Medical Device Investment Logic Is Quietly Shifting: Insights from Over 700 Financing Events

NeuroXess

Invasive Brain-Computer Interface Developer

KouTech

Developer of Microsurgical Robots

EVAHEART

Cardiovascular Medical Device Developer

The medical device industry is a high-tech industry characterized by multidisciplinary integration, knowledge intensity, and capital intensity. Many people believe that the investment logic in the medical device sector is simply import substitution, but to truly invest well, it is not that straightforward.

Roland Berger, an international management consulting firm, released the "Current Status and Trends of China's Medical Device Industry Development," which shows that the scale of China's medical device market is expected to reach 958.2 billion yuan in 2022, with a compound annual growth rate of approximately 17.5% over the past seven years, making it the world's second-largest market outside the United States.

Such a market, nearing one trillion yuan, presents golden opportunities for China's medical device sector beyond the domestic substitution trend. How can the industry further differentiate itself in the future? Has the logic of investment changed? These are all questions worth pondering. We attempt to find answers by analyzing financing information from the past year.

In June 2022, the Shanghai Stock Exchange released new regulations allowing medical device companies to list on the Sci-Tech Innovation Board under the fifth set of standards, supporting hard-tech medical device companies that have not yet reached a certain scale of revenue to issue and list on the Sci-Tech Innovation Board.

Five years ago, the implementation of Hong Kong Stock Exchange Rule 18A triggered a major boom in the biopharmaceutical sector. Does the issuance of new regulations by the Shanghai Stock Exchange mean that medical devices could take over from biopharmaceuticals to become the new investment hotspot?

In essence, the core selling point of innovative drugs is patents, but medical devices, in addition to patents, also have complex precision manufacturing systems. The research and development process of innovative drugs has relatively clear milestones, while the innovation of medical devices is a spiraling upward process.

Although it is also a race against time, the innovation of medical devices is built upon iterative research and development. After accumulation, patent moats and market share are formed, making the barriers difficult to break. Once a leading position in the medical device industry is established, it is easier to achieve a long-term advantageous position and obtain sustained, stable, and high returns. Compared to innovative drugs, where every company has the opportunity to be first-in-class, the innovation in medical devices offers more stable expectations.

Changes in the primary and secondary markets can also reflect certain trends in the industry.

According to data from VCBeat, in the past year, the number of financing and investment deals for medical devices in the primary market (870) exceeded that of innovative drugs (650). In the secondary market, there were a total of 82 IPO events in the healthcare sector last year, with medical devices ranking first in quantity, accounting for approximately 29%.

Among the medical companies listed last year, the top three in terms of market value are all innovative medical device companies, including United Imaging Healthcare, MGI Tech, and MicroPort Scientific. Similarly, among listed companies with a market value exceeding 10 billion yuan, medical device companies account for the highest proportion (33%).

Taking the financing data first published by VCBeat in the past year as a sample, from January 2022 to February 2023, VCBeat published more than 700 investment and financing information. We attempt to uncover the logic behind institutional investments in medical devices.

High-barrier Hard-tech Medical Robots

Medical robots have, over the past year or so,Over 60 financing events occurred in the primary market, with an amount exceeding 8 billion yuan.。

The emergence of a successful product is inevitably backed by strong market demand. The same holds true for medical devices, whether they are needed by patients or doctors; ultimately, their value is reflected in the treatment process, where commercial returns are also obtained.

Medical robots, represented by surgical robots, serve as an extension of a doctor's hands and eyes, assisting in surgeries where traditional methods fall short. The advent of the da Vinci system has enabled doctors to perform minimally invasive surgeries with precision control of surgical instruments surpassing human capability. Consequently, surgical robots are predominantly utilized in high-risk, complex, and difficult third- and fourth-level surgeries.

The essence of surgical robots is to assist physicians in performing surgeries and provide support to doctors, and they cannot replace doctors in the short term. Following this logic, surgical robots must develop towards tackling more indications. The development of the da Vinci system is precisely a process of continuously fulfilling the ability to expand indications. Combined with the business model of equipment + consumables + services, its commercial value can be fully realized.

According to VCBeat's data, the surgical robot sector completed 45 financings in 2022, 20 of which occurred prior to Series A, with a total amount of approximately $815 million. After experiencing a financing boom in 2021, the fact that surgical robots still possess such strong fundraising capabilities is sufficient proof of their appeal.

Some institutions have invested in surgical robots multiple times, data sourced from VCBeat.

Notably, four institutions have made multiple investments within a year. Among them, Shenzhen Capital Group and Vivo Capital favor companies with products already on the market, while TF Capital and Oriental Jiahua focus primarily on early-stage projects. TF Capital invested twice in KouTech within a short span of three months. The company also received exclusive investment from Temasek in January 2023.

KouTech Focuses on Microsurgical Robots, the Most Precise Surgical Robot Category Globally. Microsurgery typically involves anastomosing lymphatic vessels-blood vessels or nerves with diameters of 0.3-0.8 millimeters and has significant unmet needs across multiple departments such as otolaryngology, lymphatic surgery, neurosurgery, and plastic surgery. Compared to da Vinci's dominance in the endoscopic field, microsurgical robots represent a brand-new track.

Apart from the da Vinci, the remaining products are basically in the clinical introduction stage. Last year, 15 domestically produced surgical robots were approved for marketing, showing a trend of catching up.

An investor told VCBeat: "Although we are optimistic about surgical robots, it is becoming increasingly difficult to find suitable targets, as some niche areas have already formed stable competitive landscapes. In such high-tech barrier industries, companies need strong comprehensive capabilities to break through. Despite the huge market potential, it requires a longer cycle and continuous capital investment."

Artificial Organs with Continuous Investment from Top Capital

Artificial Organs in the Past YearNearly 40 Financing Events in the Primary Market, Amount Exceeding 5 Billion。

Taking intraocular lenses, the most well-known example to the public, they are currently one of the largest-used artificial organs and implantable medical device products in the world. Leading manufacturers Alcon, Johnson & Johnson, Bausch + Lomb, and Zeiss occupy nearly 70% of the global market share. Domestic companies in China are increasing investment and accelerating progress, but there is still a significant gap compared to the leading manufacturers.

However, financing events for intraocular lenses account for only 5% of the artificial organs sector, while artificial hearts and artificial heart valves make up nearly half of the sector (about 45%). The remaining financing shares are occupied by artificial joints, artificial livers, artificial pancreas, and artificial lungs. For a long time, heart transplantation has been the most effective treatment for end-stage heart failure, but due to the scarcity of donors, in recent years, the industry has turned its attention to artificial hearts. As a complex and sophisticated medical device, the artificial heart is also hailed as "the jewel in the crown of medical devices."

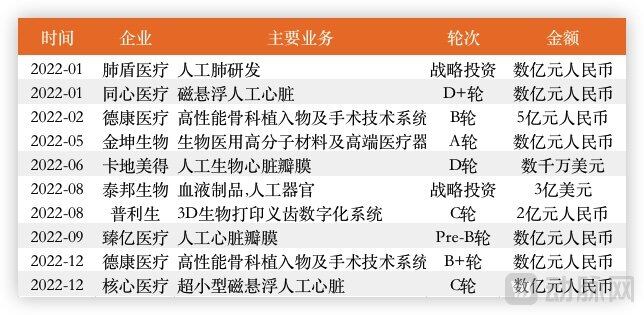

High Financing Amount Events in the Primary Market of Artificial Organs, Data from VCBeat

Artificial hearts can be classified by implantation method into surgical and interventional types. By function, they can be divided into ventricular assist devices (VAD) and total artificial hearts (TAH). Comparatively, the ventricular assist device is currently the most widely used artificial heart system in clinical applications. Based on the type of assistance provided, these devices can further be categorized into left ventricular assist devices (LVAD), right ventricular assist devices (RVAD), and biventricular assist devices (BiVAD).

Among them, the left ventricular assist device (LVAD) is a relatively focused细分领域, including companies such as CH Biomedical, Core Medical, and EVAHEART, all of which have made布局. In terms of investment institutions, these years...Including Sequoia, DCHVGC, Qianji Capital, PICC Capital, Hillhouse Ventures, and Qiming Ventures, among other star investment institutions, have already entered the market.。

With the intensification of population aging, the number of patients with end-stage heart disease continues to increase. According to the latest results of the epidemiological survey of heart failure in China, there are approximately 13.7 million heart failure patients in China. For a long time, clinical interventions for heart failure have been very limited, mainly relying on drug treatment. Due to high technical barriers, imported brand device products are priced at over a million yuan, leaving only a few patients able to afford them.

From a commercial perspective, artificial hearts require significant investment and face extremely high technical barriers. Behind artificial hearts lies one of the few billion-dollar tracks in the cardiovascular field, with heart failure being the final battleground in this domain. Over the years, clinical doctors have made progress in the treatment of almost all types of heart diseases, but heart failure remains an exception.

There are approximately 1.3 million end-stage heart failure patients in China. As an alternative to heart transplantation, artificial hearts overcome the limitation of the number of available heart donors. They can not only provide transitional treatment before heart transplantation or restore heart function but also offer lifelong long-term therapy, showing vast market potential. Abiomed, which was recently acquired by Johnson & Johnson for $16.6 billion, achieved the remarkable feat of surpassing $1 billion in annual revenue and a tenfold increase in stock price over a decade through its interventional artificial heart technology.

On the other hand, as a technological highland in the cardiovascular device field, artificial heart surgery has attracted widespread attention from doctors. Dozens of hospitals across more than ten provinces and municipalities in China have carried out this surgery, and companies are also conducting related academic promotion activities. Overall, the future development potential in the artificial heart sector is enormous, with extremely high technical barriers. As products mature and costs decrease, the arrival of a new era for artificial hearts is on the horizon.

From Science Fiction to Reality: Brain-Computer Interfaces

With the entry of Musk, who brings his own traffic spotlight, the frontier field of brain-computer interface has been brought to the public eye.

Although the number of investment and financing events was not as high as in 2021,The total financing amount still reached nearly 3 billion yuan.. With the involvement of top VC firms like Sequoia Capital and Legend Capital, brain-computer interface has become the "technological hotspot" in medical devices in 2022.

Sequoia Completes Comprehensive Brain Science Industry Layout, with Investment Coverage in Brain-Computer Interface, Neurology Specialty Hospitals, Neuropharmaceuticals, and Digital Imaging. NeuroXess, founded in October 2021, is one of the largest recipients of early-stage financing in China’s brain-computer interface sector, securing two rounds of investment from Sequoia in early and late 2022.

Some early investments in the brain-computer interface field, data sourced from VCBeat

In 2022, the financing rounds of brain-computer interface enterprises in China were all at Series A or earlier, indicating that the entire brain-computer interface industry in China is still in its early stages. Although the financing rounds are early, the amount of each financing deal reached tens of millions or even hundreds of millions of RMB, showing that investment institutions are optimistic about the future of this industry and are willing to make significant bets in its early stages.

Although still in the early stages, the technological pathway has already been validated in theoretical research. Currently, a relatively clear application scenario for brain-computer interface technology is deep brain stimulation (DBS), which has already been applied clinically in the treatment of Parkinson's disease. Additionally, it shows promising potential in addressing drug addiction and obsessive-compulsive disorder. This technology can form a complete closed loop in terms of its mechanism of action, which is precisely the direction that investment institutions hope to see developed.

In 2022, the main recipients of funding were implantable brain-computer interface companies, with investment institutions increasingly valuing the future development of such products. Implantable brain-computer interface products have minimal signal attenuation, high signal-to-noise ratio, and high spatial resolution, making them more suitable for treating or rehabilitating major diseases such as ALS, high-level paralysis, and Parkinson's disease.

As one of the most important strategic disciplines in the coming decades, brain science is bound to bring tremendous translational opportunities based on breakthroughs in fundamental science, benefiting a large number of patients with neurological diseases in the medical field first. Brain-computer interface is a complex integrated engineering project that requires capabilities to cover both scientific and engineering innovations. The financial support from investment institutions will inject new momentum into China's brain-computer interface sector, and the industry’s prosperity is expected to continue.

Summary

Overall, the medical device tracks favored by capital in the past year share the following commonalities: first, they have substantial clinical value; second, they involve the domestic substitution of high-tech-threshold products; and third, they represent genuine innovation in the direction of medical-engineering integration. An investor told VCBeat: "Investment in medical devices has entered the second half, which requires reliance on more hardcore technology. Innovation is no longer just about application-level innovation but must extend to fundamental research innovation. At the same time, the requirements for entrepreneurial teams will be higher—apart from professional capabilities, commercial implementation ability and market transformation capability are also essential."

From a technical perspective, medical devices are prone to cross-integration with multiple industries, including electronic technology, computer technology, materials, and machinery. The minimally invasive, interventional, intelligent, and digital development of medical devices relies on the continuous updating and iteration of foundational technologies from other industries. Combined with healthcare needs, including those of patients and clinicians, new niche markets can be explored by integrating market demands, new technologies, and clinical applications.

From the perspective of domestic substitution, it is not just the end products being replaced; upstream components and materials also present investment opportunities. The mid-to-low-end market for devices already has a relatively high market share, and future opportunities may be more reflected in the high-end market. However, the development of medical devices from the mid-level to the high-end will be challenging, requiring substantial and continuous capital investment, attracting top-tier talent for true innovation, and needing a long time to yield results. For investors, this is not necessarily a bad thing—longer cycles indicate long-term opportunities.

As of the end of 2021, more than 300 medical devices had entered the national innovative device approval process, and in 2022, 53 innovative medical devices were approved, reaching a record high. Although innovative medical devices are temporarily not included in centralized procurement, as the payer, entering the procurement process is still beneficial for enterprises.

In fact, for centralized procurement, medical device companies cannot avoid it. In 2020, the centralized procurement of coronary stents saw a "below-ankle discount," with the lowest bid price dropping by up to 96%. While being stunned by the drastic cut, companies did not forget how to save themselves. Take Lepu as an example; its coronary stents entered thousands of hospitals across China through centralized procurement, while also promoting products like drug-coated balloons. As revenue from traditional metal drug-eluting stents significantly declined, the revenue from Lepu's innovative interventional product portfolio (including biodegradable stents, cutting balloons, and drug-coated balloons) surged over 800%.

For medical device companies, innovation cannot avoid the storm of centralized procurement, but innovation can ensure the continuous development of new products. With innovative products, companies can maintain strategic stability amidst the impact of centralized procurement, making the price-cutting rhythm of procurement unable to keep up with the pace of product innovation. In the past, innovation in medical devices was more about application innovation, but now some companies have extended their innovation to fundamental research. The direct impact is that the implementation of cutting-edge technologies will become more defined, and the developed products will possess higher technological barriers. Companies with such hardcore innovation capabilities are also more likely to be favored by investment institutions. The development of the medical device industry requires the joint efforts of investment institutions, enterprises, and clinical practitioners.