Cardiac Surgery: A Former 'No-Go Zone' Emerges as a Hot Investment Frontier with Over RMB 2 Billion Raised and Strategic Moves by Mindray and Yuanda

BrioHealth Solutions

Ventricular Assist Device Developer and Manufacturer

BIODALS

Implantable Medical Device Developer and Manufacturer

Mindray

Medical Device R&D Manufacturer

Cardiac surgery, once a surgical no-go zone, is becoming an investment hotspot.

In a science fiction novel, a married couple of doctors return to Earth after living on Mars for 20 years. The husband is a cardiac surgeon, and the wife is a cardiologist. Upon returning to Earth, the wife undergoes retraining in medical knowledge, while the husband discovers that very little has changed in cardiac surgery—coronary artery bypass surgery has hardly evolved in 20 years, allowing him to start operating immediately.

Compared with the rapid iteration of innovative products in cardiology and the increasing popularity of surgeries, cardiac surgery is synonymous with difficulty and challenge. From 2012 to 2017, the number of hospitals in China performing cardiac surgeries had been declining year by year.

But in the past few years, under the influence of the pandemic and centralized procurement, the development of cardiac surgery has been accelerated and switched to a booming track. The most intuitive manifestation is in the number of surgeries. In the past few years, despite the overall reduction in surgeries in China due to the COVID-19 pandemic, the number of cardiac surgeries still achieved rapid growth. Among them, the growth rate of coronary artery bypass surgeries exceeded 44%, and major vascular surgeries also showed exponential growth.

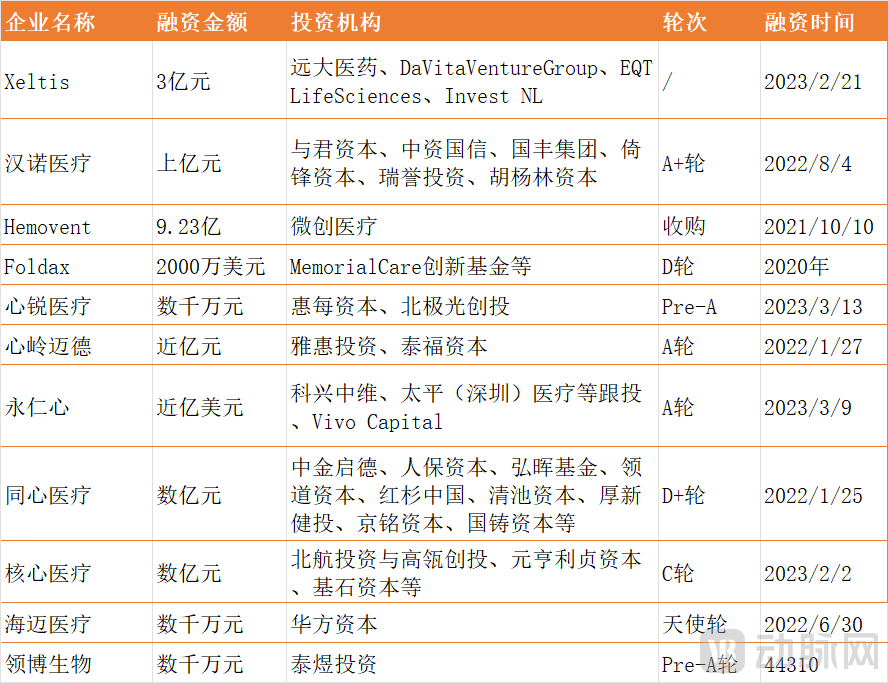

In the primary market, the investment landscape once dominated by interventional products has also started to see a rise in cardiothoracic surgical consumables and devices. Multiple companies targeting clinical needs in cardiac surgery have secured funding, with products such as ECMO, ventricular assist devices, surgical polymer heart valves, and coronary artery bypass blood flow meters gaining attention. VCBeat statistics show that the total financing amount for related companies has exceeded 2 billion yuan.

Cardiovascular Surgery Related Enterprise Financing Events

Cardiac surgery is known for its high difficulty, and doctors in China who can perform complex cardiac surgeries are scarce. Why has the volume of highly complex cardiac surgeries experienced rapid growth over the past few years? Are there innovative products in the cardiac surgery field that have gained attention? What is the outlook for these bottleneck products? VCBeat (WeChat ID: vcbeat) conducted research.

Cardiovascular diseases rank as the leading cause of death among urban and rural residents in China. Surgical treatments for cardiovascular diseases can be divided into surgical operations and interventional procedures. Among these, cardiac surgery focuses on trauma to the heart and major blood vessels, pericardial diseases, congenital heart disease, acquired heart valve diseases, ischemic heart disease, heart tumors, major vascular diseases, interventional treatment techniques, surgical treatment of arrhythmias, pacemakers and implantable cardioverter-defibrillators, dynamic cardiomyoplasty, and heart, lung, and heart-lung transplantation. Meanwhile, the treatment in cardiology is mainly based on interventional therapy.

Generally speaking, the difficulty of cardiac surgery is higher than that of cardiology. Due to the high difficulty, fewer hospitals can perform such surgeries, and the volume of cardiac surgeries is concentrated in leading centers.The total number of cardiac surgeries in China has remained around 200,000 cases, and some types of surgeries have even seen a decline. Meanwhile, the number of PCI procedures alone in cardiology has reached millions.

In the past two years, the volume of cardiac surgery has begun to grow rapidly.According to statistics, the number of cardiac surgeries in China reached 270,000 cases in 2021. Surgeries that showed rapid growth included major vascular surgeries and coronary artery bypass grafting (CABG). Taking CABG as an example, the number of CABG surgeries in China used to be around 50,000 annually but increased to approximately 65,000 in 2021. Last year, the number reached 100,000, nearly doubling the previous figure!

What Factors Drive the Growth of Cardiac Surgery Volume?

The most easily conceivable reason is the bulk procurement of stents and balloons in the interventional treatment field.Volume-based procurement has reduced the profit margins of interventional treatment products, addressed the issue of over-intervention, and allowed more patients to return to cardiac surgical procedures.

"But the bulk procurement is only a secondary reason," Yu Wenyuan, founder of Yuewei Medical and former practitioner at Anzhen Hospital, told VCBeat.The most fundamental reason for the growth of cardiac surgery is that the COVID-19 pandemic has forced local hospitals to enhance their cardiac surgical treatment capabilities."Some third-tier city hospitals have an annual surgery volume that has already surpassed that of Anzhen Hospital, a major leading center."

Yu Wenyuan stated: "Cardiac surgery is a high-threshold department. Its high threshold is reflected in two aspects: one is the requirement for surgeons' operational skills, and the other is the requirement for the hospital's comprehensive capabilities."

For example, if a hospital wants to develop cardiac surgery, it first needs to have an excellent cardiology department; it also requires an outstanding critical care team because patients undergoing heart surgery generally need to be admitted to the ICU for monitoring and postoperative management. The development of cardiac surgery demands high standards from medical staff in departments such as anesthesiology, cardiopulmonary bypass, nursing, and the ICU.

Because of its high difficulty, the success of cardiac surgery is often seen as a reflection of the medical standards in a region.

High barriers lead to a scarcity of hospitals in China capable of performing complex cardiac surgeries.Cardiac surgery is often concentrated in a few major advanced centers in China. In the past, the solution to this imbalance was "flying surgeons." However, the pandemic made this model difficult to sustain, and the overwhelming demand from heart disease patients has driven local hospitals to improve their treatment capabilities, providing more training opportunities for local doctors.

Yu Wenyuan pointed out: "Therefore,The growth in cardiac surgery volume over the past two years has mainly come from local hospitals. However, leading centers such as Anzhen and Fuwai have not seen significant growth in surgical volume.”

In the past, the main reason restricting the increase in the number of cardiac surgeries in China was the shortage of experienced doctors. In cardiac surgery, it often takes a decade to train a qualified cardiac surgeon. The slow path to becoming proficient in cardiac surgery, combined with the demanding workload, has led many young doctors to avoid choosing this field. The insufficient reserve of new talent is also an important factor limiting the development of cardiac surgery.

The growth in the past two years has been a rapid compensation for the previous shortage of cardiac surgeons in China.

The lack of sufficient doctors has led to a lower penetration rate of cardiac surgery in China.. Taking coronary artery bypass grafting (CABG) as an example, the base number of patients in China who need to undergo CABG each year is 3 to 4 million, with an annual increase of 300,000 to 400,000 patients. However, currently, only 100,000 CABG procedures are performed annually in China. Comparing the penetration rates of such surgeries between China and the U.S., there is significant room for improvement in the penetration rate of cardiac surgical treatments in China.

The United States performs about 300,000 coronary artery bypass surgeries annually for a population of 300 million, while in China, with a population of 1.4 billion, only 100,000 such surgeries are performed each year.

As the capability of cardiac surgery treatment in China expands from leading central hospitals to local hospitals, the penetration rate of cardiac surgery diagnosis and treatment in China is expected to accelerate.

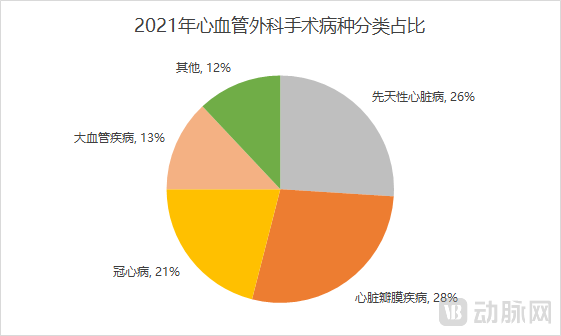

Cardiac surgery mainly includes surgeries for congenital heart disease treatment, heart valve disease treatment, coronary artery bypass grafting, large vessel diseases, and other conditions. Among these surgeries, which ones have experienced rapid growth in the past two years? What are the development trends for products in these areas?

Data source: 2021 Cardiovascular Surgery and Extracorporeal Circulation Data

The fastest-growing surgery in cardiac surgery is coronary artery bypass grafting.Coronary artery bypass grafting and stent implantation are currently the two most common methods for treating coronary heart disease and acute myocardial infarction. Compared with coronary stents, coronary artery bypass surgery can address triple-vessel disease, severe left main stem lesions, and cases where stent surgery has failed.

The consumables used in coronary artery bypass surgery mainly include surgical sutures, heart stabilizers, coronary artery bypass blood flow meters, vascular anastomosis devices, and other products.

The number of coronary artery bypass surgeries in China has been on the rise, with a previous growth rate of 5%. Although the growth rate surged after the centralized procurement, the penetration rate of coronary artery bypass surgery in China is still at a relatively low level compared to the United States and will continue to grow in the future.

Surgery for large vessel diseases is also among the faster-growing procedures in cardiac surgery.Large vessel diseases mainly refer to aortic diseases, which are divided into stenotic and dilated types. The growth rate of surgeries for large vessel diseases has been particularly prominent, with a surgery volume increase reaching 25% in 2021.

The increase in major vascular surgeries is due to a rise in incidence on one hand, and on the other hand, the extreme difficulty of such surgeries meant that fewer hospitals were able to perform them in the past, resulting in a higher concentration of procedures at leading centers. The majority of aortic surgeries in China are performed in major hospitals in Beijing, Wuhan, and Shanghai.

Under the impact of the COVID-19 pandemic, both the channels for patients to seek medical treatment across provinces and for doctors to perform "flying knife" surgeries have been restricted, forcing local hospitals in China to enhance their treatment capabilities. After the treatment capabilities of local hospitals improved, there was a significant increase in the number of major vascular surgeries.

The main consumables used in aortic disease surgeries are artificial blood vessels, which are primarily utilized for the replacement or bypass surgery of the aorta and its branch vessels.

The disease with the largest share of surgical volume in the cardiac surgery market is valvular disease.The main medical device products used for valvular diseases are artificial valves, which can be divided into interventional valves and surgical valves. Interventional valves have been approved in China for a relatively short period and are still in the early stages of development, with the annual number of surgeries in China exceeding 15,000.

Even with the rapid penetration of interventional valves, surgical valves still have a certain market space. Surgical valves still hold advantages in younger patients and those with multi-valve disease. Looking at the 20-year data from Europe and the U.S. on the development of TAVR (Transcatheter Aortic Valve Replacement), the volume of SAVR (Surgical Aortic Valve Replacement) procedures has not decreased but has continued to increase.

It is foreseeable that in the future of China's cardiovascular surgery market, surgical valve procedures will continue to grow. In the field of surgical valves, several products from Chinese manufacturers have already been approved, but Edwards Lifesciences remains dominant. Edwards' surgical valve products hold the largest market share and are also the most highly regarded in terms of market evaluation.

The market landscape in the surgical valve field is expected to be disrupted by a new generation of polymer valve products.After decades of development in the field of surgical valves, two major types of products have emerged: mechanical valves and biological valves. However, both types still face two major issues that need to be resolved: valve degeneration and anticoagulation. Valves based on polymer materials combine the advantages of both mechanical and biological valves, offering excellent fatigue resistance as well as superior blood compatibility.

Foldax, a globally leading polymer valve company, has completed its Series D financing. Its main polymer valve, the Tria surgical polymer valve, is currently in the clinical trial stage, and its transcatheter polymer valve has completed animal experiments. In China, two companies, MedPrae and Xinrui Medical, are also developing polymer surgical valve products.

Diseases with a relatively high proportion of surgical volume also include congenital heart disease.The proportion of adults undergoing surgery for congenital heart disease (CHD) in China is relatively high, reaching 41.4%. In terms of future growth, the share of CHD surgical procedures has been on a declining trend for eight consecutive years. With the continued decrease in birth rates and the improvement and popularization of CHD screening methods, the total number of CHD patients will continue to decline.

The main consumables used in the surgical treatment of congenital heart disease include surgical patches and surgical sutures. Cardiac patches are used in cardiac surgeries to repair atrial and ventricular septal defects caused by various factors. Currently, the major companies in China's cardiac patch field include Biodals, Gore, and Shanghai Chiest Medical.

There are other highly challenging surgeries in cardiac surgery, and a low volume of surgeries does not equate to low importance—every type of surgery needs to be mastered by doctors. Cardiac surgery is a peak of difficulty in surgical medicine, but the fact that it involves numerous critical illnesses means this peak must be climbed.

Highly complex cardiac surgeries demand advanced instruments. The COVID-19 pandemic exposed a significant gap in China’s domestic production of several critical products used in cardiac surgeries. The high cost of cardiac surgical instruments often results in limited stock kept by doctors. During the pandemic, shortages of products like artificial blood vessels and ECMO drew widespread attention due to supply disruptions.

Which products are still being held back in the complex cardiothoracic surgery market?

First is ECMO (Extracorporeal Membrane Oxygenation)ECMO, also known as "artificial heart and lung," revealed the gap in China's ECMO industry during the COVID-19 pandemic. In the past three years, domestic companies have accelerated the localization process through acquisitions and independent research and development.

Currently, domestically produced ECMO devices from companies such as Seton Medical, Aerospace Changzheng, and Hanno Medical have already entered the market. Although ECMO technology has faced bottlenecks, the gaps were filled during the COVID-19 pandemic, and now the configuration of ECMO devices in first-tier hospitals in China is almost saturated.

At the end of 2018, statistical data provided by the Extracorporeal Circulation Branch of the Chinese Society of Biomedical Engineering showed that China had about 500 ECMO machines. By the end of 2022, according to data released by the National Health Commission, the number of Extracorporeal Membrane Oxygenation (ECMO) machines in China had reached more than 2,600.

Although domestically produced ECMO products have been approved, Chinese companies still lack core technologies. For key components of ECMO oxygenators, such as membrane lungs, there is still a gap compared to global brands.

The second most constrained product is polypropylene suture, which is widely recognized as the preferred suture in cardiovascular surgery.Polypropylene surgical sutures are monofilament synthetic sutures, with the advantage of maintaining permanent tensile strength after being implanted in tissue (lasting up to 2 years), smooth handling, easy knotting, minimal tissue drag, and providing secure knot assurance.

In coronary artery bypass surgery, there are also bottleneck products, such as the coronary artery bypass blood flow meter. Currently, the only product on the market with verified accuracy is produced by the Norwegian company Medistim.

In traditional surgical procedures, doctors rely solely on the sense of touch with their fingers to assess a patient's pulse and blood flow conditions during surgery and before closing the chest cavity, which greatly depends on the surgeon’s personal experience. The application of Medistim products during surgery makes it possible to quantify and assist doctors in more accurately confirming the patient’s condition, thereby reducing the rate of surgical failure.

Medistim's single device price is as high as 2 million yuan, and a single consumable probe costs 20,000 yuan. Currently, Yovemed, a Chinese company, has started developing this product.

In major vascular surgeries, the product that is often a bottleneck is artificial blood vessels. Currently, the brand with a higher market share in China's artificial blood vessel sector is Maquet. Among domestically produced artificial blood vessels, products from BIODALS have already been put into production.

Globally, there are also innovative artificial blood vessel products emerging, including those under development by Humacyte, Xeltis, and Lymbio.

Cardiovascular surgery is often constrained by products involving core components that require breakthroughs in fundamental technology, such as extracorporeal circulation tubing, artificial blood vessels, and ECMO membrane lungs. These products are often expensive. However, due to high barriers, few companies pay attention to these critical products that affect patients and the industry.

In the future, the domestic substitution of key core technology products will be a major direction for the development of cardiovascular surgical devices. Besides, what other innovative directions are there for cardiovascular surgical products?

Yu Wenyuan believed that there are mainly two directions: the first is to reduce the difficulty of doctors' learning and training.Cardiac surgeons have a significantly longer training period compared to other medical departments. It often takes over 10 years of training for a surgeon to become a chief cardiac surgeon. Even though the pandemic has improved local doctors' treatment capabilities, there is still substantial room for improvement in handling critically ill patients. In terms of meeting the clinical demand gap, the number of cardiac surgeons in China is far from sufficient. Therefore, there is a need for more innovative medical device products in cardiac surgery to reduce the complexity of surgeries and shorten the training period for doctors.

The second major direction is to improve patient safety.Taking Medistim's intraoperative flowmeter as an example, the use of this product in coronary artery bypass surgery can enhance surgical safety.

Currently, cardiac surgery remains a highly challenging procedure, but for medical technology innovation, difficulty often serves as the greatest driving force for technological advancement.

Breakthroughs in high-difficulty surgeries often gain market recognition. For example, percutaneous ventricular assist devices (pVADs) can provide critical hemodynamic support for critically ill patients with cardiogenic shock, high-risk PCI, and low cardiac output during the perioperative period of cardiac surgery. Abiomed's interventional ventricular assist device, Impella, generated over $1 billion in revenue for Abiomed in 2022.

Cardiovascular diseases have a huge unmet clinical demand, leaving ample room for new technologies to make an impact. We look forward to more enterprises in China that integrate medical and engineering innovations bringing additional breakthroughs to the cardiovascular market.

Reference Article:

Jixin Style | Director Lemma's Research on the Future of Coronary Artery Bypass Surgery — Jilin Heart Disease Medical College

Heavyweight | 2021 Cardiovascular Surgery and Extracorporeal Circulation Data Released, Proportion of Heart Valve Surgeries — VCBeat