Global Weight-Loss Drug Pipeline Report: Are 42 Companies Fueling a Fierce Race with 72 Drug Candidates?

Novo Nordisk

Insulin Developer and Manufacturer

Eli Lilly

Global Pharmaceutical R&D and Production Company

The emergence of重磅 drugs can颠覆 public perceptions of a disease.

This historical pattern replayed itself in the 2023 weight-loss drug market: Obesity is a chronic biological disease that can be treated with novel medications. "People are beginning to understand that this is a real disease, not just a matter of lifestyle and willpower," said Fatima Code Stanley, an obesity specialist.

The cognitive update has successfully sparked the pursuit of new obesity therapies. For pharmaceutical companies, this means a massive weight-loss drug market and potentially explosive performance growth.

In June 2021, Novo Nordisk's Semaglutide ignited the fuse of the obesity revolution – FDA approved it for adult weight loss indications, and a few months later for adolescent use. Eli Lilly and Company’s Tirzepatide followed closely behind, already approved for diabetes treatment, and is currently undergoing regulatory review for weight loss indications.

How火爆 is the sales? Novo Nordisk reported that both the weight-loss version (Wegovy) and diabetes version (Ozempic) of semaglutide are facing shortages, even extending to the previous generation GLP-1 product, liraglutide (Saxenda).

Reportedly, Eli Lilly and Company has invested over 1 billion US dollars in building a factory in the United States, partly to keep up with the supply. STAT, a professional media outlet in the healthcare field, reported that Pfizer estimates the global weight loss market could approach 100 billion US dollars within ten years, surpassing all other pharmaceutical markets. This explosive trend has also prompted dozens of pharmaceutical companies worldwide to enter the weight loss therapy arena, with most attempting to follow in the footsteps of star products.

Based on the热度 of this track, STAT has established a special database for obesity drugs, continuously tracking the pipelines of obesity drugs on the market and under development. Its data sources comprehensively integrate research from TD Cowen Analysts, clinicaltrials.gov in North America, and STAT's proprietary artificial intelligence drug database.Currently, 72 obesity drug pipelines worldwide have been tracked.。

Based on the data from this database, VCBeat conducted a review and analysis of the global weight-loss drug pipeline.

Currently,Novo NordiskStar Weight Loss Drugs - Semaglutide, Liraglutide - Are All GLP-1R (Glucagon-Like Peptide-1 Receptor) Agonists. The Treatment Principle is to Activate GLP-1R, Enhance Insulin Secretion in a Glucose Concentration-Dependent Manner, Inhibit Glucagon Secretion, and Delay Gastric Emptying, Reducing Food Intake Through Central Appetite Suppression. Clinical Trials of Semaglutide Have Shown a Weight Loss of Up to 15%.

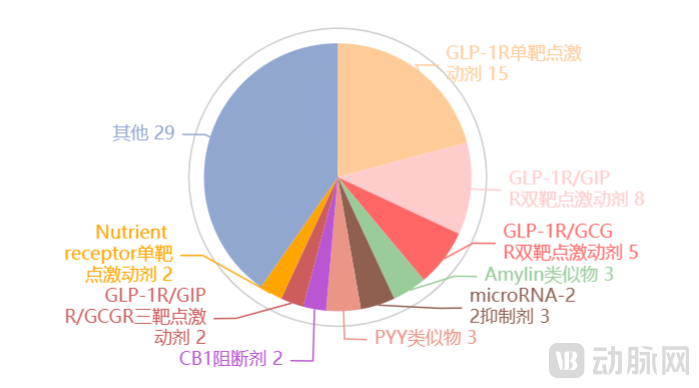

Among the 72 obesity drug pipelines,The star effect of the GLP-1R target is significant, with over 38 pipelines targeting GLP-1R, already showing a trend of internal competition.

In similar mechanisms, dual-target and multi-target combinations have become the main innovative pathways to enhance efficacy.Eli Lilly's Tirzepatide is a dual-receptor agonist, targeting both GLP-1R and GIPR. In clinical results, the average weight loss of patients was 21.1%, and with a 12-week intervention period, the average weight loss reached 26.6%. Besides this combination, there are also drug pipelines for GLP-1R/GCGR dual agonists and GLP-1R/GIPR/GCGR triple agonists.

Number and Proportion of Pipelines with Different Drug Mechanisms among 72 Global Weight-Loss Drug Pipelines / Chart by VCBeat

Moreover, there are quite a few biotech companies betting on new mechanisms. On one hand, new mechanisms possess potential unique advantages that may result in differentiated efficacy or patient subgroups compared to validated mechanisms. On the other hand, there is a possibility for new mechanisms to be used in combination with drugs like semaglutide. This implies a huge secondary market.

Other drug mechanisms include CB1-R blockers, Amylin analogs, GDF15 analogs, miRNA-122 inhibitors, etc.

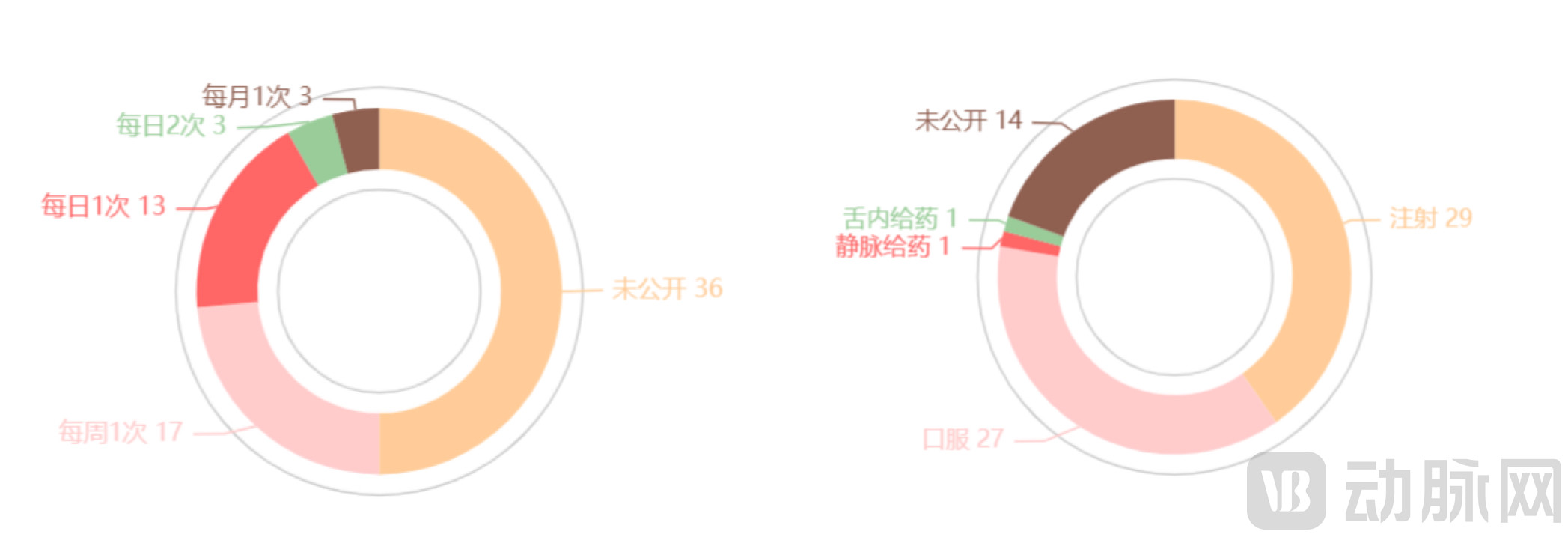

Another innovation point of weight loss drugs lies in the method and frequency of administration.Semaglutide and tirzepatide are both administered once a week via an auto-injector pen. Although the auto-injector and flexible options for multiple doses have significantly improved patient accessibility and convenience, there is still room for improvement in drug accessibility as a potential long-term therapy.

Distribution of dosing frequencies and administration methods for 72 global weight-loss drug pipelines / Chart by VCBeat

Among the 72 pipelines, 17 pipelines have disclosed a dosing frequency of once per week, and 13 pipelines require once-daily dosing. In contrast, the development difficulty for a once-monthly dosing frequency is significantly higher, with only three pipelines currently in progress, marking it as one of the key challenges yet to be overcome in weight-loss drugs. Regarding administration methods, injection and oral administration dominate, with 29 and 27 pipelines respectively.

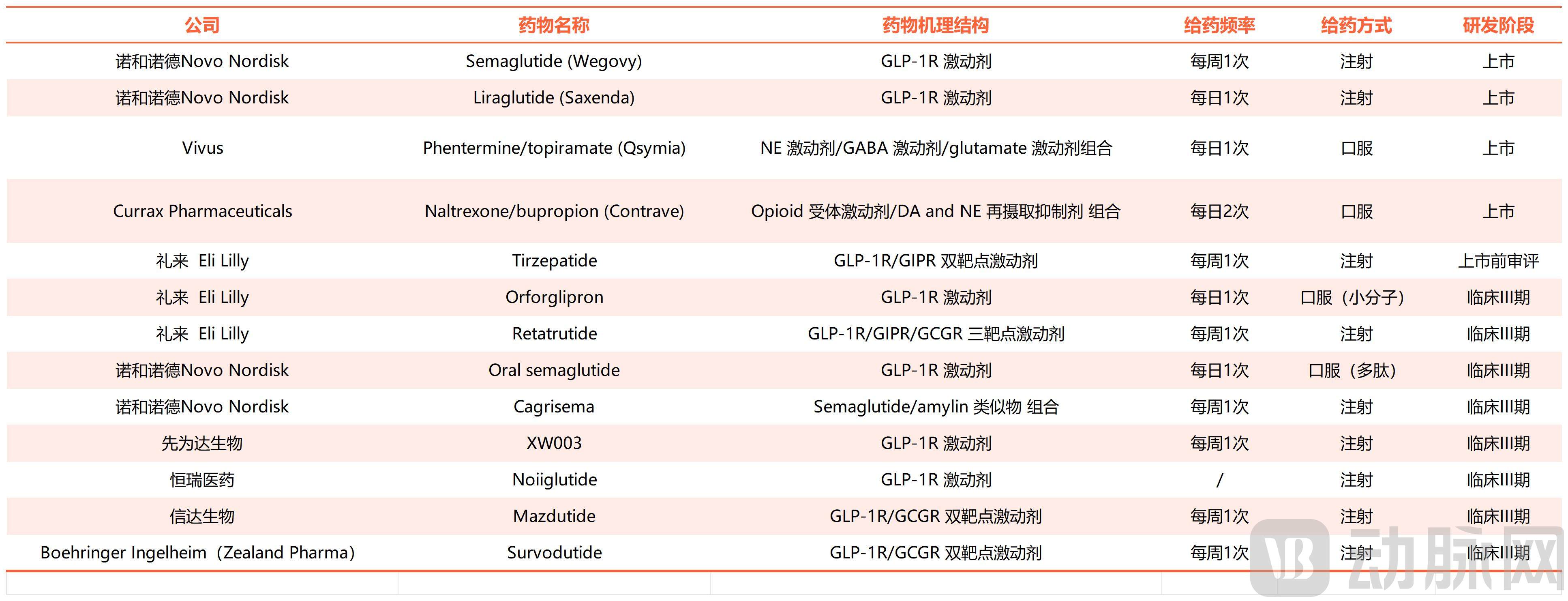

How close are the 72 pipelines to the market? The database shows that four drugs have been approved for weight loss indications. Tirzepatide is under pre-market review (FDA rolling submission), and it is expected to complete the submission of all application documents by 2024.

Overview of Pipelines Entering Phase III Clinical and Later Stages / Chart by VCBeat

Overview of Pipelines Entering Phase III Clinical and Later Stages / Chart by VCBeat

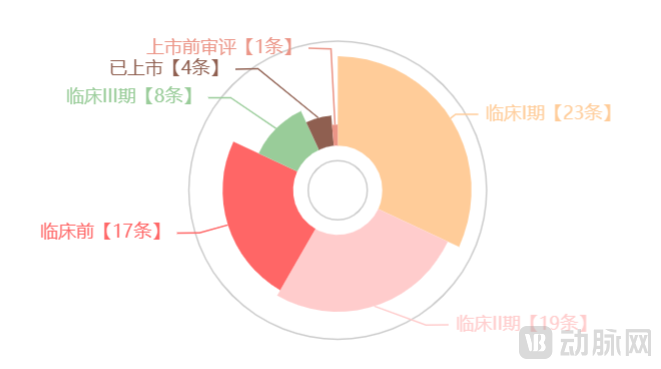

In addition, among the 72 pipelines,17 preclinical pipelines, 23 Phase I clinical pipelines, 19 Phase II clinical pipelines, which also reflects the active innovation trend in the weight-loss drug track.

Development Stages of 72 Global Obesity Drug Pipelines / Chart by VCBeat

According to Frost & Sullivan data, the size of China's weight loss market was 2.1 billion yuan in 2021, with a compound annual growth rate of 71.4% from 2017 to 2021, and it is expected to reach 11.1 billion yuan by 2026. Barclays, a major UK private bank, estimates that in the next decade, the global weight loss market could exceed $100 billion, with the majority of the market in the United States, which is expected to account for about 90% of the global market.

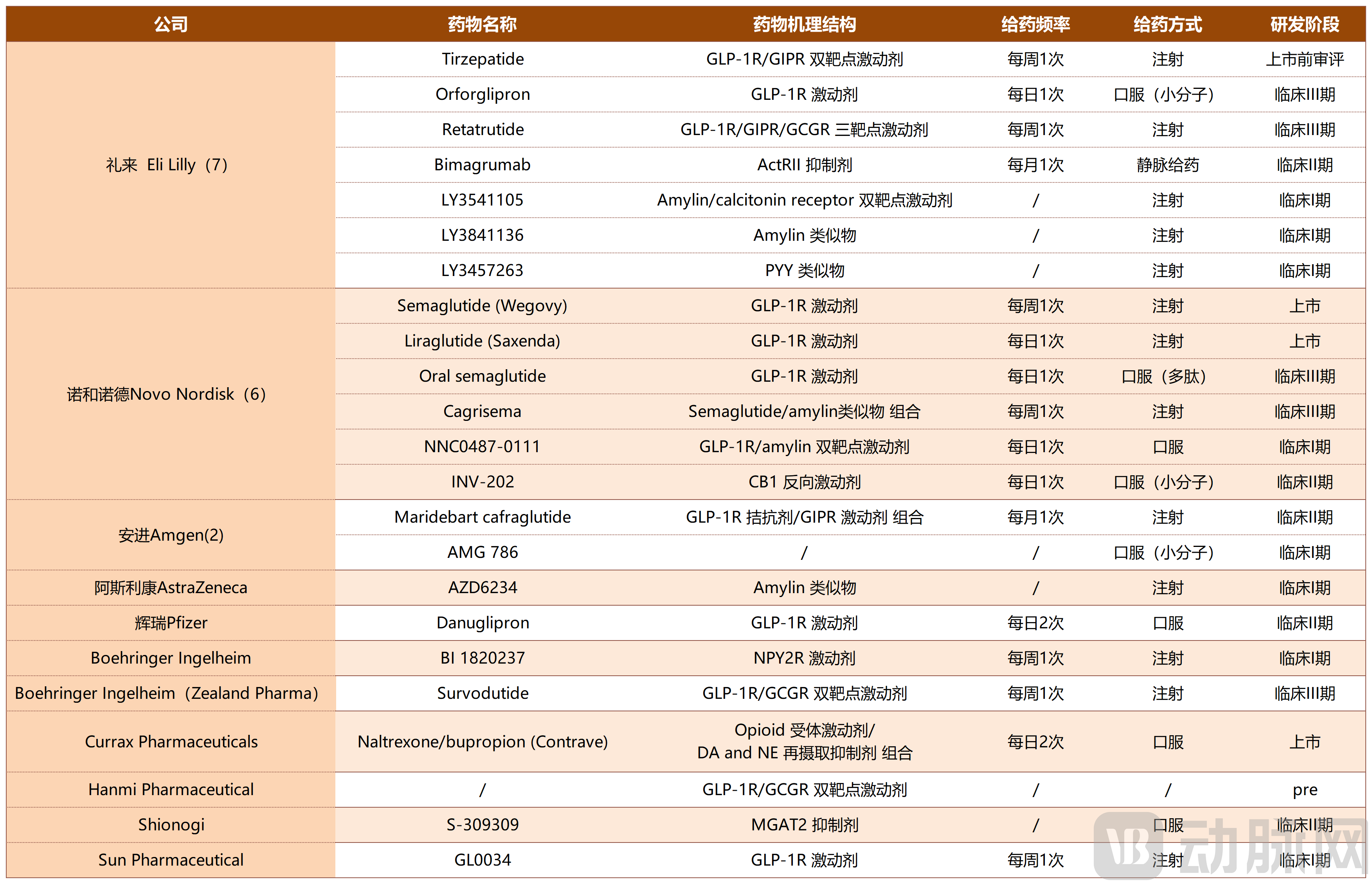

As early developers of weight-loss drugs, Novo Nordisk and Eli Lilly have clearly reaped the benefits of this massive market. There is no doubt that Novo Nordisk and Eli Lilly have become the two giants in the obesity drug sector, establishing pipelines with various drug mechanisms at different stages of development.

The competition between the two is becoming increasingly intense. Not long ago, Eli Lilly announced the acquisition of Versanis, introducing its Bimagrumab pipeline, which is administered once a month, to develop antibodies that reduce fat and enhance muscle mass.

Novo Nordisk acquired Embark for $512 million to develop a novel agonist targeting the adipocyte G protein-coupled receptor EMB1, which can accelerate glucose uptake and increase energy expenditure. Additionally, Novo Nordisk acquired Inversago for up to $1.075 billion, gaining access to the latter’s orally-administered CB1 reverse agonist INV-202, which has now entered Phase II clinical trials.

However, in the $100 billion giant cake, even a small piece means a market worth billions of dollars.With mature channels and a global layout, Big Pharma naturally wouldn't miss this opportunity. Amgen, AstraZeneca, Pfizer, and Boehringer Ingelheim all have pipeline arrangements.

Have a layout in the weight loss drug trackPharma and itsPipeline Overview / VCBeat New Medicine Chart

Hanmi Pharmaceutical, a South Korean company founded in 1973, and Shionogi, a Japanese company established in 1878, have also entered the market. Currax Pharmaceuticals and Sun Pharmaceutical are generic drug companies from the United States and India, respectively. The rights to the drug Naltrexone/bupropion (Contrave) owned by Currax Pharmaceuticals were acquired through its 2019 purchase of Nalpropion Pharmaceuticals, a company specializing in obesity drug development.

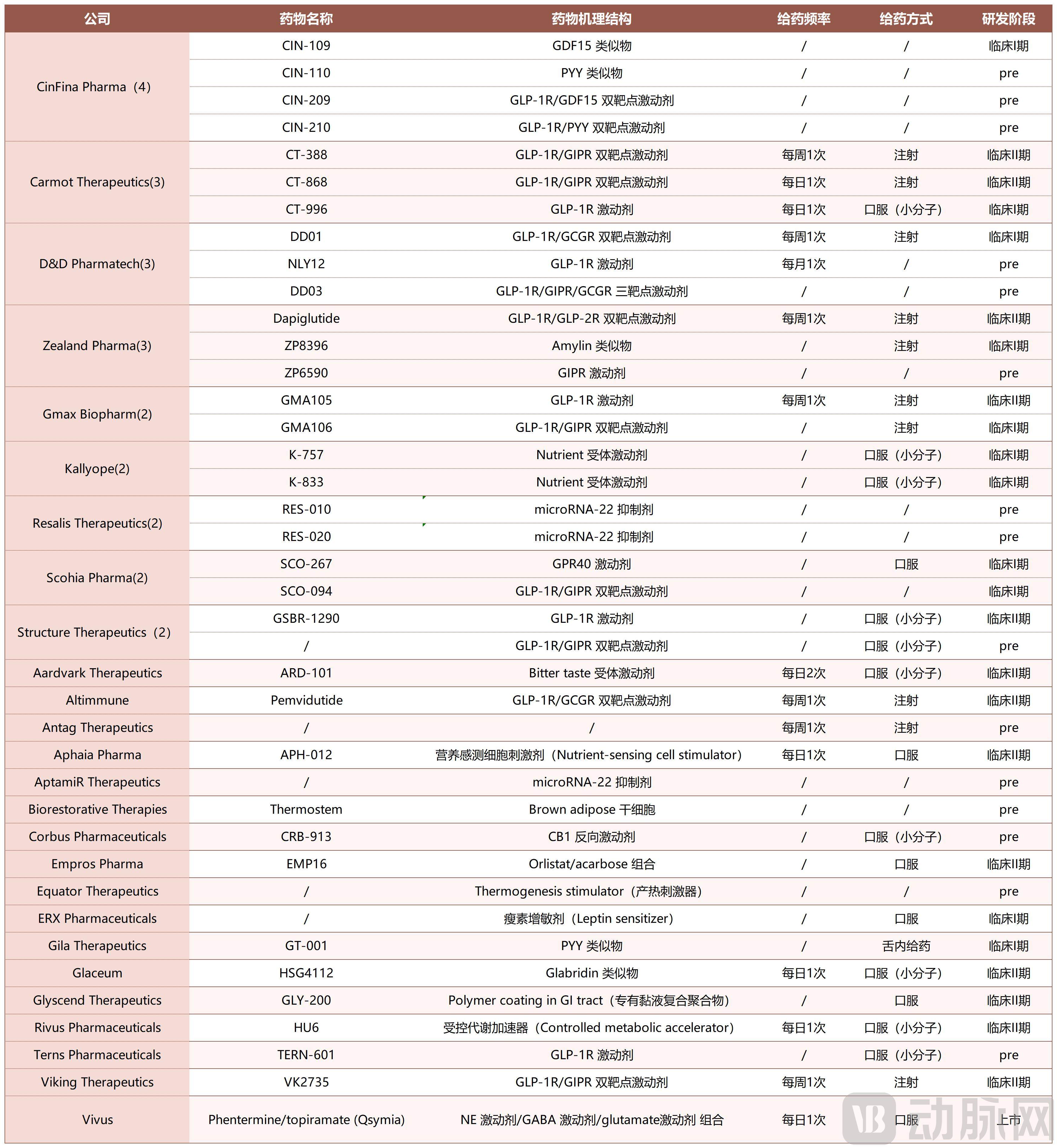

Other companies with a presence in the weight-loss drug sectorAnd itsPipeline Overview / VCBeat New Medicine Chart

Other companies with a presence in the weight-loss drug sectorAnd itsPipeline Overview / VCBeat New Medicine Chart

Among Biotech companies developing their own weight-loss drugs, more innovative targets and mechanisms of action are emerging — from stem cells to cell stimulants, leptin, bitter taste receptors, thermogenic mechanisms, and more. Corresponding to these cutting-edge new mechanisms, the drugs are in earlier stages of development, with over half of the drug pipelines still in preclinical stages.

In the weight-loss drug track with a high market ceiling, Biotech also has many opportunities, which has led to continuous investment from primary market investment institutions. Carmot Therapeutics recently completed a $150 million Series E financing round; Kallyope has completed multiple rounds of financing totaling over $400 million; and Rivus Pharmaceuticals, which has only one main drug pipeline, also completed a $132 million Series B financing round.

In the STAT Obesity Drug Database, there are five companies in China that have developed obesity drugs, with a total of nine pipelines. Unlike the diversified global pipeline layout, domestic pharmaceutical companies have focused entirely on GLP-1R-related targets, including single-target and multi-target agonists, as well as combinations of single-target agonists. In terms of research and development stages, most drugs have entered clinical trials, with three already in Phase III trials.

VCBeat New Medicine Chart

Xianweida BioIn March this year, the Phase III clinical trial for weight loss with XW003 was initiated. In the latest published clinical data, after 26 weeks of treatment, the body weight of subjects in the 2.4mg group of XW003 decreased by 14.7% from baseline. The top-line data from the Phase III registration trial is expected to be available in 2024.

Hengrui MedicineThe latest clinical data of HRS9531 showed that, in the Phase 1b clinical trial, the average weight loss range was 4.3~7.7kg after 4 weeks of treatment in the 0.9~5.4mg group, and the weight loss reached 8.0kg by Day 36 in the 5.4mg group.

Innovent BiologicsMazdutide 9mg High-Dose Regimen Achieves Primary Endpoint at 24 Weeks in Phase II Clinical Trial for Chinese Obese Subjects. In the Chinese obese population with an average BMI of 34.3 kg/㎡, the 24-week treatment resulted in a 15.4% (14.7kg) weight reduction compared to placebo. The 6mg low-dose mazdutide regimen achieved a 12.6% weight loss after six months of treatment.

In addition, according to public information,Daor BiologicsDR10624 has completed the dosing of the first subject in the Phase I clinical trial.DearDrugMDR-001 has obtained the FDA's new drug clinical trial approval for obesity and type 2 diabetes in the United States, and successfully completed the first dosing group administration in the Phase IIa clinical trial for obese subjects.

As domestic companies rapidly advance in obesity drugs, BioPharma has also set its sights on the vast Chinese market.

Novo Nordisk's semaglutide was approved in mainland China as early as 2021 for the treatment of adult type 2 diabetes and to reduce the risk of cardiovascular adverse events in patients with type 2 diabetes and cardiovascular disease. In June this year, the new indication application for semaglutide injection has been accepted by NMPA.

Eli Lilly's Tirzepatide was submitted for marketing authorization in China last September, and Boehringer Ingelheim's Survodutide has applied for Phase III clinical trials in China.

Globally, pipeline deals for weight-loss drugs are also occurring frequently.In February this year, Huadong Medicine's subsidiary Sinopharm Huadong signed a cooperation agreement with SCOHIA PHARMA, announcing the expansion of their global strategic partnership for the GLP-1R and GIPR dual agonist SCO-094 and its derivative products.

Data Source:

Weight loss drugs on the horizon: STAT's Obesity Drug Tracker

https://www.statnews.com/2023/09/12/new-weight-loss-drug-tracker-novo-nordisk-eli-lilly/

(Data in the article as of September 18, 2023)