Billion-Dollar Life Science Giants Report Revenue Declines as China Market Becomes Key Performance Barometer

Danaher

Product Design and Manufacturer

Thermo Fisher Scientific(China)

Life Science Research Services Company

As recognized leaders in the life sciences services field, Thermo Fisher Scientific and Danaher have consistently maintained high growth, each with a market value of around 200 billion US dollars. Despite being a super track capable of producing companies with market values in the billions, the market capitalization of domestic local enterprises in China lags far behind. For instance, the market value of Sunresin is approximately 30 billion yuan, while that of Tofflon is less than 20 billion yuan.

Despite such a stark contrast in scale, both Thermo Fisher Scientific and Danaher reported in their 2023 half-year reports that their performances declined by 6% and 7%, respectively, due to the impact of the Chinese market. As industry leaders, they have long occupied the major market share through robust R&D advantages, comprehensive product portfolios, and global operational networks. Now, what exactly has happened in the Chinese market to cause their performances to decline simultaneously is undoubtedly worth paying attention to.

As the performance reports for the first half of 2023 are successively released, the Chinese market shows a trend of recovery, a trend that is also reflected in the report cards of many enterprises.

Notably, an increasing number of multinational brands are beginning to recognize the direct impact of the Chinese market on their performance, reflecting this in their financial reports. Take the three major traditional imaging giants "GPS" as examples; they have significant investments and layouts in the domestic market. Therefore, the development of the Chinese market determines the level of their performance growth.

GE Healthcare's revenue in Q2 2023 was $4.817 billion, increasing approximately 7% year-over-year; the company achieved a revenue of $9.524 billion in H1 2023, marking an approximately 8% year-over-year increase. GE anticipates its full-year performance to grow between 6% and 8% year-over-year. Notably, significant business growth has been observed in the Chinese market.

Specifically, GE Healthcare's Q2 revenue in the Chinese market was $714 million, a year-on-year increase of 12%; the total revenue in the Chinese market for the first half of 2023 was $1.386 billion, a year-on-year increase of 15%. GE Healthcare was listed independently on NASDAQ in the United States this January, and the independent GE Healthcare has increasingly focused on the Chinese market.

In the first half of this year, GE Healthcare has made significant progress in its local development in the Chinese market. Its collaboration with Sinopharm Medical Devices, the groundbreaking of a domestic precision medicine industrialization base, the expansion of a high-end nuclear medicine molecular imaging equipment production line, and the establishment of solutions for grassroots and rural healthcare areas all serve as evidence of its deep commitment to the Chinese market.

Philips' financial performance report for the second quarter of 2023 shows that the revenue for the quarter reached 4.47 billion euros, a year-on-year increase of 9%. From a regional perspective, revenue from mature regions such as North America and Western Europe increased by 8% year-on-year, while emerging markets, particularly China, saw a year-on-year growth of 15%. In terms of business structure, Philips' operations consist of three major business segments: Diagnosis & Treatment, Connected Care, and Personal Health. According to the financial report, the Chinese market achieved double-digit growth across all three business segments, with overall growth rates higher than those in mature regions.

Such achievements are attributed to Philips' gradually increasing "China Strategy." In 2022, Philips established three innovation centers in China, focusing on systems, products, and software innovation. By getting closer to local customers, these centers handle functions such as R&D, manufacturing, and market channels, while closely collaborating with the local ecosystem. The aim is to serve the Chinese market better, faster, more accurately, and in a more optimized way.

Moreover, in Siemens Healthineers' Q3 2023 performance, the growth rate in the Chinese market reached 17%, surpassing the traditional EMEA market's 14%, making it the fastest-growing region in Siemens Healthineers' global market. Overall, despite a 5% revenue decline in the EMEA market and an 8% drop in the U.S. market, the Chinese market still achieved an 11% growth rate.

Since October last year, Siemens Healthineers has divided its original Asia-Pacific region into two parts: the China region and the Asia-Pacific region excluding China (including Japan), and has begun promoting the localization of its entire product line. Additionally, Siemens (Shenzhen) Magnetic Resonance Ltd. signed a strategic cooperation framework agreement with the Nanshan District People's Government of Shenzhen City, planning to build a new high-end medical equipment R&D and manufacturing base in Nanshan District, Shenzhen. Moreover, Siemens Healthineers' first diagnostics reagent production and R&D base in the Asia-Pacific region — Siemens Laboratory Systems (Shanghai) Co., Ltd. — officially began operations in Pudong this June.

Thanks to the recovery of the Chinese market, major device companies have experienced a surge in growth. However, two giants in the life sciences services sector, Thermo Fisher Scientific and Danaher — each with a market value of approximately 200 billion US dollars — have faced declining performance, signaling that the era of multinational giants having effortless success in the Chinese market has quietly come to an end.

The Chinese market has gradually evolved from a "cash cow" into an "arena."

Thermo Fisher Scientific and Danaher both indicated in their earnings calls that a significant portion of their performance decline was dragged down by reduced revenue from the Chinese market, which has started to impact the earnings trend of leading companies in certain niche sectors.

Thermo Fisher Scientific Releases Financial Results for the First Half of 2023, with Total Revenue of $21.397 Billion, a Year-on-Year Decrease of 6%.

Among the four major business units, the revenue from the Laboratory Products and Biopharma Services segment accounted for a larger proportion, reaching 54.2%, increasing by 6% year-over-year to $11.594 billion; the revenue share of the Life Sciences Solutions segment was 23.7%, decreasing by 33% year-over-year to $5.075 billion. The revenue share of the Analytical Instruments segment was 16.2%, increasing by 11% year-over-year to $3.472 billion. The revenue share of the Specialty Diagnostics segment was 10.4%, decreasing by 14% year-over-year to $2.217 billion.

Thermo Fisher Scientific's Chairman, President, and CEO Marc Casper frankly admitted during a conference call reviewing the company’s second-quarter financial performance that pressure from the macroeconomic environment and the decline in the Chinese market significantly impacted the company’s results.

CFO Stephen Williamson further revealed that about one-third of the driving force behind the change in core revenue came from the decline in the Chinese market, while the rest was triggered by cautious spending from the global customer base, particularly in the biotechnology industry.

By region, Thermo Fisher's organic revenue in North America experienced a single-digit decline in the second quarter, while its organic revenue in Europe grew by a single-digit percentage. In contrast, the organic revenue in the Asia-Pacific region also declined by a few percentage points, with the decline in the Chinese market even reaching double digits. By business segment, revenue from the Life Sciences Solutions segment dropped 25% year-over-year in the second quarter, while revenue from the diagnostics and healthcare markets also fell by approximately 20% compared to the same period last year.

In view of the above situation, Thermo Fisher Scientific has adjusted its revenue target for this year to between $40 billion and $43.4 billion, down from the previous expectation of $45.3 billion. Meanwhile, the company has also revised its core organic revenue growth target to around 0% to 2%, compared with the previous forecast of 7%.

Danaher Corporation's financial results for the first half of 2023 showed that its total revenue was $14.324 billion, a year-on-year decrease of 7%.

Among the four major business lines, the diagnostic business accounted for 32% of revenue, a year-on-year decrease of 11% to $4.607 billion; the biotechnology business accounted for 26%, a year-on-year decrease of 16% to $3.749 billion; life sciences and environmental & applied solutions accounted for 24% and 17%, respectively, with only year-on-year growth of 4% and 3%.

Like Thermo Fisher Scientific, Danaher stated in its Q2 earnings call that revenue declines in developed regions were driven by reduced pandemic-related income. Revenue in the Chinese market fell by approximately 10%, primarily due to ongoing adjustments in China's biopharmaceutical market.

In terms of order volume, Danaher's orders in the Chinese market dropped by 20% in Q1, 40% in Q2, and 50% in June. From a business perspective, biotechnology revenue in H1 2023 was $3.749 billion, a year-on-year decrease of approximately 16.35%.

At the same time, Danaher revealed in its earnings call that its biotechnology business generated over US$1.3 billion in revenue in China in 2022, while revenue from the Chinese market is expected to continue slowing in the second half of this year, with full-year revenue projected at only US$800 million. Additionally, Danaher anticipates a high single-digit to low double-digit decline in core revenue for the full year.

Not only Thermo Fisher and Danaher, but Illumina also revealed in its Q2 earnings call that it would significantly lower its 2023 revenue target, stating that 25% of the reduction is due to the impact from the Chinese market. Another life sciences giant, Agilent, also reported a 30% decline in its domestic pharmaceutical business in the third quarter of fiscal year 2023 (ended July 31, 2023), with revenue from the Chinese market accounting for 20%, down 19% year-over-year this quarter.

It can be seen that the era when foreign brands could take what they wanted from the Chinese market has passed, and the Chinese market is becoming an important battleground for influencing the performance of multinational giants.

Why Have Previously Invincible Multinational Giants Slowed Down in the Chinese Market, and What Factors Are at Play?

First, the topic of domestic substitution cannot be avoided.

In the past few years, one major theme in the medical industry has been the substitution of domestically produced products. Policy guidance, capital investment, and high-tech talent committed to innovation and entrepreneurship have led to the replacement of foreign products with domestic ones across many niche sectors. In some areas, domestic products have even taken the lead. The life sciences sector is no exception.

After recognizing the irresistible trend of localization in China, many multinational companies have opted for localized operations, conducting research and development as well as production domestically to meet market demands. For instance, Qiagen NV has achieved product localization through its R&D and production base located in Shenzhen. Meanwhile, during its Q2 earnings call, Qiagen NV also expressed its intention to create a second brand in the Chinese market, which will operate independently from its existing brand with a localized approach. Illumina has also announced the production and assembly of several products in Shanghai, with the first batch already delivered to customers.

Secondly, the epidemic also played a role in fueling the situation.

Although products related to the pandemic have led to a surge in revenue for some companies, the pandemic has also had a tangible impact on their business operations.

During the pandemic, global supply chains were strained, leading to extended delivery cycles for foreign brands, which created an opportunity for domestically produced alternatives; on the other hand, the urgent new demands brought by the pandemic further accelerated the substitution process of domestic products.

Taking the most critical raw material in the biopharmaceutical industry, cell culture media, as an example, this market is mainly monopolized by overseas giants such as Thermo Fisher Scientific, Danaher, and Merck. According to data from Frost & Sullivan, in 2020, the proportion of domestically produced cell culture media in China was only 22.8%.

As a platform company, Thermo Fisher Scientific can provide a complete set of core product packages, including culture media, chromatography resins, bioreactors, microcarriers, filters, and membranes. In contrast, domestic companies tend to offer single products. Under normal circumstances, domestic companies lack sufficient competitiveness when facing foreign brands. However, the emergence of the pandemic changed everything. With strong market demand and longer lead times for multinational giants, opportunities have arisen for domestically produced products.

Finally, the impact of the economic environment must also be considered.

Although the impact of the pandemic on the real world is gradually fading, its influence in the business world continues to ferment.

The slowdown in economic growth has reduced the frequency of financial activities, and the financing environment has gradually weakened, causing biopharmaceutical clients to become more cautious in their spending. On the other hand, over the past few years, due to the surge in demand, these clients have built up significant production capacity, particularly in CDMO capacity.

Under the premise of a slowing market pace, customers not only lack additional demands but also face a large amount of inventory that needs to be digested, which objectively leads to a decline in revenue for upstream life science giants. Therefore, several enterprises have stated in their earnings calls that helping customers clear out and manage inventory will be their next task.

Specifically, for the company itself, the reduction in Thermo Fisher Scientific's revenue is mainly reflected in the Life Sciences Solutions segment, where the majority is related to the nucleotides and enzymes business, and the remaining smaller portion is due to the bioproduction business.

The outbreak of the pandemic has ignited the mRNA vaccine track. From a long-term development perspective, aside from COVID-19 vaccines, mRNA technology has gradually been applied in areas such as cancer vaccines, gene editing, CAR-T cell therapy, protein replacement therapy, and other preventive vaccines for infectious diseases, with products progressively coming to market. Whether it is mRNA vaccines or mRNA drugs, the key raw material is nucleotides. Thermo Fisher Scientific (China) Co., Ltd. provides high-quality nucleotides in various forms, formulations, and volumes, and can offer more convenient and flexible solutions based on customers' requirements for concentration or format.

Thermo Fisher Scientific(China)Co.,Ltd. Partial Nucleotide Product Categories, Image Source: Thermo Fisher Scientific Official Website

During the pandemic, to meet the surge in demand, Thermo Fisher Scientific invested heavily in accelerating capacity building. For instance, in 2021, it invested $2.5 billion to increase the production capacity of biologics, enzymes, nucleotides, and laboratory products. Now, with the retreat of the pandemic, the slowdown in economic growth, and reduced demand from biopharmaceutical companies, sales of related products have seen a decline.

Enzymes are no exception. As fundamental raw materials playing a critical role in various products such as biochemical reagents, antibodies, recombinant proteins, PCR equipment and consumables, cell analysis products, immunoassay reagents, and molecular biology reagents, their performance inevitably declines after a downturn in downstream demand.

Moreover, due to the advance procurement of PCR instruments and reagents caused by the pandemic, the impact will continue for some time. On the other hand, the entry of an increasing number of domestically produced PCR instruments, sequencing, and reagent manufacturers is also putting more competitive pressure on multinational brands.

In recent years, a large number of reagent companies in China have gone public, such as Aladdin, Univ-Bio, Titan Technology, Acro Biosystems, Novoprotein, and Sino Biological. Although the range of products sold by domestic companies is not yet as comprehensive as that of multinational giants, some reagent products have already achieved import substitution. In the future, with the continuous progress of domestic companies, they will continue to compete with multinational enterprises.

In the short term, the pressure will continue. In the long term, market potential remains optimistic.

For multinational giants, China is a market full of risks and challenges but enormous in scale. Although revenue from this market typically accounts for about 15% of total income, fluctuations here can significantly impact overall earnings, thereby affecting investor confidence.

Therefore, companies including Thermo Fisher Scientific, Danaher, Qiagen NV, and Illumina expressed cautious sentiment during their Q2 earnings calls, with conservative forecasts for the second half of 2023 and the first quarter of 2024. However, this communication appears to reflect more of a short-term emotional release. Over the past few years, their expansion efforts have never ceased, and these strategic moves will eventually play a role in future market competition.

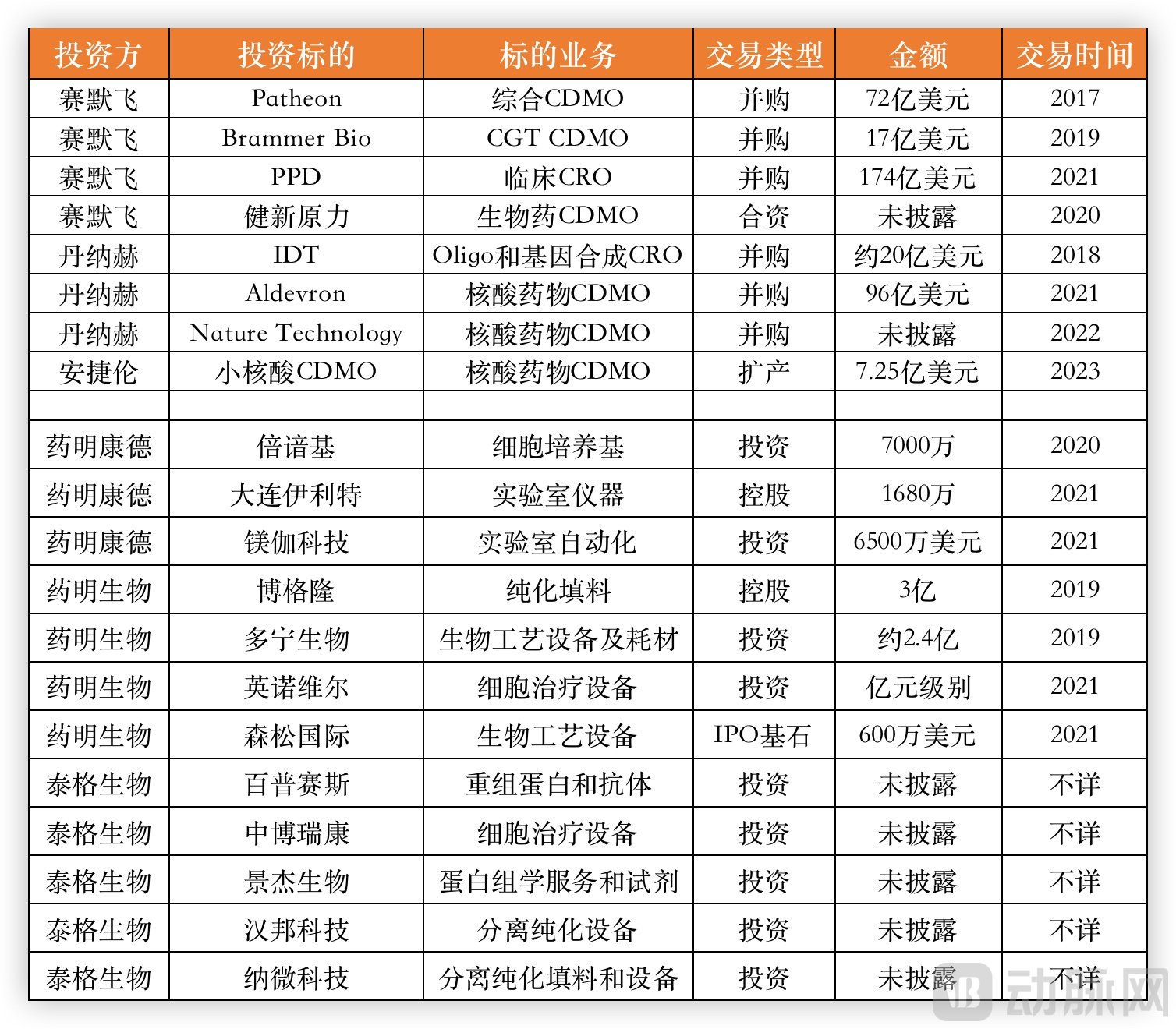

Partial mutual layout and penetration between life science companies and CXO companies, according to publicly available information.

A review of the expansion of these life science giants over the past few years shows that companies such as Thermo Fisher Scientific and Danaher have spent billions of dollars to enter the CXO industry, blurring the boundaries between two types of enterprises that originally belonged to the upstream and midstream of the biopharmaceutical industry chain.

From a business perspective, the customers of both the life sciences and CXO sectors are biopharmaceutical companies. Globally, the proportion of pharmaceutical R&D outsourcing is about 50%, while the proportion of manufacturing outsourcing is nearly 60%. This means that if a company can provide a comprehensive solution that spans both life sciences and CXO services to its target customers, it will significantly enhance customer stickiness.

In terms of growth, the scale of the CDMO business itself can meet the requirements of multinational giants. For instance, CDMOs in next-generation drugs such as cell and gene therapy, ADCs, and oligonucleotides are growing rapidly, achieving double-digit growth rates. Moreover, the profit margin in the CDMO industry is quite attractive, with Wuxi Biologics maintaining a net profit margin of around 30%. Additionally, the CDMO business cycle is relatively long, with a longer lock-in period once contracts are signed.

At the same time, domestic CXO companies are also actively investing in the upstream track of life sciences. The WuXi group has spent billions of yuan to control or invest in domestic life science companies. Tigermed has also made extensive layouts in China's pan-biomedical industry, including life science companies such as Nano Micro, Acro Biosystems, and Jingjie Biotechnology. In addition, several domestic life science companies specializing in culture media, such as OPM and Ausbian, have also started to cross over into CDMO business.

From this perspective, the competition in the future market will become even more intense. Only those who can provide customers with more valuable solutions will gain the upper hand in a challenging market. For foreign brands, how to better integrate into the domestic market and offer localized services has become a question that multinational giants must seriously consider. For domestic companies, this is also a crucial turning point. As innovation advances, the intensity of competition is increasing. Gaining a competitive edge in the market has become the next goal for these companies.

Despite the global economic slowdown, China's market still holds long-term growth potential when viewed from a broader perspective. Companies need to transform challenges into opportunities and tailor their products and services to meet the demands of the local market in order to ride on the fast track of China’s market growth.