Beijing Stock Exchange Attracts Over 200 Companies in Under a Year: A Strategic Gateway for Innovative SMEs

ChenGuang Medical

Developer, Manufacturer, and Supplier of Core Components in the MRI Industry Chain

Northland

Innovative Biopharmaceutical Manufacturer

Leveraging the power of capital to expand and strengthen enterprises is a common practice in the development process of healthcare companies. However, for small and medium-sized medical enterprises without star entrepreneurs, difficulties in financing and high financing costs remain unavoidable challenges. Particularly in drug research and development, which typically takes at least 10 years to complete, even the phase from clinical trials to market launch can take 7 years or longer, with an extremely high risk of failure, making financing increasingly difficult for such enterprises.

According to incomplete statistics, there are currently about 8,000 pharmaceutical manufacturing enterprises and approximately 30,000 medical device companies in China, more than half of which are small and medium-sized enterprises (SMEs). These SMEs also face the issue of funding shortages during their development. The emergence of the Beijing Stock Exchange (referred to as BSE) provides these SMEs with innovative development intentions the opportunity for capital financing, which will also promote the high-quality development of China's healthcare industry from the source.

After 570 days and nights, the Beijing Stock Exchange welcomed its 200th listed company.

Since the establishment and listing of the NEEQ in 2012, its official operation in 2013, the implementation of tiered management in 2016, the launch of the Select Layer and establishment of the transfer mechanism in 2020, to the official opening of the Beijing Stock Exchange in 2021, and the listing of the 200th company in June 2023, the Beijing Stock Exchange truly represents "a decade of honing a sword."

Whether viewed from their own positioning or service scope, the Beijing Stock Exchange (北交所), Shenzhen Stock Exchange (深交所), and Shanghai Stock Exchange (上交所) are entirely different. Each of the three has its own characteristics, forming complementary functions, serving enterprises at different stages of development.

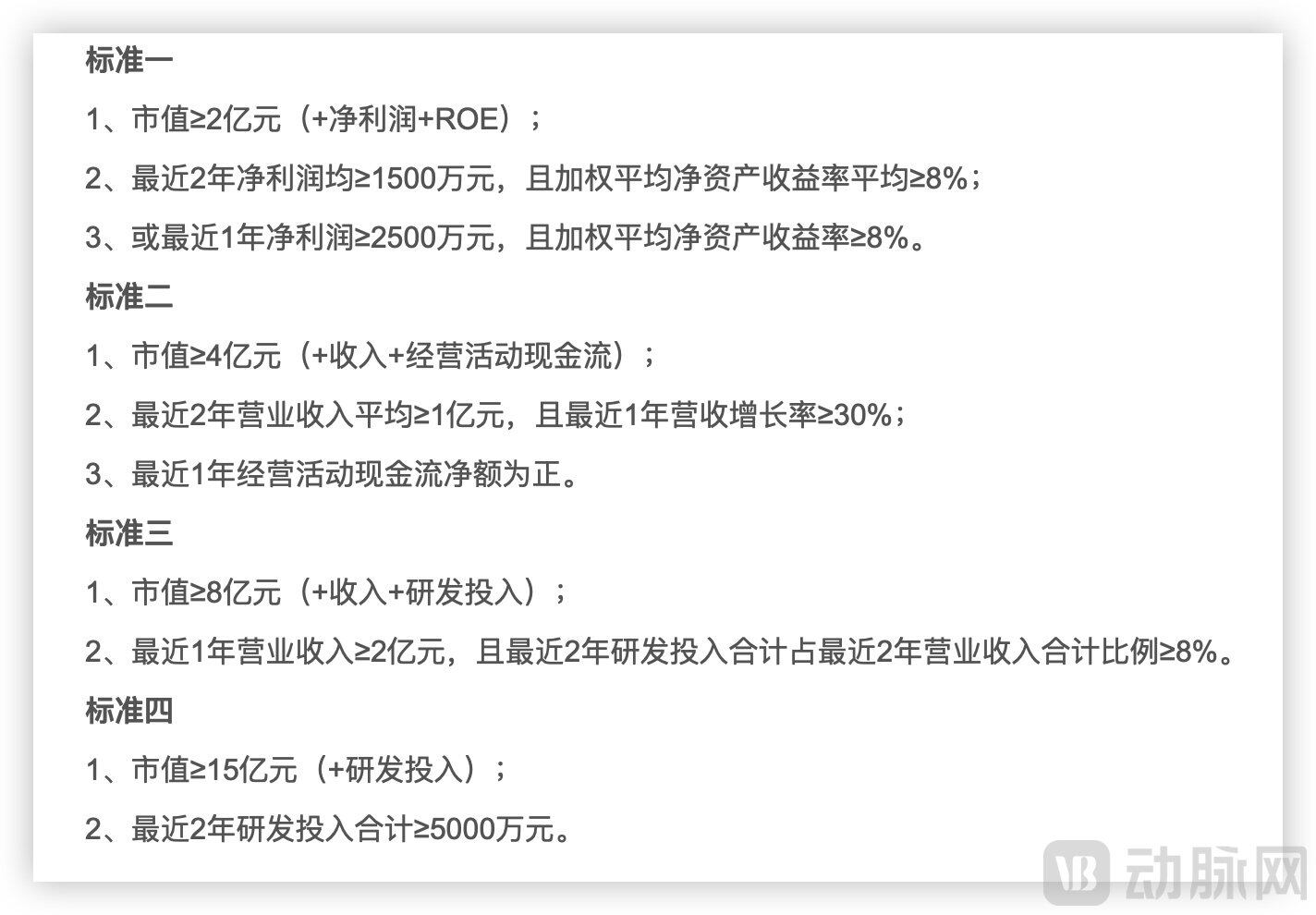

The Beijing Stock Exchange is composed of the selected layer of the New Third Board. Companies can be listed on the basic layer with an income of 10 million yuan, on the innovation layer with a profit of 10 million yuan or revenue of 120 million yuan over two years, and on the selected layer with a profit of 15 million yuan or revenue of 200 million yuan over two years.

Such policy provisions undoubtedly enable the Beijing Stock Exchange to target earlier, smaller, and more innovative small and medium-sized enterprises, offering them a tailored financing pathway.

Financial Standards for Listing on the Beijing Stock Exchange, Data Sourced from the Official Website

From the perspective of regional layout, the Shenzhen Stock Exchange (SZSE) radiates across the Pearl River Delta and the Guangdong-Hong Kong-Macao Greater Bay Area, serving the new economy. The Shanghai Stock Exchange (SSE) relies on Shanghai to radiate across the Yangtze River Delta region, serving hard technology enterprises. As another major innovation center in China, Beijing gathers a large number of research institutions, universities, and technology companies with abundant scientific and technological achievements. Transforming these scientific and technological achievements requires the empowerment of the capital market. The establishment of the Beijing Stock Exchange (BSE) will not only help them embark on a path of sustainable development but also balance financial resources between the northern and southern regions of China.

As of early June this year, the number of companies listed on the NEEQ (New Third Board) is close to 7,000, most of which comply with national industrial policies and strategic directions. These enterprises temporarily fail to meet the requirements of the STAR Market and the ChiNext Board, and the Beijing Stock Exchange (BSE) has precisely met their needs.

On the other hand, most of the companies currently listed on the Beijing Stock Exchange belong to emerging strategic industries, covering sub-sectors such as biomedicine, high-end precision manufacturing, and information technology. According to Choice data, the total market value of the 200 listed companies is about 260 billion yuan. Although their scale is relatively small, their businesses are more focused. With the support of the financial market, they have the opportunity to grow rapidly and expand their scale.

For small and medium-sized enterprises in the start-up phase, financing difficulties are a "long-standing" problem on the road to development.

Taking the pharmaceuticals and biotechnology field as an example, in recent years, an increasing number of small and medium-sized enterprises have begun to join the ranks of innovative drug research and development. However, the development of innovative drugs is characterized by high technological barriers, substantial financial investment, high risks, and long cycles. The process for a new drug, from preclinical research to gaining market approval, often takes at least a decade.

For small and medium-sized enterprises (SMEs), there is no lack of desire or motivation for innovation, but rather a shortage of resources and production factors. For instance, the development platform for innovative biopharmaceuticals needs to complete the initial construction of engineered strains, establish production processes, conduct quality research, and carry out preclinical pharmacology and toxicology studies before moving into the clinical stage. However, even when reaching Phase II or Phase III clinical trials, the possibility of R&D failure remains extremely high, posing significant risks to the enterprise.

SMEs without product revenue as a foundation will struggle to sustain the R&D of new drugs for a long time. At the same time, SMEs without star founders or those not targeting star research points face increasing difficulty in obtaining direct financing. Indirect financing requires asset collateral, and for SMEs in their start-up phase, many intangible assets are hard to evaluate, making it difficult for numerous financial institutions to grant credit or provide loans.

The same is true in the field of medical devices. Although the development cycle is not as long as that for drug research and development, medical device products often involve incremental innovations, with a high degree of diversification and personalization, leading to a large number of niche areas. As a result, the upgrading and iteration of device products occur relatively quickly, with a lifecycle typically lasting only 2 to 5 years. At the same time, the market scale for a single product is often not very large, meaning companies need to continuously expand their product lines to grow and develop. Additionally, promoting products after approval is another major challenge, one that startups often struggle to handle.

On the other hand, medical devices are characterized by their multidisciplinary nature and the high difficulty of technical integration. They typically combine knowledge and R&D production technologies from multiple disciplines such as electronic machinery, materials science, life sciences, clinical medicine, and computer science, possessing both "manufacturing + healthcare" attributes. This is a high-end manufacturing industry that is multidisciplinary, technology-intensive, and capital-intensive. The higher the degree of innovation in a product, the greater its manufacturing difficulty, and the higher the risks faced by enterprises.

Whether it is a startup in drugs or medical devices, they also face the issue of talent. How to attract talent, how to build a research and development platform, and how to ensure high-quality growth ultimately boils down to the issue of funding.

To address the issues of difficult and expensive financing for small and medium-sized enterprises (SMEs), the Beijing Stock Exchange (BSE) offers financing tools such as stock issuance, mergers and acquisitions, and refinancing. The issuance methods are relatively more flexible, significantly reducing the financing cycle and costs for SMEs.

The industry structure of the Beijing Stock Exchange is similar to that of the STAR Market and the ChiNext Board, with pharmaceuticals and biotechnology being important components of its sectors.

In November 2021, the Beijing Stock Exchange (BSE) officially opened for trading, with 71 existing Select Layer companies directly transferring to the BSE. Among them, there were 10 pharmaceutical companies: VacciBio, Northland, Senxuan Pharmaceutical, Sanyuan Gene, Honsun(nantong), BioGu, DeYuan Pharma, Zitong Palace, Datang Pharmaceutical, and Jinghao, making it the second-largest sector on the BSE in terms of quantity.

The 10 companies listed this time are mainly distributed in the sub-sectors of biotechnology, Western medicine, traditional Chinese medicine, and medical devices, with no enterprises related to medical services for now. From the perspective of sub-industries, eight out of the 10 companies are pharmaceutical firms, and the remaining two are medical device manufacturers.

Taking Northland, which focuses on gene therapy drug development, as an example, according to the 2022 annual report data, its revenue was 64.6546 million yuan, a year-on-year increase of 13.72%. However, since the new drug is still in the research and development stage, the revenue is solely supported by ophthalmic generic drugs, providing financial support for new drug development and the company's ongoing operations. Consequently, the net profit attributable to shareholders was -67.6168 million yuan.

Two medical device manufacturers, Honsun(nantong) Co., Ltd. and Jinghao, focus on home medical devices as their main business. Honsun(nantong) Co., Ltd. mainly produces chronic disease monitoring equipment such as blood pressure monitors and nebulizers, while Jinghao's primary products are hearing aids and nebulizers. According to Choice data, the latest market value of both companies is less than 1 billion. In the past three years (2020-2022), their revenue growth has been modest, with net profit growth at approximately 10%.

It can be seen that among the first batch of listed medical enterprises, the overall scale is relatively small and the development speed is slow. Without a financing platform like the Beijing Stock Exchange (BSE) that focuses on serving small and medium-sized enterprises, their production and operation could only progress gradually and would not be able to advance rapidly. The emergence of the BSE gives them an opportunity for leapfrog development, allowing them to quickly move into the next stage of development.

Moreover, the equity incentive policy of the Beijing Stock Exchange (BSE) has also given small and medium-sized medical enterprises more confidence in pursuing talent.

Although it has not received as much attention as the Shanghai and Shenzhen markets, the establishment of the Beijing Stock Exchange (BSE) still provides small and medium-sized enterprises with more exposure opportunities, thereby increasing their visibility. Moreover, the BSE has relaxed the scope of eligible participants for incentives, including senior management, core technical personnel or key business staff, as well as other employees that the company deems should be incentivized due to their direct impact on the company's operating performance and future development, including foreign employees.

The Beijing Stock Exchange's Equity Incentive and Differential Voting Rights System: Fostering a Win-Win Ecosystem for Management, Technical Talent, and Investors to Stimulate Innovation Vitality in SMEs; More Small and Medium-sized Enterprises in the Pharmaceutical Sector May Choose the Beijing Stock Exchange in the Future.

A Look at the Listed Companies on the Beijing Stock Exchange: Whether They Possess Core Competitiveness in Niche Markets is Key to Demonstrating Their Value.

In December 2022, ChenGuang Medical was listed on the Beijing Stock Exchange. In a market environment with extremely poor sentiment and a new share break-even rate exceeding 70%, it rose against the trend by 33%. In May, which has just passed, ChenGuang Medical experienced a 30cm limit-up situation, with the highest increase exceeding 80% over three trading days from May 22 to May 24.

Founded in 2004, ChenGuang Medical's main business is the research, production, and sales of core hardware for medical imaging superconducting MRI equipment and special magnets for scientific research. Its product system covers more than 90% of the hardware for superconducting MRI equipment. The company’s main revenue comes from its series of superconducting magnets and RF detector products, which accounted for a high of 90.93% of its revenue in 2022.

What attracts investors is ChenGuang Medical's own technical attributes. It possesses the capability for independent research, development, production, and commercial sales of over 90% of the core hardware in MRI equipment. It is one of the few independent third-party suppliers globally that masters the production technology of 1.5T, 3.0T, and 7.0T superconducting magnets and has formed long-term cooperative relationships with Philips, Wandong Medical, and Langrun Medical. Meanwhile, the 230/250MeV proton therapy superconducting cyclotron developed by ChenGuang Medical for the China Institute of Atomic Energy assists the institute in overcoming key technical challenges in proton therapy systems, breaking the dependence on foreign imports.

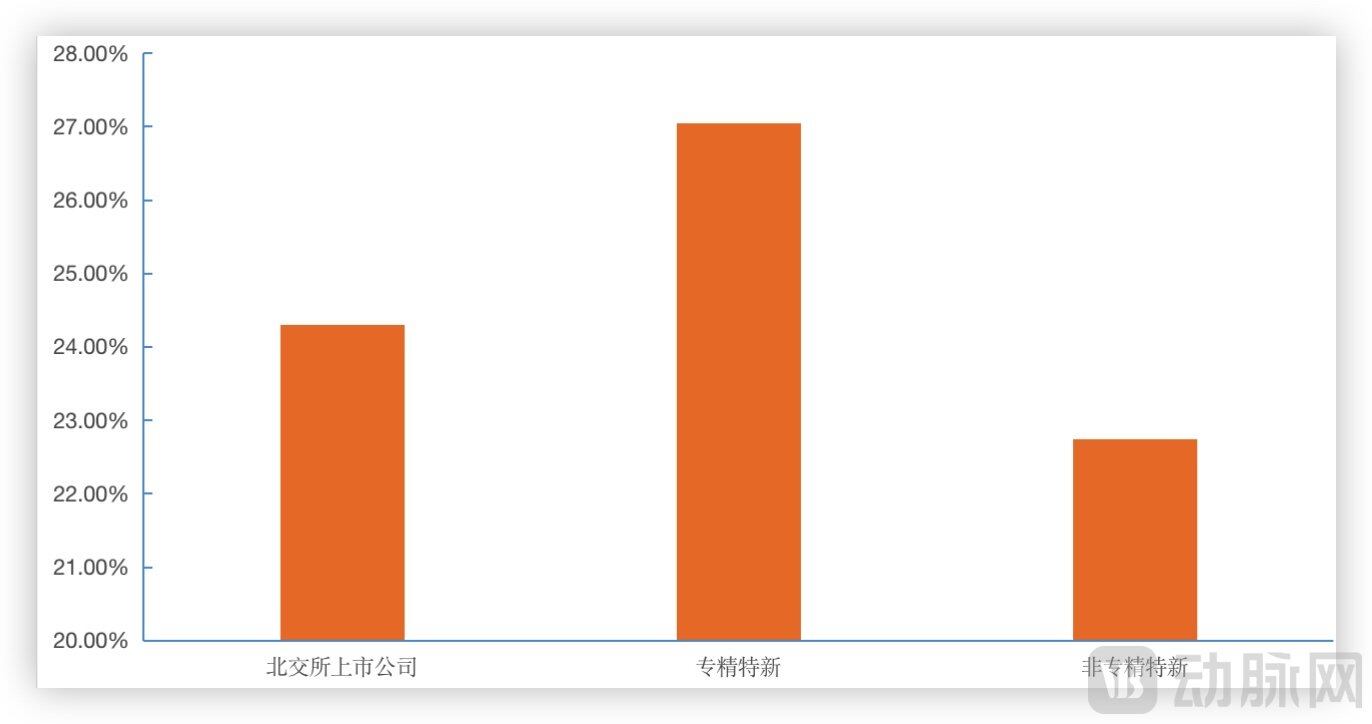

From the data, enterprises with obvious innovative attributes are more preferred by investors in the Beijing Stock Exchange. Among the 200 listed companies, 78 are "specialized, refined, distinctive, and innovative" small and medium-sized enterprises or "little giant" enterprises, accounting for 39.20% of the total. Comparing companies with "specialized, refined, distinctive, and innovative" attributes to non-specialized enterprises, the average three-year compound revenue growth rate of specialized enterprises is relatively higher, reaching 20.27%, while that of non-specialized enterprises is less than 15%. Last year, these enterprises achieved an average year-on-year growth in operating income and net profit of 19.57% and 16.41%, respectively, showing a strong growth momentum.

The Average First-day Gain of Listed Companies on the Beijing Stock Exchange, Data from Choice

Among the 20 companies with the lowest growth rates in the Beijing Stock Exchange (BSE) listed enterprises, only one company possesses the attribute of being specialized, refined, unique, and innovative. Moreover, in terms of performance at the time of listing, the average first-day increase for all currently listed BSE companies is approximately 24%, while the average first-day increase for companies with the specialized, refined, unique, and innovative attribute is 27.02%, which is higher than the average. Additionally, the initial public offering price-to-earnings ratio of companies with the specialized, refined, unique, and innovative attribute is also higher than the average.

The specialized and innovative attributes of the Beijing Stock Exchange (BSE) make it particularly attractive for certain niche sectors. For instance, Scientz Biotechnology and Jinan Hanon Instruments, which were listed on the BSE at the end of 2022, as well as Boxun Biotechnology, which just passed its review in June, are all companies focused on scientific instruments. The scientific instrument industry is a high-tech sector that provides tools and methods for scientific research. Its levels of innovation, manufacturing, and application serve as crucial indicators for measuring a nation's scientific development and potential. It is a foundational industry supporting scientific progress and technological innovation, as well as a strategic industry with significant influence on a country’s industrial capabilities, innovative strength, and even national security.

However, for domestic companies in this industry, smooth development is not easy. The related industries abroad are mature, and companies within the industry have already scaled up under the impetus of capital, completing the transition from small and medium-sized enterprises to giant corporations.

Taking Thermo Fisher's development in the analytical instruments field as an example, through the acquisition of instrument companies with high technological barriers, horizontally expanding into new product matrices, vertically extending into new application areas for instruments, and continuously strengthening the raw material and component support capabilities required for the upstream industrial chain of analytical instruments, a complete product solution has been formed. Thermo Fisher has evolved from a single-field manufacturer into a one-stop scientific research service provider.

In contrast, domestic enterprises, due to their late development and the lack of upstream supporting industrial chains, face more fundamental engineering issues such as materials and components during the R&D process. Moreover, the market scale of a single category of scientific instruments is limited, which is insufficient to support enterprises in expanding into multiple fields.

The two companies listed on the Beijing Stock Exchange this time, Ningbo Scientz Biotechnology Co., Ltd. and Jinan Hanon Instruments Co., Ltd., have revenues of only hundreds of millions and R&D funds of only tens of millions. Without financing, their development speed would definitely be restricted. It is precisely because of the platform provided by the Beijing Stock Exchange that these enterprises have been able to rapidly expand their business scale. Meanwhile, the standardization of management has put them on the right path towards cost reduction and efficiency improvement. With financial support, these enterprises can accelerate the expansion of scientific instruments into multiple fields or invest in other niche areas.

According to Choice data, in 2022, the average R&D intensity of companies listed on the Beijing Stock Exchange (BSE) was 4.63%, approximately three times the average level of enterprises above designated size. Throughout 2022, more than 2,600 new patents were added, including over 600 invention patents. Companies that focus on niche markets, possess strong innovation capabilities, and master core technologies will leverage the BSE to achieve industrial upgrading and realize leapfrog development.

As of mid-June, 40 new companies have been listed on the Beijing Stock Exchange this year, compared to only 15 in the same period last year, showing a significant increase.

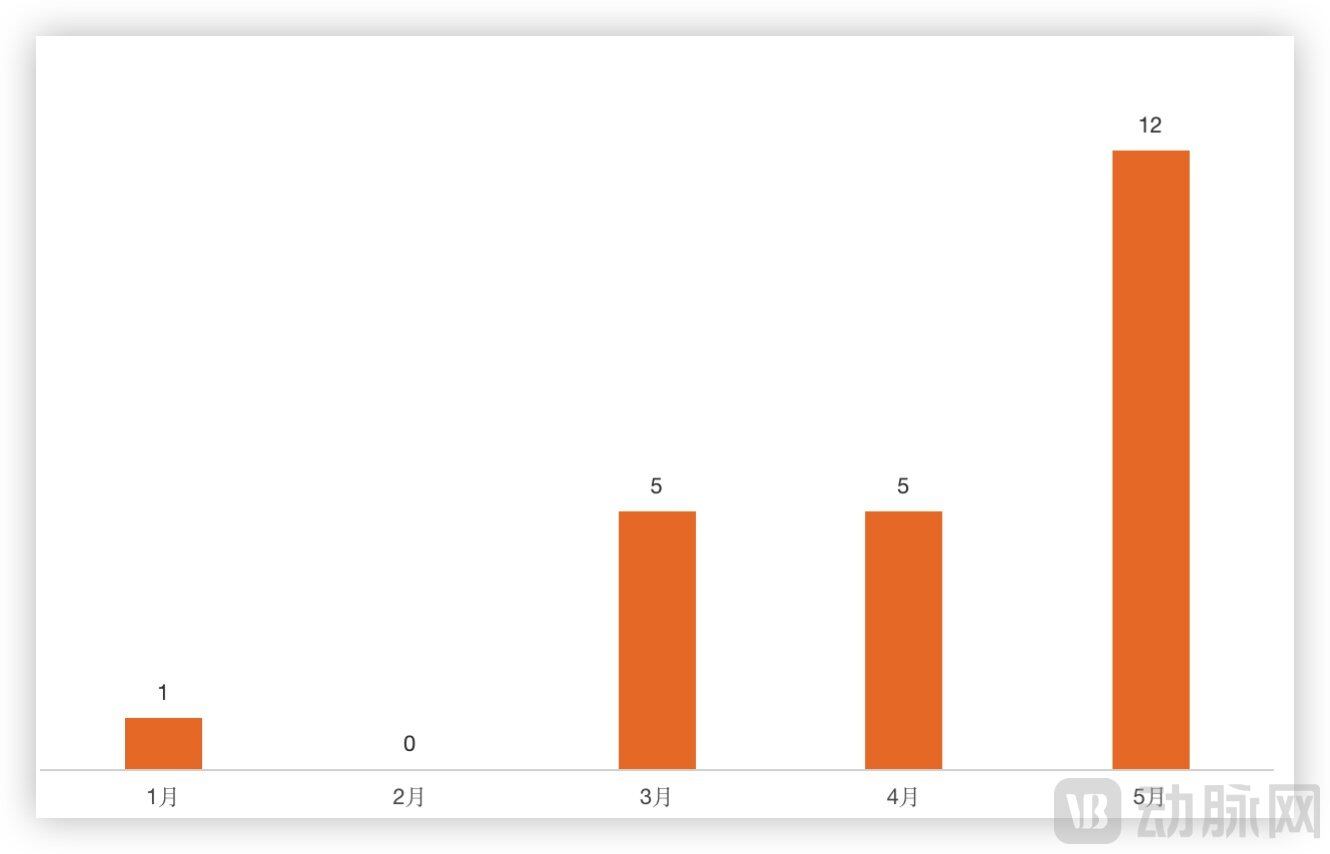

Since the second half of last year, the high-quality and rapid expansion of the Beijing Stock Exchange (BSE) has become a market consensus, with the efficiency of issuance, review, and listing continuously improving. Data from East Money Choice shows that as of June this year, the BSE averaged nearly 7 listings per month, compared to 2.5 per month in the same period last year, indicating a significant increase in efficiency this year. From January to May this year, the BSE newly accepted 23 companies, including 1 in January, 0 in February, 5 in March, 5 in April, and 12 in May, showing clear signs of acceleration.

The number of newly accepted companies on the Beijing Stock Exchange, data sourced from the official website.

At the end of last year, the Beijing Stock Exchange (BSE) introduced a direct linkage mechanism, further reducing the listing time for eligible companies from the National Equities Exchange and Quotations (NEEQ) to the BSE. High-quality enterprises can go public through the “12+1” or “12+2” process. This means that after being listed on the NEEQ for 12 months, companies can list on the BSE in the 13th or 14th month, indicated by “+1” or “+2.”

Companies like Zhongke Meiling, which focuses on low-temperature storage equipment for biomedicine, took only 37 days from acceptance to approval and 111 days from acceptance to listing, setting the fastest record at the Beijing Stock Exchange at that time. On the other hand, Kangley Weishi, a company engaged in recombinant protein vaccine research, had the longest listing process at the Beijing Stock Exchange, taking 351 days from acceptance to listing. Overall, the average time from acceptance to listing is about 240 days at the Beijing Stock Exchange, approximately 688 days at ChiNext, and around 393 days at STAR Market. In comparison, the fast pace of the Beijing Stock Exchange undoubtedly better aligns with the needs of small and medium-sized enterprises.

Expansion is an objective law of the financial sector's development. The Beijing Stock Exchange (BSE) was established not long ago, and after experiencing a wave of new stock listings at the end of last year, "high-quality" expansion has become the focus of attention this year.

The industry's expectation for "high-quality" expansion also lies in promoting the improvement of the transfer system. The positioning of the Beijing Stock Exchange (BSE) determines that it is oriented towards small and medium-sized enterprises (SMEs). When these enterprises reach a certain level of revenue through their efforts, transferring to another board would better meet their development needs while also attracting more high-quality SMEs to list on the BSE. The core objective of establishing the BSE is to improve the tier construction of China’s A-share market, and the transfer mechanism is an indispensable part of a healthy tier system.

An investor told VCBeat: "The companies listed on the Beijing Stock Exchange (BSE) still have a certain gap in scale compared to those on the Shanghai and Shenzhen boards. Although they hold a certain level of strength and status in some niche fields, the ceiling for their own development is also quite evident. How to demonstrate the scalability of their technology and the growth potential of the company, help the market deepen its understanding of various niche sectors, and thereby enhance the willingness to invest in the BSE, are issues that companies must consider."

Back to medical enterprises, taking device companies as an example, according to incomplete statistics, there were about 30,000 domestic medical device companies in China in 2022. Among them, approximately 20,000 companies could produce Class I devices, about 10,000 companies could produce Class II devices, and only around 2,000 companies were capable of producing Class III devices. Over 80% of these device companies had annual revenues of less than 20 million yuan, with only a few hundred companies having an annual output value exceeding 100 million yuan, presenting a pyramid-shaped structure.

The healthy development of small and medium-sized enterprises (SMEs) is the foundation for the orderly progress of the industry. How to enable SMEs with development potential to efficiently raise capital and achieve high-quality growth through the capital market in a timely manner has been a problem that the market has failed to solve for a long time. The emergence of the Beijing Stock Exchange (BSE) provides market support for the sustainable innovation of SMEs. The 200 listed companies are just the beginning, and in the future, more high-quality SMEs, including those in the healthcare and broader health sector, will rise with the help of the BSE.