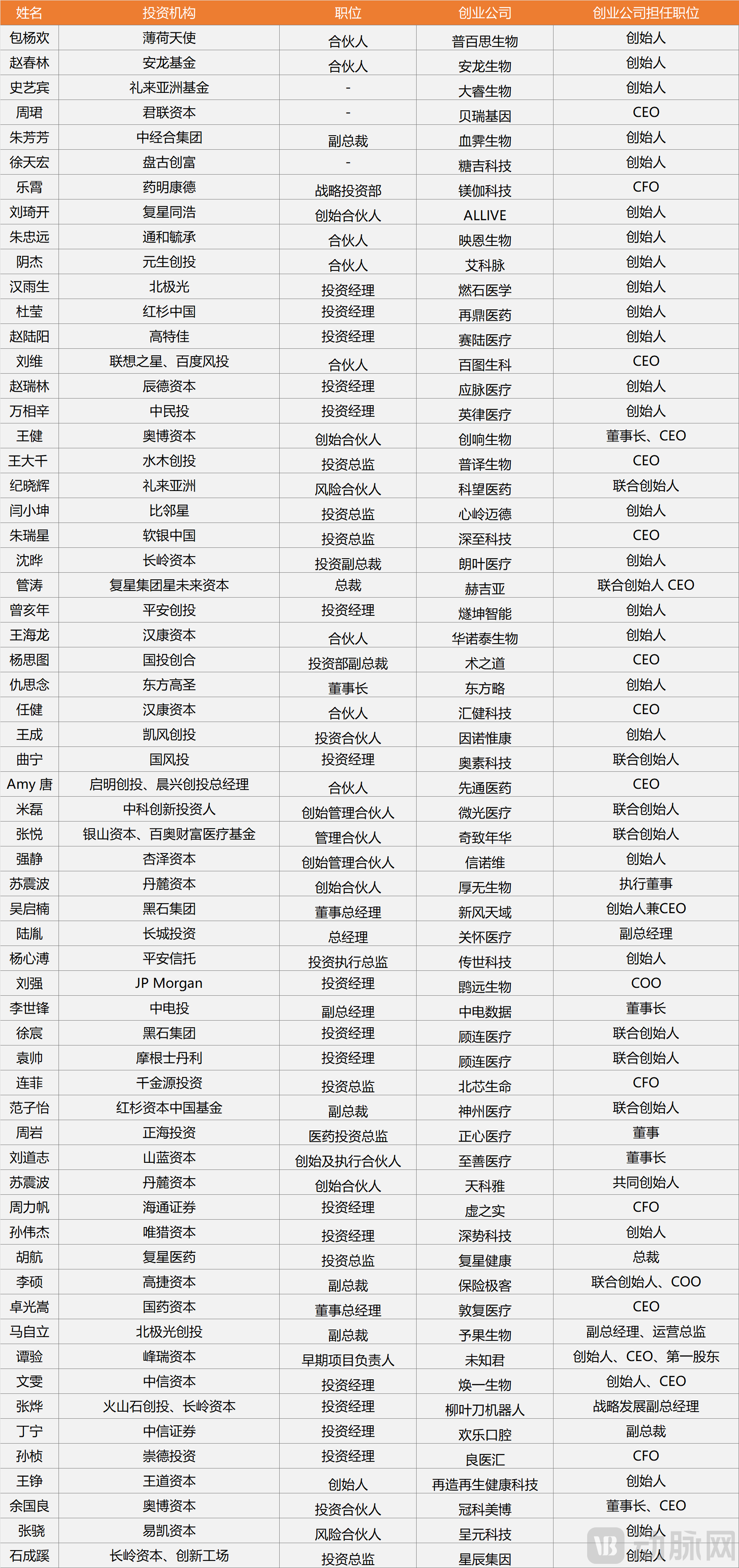

At the end of the article, we have also compiled a list of investors who have entered the entrepreneurial arena, obtained from public and social channels. We hope that, starting from this list, more inspiring entrepreneurial stories will emerge in the wave of innovation in our times.

After the Beginning of Spring in February, the world returns to its busy pace once again.

In a brand-new office in Suzhou Industrial Park, Bao Yanghuan, who recently transformed into an entrepreneur, is contemplating how to keep his newly established company, Precision Brain Science, alive after being founded for less than three months. "For angel round financing, investors focus on the founder as an individual. Moving forward, the company must continuously make progress, and its core team, direction, and technology need to gain recognition from external parties, including investors. Only then can the company be considered on the right track."

On the other side, in a biotech company's Guangzhou laboratory, the company's co-founder is staring at the clinical research data just transmitted from the lab, contemplating which环节 can be further optimized. At the end of the interview, this co-founder asked us to temporarily withhold his name.

These days, Zhao Chunlin, the founder of Anlong Biotech, has been exceptionally busy as the company's newly submitted clinical trial application has been successfully accepted. When winter gives way to spring, Anlong will initiate its pivotal clinical trial. However, years of habits as an investor have kept him bustling between various industry exhibitions and forums non-stop during this spring season when the industry is experiencing a full recovery.

Before diving into entrepreneurship, Bao Huanyang was a partner at a well-known angel fund in China. The aforementioned co-founder and Zhao Chunlin have respectively established their own angel investment funds. As angel investors, they have long become prominent figures in China's life science venture capital industry.

Having long been at the highest decision-making level of angel investment funds, they have participated in the early investment decisions of most unicorn companies in the industry. They have invested in star companies such as Genetron Health, MGI Tech, and I-Mab Biopharma. Most importantly, they possess a unique insight into early-stage projects and are the investors closest to the industry.

Angel investors are the most unique type of investors. They are the first to invest in someone else's dream, demonstrating extraordinary courage and remarkable boldness. After all, when investing in very early-stage projects, angel investors cannot rely on product or financial data like institutional investors do in later stages to rationally assess investment opportunities—the risk of loss is considerable.

Generally, a truly successful angel investor must also be an industrially hands-on expert with strong practical abilities. Most of the time, angel investors are faced with products that are not yet fully developed and teams that have not been assembled. At this point, their only points of reference are their understanding of the team founder, the technology itself, a reasonable expectation of the product's potential, and their own hands-on capabilities.

More often than not, angel investors were originally entrepreneurs themselves, their careers being an intertwining of these two identities.

"Born to be restless, simply can't stop." In 2013, the aforementioned unnamed co-founder, who was not yet 40 years old, sold the company he had co-founded nearly a decade earlier for a good price, achieving financial freedom. According to plan, he originally intended to immediately start a new company and continue developing innovative medical devices. However, when it came to selecting specific products, this angel investor failed to find an opportunity worth fighting for.

A Clinician by Background, He Has a Strong Sense of Professional Boundaries. In His View, Everyone Should Recognize Their Place in the Industry Chain: "Some Opportunities May Seem Great, but If You Can't Make Them Work Yourself, It's Better to Invest and Let Others Do It." After Selling His Company, He Sporadically Invested in Some Angel Round Projects Using His Own Funds.

In 2013, when a domestic investment institution planned to set up a fund focusing on healthcare investment, he joined the team as a venture partner, starting his career as an angel investor. In the third year of becoming a professional angel investor, he met the team that he would later co-found a startup with, and immediately jumped into the fray, becoming an entrepreneur once again.

Bao Yanghuan, who came from Cold Spring Harbor Laboratory in the United States, also went through a very similar process of entrepreneurship, investment, and then returning to entrepreneurship. In 2009, Bao Yanghuan joined a laboratory at Cold Spring Harbor Laboratory that focused on researching central nervous system (CNS) diseases as the first member of the lab team. He participated in the process of transforming the lab’s scientific research results into a startup company. This company later provided services to many CNS drug development companies worldwide and advanced its own CNS drug pipeline into clinical trials.

So when Bao Yanghuan returned to China in 2012 to seek new career opportunities, one of the key areas he considered was innovation and entrepreneurship in the CNS and brain science fields. However, at that time, China's new drug R&D ecosystem struggled to provide the necessary support, making his plans seem like a mirage. As an angel investor, Bao Yanghuan is steady, professional, and has an outstanding track record.

In 2019, Bao Yanghuan noticed that as several foreign CNS new drug research and development companies successively revealed excellent clinical trial data, the investment in brain science basic research over the past decade began to yield results. Both the industry and investment circles in China started to pay attention to CNS and brain science, which made him very excited. Bao Yanghuan admitted that before making the decision to pursue full-time entrepreneurship, he had been waiting for this opportunity for 10 years and happened to meet suitable scientific and technical co-founders.

Born in the 1960s, Zhao Chunlin's career experience is slightly more complex than the previous two angel investors, but the life trajectories of the three intersect at the crossroads of angel investors and entrepreneurs.

Zhao Chunlin was among the first batch of university students after the reform and opening up, and also one of the earliest group of people who became wealthy through the power of knowledge. In 2010, Zhao Chunlin fully transferred the scientific research equipment trading company he founded to a Taiwanese-funded enterprise. Achieving financial freedom at over 40 years old, Zhao Chunlin was one of the fortunate trailblazers of his time. He told VCBeat that the field of venture capital was very mysterious at the time, which immediately attracted him.

In 2010, Guoke Jiahé, a venture capital firm that had invested in many high-quality internet projects, attempted to establish a healthcare fund. At the time, professional healthcare investment talent was extremely scarce in China. Although Zhao Chunlin had no prior experience in investment, his past background in scientific research, business, entrepreneurship, and large corporations made him one of the few individuals capable of understanding innovative healthcare projects. In early 2011, Zhao Chunlin joined Guoke Jiahé to lead the healthcare investment team. However, he left behind many regrets at Guoke Jiahé. The team's background in internet investments made it difficult for new drug development projects, which have very long payback periods, to gain approval from the investment committee—almost all were rejected.

In 2014, Zhao Chunlin joined C-Bridge Capital, which focuses on medical investments, and became colleagues with a group of like-minded investors. He invested in Innovent Biologics, Ascletis Pharma, Berry Genomics, and Beirui Health. It was just the right time for innovative drugs to take off. "It seemed that every investment we made eventually succeeded," Zhao Chunlin joked. "Founders create opportunities, investors seize them, and whether the industry succeeds or not mainly depends on market trends." The sense of accomplishment from being an investor made Zhao Chunlin feel comfortable. With the support of Guoke Jiahe, he established Anlong Fund, adopting an "80% focus on people, 20% on technology" approach. As an angel investor, Zhao Chunlin doesn’t even need to step out of his comfort zone to continue enjoying fame and fortune.

In 2019, Zhao Chunlin seemed to have seen the ceiling of himself as an angel investor. He told VCBeat that angel investors grow together with the founding team, but regrettably, if they choose not to detach from the industry, angel investors cannot accompany the company for too long—"the company grows, but the fund remains stagnant."

Perhaps angel investors are inherently entrepreneurs. But when they actually step into entrepreneurship, the microscopic differences between startups and angel investing are qualitative.

First, angel investment emphasizes risk diversification, while entrepreneurship requires the courage to go all-in and walk a single path to the end., which corresponds to the completely different underlying logic of entrepreneurship and investment. For angel investors, the most basic principle is not to put all eggs in one basket. Within a certain period, what angel investors need to do is to ensure that a few projects will eventually yield substantial returns. Betting entirely on any single project will increase risks, as the success of only a few projects can offset the losses caused by the majority of projects failing. An angel investor told VCBeat that as an investor, you need to look at and discuss at least a hundred projects in a year, but the projects you actually invest in will probably not exceed five, sometimes even none at all, "This is a manifestation of the rigor in an investor's work."

But running a company requires going all-in to seek results, concentrating the entire team's strengths and energy to break through every link from technology to product, and then to the market. Bao Yanghuan emphasized that the determination to go ALL IN is a crucial factor in the success or failure of a company in its early stages. During the entrepreneurial process, no matter what setbacks and challenges the core team encounters, they must remain resolute in keeping the company moving forward. If there’s always a backup plan, product development will stagnate; if difficulties aren’t met with full effort to resolve them, it’s easy to fall into a death spiral—team attrition, inability to secure financing, and ultimately, the company won't succeed.

Secondly, angel investment is about planning, selecting, and replanning, while entrepreneurship is about practicing, reflecting, and practicing again."They are different aspects of the same thing, testing different abilities. We see many investors with industry experience who hope to use their experience to help invested companies solve problems and always give a lot of advice. Their intentions are good, but this advice is often difficult to implement." An angel investor who has also ventured into entrepreneurship stated that in the practice of starting a business, the relationship between the founder and the investor is like that of a driver and a passenger in the co-pilot seat. "Sometimes the investor may just be a pedestrian on the roadside." Many details in the establishment and operation of a business are best understood by the entrepreneurs themselves, and their judgment based on sufficient information often surpasses the advice given by investors based on past experience.

In this sense, investors may have met countless people, but if they haven’t personally tried it, they still don’t understand entrepreneurship. The challenges they face are no less than those of ordinary entrepreneurs. As one of the entrepreneurs mentioned earlier said, the various small obstacles and major issues on the entrepreneurial journey persist from start to finish. From the moment they decide to start a business, founders are constantly making decisions—where to save, where to spend, when to rush, and when to wait. There are many details, yet they often determine life or death. "Once many decisions are made, they may lead to gains or losses among different teams. At this point, the founder needs to strike a balance to ensure that the teams continue to work together seamlessly," he pointed out.

Third, whether it is entrepreneurship or angel investment, it is a splash raised by the tide of the times. Under different historical contexts, opportunities and risks vary."In the past, many unmet needs in the medical industry could be transformed into entrepreneurial opportunities. But as competition becomes increasingly fierce and room for error has significantly diminished, entrepreneurs without strong core capabilities will hardly succeed," analyzed an angel investor.

Generally, when analyzing the potential of innovative projects, factors such as technological maturity, technological barriers, and potential market space are considered comprehensively. Previously, significant unmet clinical needs offered considerable potential, which meant the market did not focus excessively on technological maturity or barriers. However, with the continuous emergence of innovative products, the technological and functional attributes of the products themselves have become increasingly critical to the success or failure of ventures.

This means that top angel investors who enter the field will find it difficult to replicate their past successes of betting on the racetrack and coaching from the sidelines during their own entrepreneurial journey. "You must work within an industry you're familiar with, otherwise the risks will be significant," emphasized Bao Yanghuan. Another angel investor who has entered the field also noted that although many experiences in clinical and medical areas are transferable, one should not easily venture into completely unfamiliar territory.

"Starting a business alone definitely won't work; no matter how strong an individual's ability is, it's not enough to build up a company." Almost every angel investor interviewed by VCBeat emphasized the value of the team.

Undoubtedly, people are the most crucial factor in entrepreneurship. As angel investors who actively participate in startups, they have broader channels to access talent. Generally speaking, a company needs three types of talents: research-oriented, industry-oriented, and business-oriented. Typically, for entrepreneurs with a research background, such as professors or scientists, finding research talent is relatively easy. For example, those professors from Tsinghua University or Peking University who venture into entrepreneurship often already have top-tier research talent within their teams, enabling them to quickly complete recruitment. However, they face more challenges when building an industrialization team. On the other hand, entrepreneurs with an industry background excel in this area—such as senior executives from multinational corporations in Shanghai's Zhangjiang Park who transition into entrepreneurship. They can swiftly assemble the necessary industry talent from familiar pharmaceutical or medical device companies. In the earliest stages of entrepreneurship, the ability to quickly form a stable research and industry team is key to whether a new enterprise can grow steadily. The social resource networks that angel investors have built through their extensive investment and incubation experiences can precisely address the shortcomings of research-focused or industry-focused entrepreneurs in team recruitment.

Bao Yanghuan admitted that as a senior angel investor, he has slightly more convenience than ordinary first-time entrepreneurs when looking for various external partners. One day before the Spring Festival in 2023, Bao Yanghuan gave an exclusive interview published on VCBeat, officially announcing for the first time his establishment of ProBest Bio.

In the past, most companies would choose to make their first media debut after completing angel round financing to avoid having their innovative businesses copied by competitors. Bao Yanghuan firmly believes that high-difficulty and high-barrier innovations cannot be easily replicated, and he wants to use public statements to convey the logic of his entrepreneurship to potential partners. Bao Yanghuan received encouragement and support from a large group of friends, many of whom provided him with leads on financing and business cooperation. His personal seed round financing was quickly completed, and this small amount of investment allowed Pubeisi Bio's research and development to kick off more rapidly.

After more than three years of entrepreneurship, Zhao Chunlin has been continuously seeking a team for Anlong. He first identified the direction of his venture: developing gene therapies. Subsequently, he invited Professor Ding Wei from Capital Medical University to lead the team in product development. At that time, Zhao aimed to develop gene drugs using AAV as a vector, targeting macular diseases in ophthalmology. Later, the scope expanded to include diabetic macular edema and venous occlusion. This represents new technology, a large market, suitable for China's national conditions, and fitting for a startup.

He first needed to find experts with research and development experience in the AAV field. After searching around, he selected Professor Ding Wei, who, as the Vice Dean of the School of Basic Medical Sciences at Capital Medical University, has conducted more than 20 years of applied research in the AAV field. Zhao Chunlin was well aware that in this area, Professor Ding Wei could deliver results. Under Professor Ding Wei’s guidance, Anlong, which at the time did not yet have its own R&D team or laboratory, entrusted Kerui Bio, invested in by the Anlong Fund, to design and construct, bringing the product to fruition.

Interestingly, when settling with Carebiomics, the latter refused cash payment and instead opted to hold a portion of Anlong's stock options. "I have great confidence in Carebiomics' technical service capabilities, so I didn't reject this deal," Zhao Chunlin told VCBeat. Subsequently, he also invited a well-known CMC expert in the industry to help build Anlong's CMC team and establish CMC standards for its products.

On February 7, Anlong officially submitted clinical application materials to the CDE. The specific clinical application and clinical trial work are led by Dr. Changdong Liu, who joined Anlong in September last year. Chulin Zhao revealed that in the pre-IND submitted in October last year, the CDE provided positive feedback. Chulin Zhao judged that this formal IND would pass smoothly, and the clinical trial would start in May.

Zha Chunlin told VCBeat that since his early days of studying abroad, he has been an active member among his classmates. While organizing and participating in scientific research community activities, he met many research and industry talents, understanding their strengths, which provided considerable convenience for the team formation of Anlong. However, even so, he still needs to continuously learn and communicate to grasp the most cutting-edge technologies and discover the best talents. After the Spring Festival, offline academic activities suddenly revived, and Zha Chunlin began to shuttle between various forums again. Talking about technology and making friends have become part of his daily routine beyond his work as a founder.

An angel investor told VCBeat that as the funding, talent, and regulatory environment for healthcare innovation in China matures, an increasing number of people are choosing to become serial entrepreneurs. This is undoubtedly an inspiring scenario—successful investors or seasoned entrepreneurs are, at a new turning point in this era, tacitly choosing to set aside past achievements, taking with them invaluable experience to start anew. More exciting journeys lie ahead.