How Did the 12 Big Pharma Companies Respond to the Disruptive Potential of Biotechnology?

GSK

Pharmaceutical R&D Manufacturer

AstraZeneca

Biopharmaceutical Manufacturer

How do large companies respond to potentially disruptive technologies over time? This is a key strategic challenge for companies in mature industries.

Especially in the biotechnology field, the early stages of new technology development are often marked by unclear directions, requiring long research and development cycles, coupled with uncertainties in commercialization, making such strategic challenges even more pronounced.

What are the coping strategies chosen by Big Pharma? How have these strategies evolved over time? And which methods have ultimately been more successful?

This paper, published in the California Management Review in 2018,Provided an enlightening insight and a nuanced perspective.Researchers studied how 12 Big Pharma companies responded to the opportunities/challenges of biotechnology over 25 years? (1990-2015, including two major up and down cycles of biotechnology)

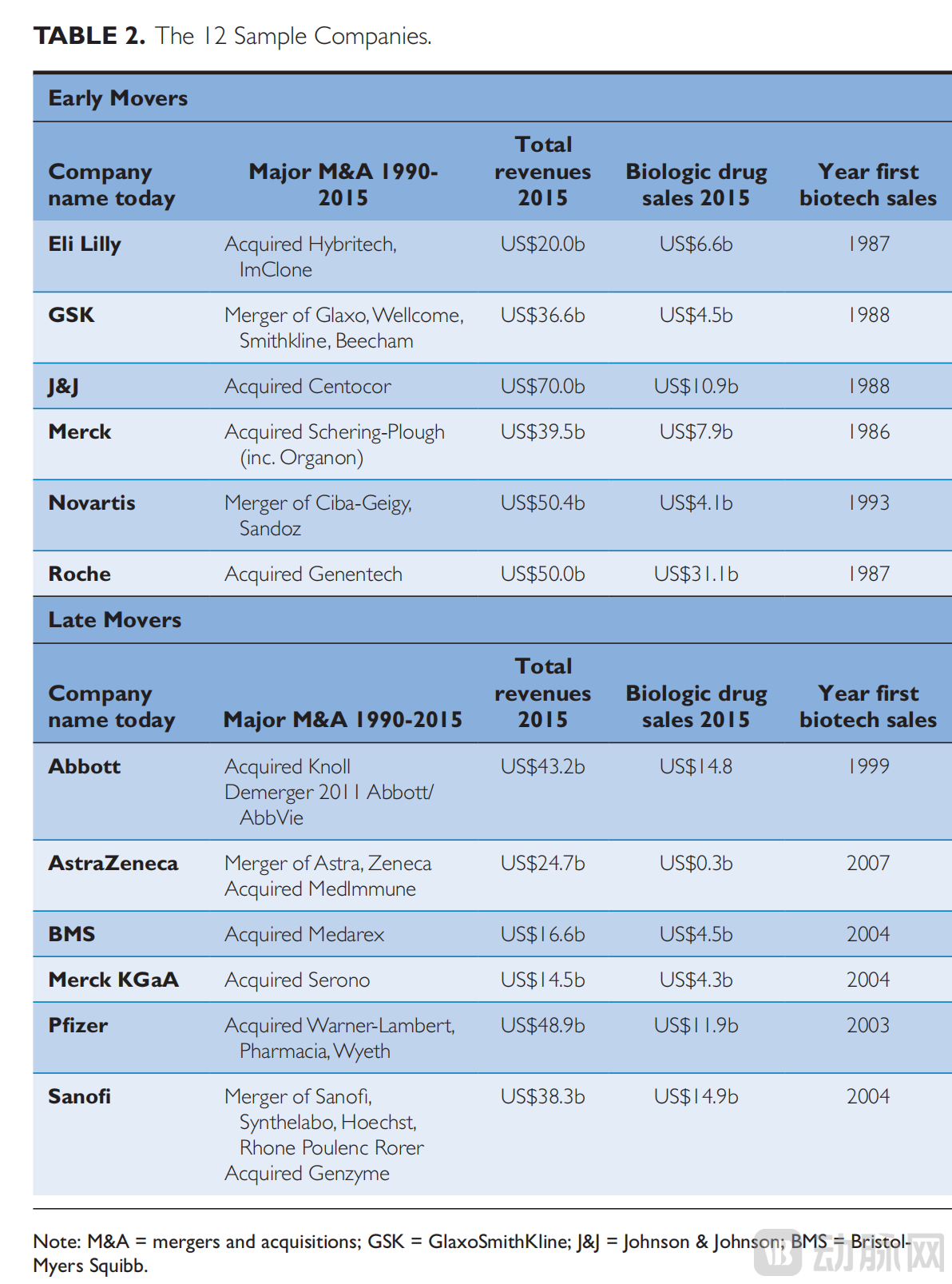

The 12 Big Pharma companies are divided into two camps:6 Early Movers(including Johnson & Johnson, Merck & Co., Eli Lilly, Roche, Novartis, and GlaxoSmithKline), they have entered the biotechnology field more quickly through a series of different mechanisms, including acquisitions, alliances, and sustainable investments;The other six are latecomers.(Including Pfizer, Bristol-Myers Squibb, Abbott, Sanofi, AstraZeneca, and Merck KGaA), they developed relatively slowly and did not make significant commitments to biotechnology until the early 21st century. By 2015, all of these companies had achieved relatively high levels of biotech sales, but their profitability and future growth prospects varied significantly.

Although the executives of 12 companies were aware of the emergence of biotechnology, their responses varied greatly, both in terms of the type of investment activities and the timing of their investments. Analysis shows that some responses were more effective than others. Early movers were more successful than latecomers. Based on this, the authors of the paper proposed several ways in which long-term commitment to biotechnology can be rewarded.

VCBeat has compiled the core information and viewpoints of this paper:

Large Pharmaceutical Companies and Biotechnology Industry (1990-2015)

Although biotechnology has always played a role in drug development, the breakthrough in gene-splicing technology in the 1970s made it possible to scale up natural products produced within the body, such as insulin, growth hormone, and erythropoietin (EPO). The first product—human insulin ("Humulin"), manufactured by Genentech and licensed to Eli Lilly—was successfully brought to market. These initial successes enabled the first "biotech" companies, such as Genentech and Amgen, to secure venture capital funding.

In the 1980s and 1990s, large pharmaceutical companies such as Merck, GlaxoSmithKline, and Roche had developed deep expertise in chemistry, utilizing technologies like combinatorial chemistry and high-throughput screening to standardize the development process of "small molecule" drugs. However, as the return on investment from these technologies gradually slowed and advancements in biotechnology research accelerated, many major pharmaceutical companies began closely monitoring this emerging field, for example, through strategic alliances with the most promising startups and selective acquisitions. Biotechnology was seen as an exciting new field, with "over 400 U.S. companies investing up to $2 billion annually in biotech R&D."

However, the biotech revolution proved to be "full of promise but with few profitable drugs," and in 2000, the biotech "bubble" burst, leading to the collapse of many startups and causing large companies to shelve their investment plans.

In the 2000s, fundamental science in biotechnology made progress, primarily advancing in three major directions. One of these was the creation of entirely new biologic drugs, such as those based on monoclonal antibodies (MABs). Pioneering research on monoclonal antibodies began in the 1970s, and the first fully human product, adalimumab, received approval for the treatment of rheumatoid arthritis in 2002. By 2015, there were already more than fifty monoclonal antibody drugs on the market.

Secondly, the Human Genome Project, which began in 1990 and was completed in 2001, provided tools for a better understanding of diseases and therapeutic targets, as well as for improving the discovery and development processes of small molecules and biologic drugs. The third direction is the creation of new interventions for treating genetic disorders and enhancing the immune system’s ability to combat infectious diseases and cancer. Although these forms of "gene therapy" show great potential, progress has been slow and expensive, with some drug withdrawals (e.g., Glybera).

In all these fields of opportunity, coupled with the strong economy in the early 2000s, biotechnology ushered in a second wave of optimism and investment boom. By the early 2010s, these investments began to bear fruit, with an increasing number of "biologics" drugs gaining approval from the U.S. Food and Drug Administration (FDA). Many of these proved to be blockbusters: by 2015, six of the top ten best-selling drugs globally were biologics, compared to only two in 2010. Despite the rapid growth in total sales revenue of biologic drugs, sales revenue based on chemicals had begun to decline.

We selected 12 companies for in-depth analysis, all of which had already developed core technologies based on chemistry by 1990.All companies have recognized the potential of biotechnology, but their responses vary significantly in terms of timing (early/late) and operational focus (external acquisition/internal development).Of these 12 companies, six entered the biotechnology field relatively early, meaning they had sales of biopharmaceutical products before 1999; the other six entered relatively late, generating revenue from biopharmaceutical products for the first time in or after 1999, and are now committed to a certain level of biotechnology-based R&D.

Note: The table analyzes six companies that entered the biopharmaceutical field early: [Eli Lilly, GSK (GlaxoSmithKline), J&J (Johnson & Johnson), Merck (Merck & Co.), Novartis, Roche] and six companies that entered late: [Abbott, AstraZeneca, BMS (Bristol-Myers Squibb), Merck KGaA, Pfizer, Sanofi]. For these 12 companies, major mergers/acquisitions or spin-offs during 1990-2015, total revenue in 2015, biopharmaceutical sales revenue in 2015, and the year they first sold biopharmaceuticals are included.

We collected data from multiple sources. First, we used Thomson's databases (ReCap and Cortelis) to gather year-by-year data on each company’s external biotechnology-related activities. We also tracked significant drug events (product launches, clinical trials), as well as all income statement and balance sheet data. Second, by reading annual reports, all major press releases, and analyst reports, we compiled detailed case histories for each company. Third,We interviewed 17 experts in this field.. These interviews were not used as the primary data source, as changes occurred over a long period (1990 to 2015), and retrospective statements are often biased. However, as "expert interviews," they helped validate the findings and provided interpretations to aid in understanding complex situations.

Although the early stages of the analysis are relatively informal,But the subsequent phase is structured, mainly focusing on establishing a "response model" for each company.。

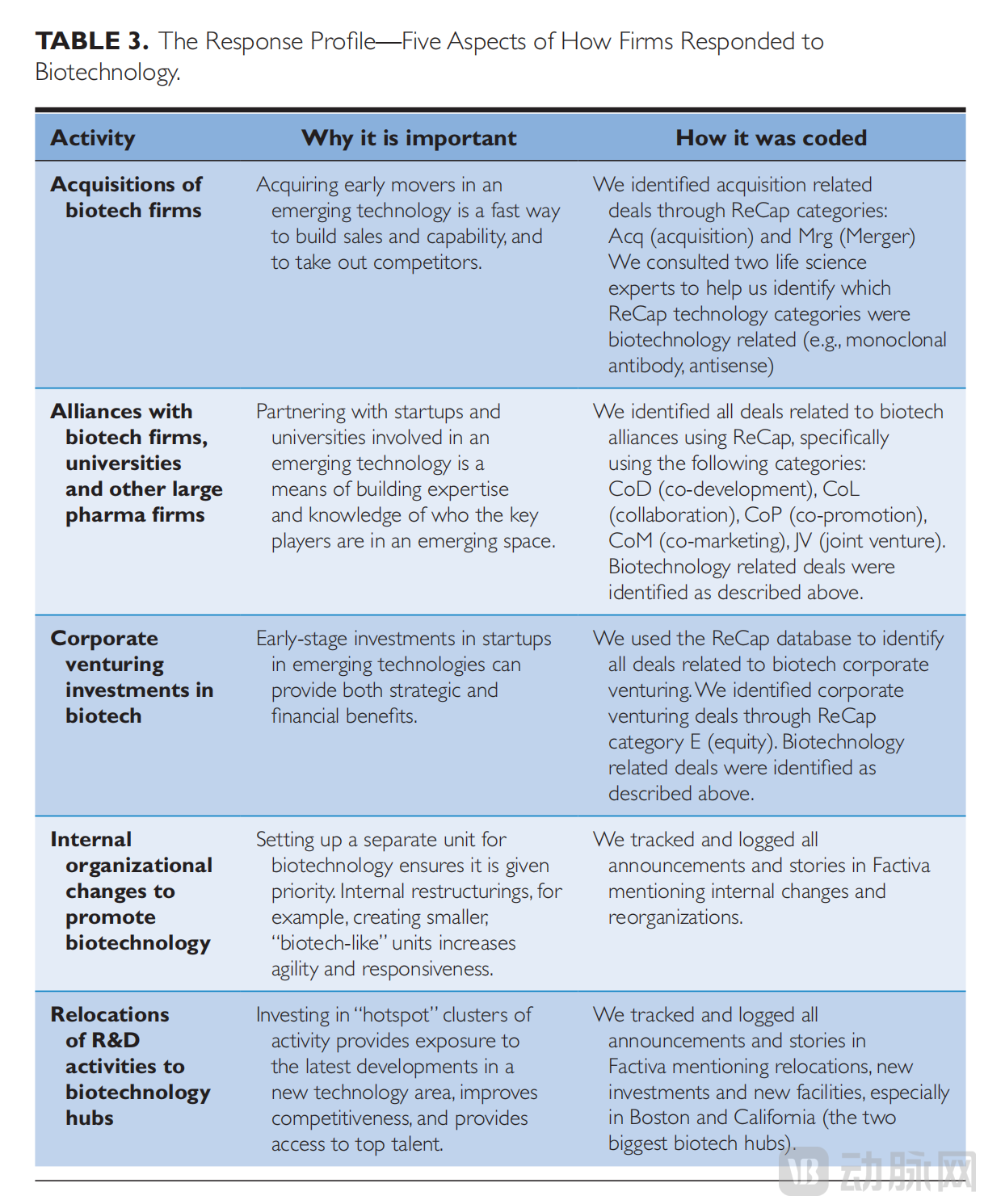

We have defined two phases:The First WaveFromThe biotech crash from 1990 to 2000 and to 2001,The Second WaveFromFrom 2002 to 2013. The response model shows how each company deals with biotechnology as a potentially disruptive technology.It covers five dimensions. The first three dimensions focus more on external activities, while the last two dimensions are more internally oriented.The following table details these models and their significance.

Note: The table shows each company's response to biotechnology as a potentially disruptive technology, with a total of five approaches: 1. Acquiring biotech companies. 2. Forming alliances with biotech companies, universities, and other large pharmaceutical companies. 3. Corporate venture capital investments in the biotech sector. 4. Promoting internal organizational changes in biotechnology. 5. Shifting R&D activities to biotech hubs. The importance of these five approaches is also analyzed, along with how the author collected this information.

Early Movers

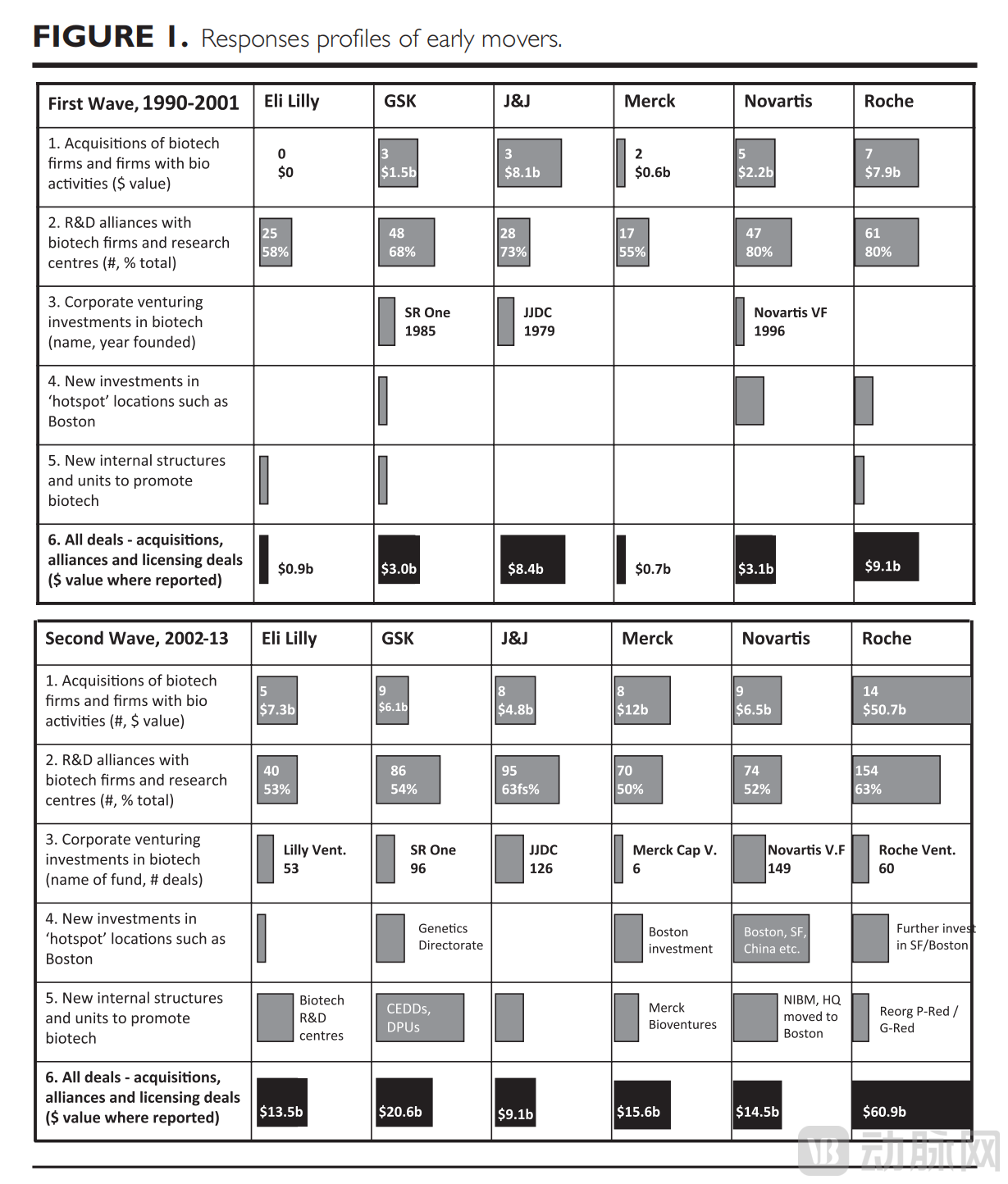

The early actors include Eli Lilly, GSK, Johnson & Johnson, Merck, Novartis, and Roche.

Eli LillyInvesting in biotechnology as a continuously evolving technology, and as early as 1987, began generating revenue from Humulin R (insulin) and Humatrope (growth hormone). In 1986, Eli Lilly made its first major acquisition by purchasing Hybritech, a monoclonal antibody company based in San Diego, for $350 million, but sold it a decade later for $10 million. In the early 1990s, Eli Lilly established a series of collaborations with external partners in genomics and proteomics. In 1997, Chief Operating Officer Sidney Taurel publicly stated that the company needed to shift its strategic thinking, integrating its core technologies with biotechnology and other companies' technologies as a powerful method for new drug development. However, sales based on biotechnology remained relatively small overall.

Entering the 2000s, Eli Lilly and Company continued with a sustainable development approach, making a series of publicly announced investments, such as the $225 million facility in Indianapolis in 2002, the Indiana Center for Applied Protein Sciences (INCAPS) in 2004, and a center in San Diego in 2009. They also carried out several medium-sized acquisitions (Applied Molecular Evolution in 2003, ImClone in 2008, and Alnara in 2010) and created a fund named Lilly Ventures, which made 53 investments. During this period, there was no lack of expression of determination towards biotechnology. However, despite some successful drug launches (e.g., Tanezumab for osteoarthritis), a series of seemingly promising drugs for Alzheimer's disease failed in late-stage trials. As a result, during the research period, Eli Lilly only had a moderately successful biotechnology-based product portfolio.

In the 1990s,GlaxoSmithKline PLC (GSK)Established. Among the constituent companies, Smith Kline made early investments in vaccine development, bioinformatics, and genomics, while Glaxo Wellcome acquired the biopharmaceutical company Affymax Inc. in 1995 (Affymax: released Omontys in 2013 for anemia treatment, which led to multiple deaths, after which the company gradually declined). The following year, Glaxo Wellcome established a Genetics Directorate with a budget of £30 million. During this period, there were 12 acquisitions and 48 external alliances involving the biotechnology sector, and SmithKline's venture capital fund, SR One, also actively invested in these new technologies. Overall, the founding companies of GSK were among the most active players in the biotechnology field in the 1990s.

In the early 2000s, GlaxoSmithKline (GSK) undertook an ambitious internal reorganization, dividing into six "Centers of Excellence for Drug Discovery," and creating "an R&D organization capable of leveraging the best features of both large pharmaceutical companies and small biotech firms." These semi-autonomous units consisted of 300 to 350 scientists focused on specific disease areas. By 2008, they were further broken down into 38 Pharmaceutical Performance Units, each comprising around 40 people. Additionally, there were 50 similar units collaborating with external entities. During this period, GSK made several medium-sized acquisitions, notably Corixa in 2005, Domantis in 2006, and Human Genome Sciences in 2012.

In terms of output, compared to its competitors, GSK has launched more biopharmaceutical drugs in the market but lacks any blockbuster drugs. This issue may stem from its fragmented internal structure. Overall, despite many influencing factors during this period, GSK's performance in the 2000s was relatively weak.

Compared with other early entrants,Johnson & Johnson (J&J)The business scope is broader, with only one-third of its revenue coming from its pharmaceutical subsidiary, Janssen-Cilag. Although it lacks the high commitment to basic research seen in some competitors, Johnson & Johnson has a well-established venture capital division (J&J Development Corporation, JJDC) and external collaborations, achieving early successes including the development of Procrit (EPO) in partnership with Amgen. In 1998, Johnson & Johnson acquired the highly regarded biotechnology company Centocor for $4.9 billion, making biotechnology an essential part of the company’s overall strategy. Centocor, which had two approved drugs and a robust R&D pipeline, was granted significant operational autonomy, and its former CEO, David Holveck, became the president of JJDC.

Many of Johnson & Johnson's successes in the 2000s can be attributed to its acquisition of Centocor, with the monoclonal antibody drugs Remicade and Simponi becoming blockbuster medications. Johnson & Johnson made several medium-sized acquisitions, particularly the purchases of Elan and Crucell in 2009, which strengthened their position in antibody research and immunotherapy. At the same time, internal organizational changes were implemented. In 2012, Johnson & Johnson established four innovation centers in Boston, California, London, and China.

As a science-oriented company,Merck & Co. (USA)In the 1980s and 1990s, investments were made in biotechnology and other technologies, and early revenue was generated during this period from biotechnology-based vaccines. Compared to other early entrants, Merck's operations in the United States were more moderate, without significant acquisitions and with fewer external partnerships. Its only major acquisition was the purchase of Rosetta Inpharmatics in 2001.

Merck & Co., Inc. (USA) established a venture capital fund (Merck Capital Ventures) in 2000 and has continued to selectively invest in biotech alliances. Beyond this, Merck has also made several small-scale acquisitions as well as one large-scale acquisition, the 2009 purchase of Schering-Plough, which included investments in immunotherapy that ultimately led to the launch of the cancer drug Keytruda. Some internal structural changes were also implemented, including the establishment of a 500-person unit in Boston in 2004. Overall, Merck did not take any bold steps, but its biotech activities have continued to grow steadily.

NovartisFormed by the merger of Sandoz and Ciba-Geigy in 1996. Prior to this, Ciba-Geigy acquired 49.9% of Chiron, one of the early success stories in biotechnology, for $2.1 billion, while Sandoz acquired Systemix, a specialist in blood disorders. Not long after the merger was completed, CEO Daniel Vasella further committed to investing in biotechnology, prioritizing investments in North America over Switzerland. He established the Novartis Venture Fund in Boston, invested $28 million in biotechnology in North Carolina, and in 1998 pledged $250 million for the Novartis Functional Genomics Institute in California, stating: "We need to improve collaboration with other scientists." In 2000, Vasella announced an additional investment of $58 million in genetic research therapies: "You can't spread resources across many small initiatives and compromise on the big bets you take." Most of Novartis' acquisitions and deals have focused on cutting-edge gene therapies.

Novartis underwent a significant restructuring in 2002, relocating its global R&D headquarters to Boston and establishing a series of Novartis Institutes for BioMedical Research (NIBRs) in Boston, California, and Basel. Subsequently, research institutes were also set up in China, Singapore, and India. Novartis acquired the remaining shares of Chiron and carried out a series of smaller acquisitions. During this period, the Novartis Venture Fund made 149 investments.

RocheActive in the biotechnology field before 1990 through the pioneering work of immunologist Georges Kohler, early collaboration with Genentech, and the establishment of the Roche Institute of Molecular Biology. In 1990, when Genentech decided to sell its shares, after Merck and several other companies declined, Roche stepped in and purchased a controlling stake for $2.1 billion. Throughout the 1990s, Roche continued to invest in the biotechnology sector, engaging in extensive external collaborations and acquisitions with multiple companies, including the $5.1 billion acquisition of Syntex (1994) and obtaining exclusive rights to the polymerase chain reaction (PCR) technology—a technique for amplifying genetic material samples—from Cetus (1991). Internally, changes were also made as the head of the R&D department aimed to grant greater autonomy to laboratories: "We want decisions to be made by those who understand the problems."

In the 2000s, Roche continued to place biotechnology at the core of its strategy. In 2008, Roche acquired a minority stake in Genentech and purchased several other medium-sized biotech companies. Roche Venture Fund was established in 2002, and throughout the 2000s, Roche engaged in more strategic alliances than its competitors. Internally, Genentech continued to operate with a high degree of autonomy. By the end of this period, Roche was the most successful among our 12 companies in biotech sales, with three blockbuster drugs, all originating from the acquisition of Genentech.

Overall, these six early entrants have all made significant investments in external collaborations, with the exception of Merck & Co., which has not engaged in major acquisitions. However, there are notable differences in their approaches to biotechnology. Three European companies—GSK, Novartis, and Roche—as well as Johnson & Johnson, placed bolder bets on biotechnology during the 1990s, while Eli Lilly and Merck & Co. adopted a more conservative stance. It is worth emphasizing that these "bold bets" took various forms: Johnson & Johnson focused on monoclonal antibody-based products and late-stage development opportunities; Novartis concentrated more on gene therapies and early-stage opportunities; GSK conducted the most acquisitions but covered a broader range of technologies compared to others; Roche made the largest financial commitment through its acquisition of Genentech.

In the 2000s (the second wave), all six of these early entrants continued to heavily invest in biotechnology. Novartis and Roche both increased their previous investments in the United States, with the former relocating its R&D headquarters to Boston and the latter paying $47 billion to acquire the remaining shares of Genentech. GlaxoSmithKline (GSK) undertook a bold internal restructuring to create a "biotech-like" working approach, but the results were mixed. The three U.S.-headquartered companies continued along their existing trajectories, with Johnson & Johnson and Merck achieving strong positions, while Eli Lilly lagged behind.

Note: The table shows the changes in six aspects for six companies that entered the biotechnology field early, during the periods of 1990-2001 and 2002-2013: 1. Acquisition amounts of biotech firms and companies with bio-related activities. 2. Number of R&D alliances with biotech firms and research centers. 3. Corporate venture capital investments in the biotechnology sector. 4. New investments in "hotspot" areas such as Boston. 5. Establishment of new internal structures and departments to promote biotechnology. 6. All deals [acquisitions, alliances, and licensing deals (value in USD)].

Latecomer

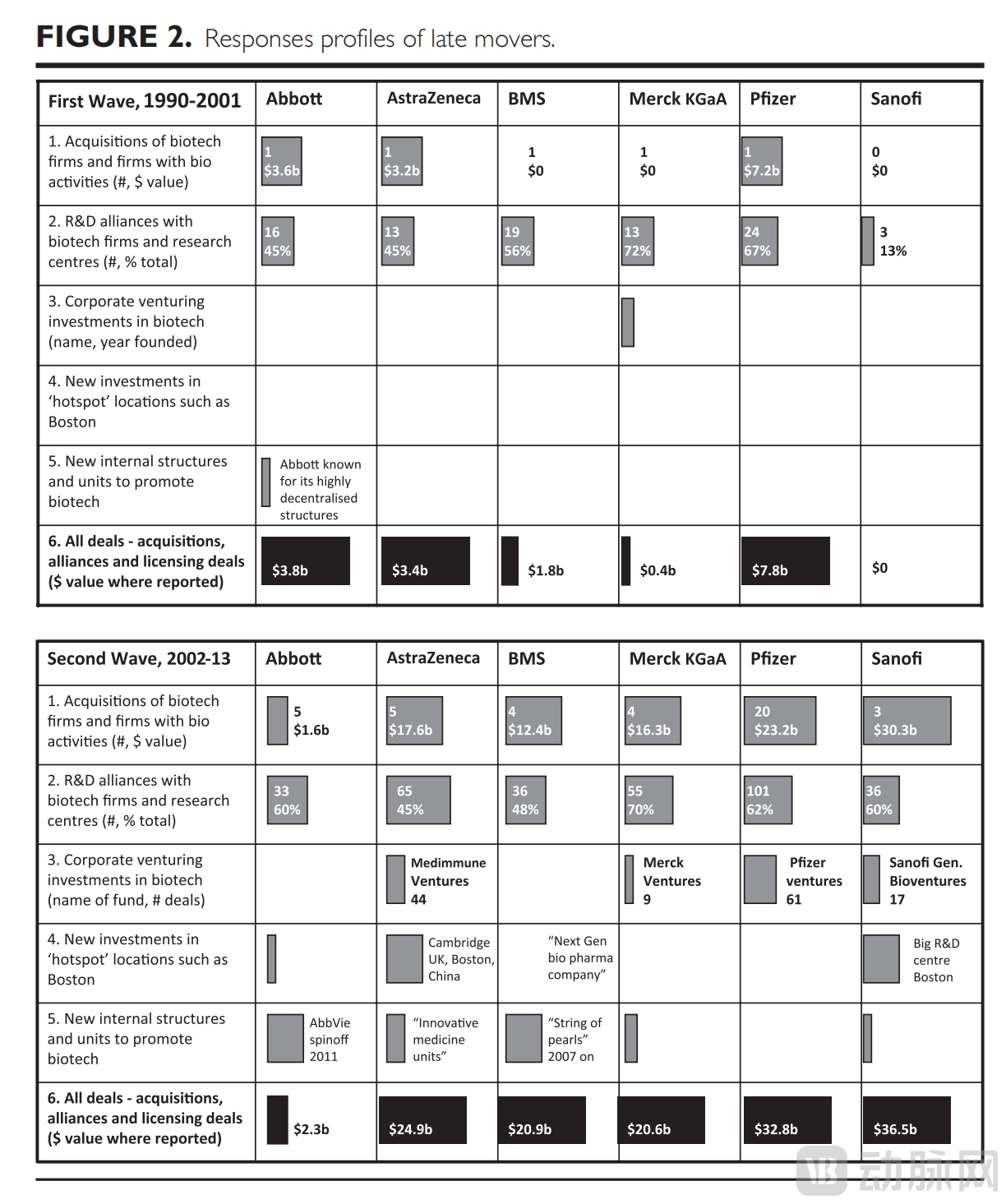

Although the latter six large companies invested in biotechnology relatively late, from the perspective of biotech drug sales, not until 1999 or later, they made some initial small-scale investments through strategic alliances and university collaborations during the 1990s. Then, in the 2000s, they all worked hard to catch up, but with varying degrees of success.

AbbottIn the 1990s, some tentative biotechnology efforts were made, with the first drug Synagis reaching the market in 1999 following three small-scale acquisitions. Among the R&D projects, there were also external biotechnology-based collaboration initiatives. Just as this period was coming to an end, in 2001, Abbott acquired Knoll, the pharmaceutical division of German chemical company BASF, for $6.9 billion. This acquisition was aimed at scaling up: "to consolidate key capabilities in drug research and strengthen the sales force." However, as part of the deal, Abbott also recognized that it was acquiring "leading monoclonal antibody technology," which held promise for use in rheumatoid arthritis. The product, named Humira (adalimumab), became the world’s best-selling drug, accounting for over 60% of Abbott's total pharmaceutical sales.

Abbott has made several medium-sized acquisitions and pursued a series of strategic alliances but has not established a corporate venture capital division. Among later investors, it has focused the least on external investment activities, possibly due to the success of Humira (adalimumab). In 2011, Abbott spun off its entire biopharmaceutical business to form AbbVie, reserving its own brand for traditional diagnostics and consumer health businesses.

AstraZenecaIt was established in 1999 through a merger. Astra once owned 20% of Cambridge Antibodies Technology (CAT), and Zeneca formed a pharmacogenomics group in 1997. Throughout this period, biotechnology was mentioned as a high-potential field in annual reports. However, a closer look at the deals completed during this time reveals that they were all relatively small in scale (all below $50 million) and did not result in any successful product launches. Two interviewees noted that during this period, some senior biotechnology experts left the company due to disappointment, as they felt their R&D efforts were not receiving the high-level commitment they deserved.

Until 2005, AstraZeneca continued to make small-scale biotech investments without a clear commitment or any successful drug launches. In 2006, new CEO David Brennan took office, facing the expiration of patents for several key drugs. He made a significant commitment to biotechnology by acquiring CAT for $1 billion in 2007 and MedImmune for $15.6 billion in 2008. These acquisitions subsequently led to internal reorganization, with Cambridge (UK) becoming the new R&D headquarters. New investments were made in Maryland, Boston, and China, while the old R&D center in Manchester (UK) was closed.

Despite all this investment, AstraZeneca still lags behind its rivals in sales based on biologics. In 2014, new chief executive Pascal Soriot fended off a hostile takeover from Pfizer, promising a clutch of new drugs in the immunotherapy field. By 2015, they still looked promising.

Bristol-Myers Squibb (BMS)In the 1990s, some strategic cooperation was carried out, mainly in the early development of monoclonal antibodies. In 1997, the company’s strategy changed as it invested $60 million into a biotechnology development center and hired Elliott Segal as the Vice President of Applied Genomics. This foray into biotechnology led Bristol-Myers Squibb (BMS) to invest in ImClone in 1999, but the approval of its key drug, Erbitux, took longer than expected. Subsequent insider trading scandals caused significant problems for BMS, resulting in losses exceeding $1 billion and years of negative publicity.

After experiencing painful lessons, Bristol-Myers Squibb did not make significant biotech investments in the following years. In 2004, they formed an alliance with Medarex and later acquired it in 2009. In 2005, new CEO Andreotti and R&D head Elliott Segal signaled a major strategic shift, intending to transform Bristol-Myers Squibb into a "next-generation biopharmaceutical company." They carried out a series of medium-scale acquisitions, completing 11 purchases from 2007 to 2012, known as the "string of pearls" strategy. Bristol-Myers Squibb also made some internal investments, particularly with a $750 million investment in the Boston area. An industry magazine noted that Bristol-Myers Squibb "has largely executed its 'string of pearls strategy' effectively and has a positive track record in discovering these opportunities."

Merck KGaAIn the 1990s, there were no significant biotech investments, apart from two medium-scale regional distribution alliances established with ImClone in 1994 and 1998. Although they had some small partnerships and alliances, these did not result in any new products or biotechnology-based sales.

At the beginning of the 21st century, Merck of Germany did not show significant interest in biotechnology. In 2005, Merck acquired Survac, a small Danish biotech company, and a year later, purchased Serono, headquartered in Geneva, for $13.1 billion. The global R&D headquarters was relocated to Geneva, and the deal also brought an investment arm, Merck-Serono (MS) Ventures, headquartered in Amsterdam. Merck CEO Michael Roemer stated, "This acquisition transformed Merck's pharmaceutical business and created a leading position in the biopharmaceutical field." Subsequently, Merck made two more major acquisitions: Millipore in 2010 and Sigma-Aldrich in 2014, which enabled the company to develop capabilities in monoclonal antibodies and stem cells.

In the 1990s, Pfizer did not make any significant biotechnology investments, although it had some external collaborations with biotech partners. The company was highly successful during this period, driven by blockbuster chemically-based drugs such as Lipitor and Viagra. Its acquisition of Warner-Lambert in 2000 included a small biotech operation, Agouron, but Pfizer’s first biotech-related revenue did not occur until 2003.

PfizerIn the early 21st century, Pfizer continued to carry out large-scale acquisitions, purchasing Pharmacia & Upjohn (in 2001) and Wyeth (in 2009), and attempted (but failed) to acquire the Irish pharmaceutical company Allergan and the British pharmaceutical company AstraZeneca in the 2010s. However, these acquisitions were based on integration and scale rather than a bet on biotechnology. Pfizer's first biologic was a growth hormone obtained as part of the Pharmacia & Upjohn acquisition, but in the early 21st century, Pfizer remained ambivalent about biotechnology. In an interview, Pfizer CEO Hank McKinnell observed: "The sequencing of the human genome in 2000 raised high hopes for new drugs, but those hopes have yet to be translated into marketable new medicines."

Sanofi (Sanofi)Changes occurred in the 1990s and early 21st century, resulting from the mergers of Hoechst, Rhône-Poulenc Rorer (earlier consolidated into Aventis), Sanofi, and Synthelabo. However, considering the backgrounds of these founding companies, there was no significant evidence of biotechnology activities during this period, aside from a few external partnerships and collaboration with the French government on a biotechnology fund in 2004.

The leadership change in 2008 led to a significant shift, with their strategic alliance with Regeneron significantly expanded. In 2009, a major investment in cancer research was made in Boston, followed by the $20 billion acquisition of San Francisco-based Genzyme in 2010. New CEO Chris Viehbacher pledged to fully leverage Genzyme’s R&D capabilities, making it the "tail wagging the dog" — a proverb meaning that the acquired company provides value and benefits to the larger company, similar to what Genentech did for Roche. However, he faced resistance from traditional internal R&D organizations in France and Germany, which were supported by their national governments and a Europe-centric board.

Overall, observing these six latecomers reveals several noteworthy patterns.First, none of them completely ignored biotechnology—during the 1990s, they made some small-scale "seed" investments, usually through external collaborations or minor acquisitions within a broad R&D investment portfolio. Compared to early movers, the latecomers were distinguished by their reluctance to make significant investments in this emerging technology. This ties into the second point: during the 1990s, the CEOs of these latecomers did not fully recognize the potential of biotechnology. Among the six latecomers, Bristol-Myers Squibb and Abbott were the only companies that "realized" the potential of biotechnology in the first phase (i.e., the late 1990s).

Third, there is a significant element of luck involved here. For instance, Bristol-Myers Squibb made a major bet in the biotech field (ImClone), which ultimately led to an insider trading scandal, whereas Abbott completed an acquisition primarily based on scale and global influence, gaining a blockbuster drug—Humira (adalimumab).

Note: The table shows the changes in six aspects for six companies that entered the biotechnology field later during the two periods of 1990-2001/2002-2013: 1. Acquisition amount of biotech companies and companies with bio-related activities. 2. Number of R&D alliances with biotech companies and research centers. 3. Corporate venture capital investment in the biotechnology sector. 4. New investments in "hotspot" areas like Boston. 5. Establishment of new internal structures and departments to promote biotechnology. 6. All transactions [acquisitions, alliances, and licensing deals (value in USD)].

Why Did 6 Early Movers Perform Better?

What impact have biotech investments and activities had on the market positions of these companies? By the end of the first wave of investment, around the early 21st century, no clear pattern had emerged: it was still too early to tell whether these early investments would pay off.Reviewing the news commentary of the time, there were concerns about the science ("Early results of clinical efficacy of gene therapy are disappointing") and the companies being created ("If success has many fathers, and failure is an orphan, then this still-young biotech community might be opening an orphanage").

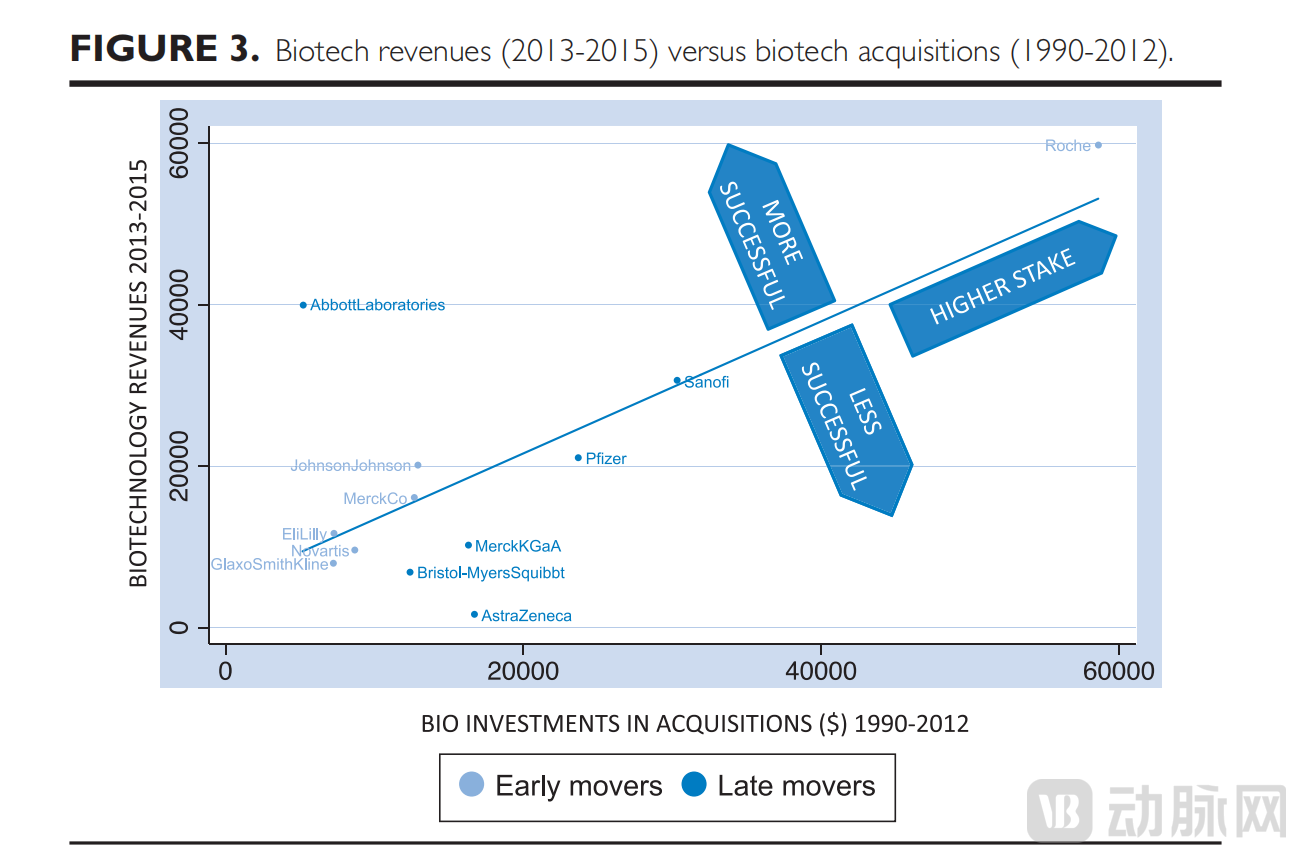

By contrast, in the 2010s, a clear pattern is emerging. Five of the six latecomers have placed biotechnology at the core of their strategy (with the exception of Pfizer), and all but AstraZeneca have derived substantial revenue from biopharmaceuticals.However, despite such positioning,These latecomers did not perform as well as the early investors.The figure below shows evidence linking the total amount spent on biotechnology-related acquisitions over 22 years to the average revenue of biologics between 2013 and 2015 (i.e., at the end of the study period). As expected, there is a strong positive correlation between the two. Interestingly, early investors are all located on or above the trend line, indicating better returns on their investments (with the exception of Abbott, which is mainly due to Humira).

Note: The comparison between the vertical axis [Biotechnology Revenue (2013-2015)] and the horizontal axis [Biotechnology Acquisition Amount (1990-2012)].

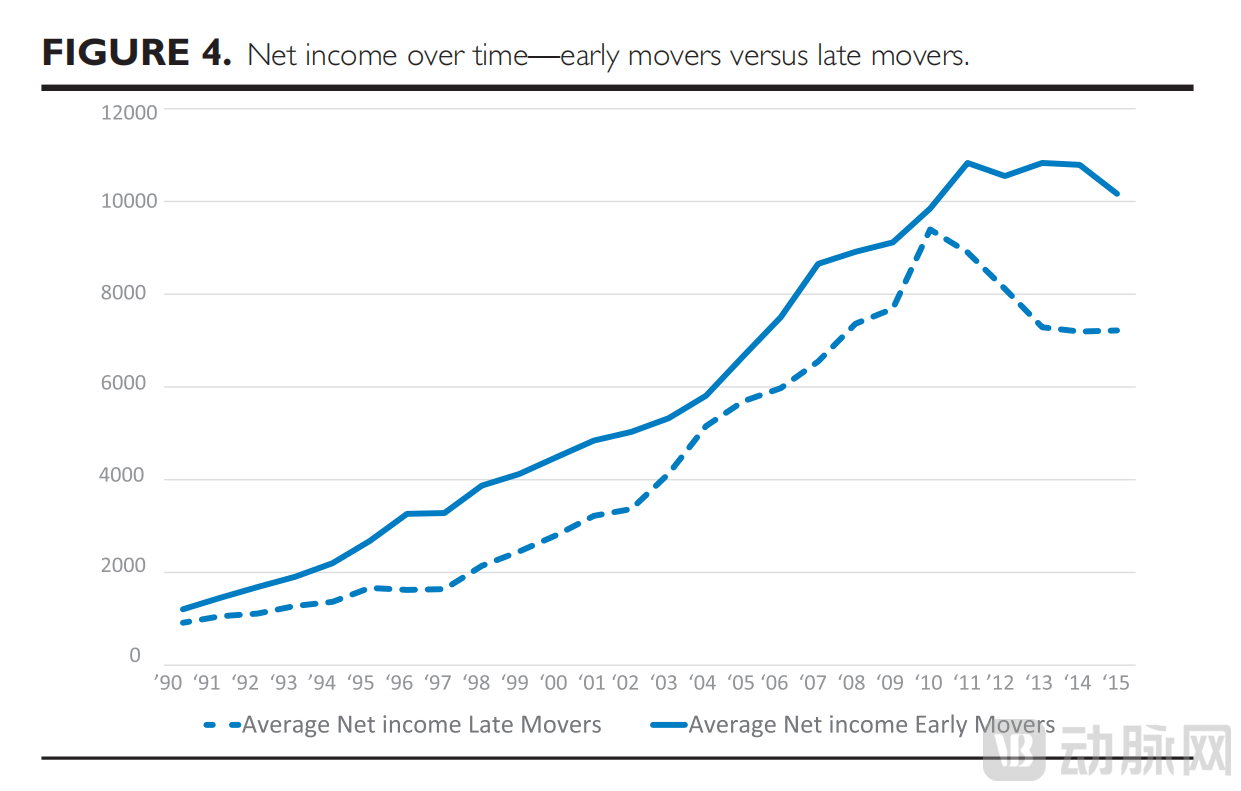

Note:Net income over time for early entrants (solid line) compared to latecomers (dashed line).

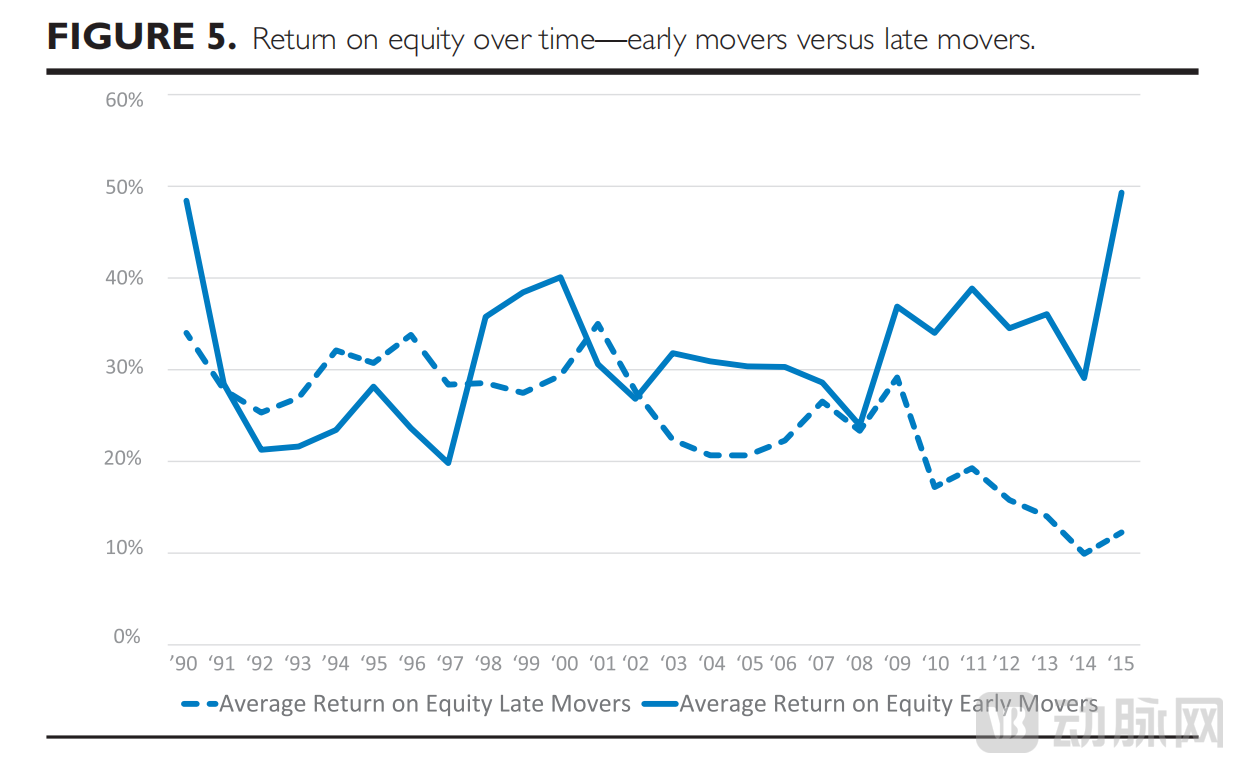

Note: Over time, the return on stock also changes constantly, comparing early entrants (solid line) with latecomers (dashed line).

Our research question is, how do incumbent firms respond to potentially disruptive technologies?Before integrating all research findings into a comprehensive framework, we offer some general observations.

First, companies have reacted to potentially disruptive technologies in a variety of ways. This is not particularly surprising, but it is worth noting that, perhaps due to the gradual emergence of opportunities and challenges in biotechnology, the timing and manner of responses have been diverse. There are early investors, late investors, and non-investors. Among early investors, some companies emphasize acquisitions or alliances, while others focus on internal structural changes. In the 1990s, these different approaches did not converge; it was not until the mid-2000s that some convergence began to appear.

Secondly, small-scale early investments in emerging technologies did not significantly impact subsequent success. There is a perspective that, when faced with emerging technologies, companies should adopt a "real options" approach (introducing the rules of financial markets into internal corporate strategic investment decisions for planning and managing strategic investments), making small-scale investments (e.g., alliances or R&D projects) and scaling up at the right time. However, our data shows that all 12 companies established a series of strategic alliances in the 1990s.Therefore, the connection between these small-scale investments and the subsequent large-scale biotechnology investments, which are often made many years later, tends to be very weak.

We agree that small-scale investments are useful first steps in perceiving and responding to emerging technologies. However, they seem to have little significant impact on subsequent decisions to heavily invest in the technology. In other words, many latecomers made "symbolic" investments in biotech projects during the 1990s, but these investments were often overlooked by senior management. Based on our expert interviews, the executives involved typically had a business background rather than a scientific one. When asked to allocate small amounts of funding to biotech projects, they did not object, but it was not until the evidence (in the 2000s) became overwhelmingly strong that they regarded biotechnology as a major strategic priority.

Third, there is no one-size-fits-all response to potentially disruptive technologies. Previous research has suggested that, for incumbent firms, creating a separate business unit is the optimal approach to leveraging disruptive technologies. However, our research focuses on how companies respond to potentially disruptive technologies over time, revealing a more nuanced perspective. For instance, there is little evidence that establishing separate divisions for biotech R&D is helpful. Moreover, early investments in strategic alliances, as mentioned above, show no correlation with subsequent success.

Fourth, not all large-scale investments can be successful. This is not particularly surprising, as any environment with high uncertainty will lead to some investments succeeding while others fail. However, it is important to emphasize that our data does not support the argument that "the bold will always win." Some companies made significant investments early on and achieved excellent results, such as Johnson & Johnson and Roche's large-scale acquisitions in the 1990s, and Novartis' major investment in Boston in 2002. But there are also examples of less successful large-scale investments, such as GSK's Center of Excellence for Drug Discovery and Bristol-Myers Squibb's early investment in ImClone.

So, what general conclusions can we draw about how to better address potentially disruptive technologies?

FirstWe observed that early movers had an advantage: the six companies that made significant early investments in biotechnology eventually outperformed the six latecomers (despite a long time lag).Based on our analysis and interviews, there seem to be three interconnected reasons.

First, the ability to develop biologics takes years to cultivate, so investments made in the 1990s would appreciate over time. In other words, for companies trying to catch up, there is a relative disadvantage of time compression, which is difficult to overcome even through aggressive external strategies such as acquisitions.

Second, strong internal biotechnology capabilities enable companies to better determine when to make acquisitions. Early movers give themselves the opportunity to evaluate and acquire the most attractive biotech companies, while latecomers often haven’t even considered these issues. Between 2005 and 2012, many biotech companies were sold at very high prices, and according to our expert interviews, these were often cases where latecomers paid a premium to gain a foothold in the industry.

Third, early movers have a signaling effect, meaning that top scientists and emerging biotechnology companies tend to favor firms that explicitly emphasize their positive stance on biotechnology. In future research, it would be interesting to explore the relative importance of these mechanisms in shaping the advantages of early movers.

The key here is that the early actors did not gain an advantage through their small-scale initial investments (since we know all 12 companies made such investments), but rather by gradually building knowledge and expertise in this emerging technology field while closely monitoring its development. It is the building of capabilities, rather than awareness, that made the difference.

Secondly, for emerging technologies, adopting an "open innovation" approach is more effective than doing it alone.Observing the more successful early movers, Roche and Novartis have respectively chosen San Francisco and Boston as the bases for their emerging biotechnology operations, while GSK and Merck have placed more trust in their existing scientists and locations. Biotech acquisitions generally yield positive outcomes, though the obvious warning about the risk of overpayment should not be overlooked. Early movers have also established venture capital arms ahead of latecomers, which is another significant indicator of openness.

Of course, an open approach to innovation is not just reflected in the acquisition of data, new office locations, and venture capital;At least within the company, it is more of a "mindset.", that is, the relationship between experts in traditional technology fields and personnel engaged in new technologies. For instance, according to our interviews,Roche has done well in embracing Genentech's way of working and giving them a prominent position post-integration, while Sanofi has struggled in its collaboration with Genzyme.How to manage disruptive changes internally, such as integrating old technical capabilities with new ones and overcoming resistance, is important but beyond the scope of this article. We encourage future research in this area.

Link these two points together,A notable characteristic of biotechnology in the 1990s was the limited number of scientists and entrepreneurs who truly understood its potential. For traditional pharmaceutical companies, the challenge lay in acquiring this limited pool of skilled talent.Most of them prefer to work in universities and startups concentrated in a few locations (such as San Francisco, San Diego, Boston, and Cambridge in the UK). Therefore, early entry into these agglomeration areas is an effective way to build capabilities. More broadly, this perspective suggests that the theory of first-mover advantage should incorporate geographical factors. It is acknowledged that early entrants benefit from temporal advantages and economies of scale in resources. Based on this study, we can conclude that these advantages are more pronounced when the supply of relevant expertise is limited and geographically constrained.

A Three-Step Process

As previously mentioned, we framed this research in terms of perception and response, an established two-step process, and created a response profile for each company to capture the various actions they took.

However, in conducting this analysis, it became evident that "responses" are more complex than previously understood. An important part of early actors' responses involves the gradual development of skills and capabilities to compete in this emerging technology field. The second key aspect of responses is the formation of senior management's perspective on industry developments (i.e., towards biopharmaceuticals) and driving a significant repositioning from traditional areas of strength. These are conceptually separate activities — capabilities can be built without a strategic shift, and a strategic shift can be pursued before foundational capabilities are established.

Therefore, we recommend a three-step approach to address potentially disruptive technologies. Sensing is the initial action of monitoring developments in relevant technological fields, serving as a means to establish awareness. The response involves investing in and experimenting with emerging technology areas, acting as a means to build capability. Scaling up includes prioritizing large-scale investments in the most promising technologies and overcoming internal resistance, serving as a means to establish commitment.

To reiterate our main findings, all companies in the sample attempted to build awareness, but there was significant variation in their efforts to establish biotech capabilities (response). Perhaps because biotechnology requires deep expertise accumulated over many years, early movers like Roche and Novartis were able to respond effectively—such as by acquiring or building key skills, pursuing good acquisition targets, and subsequently being able to establish commitment to new technologies within the company (extension). In contrast, latecomers (such as AstraZeneca and Merck KGaA) tried to build commitment to new biotech-based strategies without having previously established capabilities, made less wise acquisitions, and performed poorly. In summary, our argument is that when responding to potentially disruptive technologies, following a specific sequence of building awareness, capability, and commitment is more effective, while adopting a different order or subsets of these steps yields poorer results.

Notably, other studies on technological change typically focus on fast-moving industries such as disk drives, software, or telecommunications, where incumbent firms have only a few years to adapt. In these cases, the short timeframes mean that capability-building (coping) and commitment-building (scaling) are often conflated. In contrast, our choice to study a slowly evolving disruption allows us to separate these two steps and indeed highlight the intermediate step of capability-building as a crucial and challenging part of the process.

It should also be acknowledged that we haven’t fully resolved the question of which emerging technologies to focus on when it comes to potentially disruptive technologies. Clearly, too narrow a focus carries risks, but covering all possibly relevant technologies is expensive and impractical; a balance needs to be maintained. We believe the term “potentially disruptive” is helpful in this regard, allowing executives to have clear discussions about the scope of technologies that require active consideration, while remaining diligent in monitoring the development trajectory of each technology.

One advantage of our study is that we have examined a group of companies in detail over a long period. However, with only 12 companies, it is difficult to draw general conclusions. As mentioned earlier, there is a significant element of luck in the development of this industry. Related to this, the biotechnology revolution is not yet over, so if the research were conducted a decade from now, we might arrive at different conclusions rather than those based on the current state after 25 years of study.

Another limitation is that by focusing on large pharmaceutical companies, we have overlooked the role of biotechnology companies in shaping the industry. Companies like Amgen, Biogen, Genentech, Centocor, and Gilead made unique choices based on their capabilities and perspectives on industry development, which ultimately shaped opportunities for large pharmaceutical companies, especially in terms of acquisition targets. Notably, we only focus on companies in the U.S. and Europe, so we do not generalize this to other regions of the world.

How much can other industries learn from this one? People often think the pharmaceuticals industry is special because it takes a long time to develop new medicines and it’s highly regulated. But in some ways, it’s not very different from other industry settings. The newspaper and magazine industry, for example, is still adjusting to online news that emerged more than 20 years ago. It took 30 years for the story of Kodak’s bankruptcy due to digital imaging to unfold. And right now, we see car manufacturers in the midst of an adjustment to electronics, automation, artificial intelligence and alternative fuels – technologies that have been emerging for decades. The point is, it often takes many years for an emerging technology to mature, and its full effect on a well-established industry will only be clear in hindsight. For executives, understanding the likely length of the transition is an important consideration before deciding what course of action to take.

In summary,Our research highlights the complexity of how established companies in an industry respond to potentially disruptive technologies.. Although previous suggestions were not wrong in addressing this technological challenge/opportunity, they were often too narrow. Instead, we believe that companies should start from their response strategies — that is, the different approaches they need to take, the scope of investment, and how they evolve over time — to ensure that corresponding capabilities are built before making large-scale commitments to emerging technologies.

Reference: Responding to a Potentially Disruptive Technology: How Big Pharma Embraced Biotechnology;Julian Birkinshaw、Ivanka Visnjic、Simon Best;California Management Review,volume 60, number 3, pages 5-28;2018