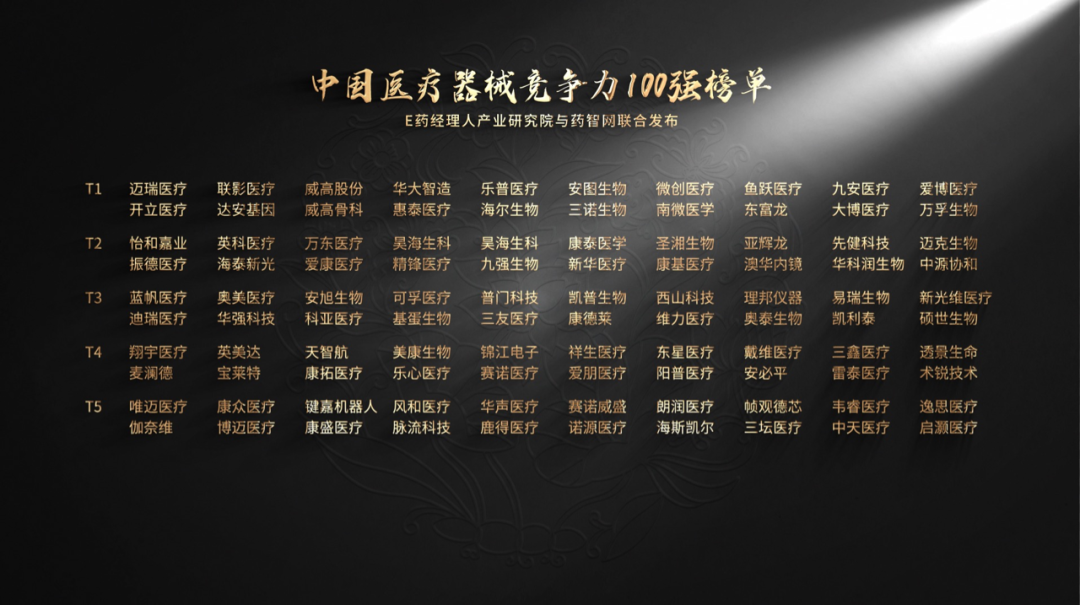

Mindray, United Imaging, and Weigao Lead the Inaugural China Medical Device Competitiveness Top 100 List

MicroPort

High-end Medical Device R&D and Manufacturer

yuwell

Developer and Manufacturer of Basic Medical Devices

Mindray

Medical Device R&D Manufacturer

Lepu Medical

Developer and Manufacturer of Cardiac Interventional Medical Devices and Pharmaceuticals

Weigao

Blood Purification Product R&D and Manufacturer

It was the best of times, it was the worst of times.

Turning the clock back four years, there was no centralized procurement or COVID-19, and the medical device capital market was just recovering from a significant downturn. The sudden outbreak of COVID-19 accelerated this "recovery" path. In just 8 months, the medical device industry index surged from 7,000 points to over 14,000 points, with an increase of more than 100%.

However, as the saying goes, "misfortune may be an actual blessing," but the opposite can also be true. Affected by multiple factors such as the COVID-19 pandemic, the expansion of centralized procurement, and the normalization of these measures, the performance of the medical device industry index has been like a downward "roller coaster" since January 2022. So far, there is still no sign of recovery.

It is worth noting that in this frenzy, some innovative medical devices with technical barriers but no revenue have landed on the capital market, but they still encountered a cold reception afterward. The investors' confusion permeated the entire industry.

At the juncture of industry cycle transitions, E Pharm Manager has adhered to an utmost passion and belief in the industry. It aims to identify a group of medical device companies characterized by "high technical barriers, confirmed clinical value, and strong commercialization capabilities," helping to unveil the industry's potential and contributing to the establishment of a healthy industrial ecosystem. Hence, the inaugural "Top 100 Most Competitive Medical Device Companies in China" list was born.

In keeping with E Pharm Exec's consistent independence and rigor, we have selected more than 310 listed and unlisted medical device companies based on Wind,烯牛数据 (Xiniu Data), and药智数据 (Pharmcube Data). These companies do not include pharmaceutical equipment, CROs, low-value consumables, or consumer healthcare product enterprises. They are categorized by track into medical devices, high-value consumables, and in vitro diagnostics.

The data processing takes into account both objective and subjective scoring. Based on the normalized data, different weights are assigned to sub-indicators such as patent richness, product maturity, and platform potential to calculate the objective score; subjective scores are given based on the opinions of experts in the medical device field regarding corporate resources and entrepreneurial spirit.

Ultimately, based on the market value proportions of medical device companies, high-value consumables companies, and in vitro diagnostic companies, the number of 100 shortlisted enterprises in different sectors was determined. These companies were ranked by total scores and included sequentially to form the "Top 100 List of China's Medical Device Competitiveness" (hereinafter referred to as "Device 100"). Within the list, the top 100 companies are divided into five tiers, with each tier presented in descending order of market value (non-listed companies are ranked according to their most recent disclosed valuation).

This list was announced by E-Pharma Manager on September 19 at the "12th China Medical Device Industry Conference" (DeviceChina) hosted by BioBAY. The conference, themed “Breaking Boundaries and Innovating – The Recovery and Reshaping of China-Produced Medical Devices,” focused on medical equipment, high-value consumables, in vitro diagnostics, digital healthcare, and health management. It featured one main forum, 16 specialized sub-forums, and 112 thematic presentations. The event attracted 150 experts for forward-looking exchange dialogues, including academicians and scientists from home and abroad, founders of medical device companies, and investment firm managers. Over 1,500 participants attended in person, comprising government officials, university scholars, industry leaders, corporate executives, technology media, and other professional representatives.

"In developed countries, the ratio of pharmaceuticals to medical devices is basically 1:1; whereas in China, the ratio of pharmaceuticals to medical devices is 1:3, indicating that there will be significant room for growth in the medical device sector in the near future," said Academician Ge Junbo of the Chinese Academy of Sciences at the main forum of this conference.

This market space will come from high-end medical device products. Because many mid-to-low range medical device products in China have already completed local substitution, the proportion of high-end products is still relatively low. Developing high-end products requires long-term R&D investment and the accumulation of innovation.

Patent layout has always been one of the most critical indicators for measuring a company's innovation. In the "Top 100 Medical Device Companies" list, the possession of patents shows a significant "80/20 effect," with companies in the top two tiers holding over 80% of the patents.

United Imaging Healthcare is the company with the most patents. As of the first half of 2023, United Imaging Healthcare has applied for a total of 6,229 invention patents and obtained 2,646 invention patents. It is reported that the company has always adhered to the independent research and development of core components, and under substantial R&D investment, it has broken the monopoly of foreign companies in many fields.

United Imaging Healthcare is a leader in China's medical imaging equipment industry, holding a leading position domestically in areas such as Magnetic Resonance Imaging systems (MR), X-ray Computed Tomography systems (CT), X-ray Imaging systems (XR), Molecular Imaging systems (PET/CT, PET/MR), and Medical Linear Accelerator systems (RT). It is the forerunner among local companies breaking the monopoly of international manufacturers like GE Healthcare, Philips Healthcare, and Siemens Healthineers.

The 2022 annual report shows that United Imaging Healthcare has been deployed in over 1,000 tertiary hospitals across China. According to the statistical data based on the value of newly added markets in China in 2022, the market shares of CT, PET/CT, PET/MR, and XR products from United Imaging Healthcare ranked first in the industry. The market shares of MR and RT products also ranked among the top in the industry.

In the first tier, more than ten companies, including MicroPort, Jiangsu Yuyue Medical Equipment&Supply Co.,Ltd., Mindray, Autobio Diagnostics Co., Ltd., Lepu Medical, and Weigao, also have a relatively rich patent layout.

As is known to all, IVD, cardiovascular, and imaging are the three largest subfields in the medical device industry, and they are most likely to produce giants. MicroPort is the leader in the cardiovascular field.

When it was first established, MicroPort targeted medical devices for minimally invasive interventional treatments, such as coronary drug-eluting stents used for the treatment of coronary heart disease. After more than 20 years of independent research and development and collaborative innovation, the MicroPort Group, including MicroPort Medical, has now filed over 8,500 patent applications, with more than 400 approved products on the market, and its products have entered more than 20,000 hospitals worldwide.

Whether it is the pharmaceuticals market or the medical devices market, enterprises must focus on two words to grow bigger — "going global."

In the global medical market, the United States and Europe account for more than 60% of the market size, with a total of approximately $370 billion in 2021, making them the core markets for medical devices. The compound annual growth rate is expected to be 5.9% over the next five years.

The second keyword revealed in the list is "going global."

In the first tier, several medical device companies, including Mindray, United Imaging Healthcare, Sonoscape, and MGI, are all without exception pioneers in "going global."

In terms of revenue in 2022, Mindray had the highest international income, reaching 11.7 billion yuan; United Imaging, MGI Tech, and BMC achieved over 1 billion yuan each; most other pharmaceutical companies did not exceed 1 billion yuan. In terms of the proportion of international business income, BMC’s revenue from overseas has already exceeded 80%, followed closely by Chison with 78%; for most other enterprises, overseas revenue still does not exceed 50%.

Unlike pharmaceuticals, medical device companies often "go global" by first participating in overseas exhibitions, seeking overseas agents, and understanding overseas markets. If they have sufficient confidence in their products and the overseas market, they will establish a local branch, hire local personnel, and ultimately achieve localized sales.

Currently, most Chinese manufacturers are in the two phases of market research/product registration and channel expansion/installation, while leading manufacturers are in the phase of confirming distributors and deploying market strategies, and will soon enter a new stage of scale formation.

The "pioneers" in going global mainly adopt three approaches: The first is led by Mindray, with companies such as MGI Tech, MicroPort, and Akeso Biomedical entering the market through overseas mergers and acquisitions; the second is the R&D-driven approach, represented by United Imaging Healthcare, which primarily enters by overcoming R&D bottlenecks; the third approach involves leveraging overseas partners to achieve rapid scaling of product sales, which most medical device companies are closest to. Among them, BMC Medical stands out the most, as the company seized the opportunity from a competitor's mistake, formed deep partnerships with overseas collaborators, and quickly captured the market.

Taking Mindray as an example, the company began entering the U.S. market with its patient monitors as early as 2004. Throughout this process, it maintained a strong focus on FDA certification and finally achieved a breakthrough in the high-end customer segment in 2019, moving from profit-driven hospitals that only focused on price to integrated healthcare networks that value comprehensive solutions. In 2021, Mindray continued to expand its IDN (Integrated Delivery Network) customers, and by 2022, it had covered 80% of IDN networks. During this period, Mindray's sales in the U.S. maintained positive growth. Unlike the direct sales model adopted in the U.S., due to Europe’s lower willingness to accept new products compared to the U.S., Mindray adopted a mixed model of direct sales and distribution in Europe during the same period. This localized strategy has also been a key factor in the relative success of Mindray's internationalization.

Reply "Newborn" to learn more about the e-journal.

Register Email Information

Subscribe to E Drug Manager

Information Services

Scan QR Code

Featured Recommendations