Top 5 Global and Domestic Orthopedic Giants: H1 2023 Financial Highlights and Product Portfolio Overview

Johnson & Johnson

Healthcare Product Manufacturers, Health Service Providers

Stryker

Orthopedic Product Developer

Zimmer Biomet

Medical Device R&D Manufacturer

Medtronic

Chronic Disease Medical Device and Therapy Developer

Smith and Nephew

Medical Device Manufacturer

WEGO ORTHO

Orthopedic Medical Device Manufacturer

MicroPort

Medical Device Manufacturing Enterprise

Double Medical

Developer and Manufacturer of High-Value Medical Consumables

Chunlizhengda

Orthopedic Medical Device R&D and Manufacturer

AK Medical

Orthopedic Implant R&D and Production Company

Pioneer in Medical Device Media Reports

Share Professional Medical Device Knowledge

Source:Instrument Family,Reproduction without authorization is prohibited, and reproduction is allowed 24 hours later.

In 2023, with the fading of the pandemic, the global orthopedic medical device market has fully recovered. GlobalData predicts that the global orthopedic devices market will reach nearly 500 billion US dollars.

In China, the volume-based procurement of orthopedic implants has also pushed the entire industry into a phase of accelerated consolidation.

Recently, the half-year financial reports released by orthopedic giants at home and abroad clearly reflect this trend. Devicehome has compiled the information.List of Top Five Companies in Revenue and Income in Various Segments of Orthopedic Enterprises in China and Abroad, let's take a look at which companies made the list.

Note: The statistical period for Medtronic's semi-annual financial report is from January 28, 2023, to July 28, 2023.

According to the revenue statistics of the first half of the year, the ranking of the top five global orthopedic companies remains the same as the same period last year.Johnson & Johnson ranked first with a revenue of $4.509 billion.

Orthopedics is the second largest business of Johnson & Johnson Medical Technologies. In March 2023,Johnson & Johnson Medical Technology Announces Restructuring Plan Involving Orthopedic Business, aiming to achieve "cost reduction and efficiency increase" in the orthopedic department. It is reported that Johnson & Johnson is integrating its sports medicine products into trauma and extremities, while shoulder reconstruction is shifting towards joint reconstruction.

Stryker ranked second with 4.224 billion dollars and achieved high double-digit growth.

Zimmer Biomet ranked third with revenue of $3.912 billion.On March 1, 2022, Zimmer Biomet announced the completion of the spin-off of its spine and dental business, ZimVie. On May 1, 2023, it announced that it had reached a definitive agreement to acquire Ossis, a manufacturer of personalized 3D-printed implants.

In terms of growth, except for Medtronic, the other four companies all achieved positive growth.

Note: Double Medical's revenue data includes minimally invasive surgical products.

Let's take a look at the situation in China. According to the semi-annual reports of listed orthopedic device companies in China,WEGO ORTHO ranked first with a revenue of 805 million RMB, a decrease of 404.198 million RMB compared to the same period last year, representing a decline of 33.42%.The company stated that the main reasons were the decrease in product ex-factory prices due to the implementation of volume-based procurement and the price discounts given for channel inventory replenishment, which led to a reduction in revenue during the reporting period.

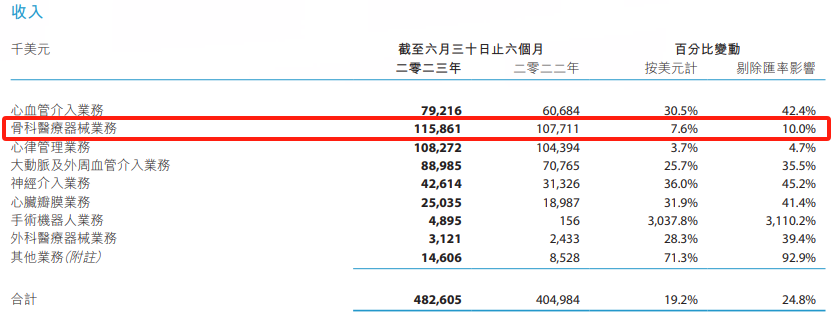

MicroPort ranked second with US$115.9 million (approximately RMB 7.58 billion), representing a 10.0% increase from the same period last year (excluding the impact of exchange rate fluctuations).Of which, domestic revenue reached 11.6 million US dollars, increasing by 51% year-on-year, fulfilling the volume growth logic brought by centralized procurement.

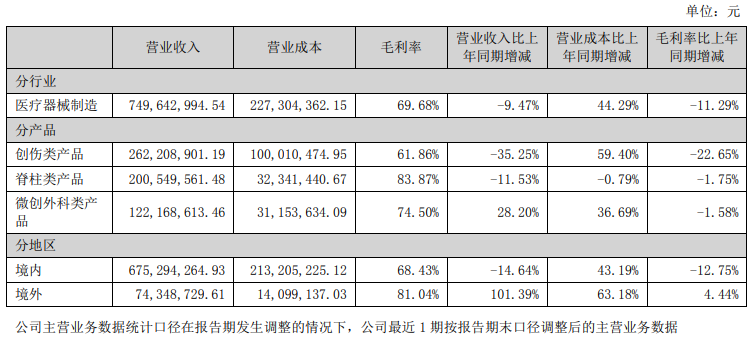

Double Medical's revenue in the first half of 2023 was RMB 7.50 billion, a decrease of 9.47% compared to the same period last year.

The company stated that the profit margin of its main products has declined due to the price reduction from centralized procurement, which will have a certain impact on the company's short-term revenue and profits.After the implementation of centralized procurement for orthopedic trauma and spinal consumables, the end-product prices dropped significantly. During the reporting period, the gross profit margin for orthopedic trauma products decreased to 61.86%, with revenue declining by 35.25% year-over-year; the gross profit margin for orthopedic spinal products decreased to 83.87%, with revenue dropping by 11.53% year-over-year. The gross margins for the company’s two main product categories declined. Following the implementation of centralized procurement for orthopedic joint consumables, the process of domestic substitution accelerated, further increasing product concentration. During the reporting period, the company's orthopedic joint products generated revenue of 58,265,655.57 yuan, representing a year-over-year increase of 104.46%.

AK Medical's Revenue in the First Half of the Year Reached 649 Million RMB, a 22.1% Increase Compared to the Same Period Last Year.The company stated that in the first half of 2023, with the end of the COVID-19 pandemic, the volume of orthopedic surgeries in China saw a rapid increase in the latter part of the first quarter, followed by stabilization at a relatively fast growth rate. Meanwhile, the steady implementation of the volume-based procurement policy further accelerated import substitution, allowing domestically produced brands to continue expanding their market share.

In terms of细分 business, AK Medical's hip and knee joint revenue reached RMB 552.5 million in the first half of the year, increasing by 21.2% year-on-year; the revenue of spinal and trauma implant products was RMB 50.2 million, up by 10.8% year-on-year.

Chunli Medical's revenue in the first half of the year was RMB 5.41 billion, a decrease of 5.37% compared to the same period last year, mainly due to the impact of "volume-based procurement" on the company's product sales, resulting in a decrease in the selling price of related products.

In terms of growth trends, as the state and provinces/municipalities routinely carry out centralized bulk procurement of high-value medical consumables, the three major fields of orthopedic joints, trauma, and spine have all been included in the scope of orthopedic medical consumables procurement, with implementation gradually being rolled out. The impact of such procurement on domestic companies is evident.

Next, let's take a look at the revenue rankings of various细分 fields in the orthopedic industry. Since most domestic orthopedic device companies have not disclosed细分 business revenue data, the following statistics only include the rankings of overseas device companies.

Zimmer Biomet ranks first in the global market share in the细分领域 of joint products. In the first half of this year, the company's revenue was $2.531 billion, a year-on-year increase of 9.76%.

Stryker ranked second with revenue of $1.896 billion and achieved a high growth rate of 14.56%.

In the spinal field, Medtronic ranked first globally with an income of $2.301 billion in the first half of 2023, representing a 4.24% decrease from the same period last year.

August 8, 2023Medtronic Announces Strategic Cooperation Agreement with Asia Pacific Medical Group, a Leading Medical Service Provider in ChinaThe two parties will cooperate to promote the implementation and promotion of advanced orthopedic and neurosurgical diagnosis and treatment services. The strategic cooperation between Medtronic and Asia Pacific Medical Group aims to establish an innovative integrated cooperation model, and carry out in-depth cooperation in treatment plans and surgical applications in related fields such as spinal surgery, trauma surgery, and bone tumors.

DePuy Synthes, a subsidiary of Johnson & Johnson, ranked second with $1.495 billion in revenue, representing a 4.11% increase from the same period last year.

Recently, Johnson & Johnson's DePuy Synthes and GE Healthcare have reached a collaboration to integrate GE Healthcare’s OEC 3D imaging system with DePuy Synthes' extensive product portfolio, aiming to better meet the needs of surgeons and patients.The OEC 3D imaging system can be used in fields such as orthopedics, cardiac, and vascular surgeries. It is reported that DePuy Synthes will focus this imaging technology on complex spinal surgeries.

The merged NuVasive and Globus Medical ranked third with revenue of $1.194 billion, increasing by 9.04% year-over-year.On September 1 this year, the two companies announced the completion of their merger. Since both parties involved in the transaction hold leading positions especially in the spine field, it is estimated that the merged company will become the world's second-largest spinal technology company, only after Medtronic.

ZimVie ranks fifth globally with $211 million, second only to Stryker. In March 2022, Zimmer Biomet spun off its spine, dental, and bone healing businesses to form a new company, ZimVie, which was independently listed.

Moreover, due to the impact of China's domestic spinal volume procurement, the company experienced a setback in its Q4 2022 performance. In March this year, ZimVie announced the complete withdrawal of its spinal business from China.

In the trauma business field, Stryker ranked first globally with a revenue of $1.535 billion, representing a year-on-year increase of 12.78%.

Johnson & Johnson DePuy Synthes ranked second with $1.496 billion.

——

The "2023-2028 In-depth Market Research and Investment Prospect Forecast Analysis Report on the Orthopedic Devices Industry" released by the New Think Tank Industry Research Center shows that in recent years, with the continuous improvement of global orthopedic treatment capabilities and the rapid development of orthopedic device technology, the global demand for orthopedic devices has been continuously increasing.As of 2022, the global orthopedic device market size has exceeded the 250 billion yuan mark.

China's orthopedic medical device industry is currently in an era of market expansion and import substitution. According to data from the Southern Medical Economic Research Institute, calculated based on revenue,The market size of orthopedic implant medical devices in China grew from 16.4 billion yuan in 2015 to 42.4 billion yuan in 2021, with a compound annual growth rate of 17.15%.

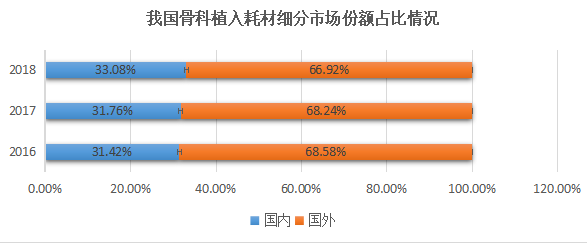

The market for orthopedic implant consumables in China will still be dominated by foreign brands. Foreign products occupy a significant share of the joint and spinal markets, and multinational orthopedic device companies have a strong competitive advantage in the high-end market due to their product technical performance and quality standards.

Image Source: Sanze Venture Capital

In 2021, China further advanced the reform of centralized bulk procurement of high-value medical consumables, implementing the requirements of relevant documents on the governance of high-value medical consumables reform. This aims to further improve procurement efficiency and promote the normalization of volume-based procurement.According to incomplete statistics, between 2021 and 2022, the average price reduction for trauma, joint, and spinal products in national and provincial-level centralized procurement in China was 73-89%.

Thanks to the centralized procurement policy for orthopedic consumables and the substitution of domestically produced products, the orthopedic implant consumables industry is expected to continuously increase industry concentration. Leading domestic companies are likely to further expand their market share, also driving more Chinese companies to participate in international competition.

According to the research and analysis of the online customs statistics data platform,In 2021, the export of orthopedic implants in China continued to increase, with an export value of approximately US$864 million, a year-on-year increase of 39% compared to 2022. Among the细分 markets, the export value of trauma and spine products was approximately US$646 million, a year-on-year increase of 44% compared to 2022. The export value of joint类产品 was US$218 million, up 28% year-on-year.

It can be said that bulk procurement is both a challenge and an opportunity. Looking ahead, Medical Device News will continue to monitor the potential changes in the global and domestic orthopedic markets.

More exciting content

Welcome to follow WeChat Video Channel

Global Third, Giant Enters This Track

4.6 Billion, Another Acquisition by Top 100 Medical Device Company

Boston Scientific Makes Significant Moves in Localization

Just now, the first rotary-type dental implant robot in China has been approved.

China's Only, "National Heavyweight" Medical-Engineering Base Breaks Ground

This Giant May Sell Part of Its Diagnostic Imaging Business

Olympus, Major Personnel Changes

SoftBank and Tencent Invest as Surgical Robots Make Big Moves

Major Executive Changes at the Largest Imaging Service Company in the U.S.

World's First: Chinese-Made Ultrasound to Combat "Female Killer"

BusinessBusiness cooperation email: qxzj@landianyiliao.com