2023: The Year of NASH? MNCs Step Back as Biotechs Surge Ahead – When Will China Catch Up?

XZenith Biopharm

Researcher and Developer of New Molecular Entity Drugs

Apricot capital

Venture Capital Institution

Madrigal Pharmaceuticals

Developer of Fatty Liver Disease Treatment Drugs

CARGENE BIOPHARMA

Small Nucleic Acid Drug Developer

Since the second half of 2022, there has been a surge of breakthroughs in the NASH field among Biotechs. The most notable results came from Madrigal's Phase III clinical trial, where Resmetirom could potentially become the first approved drug; Intercept resubmitted the NDA for Obeticholic Acid in treating NASH-related liver fibrosis; Akero and Poxel also reported positive progress in their Phase II clinical trials.

Some industry insiders said: after 40 years of R&D black hole, the year for NASH is coming.

However, this is not the first time the industry has anticipated a "NASH year." In the past few years, the NASH field has experienced multiple instances of "false prosperity." In 2018, Goldman Sachs predicted that 2019 would be the "NASH year." But soon after, Gilead, which had heavily invested in NASH, announced that its ASK1 inhibitor selonsertib (GS4997) missed the primary endpoint in its first Phase III clinical trial. Subsequently, unfavorable news about clinical trials in the NASH field kept emerging, and the initial excitement dimmed once again.

But the huge market is still driving the progress of NASH drug research and development. It is expected that by 2026, the value of the NASH market will reach 18.3 billion US dollars. According to incomplete statistics, there are more than 200 NASH new drug projects under research and development globally, of which more than 100 projects are in the clinical development stage.

Among the targets of drugs in the clinical stage, GLP-1R, FXR, and PPAR are the drug targets with the highest number of clinical trial applications, and these targets have already been successfully approved for marketing in other indications such as type 2 diabetes. "Second-generation targets" like THR-beta represented by Madrigal and FGF21 represented by Akero have begun to show outstanding results in recent clinical trials.

First to aim at the NASH field are naturally the MNCs, but compared with the recent string of good news from Biotechs, there comes the news that MNCs are "withdrawing" or semi-shelving the NASH track. Johnson & Johnson and Arrowhead broke up, returning all rights to the RNA interference (RNAi) therapy ARO-PNPLA3 under development to the latter; Novartis is fully withdrawing from the NASH field, saying it will focus on limited therapeutic areas; Merck decided to terminate the Phase IIb study of MK-3655 (NGM313) for the treatment of NASH.

The first drug for NASH is on its way, but the moves by MNCs have raised doubts. Especially in China, some discussions are still focused on disease awareness, including how NASH should be diagnosed, and whether medication is necessary or how drug interventions should be carried out.

In fact, similar discussions and doubts occurred in leading foreign markets a few years ago, which is precisely the time lag in the NASH field, and behind this "gap" lies unmet demand and opportunity waiting to be tapped.

Therefore, VCBeat recently analyzed some representative overseas Biotech companies in the NASH field – some of them have made the most cutting-edge attempts in this field, while others can provide inspiration for pipeline operations (see detailsVCBeat NASH Special), we have summarized the dynamics and characteristics of these companies.Organize,and exchanged views with investors and entrepreneurs in China's NASH field on the current market situation:

Why is Biotech the first to achieve Phase III clinical results? What are the standout qualities of the faster-progressing Biotechs? Which advancements should we focus on this year? Why have some Biotechs that gave up competition failed?

What is the role of MNCs, and will their withdrawal affect confidence in the NASH field?

Is China's NASH Field Entering an Investment Boom?

You are also welcome to scan the QR code at the end of the article to register for the NASH-themed offline salon event co-hosted by VCBeat and the Drug Hunter Club. The event will take place from 15:00-18:00 on Friday, March 31, where we will meet with pioneers in China's NASH field in Shanghai to discuss industry development face-to-face.

Clinical Design, Cash Flow Management, Biotech Crossing the Finish Line Under Heavy Load

Compared to many disease areas, NASH is a field where Biotech performs exceptionally well.

"The development of NASH drugs was initiated by these large pharmaceutical companies. In the early stages, the main targets focused on the downstream of the treatment pathway, and the understanding of NASH was still in exploration, resulting in many early failures," said Dr. JiaKui Li, Vice General Manager of XZenith Biopharm. "As big companies entered the NASH treatment field, many Biotech companies quickly followed suit. Biotech companies explore a wider range of areas and develop more targets, so we can see that Biotech companies have persisted in research and development on one or two pipelines and have achieved results currently."

XZenith Biopharm has two self-developed small molecule drugs for the treatment of NASH currently in clinical research, including the FXR agonist XZP-5610 and the KHK inhibitor XZP-6019. Li Jia-kui previously worked at Roche for 15 years and participated in the development of the predecessor to Madrigal Pharmaceuticals' star product, Resmetirom.

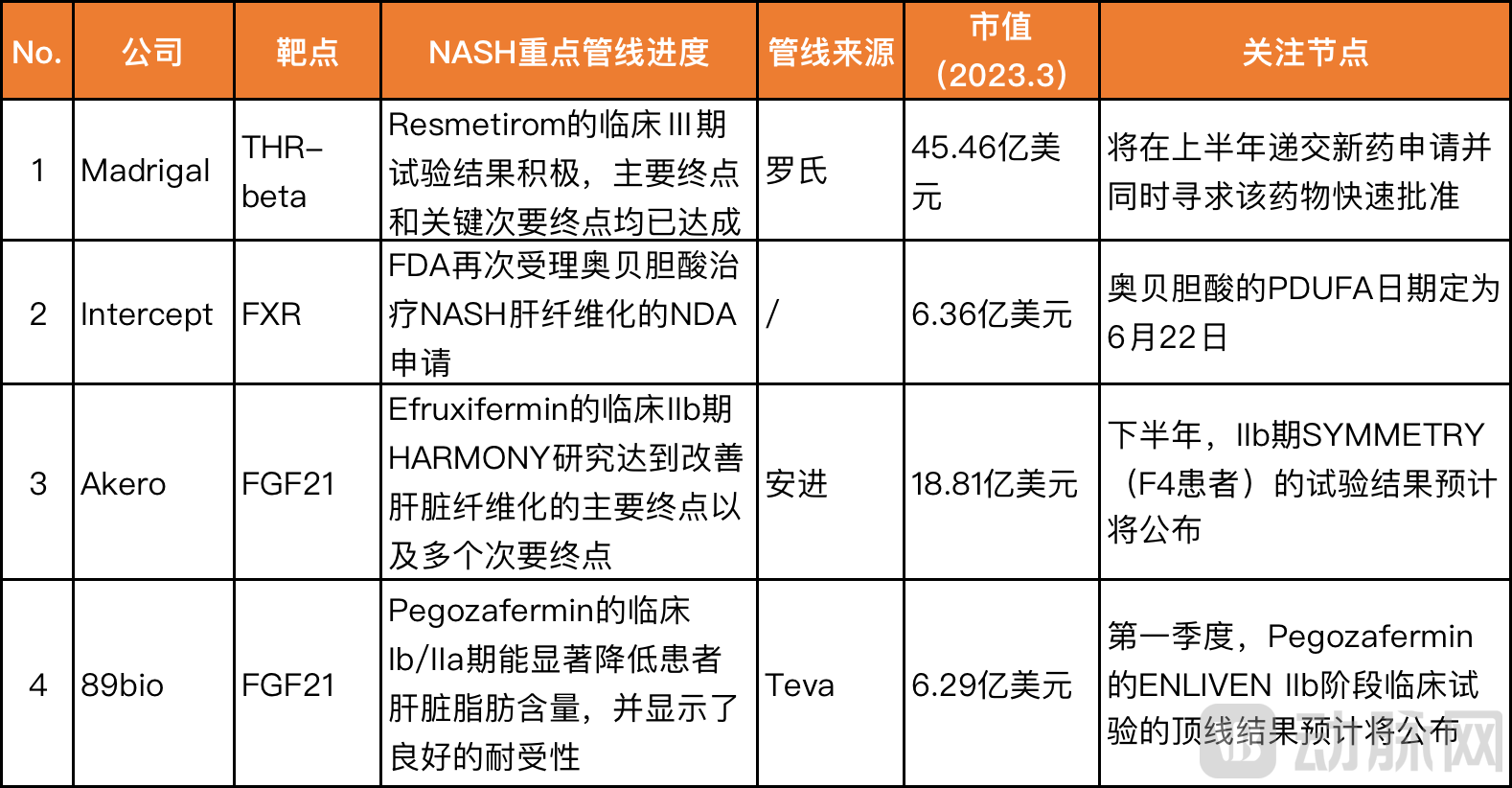

Last December, after the publication of Madrigal's Phase III clinical trial results, its stock price surged significantly. With the growing sentiment surrounding the approval of NASH drugs, many companies in the NASH field experienced a high point in the capital markets. We have compiled information on four overseas NASH biotech companies that are progressing rapidly and are also popular in the market:

The significant progress of these four companies all occurred after 2018, due to changes in the FDA's review standards for NASH drugs. In December 2018 and June 2019, the FDA consecutively issued two draft guidance documents for NASH research and development.

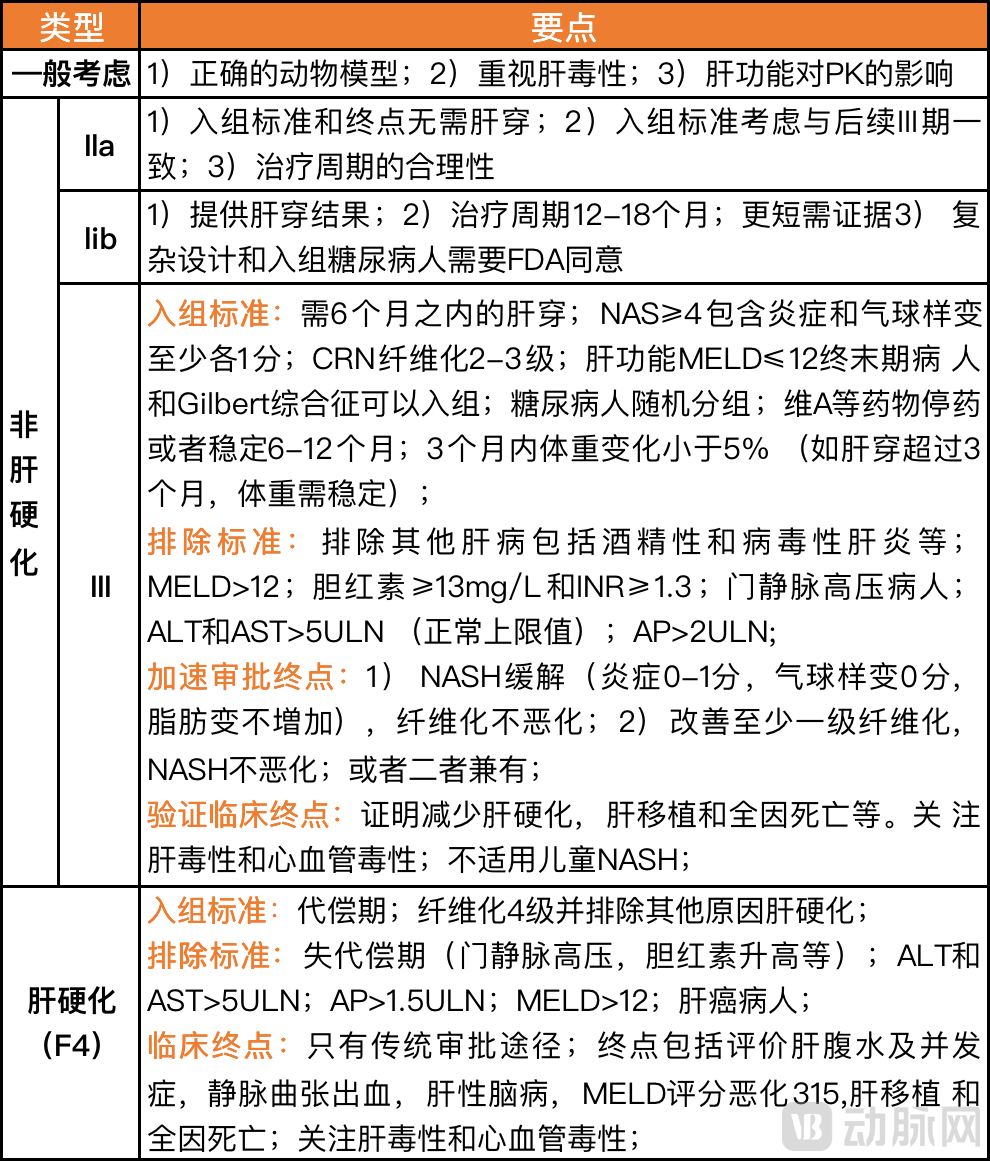

"The design of clinical trial protocols for NASH is very critical, including which stage of patients to select, what indicators to use as endpoints, sample size, trial duration, whether the pathological specimen testing methods are standardized, and so on. Each link may affect the final outcome. Currently, the FDA has guidelines for NASH clinical trials, especially with clear requirements for endpoint determination," explained Li Jia-kui.

The guidelines published by the FDA in 2018 clearly pointed out that drug interventions are mainly required for non-cirrhotic NASH at stages F2-F3, and compensated cirrhosis at stage F4. The three key indicators for accelerated approval of non-cirrhotic NASH are: regression of steatohepatitis based on overall histopathological parameters without worsening of liver fibrosis; improvement of liver fibrosis by one stage or more without worsening of steatohepatitis; simultaneous achievement of both regression of steatohepatitis and improvement of fibrosis.

Source: Dr. Xie Yuli | Annual Review of NASH New Drug Development (2020)

Therefore, clinical design capability is crucial for pipeline advancement, and these four companies each have their unique strengths in clinical design.

For example, Madrigal's subject recruitment became more precise, adjusting the proportion of patients with severe liver fibrosis during Phase III clinical trials. This led to the significant improvement in liver fibrosis in the drug group compared to the placebo group in the Phase III clinical trial of Resmetirom. Madrigal also adopted a non-invasive testing strategy: imaging information provided by FibroScan and MRE showed reductions in liver fat, liver fibrosis, liver enzymes, and various pro-atherosclerotic lipids. As a result, both liver biopsy and imaging tests reached clinical endpoints, which was beneficial for both the industry and FDA evaluation standards.

Intercept was once the frontrunner in NASH research and development, with its decisive advantage lying in extensive studies on the role of FXR in liver diseases. Since obeticholic acid was approved for marketing in 2016 for the treatment of primary biliary cholangitis, it provided Intercept with valuable and abundant first-hand real-world research data, offering significant assistance in designing subsequent NASH clinical trials.

Akero's Phase IIa clinical trial extension study Cohort C ventured into the treatment effects on advanced cirrhosis (F4) patients, a high-difficulty area, with a small sample size. This has provided Akero with unprecedented, proprietary data, paving the way for future trial designs.

However, some investors noted: “‘Elegance’ is a double-edged sword—impressive clinical trial results do not necessarily equate to real therapeutic benefits for patients. Still, we look forward to seeing breakthrough drugs crossing the finish line, which would be a significant boost for the NASH field.”

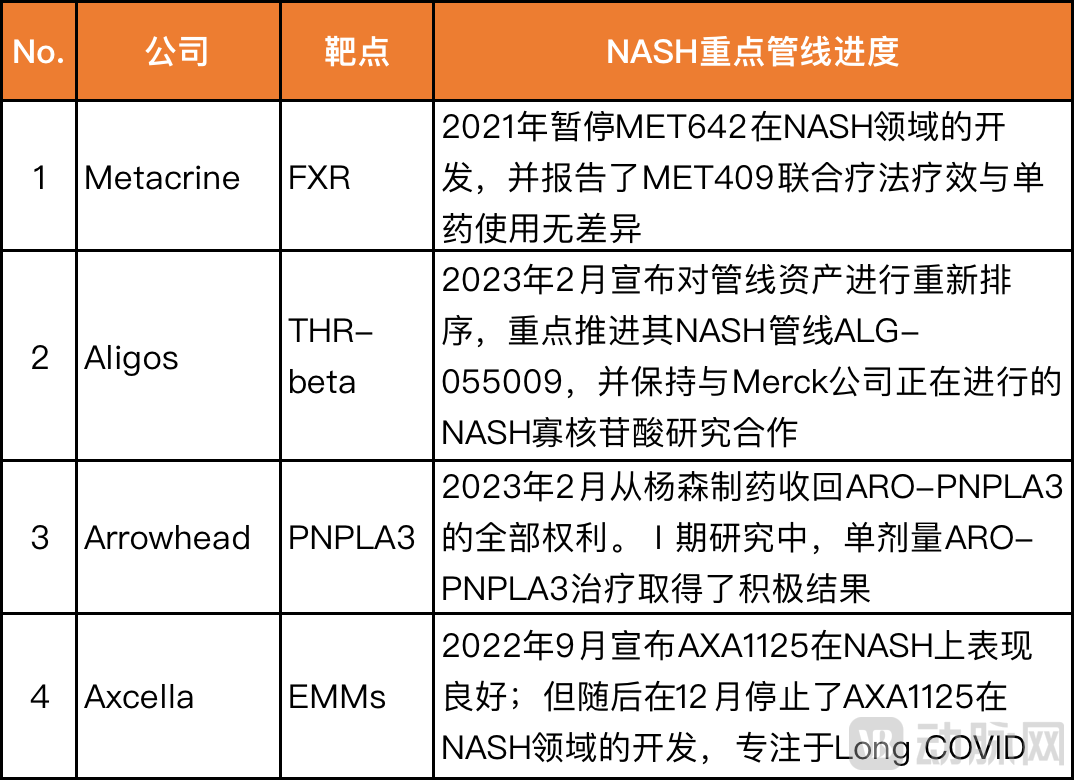

We have also compiled a list of star companies that have faced significant challenges in NASH research progress over the past two years:

This includes companies with innovative technological approaches, such as Axcella, which pioneered a new therapy using multi-target endogenous metabolic modulators (EMMs) to treat complex diseases. EMMs are key regulators and signaling agents in systemic metabolic pathways, capable of fundamentally regulating metabolism.

Or companies that have tried innovative therapies, such as Metacrine, which has launched clinical trials combining diabetes drugs like SGLT2 inhibitors to treat the complex pathogenesis of NASH. Combination therapy is also a path that many multinational corporations (MNCs) are exploring and validating.

But the pressure from cash flow, the interests of shareholders, or setbacks in clinical trials have forced them to shift their focus away from the NASH field.

"The R&D investment for NASH drugs is substantial, the treatment cycle is long, and the difficulty is relatively high. We can also see many Biotech companies strengthening cooperation with MNCs to jointly bear the R&D risks and benefits. Hopefully, the launch of NASH drugs will come in the near future," commented Li Jiakui.

Companies that cooperate with MNCs also have to face the possibility of strategic adjustments by MNCs at any time. For example, the RNAi therapy collaboration between Arrowhead and Johnson & Johnson—signals were positive one week, and the next week they announced a breakup.

Due to the positive Phase I clinical results, a breakup does not affect industry recognition. ARO-PNPLA3 is a highly promising NASH drug, and Arrowhead is also a "veteran" Biotech with over a dozen pipelines and a stable cash flow. However, for most Biotechs, careful navigation is required in a volatile environment.

MNCs Have Never Left the Playing Field

In the NASH field, a track that is theoretically and commercially promising, multinational corporations (MNCs) have consistently made significant investments. Gilead has 18 ongoing NASH projects, Pfizer has initiated 7 projects, while Novo Nordisk, AstraZeneca, and Boehringer Ingelheim each have 6 projects in development. However, the first to deliver positive news from Phase III clinical trials is the biotech company Madrigal Pharmaceuticals.

“NASH has broad prospects, and no MNC would be uninterested. However, they will consider the maturity of the field: Can the mechanisms currently advanced to later clinical stages truly open up this area? Or, if they are not particularly optimistic about existing mechanisms, should they invest in earlier-stage technologies and assets?"They must consider the position of the entire track within its cycle while coordinating with their own pipelines." Regarding the recent withdrawal of some MNCs from the NASH field, Kathy He, CEO of CARGENE BIOPHARMA, analyzed.

Kathy has over 20 years of experience in the pharmaceutical industry in both China and the U.S. She has led the U.S. market promotion of several blockbuster drugs for multinational corporations (MNCs) such as Takeda, Merck, and Abbott, and is well-versed in MNC product portfolio planning and strategic development. CARGENE BIOPHARMA, where she works, focuses on developing novel oligonucleotide drugs for advanced liver diseases, liver fibrosis, and ophthalmic conditions. The innovative mechanism of its first product pipeline shows unique potential in treating various liver diseases, including NASH.

Kathy believes: "MNCs can also make mistakes when making decisions, potentially returning some promising pipelines. However, if Biotech companies don’t lose confidence and continue to invest, and later develop a blockbuster product, MNCs will often pay a high price to buy it back. In terms of innovative technologies, Biotech companies tend to have a more accurate vision. Throughout this process, Biotech assumes more of the R&D role, while MNCs take on the later-stage commercialization, promoting the drug and scaling it up."

Besides, promoting disease awareness and industry standards is also an important role of MNCs. For example, in 2019, Gilead faced consecutive setbacks in the NASH field, but it applied clinical research data to other practices, including promoting better non-invasive diagnostic tests into clinical trials and improving invasive liver biopsy standards.

Therefore, it is not accurate to describe MNCs' attitude towards NASH as disinterested just because of some failed cases or halted pipelines. MNCs may have temporarily chosen not to directly engage, but that does not prevent them from investing in and supporting promising technologies behind the scenes: Pfizer abandoned its NASH candidate drug KHK inhibitor PF-06835919 in July 2021, but the following year it provided Akero with a $25 million equity investment.

MNCs can also choose not to engage in direct competition but instead wait for the right moment to acquire based on clinical trial results. Among the most sought-after M&A targets in the biopharmaceutical industry this year, Madrigal Pharmaceuticals is prominently listed, and Viking Therapeutics, known for its better cost-performance ratio, is also among them.

MNCs are always ready to re-enter the competition, or rather, they have never left and will never be absent from this market.

Is a domestic investment boom coming?

Many industry insiders believe that Madrigal's Resmetirom has a high likelihood of being approved as the first drug. At the JPM conference in January, investors also showed great enthusiasm for the NASH field.

In the NASH field, success for one is success for all. The good news from Madrigal has also brought attention to China's NASH-related companies, but China’s efforts in NASH are still in the early stages.

One of the earliest companies in China to invest in NASH is Terns Biopharma. In April 2018, Terns obtained the global exclusive rights for the development and commercialization of three small molecule drug candidates from Eli Lilly that have the potential to treat NASH. Among the companies with faster progress are Ascletis andJun Sheng Tai, which initiated the Phase IIb trial in December last year.

Younger competitors include Eternity Bioscience, founded in 2018, which is exploring combination therapies targeting THR-beta and GLP-1; and Hidragon Pharma, established in 2017. In January this year, Hidragon disclosed positive Phase IIa clinical data for its FXR agonist HPG1860 in the treatment of NASH, effectively supporting subsequent clinical development.

Apricot Capital, the investor of Yachuang, was one of the earlier VC institutions in China to focus on metabolic diseases and NASH. When investing in Yachuang in 2019, managing partner Chen Haigang judged that the best window period for VC investment in NASH would be before 2023.

"At that time, the global R&D had entered the second half, while in China, it had just started.In recent years, there has been a new understanding of targets, pathways, and more, and the industry has developed, but NASH remains a field where investment consensus has yet to form in China."At this stage, many investors are still unwilling to take relatively large risks on such early-stage projects." Chen Haigang believes that the domestic NASH field has not yet reached a boiling point; everyone is still waiting for the situation to become clearer or waiting to invest in some later-stage projects.The clear demand in China has not yet emerged, but in the long term, with a large patient base, there will definitely be enormous potential.”

"In recent years, new technologies have emerged. I believe that small nucleic acid drugs have great potential in metabolic diseases such as NASH. Areas where small molecules have struggled to become effective drugs now have hope of success, and the dosing interval can be extended. In this aspect, I am optimistic about new breakthroughs in the future."

CARGENE BIOPHARMA is one of the companies at the forefront of exploring treatments for liver fibrosis and hepatic functional decline caused by various liver diseases using RNAi technology. This company emerged from stealth mode in 2021, focusing on developing innovative targets that restore liver regeneration capabilities for the first time globally. It aims to complement other therapies that alleviate inflammation or modulate metabolic mechanisms, with the goal of achieving the ablation of liver fibrosis in patients.

However, it is clear that investors in China are paying more attention to the sugar and lipid metabolism field. With continuous iterations of GLP-1, Eli Lilly and Novo Nordisk, as giants in the diabetes sector, have seen their stock prices multiply in recent years, with both currently holding market values exceeding 300 billion US dollars.Changes in lifestyle, the pursuit of quality of life, and the need for long-term medication have brought drugs for metabolic diseases such as NASH into the spotlight.

Some investors have expressed to us that we should accelerate coverage before the consensus phase arrives: "The pathogenesis of metabolic diseases such as NASH is complex, and it won't become clear as quickly as in the oncology field, but we know the market potential is enormous, so we will pay special attention to new players emerging in this field."