Medical Sector Investment Slows: How Much Discount Are Startups Facing in Fundraising?

Intalight

High-end Ophthalmic Equipment Developer

Cornerstone Robotics

Innovative Surgical Robot Developer

EVAHEART

Cardiovascular Medical Device Developer

Dessight Biomedical

Developer of Microsurgical Robotics Platform

Six months ago, when the pandemic completely became"Past Tense", it is generally believed that the capital market will welcome a "winter gone, spring coming", and the investment and financing situation in the primary market will...2023The year was able to recover rapidly.

However, more than half of the year has passed, and the performance of the capital market is not consistent with expectations. According to the "2023 H1 Global Medical and Health Industry Capital Report" jointly released by VCBeat and VCBeat Research Institute, in the first half of 2023,China's healthcare industry financing and investment total approximately US$5.6 billion (approximately 41.051 billion RMB), a year-on-year decrease of about 43%.。Among them, the total financing amount in China's medical device sector decreased by 48% from the previous quarter.The significantly reduced financing amount means that the capital winter is still continuing.

Of course, the emergence of this phenomenon does not mean that the industry is in a desperate situation. Although the financing environment is not optimistic, there are still institutions actively investing.Institutions such as Qiming Venture Partners, CITIC Securities, Legend Capital, Sequoia China, Yida Capital, CICC Capital, YuanSheng Ventures, Shenzhen Capital Group, Haier Venture Capital, Lilly Asia Ventures, and Yuexiu Industrial Fund have invested in medical companies multiple times in the first half of the year. Among them, Qiming Venture Partners and CITIC Securities each made 16 investments.

Innovative companies still complete large-scale financing against the trendSuch as Haisen Bio completing $315 million in financing, Sangon Biotech completing 2 billion yuan in financing, Cornerstone Robotics completing 800 million yuan in financing, and EVAHEART completing nearly $100 million in financing;

Some niche areas are still booming.Such as the ophthalmic consumables sector with a total financing amount increasing 1501% month-over-month, the medical robotics track that attracted $600 million in the first half of the year, and fields like brain science and AIGC that have been heavily pursued by numerous investors…

Against this backdrop, what are the changes in the capital market in the first half of 2023? What trends do these changes reveal? Which tracks will investors focus on in the second half of 2023? When will the investment and financing market recover? To answer these questions, VCBeat interviewed several industry insiders.

All are talking about the capital winter, so how cold is the capital market in the first half of 2023?

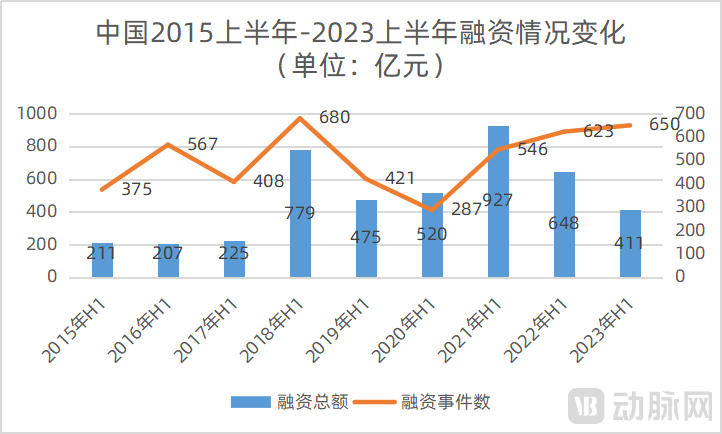

From the data, the total financing in the medical industry in the first half of 2023 hit the lowest point since the first half of 2018, with only 41.1 billion yuan, a decrease of 23.7 billion yuan compared to the first half of 2022, representing a decline of approximately 37%; and a reduction of 51.6 billion yuan compared to the peak period in the first half of 2021, marking a decrease of about 56%.

This data falls within the estimates of industry insiders. Xia Lin, Director of Medical Investment at Haier Venture Capital, stated, "The investment and financing situation in the medical industry has significantly cooled this year, with the investment amount in the first half of the year roughly being 1/3 to 1/2 of that in the first half of 2021."

Apart from data statistics, real cases in the primary market also reveal the chill in the capital market. According to an unnamed industry insider, there are now quite a few projects starting to seek financing at discounted valuations; some of these were star projects once highly sought after by investors and had completed multiple rounds of financing just a few years ago. Additionally, due to policy changes, macro-environmental factors, and more, the investment logic in certain niche industries has shifted—previous valuation systems no longer make sense. Some projects cannot find investors even after lowering their valuations. Meanwhile, for most companies that do manage to secure funding, their valuation growth remains relatively limited.

Although the total amount of financing in the primary market has plummeted, the workload of investors has not decreased. Several investors stated that investment institutions are still actively searching for new projects and seeking investment targets, while FA agencies are also recommending innovative projects in batches. However, most investors (investment institutions) are making decisions more cautiously than before, and many are even in a wait-and-see state.

For projects worth investing in, investors will also conduct more rigorous research than before making an investment. Moreover, the investment decision for a project often requires multiple investors to encourage each other. As a result, there are many projects in the market that have found multiple follow-up investors but cannot find a lead investor, causing delays or even suspension of financing.

This situation arose due to several factors: firstly, the severe capital bubble of the previous two years led to excessively high valuations for many projects, causing a significant inversion between the primary and secondary markets; secondly, an increase in the proportion of companies breaking below their issue price on secondary markets such as the STAR Market, ChiNext, and the Hong Kong Stock Exchange affected the exit strategies of investment institutions and investor confidence; thirdly, changes in policy and the broader environment caused abrupt shifts in the performance of numerous mainstream sectors, rendering past investment logic obsolete; and fourthly, the substantial reduction in dollar-denominated funds, with fewer funds now willing to commit to long-term investments.

"In the short term, the investment and financing environment will not improve significantly, and it will take time to digest and clear the bubble," said Xia Lin, Director of Medical Investment at Haier Venture Capital.

However, even though the investment environment is not optimistic, there are still many companies in the market that have successfully obtained financing.Junhe Alliance Bio completed two rounds of financing worth hundreds of millions in three months; Dessight Biomedical completed two rounds of financing worth tens of millions in half a year; Xiantong Pharmaceutical completed a new round of market-oriented equity financing exceeding 1.1 billion yuan…

Zou Guowen, founder of WinX Capital, revealed to VCBeat: "In the first half of the year, although the industry as a whole was relatively quiet, we completed the closing of 21 project financings relying on our professional capabilities, achieving a counter-trend growth in both number and amount compared to the same period last year."

Reviewing the financing situation in the first half of previous years, we found that:From the first half of 2020 to the first half of 2023, the number of investment and financing events in China's medical industry has been growing slowly.The number of financing events were 287, 546, 623, and 650, respectively. Among them, in the first half of 2023, the main distribution of financing rounds was in Series A and Series B, with 301 and 111 rounds, respectively. This indicates that investment scenarios are tilting towards earlier industry stages. Startups find it relatively easier to secure funding, while companies in the mid-to-late stages, which are entering commercialization but lack revenue data support, are facing increasing difficulties in financing.

Another dimension also supports the above view: the number of financing events is slowly increasing, but the total amount of financing has significantly decreased. Early-stage projects are relatively cheaper, but this also means that the average financing amount per project is notably decreasing. According to calculations, from the first half of 2018 to the first half of 2023, the average financing amounts were 114 million, 112 million, 180 million, 170 million, 104 million, and 63 million yuan, respectively.

Overall, investment institutions are increasingly inclined to invest early and small (Series A, Series B), with investors' (average) offers also decreasing from over 100 million yuan in the past to tens of millions of yuan. For companies in the medium-to-late stages, securing smooth financing relies more on gaining investors' approval regarding commercial prospects and commercial feasibility.

Against the backdrop of intensifying industry competition and sudden changes in the market environment, companies have a more urgent need for financing.

This is because major strategic layouts of enterprises often need to race against time. If one does not invest, competitors increasing their investment will seize the advantageous competitive position. At the same time, financing is not only about seeking financial support but also about gaining access to premium resources. However, high-quality resources in the market are scarce and limited, and if they are captured by competitors, one may fall into a precarious situation.

Zou Guowen, founder of VCBeat, advised companies: "Repair the roof while the weather is fine; prepare for a rainy day. Even if things are going smoothly and financial pressure is low at this moment, financing work must be taken very seriously. Once a track starts to gain attention from the capital market and an arms race begins, it must be carried through to the end. During this period, you can slow down the pace, think more, and adjust strategies, but you cannot stop. Stopping halfway like the rabbit in the tortoise and hare race is extremely dangerous."

In fact, although the current financing environment is not ideal, most companies still need to seek financing. It's just that different companies have different levels of urgency for financing.

Those enterprises with self-sustaining capabilities and those that received substantial financing in the past two years, their reserve cash flow can support for a long period, showing strong risk resistance. These companies are aware of the current financing environment and are not in urgent need of financing. Most choose to slow down the pace of financing, return to the essence of business, and focus more on the market, operations, and commercialization. However, they also express a strong willingness to raise funds, hoping to gain access to high-quality capital and resources, using this opportunity to surpass and outperform competitors.

Some enterprises without self-hematopoietic capacity that have not raised funds in the past or have only received small amounts of financing, due to the short duration that cash flow can sustain, they will face the risk of a broken capital chain and thus are more eager for financing, placing them in a weaker position at the negotiating table.

At this life-and-death moment, investors often advise founders not to be obsessed with the company’s valuation. The company valuation is a temporary pricing given by investors and entrepreneurs. Entrepreneurs should prioritize securing funds and developing the company, rather than missing out on financing and losing opportunities for enterprise development while being stuck on valuation negotiations. Meanwhile, the current market environment makes it easier to widen the gap with competitors, so companies should accelerate financing, expand their business, and surpass their rivals.

An investor said: "We firmly believe that companies with good fundamentals can weather this round of winter. At the same time, under such market conditions, it is a wise decision for founders and shareholders to make tough choices. It just needs further digestion of the gap between fundamentals and the valuation system, and also requires some patience to wait for the recovery of market confidence."

In the capital winter, not only are companies making adjustments, but investment institutions are also adjusting.。

In the past, market-oriented funds and US dollar funds were the main investors, but currently,Funds with state-owned capital backgrounds begin to riseIn the first half of 2023, nearly 20 super-large state-owned teams, along with other industry investors and well-known investment institutions, invested 1.1 billion yuan in Xiantong Pharmaceutical, creating the largest market-based financing in the pharmaceutical field in the first half of the year.

Industry insiders predict:Funds with state-owned capital background will be the mainstream supporting the primary market for a considerable period of time in the future.The operation model, investment thinking, requirements and demands, risk control and terms of state-owned capital are vastly different from previous market-oriented funds and US dollar funds. Companies need to flexibly adjust and quickly adapt.

In addition,Compared to the larger scale of managed funds、For investment institutions that previously focused on mid-to-late stage investments, those that invested purely in early-stage ventures have been hit harder during the downturn.. In the past, early-stage investment institutions followed the mindset of "high risk, high return," but currently, most funds are risk-averse, seeking certainty in exits. Especially with the retreat of US dollar funds that favor long-term investments, these types of early-stage investment institutions generally face difficulties in fundraising, and their subsequent investments will become even more cautious.

Even in the midst of winter, we must look forward to spring. The successful financing of hundreds of companies has also given confidence to the industry.

Through sorting out, we found that investors' preferences have changed compared to previous years.

First, investors have become more "pragmatic." Compared to the past two years when they heavily invested in R&D-focused companies, bet on innovative technologies, and positioned themselves in the latest concepts, investors now prefer healthcare companies with revenue, profits, and growth.

Second, investors prefer companies with the ability to expand overseas or assist other companies in going global. An anonymous investor stated, "There is currently a consensus that policies such as centralized procurement have restricted the domestic market space, while overseas markets are very appealing. Although overseas markets also present various competitive challenges, only companies with the capability to go global can significantly increase their revenue scale. Based on this, investors are paying more attention to companies involved in overseas expansion compared to before."

Third, investors tend to favor companies such as "enablers" and "hidden champions."

From an industry perspective, the upstream of life sciences, the upstream of high-end medical devices, surgical robots, ophthalmic consumables, brain science, and AIGC were the popular sectors for financing in the first half of the year.。

In the upstream of life sciences, on the one hand, domestic companies have achieved technological breakthroughs, such as OPM breaking through in culture media and Nano Micro Technology making advancements in chromatography fillers. On the other hand, the pandemic has impacted overseas supply chains, allowing domestic companies to gain recognition in the Chinese market through more timely supply, lower prices, and higher-quality products. As a result, the upstream of life sciences has also started to see the replacement of imports with domestic alternatives. Against this backdrop, well-known institutions like Legend Capital and Matrix Partners have chosen to heavily invest in the upstream of life sciences, supporting breakthroughs in high-end technologies and the shift toward domestically produced alternatives.

Upstream High-End Medical Device Companies Also Attract Attention from Investment Firms. Companies such as Poseidon, Kunshan Medical Source, Memore Vacuum, Scolarat, ZhenGuang DeCore, and SansThink have all successfully secured financing during the capital market downturn. Some of these companies provide products like CT tubes that are already widely used in the market.

In the surgical robot field, 15 domestic surgical robot companies completed financing in the first half of the year. Among them, compared to the previously popular laparoscopic surgical robots and orthopedic surgical robots, the primary market has seen a wider variety of surgical robots, such as Dessight Biomedical and Xianwei Medical's ophthalmic surgical robots, Antai Weijing's microsurgical robots, and MicroNano Power's magnetically levitated capsule endoscopy robots… Notably, globally, the total financing for surgical robots reached $600 million in the first half of the year, ranking first in the medical device industry, followed by cardiovascular consumables and electrophysiological technology with total financing of $500 million each.

Ophthalmic consumables are one of the few tracks with significant growth in both total financing and the number of events. In the first half of 2023, the total financing in the ophthalmic consumables sector increased by 1501% quarter-over-quarter, and the number of financing events increased by 75% quarter-over-quarter. Among them, Intalight received 300 million yuan in financing, Dessight Biomedical received hundreds of millions of yuan in financing, and RuiTai Bio received nearly hundreds of millions of yuan in financing, which raised the total financing amount in the ophthalmic consumables field.

Since the explosive popularity of ChatGPT, AIGC (Generative AI) has garnered significant attention from the capital market. First, investors packed the venue of the "Generative AI and Healthcare Forum," and later generative AI companies such as Wanmu Health, Lingxin Intelligence, Duowen Doctor, and Fuxin Technology completed their financing rounds, demonstrating the high level of interest.

In addition, there are also many financing events in the fields of brain science instruments, IVD upstream, small molecule innovative drugs, GLP-1, cell therapy, antibody drugs, and animal protection.

2023 is already halfway through, what changes will occur in the medical industry's investment and financing market in the second half of the year?

First, investors will focus on "true innovation" in pharmaceuticals and medical devices. Pharmaceuticals, devices, and diagnostics all have solid industry logic and foundations. A few projects experienced valuation growth in the early stages that exceeded fundamental growth and will require some time to digest, but most projects can still secure financing within a reasonable valuation.

Different from before, in the pharmaceuticals field, investors have started to focus on the balance among team, target, and technology, paying more attention to the choice of indications and the market prospects of pipelines. They also take heed of fundamental information such as clinical promotion and policy preferences.

In the medical device field, investors no longer focus solely on "technology" but take a comprehensive view of a company's product lines, business pathways, market prospects, competitive landscape, and overseas expansion capabilities, among other integrated information.

Secondly, the substitution of domestically produced products remains an important logic in the medical industry, and bottleneck technologies and bottleneck products will usher in a new round of development opportunities. For example, technologies/markets that are supported by policies and receive national attention, such as core components of scientific instruments and medical devices, as well as upstream raw materials, will be given special attention by investors.

Finally, going global is a hot scenario. Companies with the ability to go global and assist others in doing so will also gain favor with investors.