Soaring 190% at open, Vigonvita makes blockbuster Hong Kong IPO debut

Vigonvita

New Drug Developer

The fervor surrounding Hong Kong's Chapter 18A biotech listings continues.

On November 6, Suzhou Vigonvita Life Sciences Co., Ltd. ("Vigonvita") successfully debuted on the Main Board of the Hong Kong Stock Exchange. Its stock price soared over 190% during early trading, reaching an intraday high of HK$97 per share. By market close, the shares settled at HK$82, representing a gain of over 145% for the day and giving the company a total market capitalization of approximately HK$13.7 billion.

Following the remarkable subscription performances previously set by Chinese innovative drugmakers like Leads Biolabs and TransThera, Vigonvita achieved exceptional investor demand during its public offering. The retail tranche recorded a staggering margin financing amount of HK$279.7 billion, reflecting an oversubscription rate of 4,974 times.

Image Source: Vigonvita Official Website

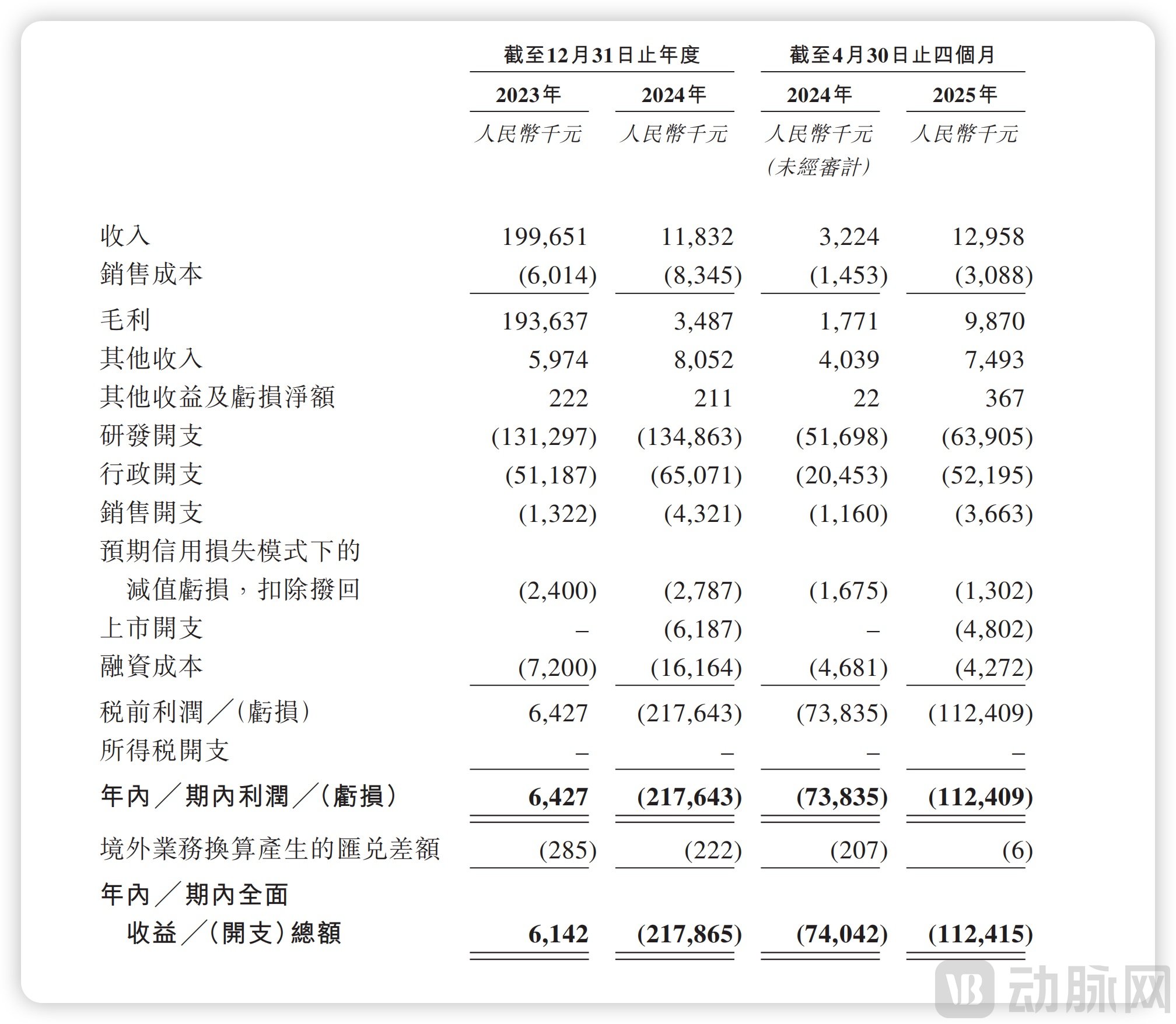

According to its prospectus, Vigonvita's revenue for 2023, 2024, and the first four months of 2025 was RMB 199.651 million, RMB 11.832 million, and RMB 12.958 million, respectively. Net profit was RMB 6.427 million, RMB -218 million, and RMB -112 million for the same periods. The company reported a profit of RMB 6 million in 2023, followed by a loss of RMB 218 million in 2024, and a further loss of RMB 112 million in the first four months of 2025.

This contrasts sharply with its warm market reception, highlighting significant volatility in its financial performance.

Vigonvita's story began in 2013 when its 51-year-old founder, Shen Jingshan, a doctoral supervisor at the Shanghai Institute of Materia Medica (SIMM) of the Chinese Academy of Sciences with over 30 years of experience in small-molecule drug research, decisively entered the innovative drug industry and established the company. This typical scientist-led startup is now experiencing the common biotech trajectory—transitioning from a market darling to facing financial pressures.

Vigonvita's ONVITA® (Simenafil Hydrochloride Tablets) serves as a crucial asset in its pursuit of capital market success.

In July 2025, Vigonvita gained approval for its novel erectile dysfunction (ED) drug ONVITA® (TPN171). The label of a "China-made Viagra" quickly redirected market attention to the company.

ONVITA® is regarded as a key product for achieving near-term commercial success and supporting the company's valuation. Positioned as a potential best-in-class PDE5 inhibitor, this ED treatment aims to disrupt China's male health market—a sector with an annual value exceeding RMB 10 billion, long dominated by global brands like Pfizer and Bayer, as well as Chinese generics—with its differentiated selling points of "efficacy within 30 minutes and compatibility with alcohol consumption."

According to the "Chinese Guidelines for the Diagnosis and Treatment of Andrological Diseases," the prevalence of ED among Chinese men aged 40 and above is as high as 40.5%. Data from CIC shows that the market size for ED drugs in China was only RMB 4.28 billion in 2019, reached RMB 9.3 billion in 2024, and is projected to grow to approximately RMB 15 billion by 2035. However, this market has long become a red ocean.

Historically, China's ED drug market was predominantly occupied by international brands such as Viagra (sildenafil), Cialis (tadalafil), and Levitra (vardenafil). Following the expiration of their patent protections in China, a wave of Chinese generic drugs has emerged. According to Pharnexcloud data, dozens of generic versions of sildenafil and tadalafil alone have received approval, indicating intensely fierce competition.

Yet, within this fiercely competitive market focused on price wars, a window of opportunity remains for differentiated products.

Currently, the majority of anti-ED generic drugs available in the Chinese market are older medications like sildenafil and tadalafil, with no novel mechanism drugs emerging. Consequently, market competition primarily revolves around pricing strategies. Particularly with the advancement of centralized procurement policies, this market is experiencing significant price fluctuations. For instance, the unit price of Qilu Pharma's Qianwei has dropped to just RMB 2.08 per tablet, while Baiyunshan Pharmaceutical's Jinge has also been reduced to approximately RMB 5. However, low prices alone cannot secure market share.

Baiyunshan serves as a typical case study. Its product Jinge achieved sales of approximately RMB 1.2 billion in 2023, yet revenue declined by nearly 20% just one year later. Baiyunshan publicly stated, "Nearly 50 companies in China have obtained sildenafil approvals, leading to increasing competition that has impacted the end market." Additionally, side effects such as visual abnormalities, muscle pain, and flushing, along with the hepatic and renal metabolism burden associated with high-dose generic drugs, are negatively affecting drug sales.

These pain points have naturally become the focal direction for Vigonvita's breakthrough efforts.

The R&D team discovered highly active flavonoids from the traditional Chinese medicine Epimedium extract. Through structural optimization, they developed the novel chemical entity simenafil, which exhibits PDE5 inhibitory activity seven times greater than sildenafil. This means a 2.5 mg dose can achieve efficacy comparable to the 50 mg dose of traditional drugs.

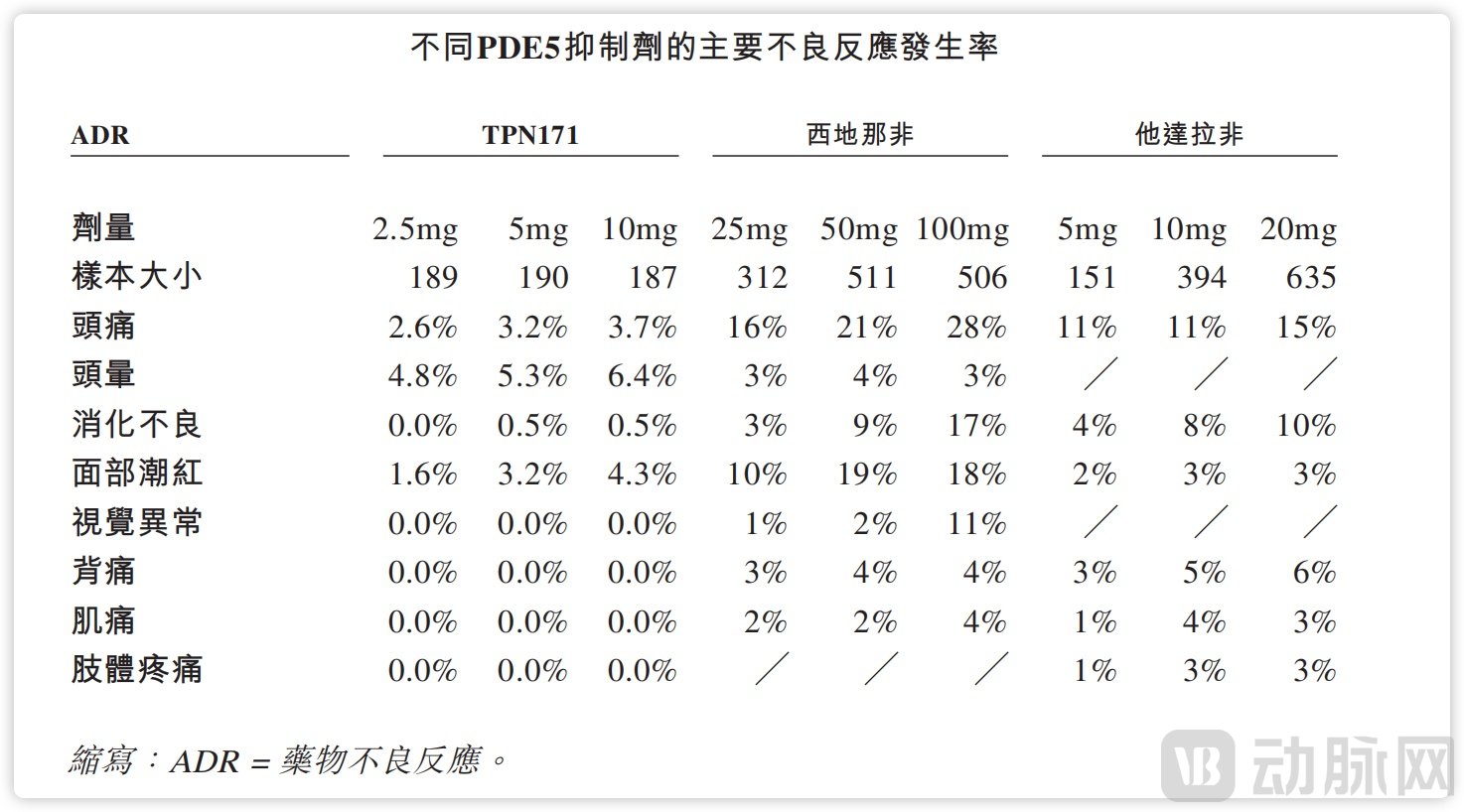

Pharmacokinetic data indicate that ONVITA® takes effect within 30 minutes after oral administration, with a half-life of 8 to 11 hours, and its efficacy is not affected by alcohol or high-fat food intake. Compared to Viagra, which requires avoiding alcohol for 3 hours before dosing, ONVITA® offers significantly higher compliance. Regarding side effects, its inhibition rate for PDE6 (vision-related) is 58 times lower than that of sildenafil, and it shows almost no inhibition of PDE11 (muscle-related). In the Phase III clinical trial, no instances of visual abnormalities or myalgia were reported, and the incidence of adverse reactions was comparable to the placebo group.

Incidence of Adverse Reactions to Anti-ED Drugs, Source: Prospectus

In a market saturated with anti-ED drugs priced under RMB 30, ONVITA® stands out with its launch price exceeding RMB 60 per unit.

This pricing strategy and marketing approach, which consistently benchmarks against Viagra, reflect Vigonvita's decision to compete on quality rather than engage in price wars. Particularly in the anti-ED drug market, where products offer similar efficacy, price is typically the primary consideration. However, a price premium becomes acceptable if a drug demonstrates superior effectiveness.

Given the intense market competition and the considerable challenge of maintaining market share, whether Vigonvita's strategy will ultimately succeed remains to be seen.

The market ceiling is limited, and commercial capabilities remain unproven.

Vigonvita was once a market darling. During the pandemic, it gained significant prominence with its COVID-19 antiviral drug VV116 and entered into a licensing agreement with Junshi Biosciences. According to its prospectus, Vigonvita's 2023 revenue reached a high of RMB 199.6 million, the majority of which came from a single licensing deal: the VV116 collaboration with Junshi Biosciences contributed RMB 184 million in milestone and transfer payments, accounting for 92% of its annual revenue.

VV116 is a nucleoside antiviral drug. Although initially held great promise, its revenue generation capacity rapidly diminished as the pandemic receded, and its commercial value has nearly vanished. Vigonvita is attempting to find a new lifeline for VV116 by pursuing a new indication for Respiratory Syncytial Virus (RSV) infection, which has entered Phase II/III clinical trials. However, the prospects for this development remain highly uncertain.

Recent revenue situation of Vigonvita, source: prospectus

This is reflected in its specific financials. In 2024, Vigonvita's licensing revenue plummeted by 97%, with full-year revenue reaching only RMB 11.83 million—a cliff-like drop. By the first four months of 2025, revenue had slightly recovered to RMB 12.96 million. Regarding net profit, driven by the substantial licensing income in 2023, the company recorded a net profit of RMB 64.27 million. However, in 2024, it returned to a loss-making position with a net loss of RMB 218 million, and in just the first four months of 2025, it had already incurred a net loss of RMB 112 million.

In other words, Vigonvita is currently in a typical biotech state characterized by high investment, low revenue, and sustained losses.

Despite this, following its Series C round in 2024, the company still achieved a valuation of RMB 4.45 billion, which may be attributed to its pipeline portfolio.

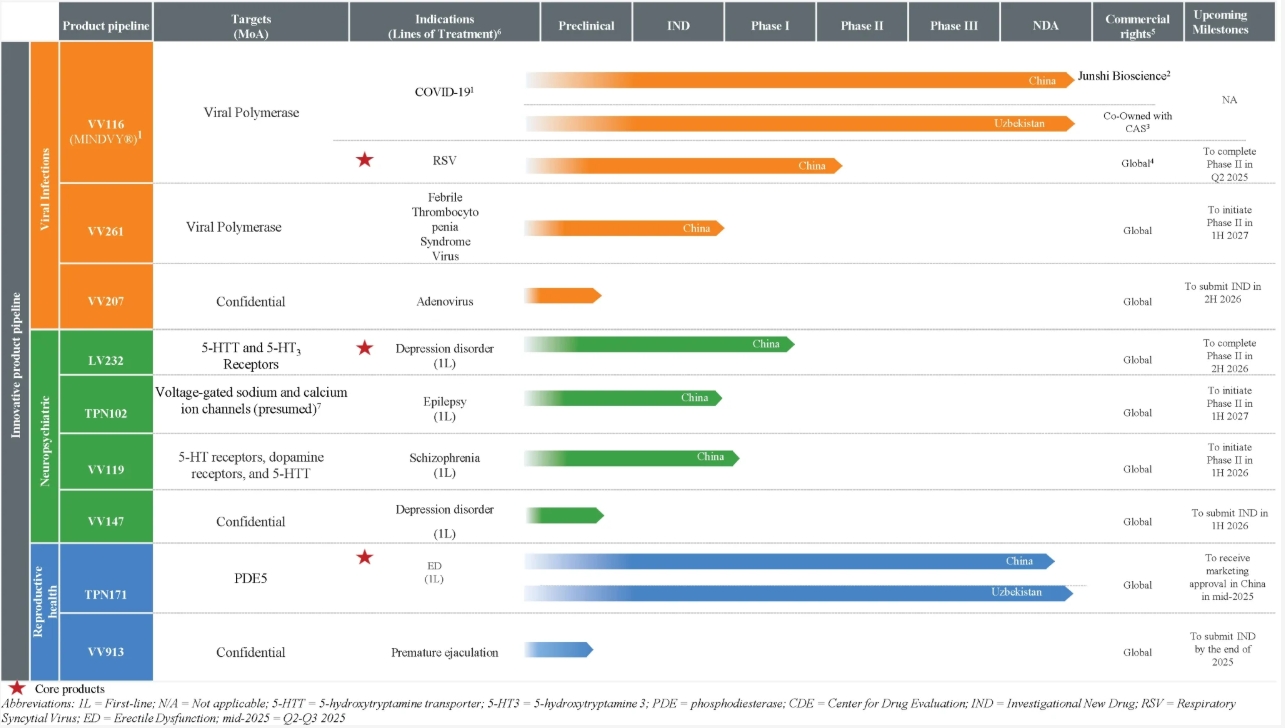

Vigonvita's Pipeline. Source: Prospectus

Beyond TPN171, the most advanced candidate in Vigonvita's R&D pipeline is the antidepressant LV232, a potential first-in-class dual-target modulator of the 5-HTT and 5-HT3 receptors. Leveraging its unique mechanism of action, the dual targets of LV232 function synergistically to enhance antidepressant efficacy while mitigating common gastrointestinal side effects such as nausea and vomiting. The drug initiated a Phase II clinical trial in China for depression disorder in April 2025.

It is noteworthy that although the antidepressant market presents substantial potential – with CIC projecting its size to reach RMB 18.8 billion by 2035 – it constitutes a fiercely competitive landscape populated by both established industry leaders and emerging innovators. CIC data indicates that over 20 innovative small-molecule antidepressants have already been launched in China, with nearly 20 additional candidates in Phase II or later-stage development. The Phase II trial for LV232 is anticipated to complete only in the second half of 2026, underscoring that a considerable journey lies ahead before potential regulatory approval, commercial launch, and profitable revenue generation.

Beyond these three core products, Vigonvita's pipeline also includes VV261 (a broad-spectrum antiviral nucleoside prodrug), TPN102 (a voltage-gated sodium/calcium channel inhibitor for epilepsy), VV119 (a multi-target serotonin-dopamine activity modulator for schizophrenia), VV207 (a novel oral nucleoside prodrug), VV147 (for depression), and VV913 (for premature ejaculation). The company also has several generic drug products.

This pipeline layout clearly revolves around three core therapeutic areas. According to CIC data, China's antiviral drug market reached RMB 20.3 billion in 2024 and is projected to grow to RMB 40.3 billion by 2035, representing a CAGR of 6.4%. The neuropsychiatric market is expected to expand from RMB 103.9 billion in 2024 to RMB 123.5 billion in 2035, while the reproductive health drug market is forecast to grow from RMB 36.2 billion to RMB 42.2 billion during the same period.

Overall, while the total market size of these three areas is substantial, their growth rates are moderate. Compared to hotly contested fields like oncology and autoimmune diseases, they attract relatively less industry attention. Regarding Vigonvita's current product strategy, the approved ONVITA® will be the decisive factor for its near-term development. However, as a scientist-founded company, Vigonvita's commercial capabilities in distribution and marketing remain unproven. Following its successful listing, whether the raised capital can effectively drive product commercialization and advance subsequent pipeline development will be the true test of its long-term viability.

When core products fade into obsolescence, how should a company respond?

The biotech sector consistently faces two fundamental challenges: securing funding and achieving commercialization. While a successful IPO may temporarily alleviate financial constraints, the subsequent hurdle of generating sustainable revenue remains. According to its prospectus, Vigonvita has identified four primary monetization pathways: out-licensing (primarily its COVID-19 drug developed in collaboration with Junshi Biosciences), CRO services, product sales (revenue from ONVITA®), and intellectual property transfers.

Prior to 2024, CRO services and out-licensing constituted Vigonvita's main revenue streams, leveraging the end-to-end capabilities across R&D, clinical development, manufacturing, and commercialization built over more than a decade. By 2025, however, intellectual property transfers and drug sales have become the dominant revenue contributors.

Concurrently, its GMP-compliant production facility in Lianyungang has officially commenced operations, while a Qingdao plant is currently in the design phase with expected completion by late 2026. While Vigonvita has demonstrably prepared for its commercial phase, these preparations alone may prove insufficient.

Setbacks followed by successful revivals are not uncommon among Chinese biotech companies, and we can glean insights from these cases.

Take Ascletis Pharma, which became the first company to list under the Chapter 18A rules as an "innovator in hepatitis C treatment." The sales of its core product, Ganovo (danoprevir), plummeted by 98% due to centralized procurement and changes in clinical treatment standards for hepatitis C. This forced Ascletis into a difficult transformation. While it briefly benefited from a pandemic-related product, the boost was short-lived. Its stock price declined steadily, and its market capitalization shrank by 95% to just HK$700 million.

During this period, however, Ascletis did not remain passive. It proactively overhauled its pipeline, discontinuing nearly all its previous focus areas—antiviral, oncology, and liver diseases—and channeling its limited R&D resources entirely into metabolic diseases. By differentiating its new product portfolio and demonstrating precise judgment in targeting next-generation drug candidates, the company regained market confidence. Its stock price recovered significantly, and its market capitalization now exceeds HK$9 billion.

Ascletis Pharma's transformation was remarkably decisive. When its core hepatitis C drug business shrank due to market competition and healthcare policy changes, it didn't cling to a sinking ship. Instead, it swiftly redirected R&D resources toward the GLP-1 weight-loss segment, then on the verge of explosive growth. This resolve to abandon past successful paths and embrace new trends was key to its recovery.

Similarly, Everest Medicines decisively pivoted away from its core oncology products at the time to focus on emerging areas like renal diseases and mRNA vaccines. This strategic shift paved the way for its current achievement: NEFECON now generates over RMB 500 million in monthly sales. Overall, these successful transformations share common traits: first, clearly defining resource allocation and prudently assessing capabilities; second, deeply exploring differentiated value in niche segments; and finally, pursuing out-licensing collaborations to accelerate new product commercialization.

Vigonvita shares several similarities with these companies. It became over-reliant on VV116, which had a brief period of success during the pandemic. Now, its antidepressant LV232 and ED drug ONVITA® face intense competition. Perhaps these successful pioneers have already offered some insights for those who follow.