Merck Inks $22 Billion Deal for Daiichi Sankyo's Three DXd ADC Candidates, Sending Stock Soaring

Daiichi - Sankyo

Pharmaceutical Development, Production, Sales, and Consulting Service Provider

MSD

Pharmaceutical R&D and Manufacturer

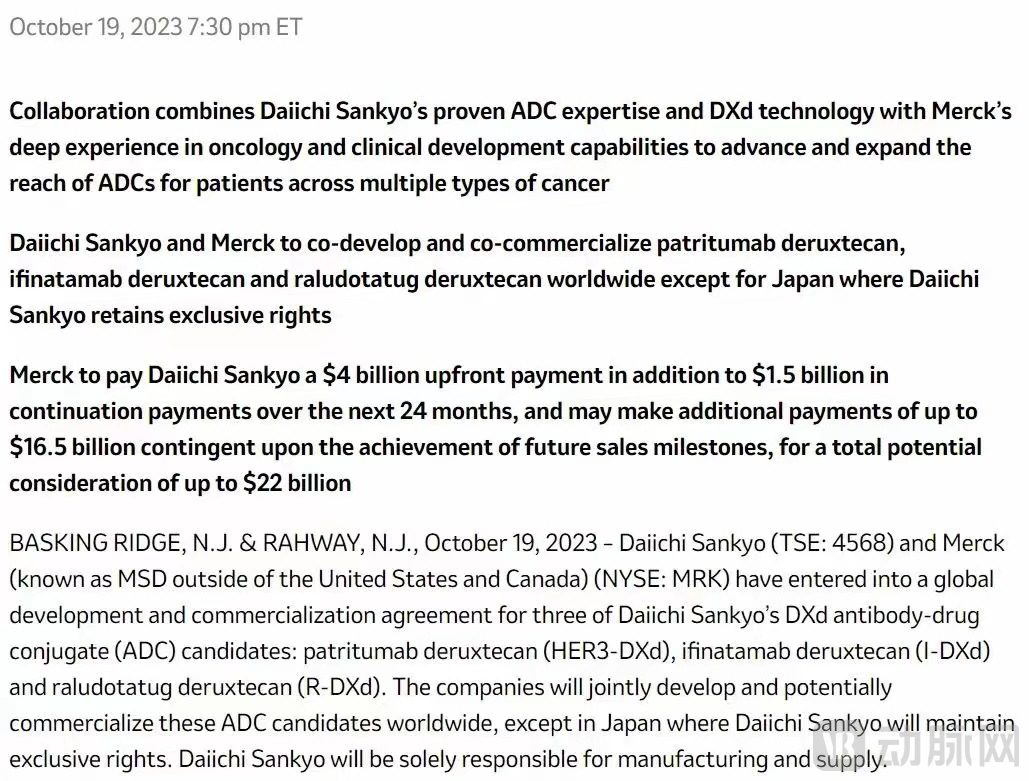

On October 19, MSD and Daiichi-Sankyo reached a global development and commercialization agreement for three DXd antibody-drug conjugate (ADC) candidates from Daiichi-Sankyo: patritumab deruxtecan (HER3-DXd), ifinatamab deruxtecan (I-DXd), and raludotatug deruxtecan (R-DXd).

The two companies will jointly develop the above three ADC candidate drugs and potentially commercialize them globally. Daiichi Sankyo will retain exclusive rights in Japan and will be fully responsible for the manufacturing and supply of the three candidate drugs.

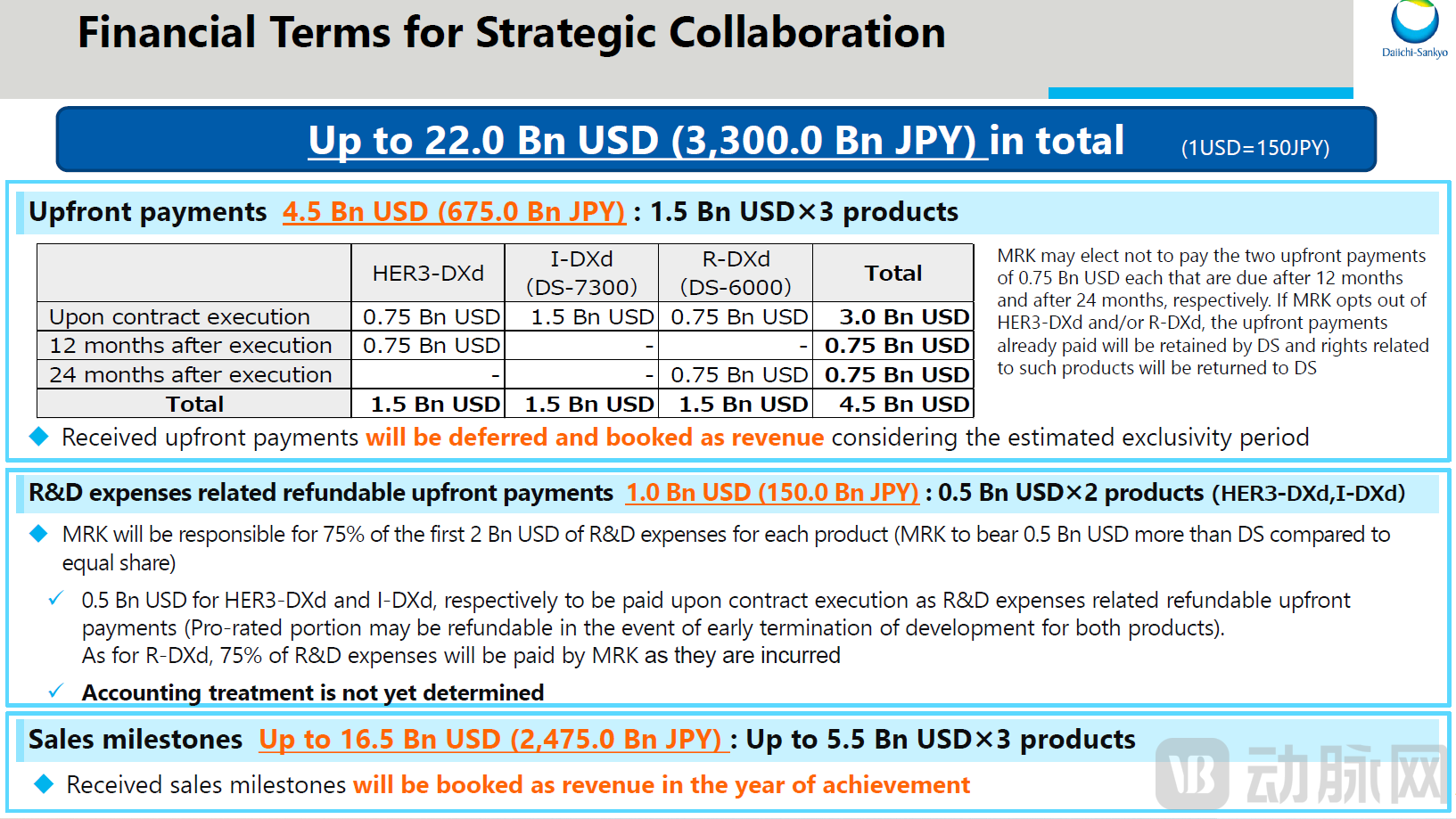

According to the agreement, MSD will pay $4.5 billion as an upfront payment, a $1 billion refundable upfront payment related to R&D costs, and up to $16.5 billion in commercial milestone payments, with the total agreement amounting to $22 billion.

Following the announcement, the share price of Daiichi-Sankyo surged by up to 18%, hitting a record high.

These three ADCs are all designed using Daiichi-Sankyo's proprietary DXd ADC technology, consisting of monoclonal antibodies connected through a cleavable linker based on tetrapeptides to multiple topoisomerase I inhibitor payloads.

As potential "first-in-class" therapies, all three products are currently in clinical development, primarily as monotherapies or in combination with other treatments for various solid tumors.

Patritumab deruxtecan, targeting HER3, was granted Breakthrough Therapy Designation by the U.S. FDA in December 2021 for the treatment of patients with locally advanced or metastatic non-small cell lung cancer (NSCLC) harboring EGFR mutations, whose disease progressed during or after treatment with a third-generation tyrosine kinase inhibitor (TKI) and platinum-based therapy. The Biologics License Application (BLA) for patritumab deruxtecan is planned to be submitted by the end of March 2024, based on the Phase 2 clinical trial named HERTHENA-Lung01. The trial results were recently presented at the IASLC 2023 World Conference on Lung Cancer.

Ifinatamab deruxtecan, targeting B7-H3, is currently being evaluated in a Phase 2 clinical trial named IDeate-01 for the treatment of patients with previously treated extensive-stage small cell lung cancer (SCLC). Updated results from a subgroup analysis of the Phase 1/2 trial of ifinatamab deruxtecan in SCLC were recently presented at the IASLC 2023 World Conference on Lung Cancer.

Raludotatug Deruxtecan Targeting CDH6 Is Currently Undergoing a First-in-Human Phase 1 Clinical Trial. CDH6 is a member of the cadherin family of proteins that is overexpressed in various cancers, particularly renal cell carcinoma and ovarian cancer. Overexpression of CDH6 is associated with tumor growth and proliferation and correlates with poor prognosis in renal cell carcinoma. Raludotatug deruxtecan is the sixth DXd ADC product from Daiichi-Sankyo’s oncology pipeline to enter clinical development and is currently under clinical investigation for safety and efficacy in adult patients with refractory or resistant advanced renal cell carcinoma and ovarian cancer. Updated results for the treatment of patients with advanced ovarian cancer will be presented at the upcoming European Society for Medical Oncology (ESMO) Congress 2023.

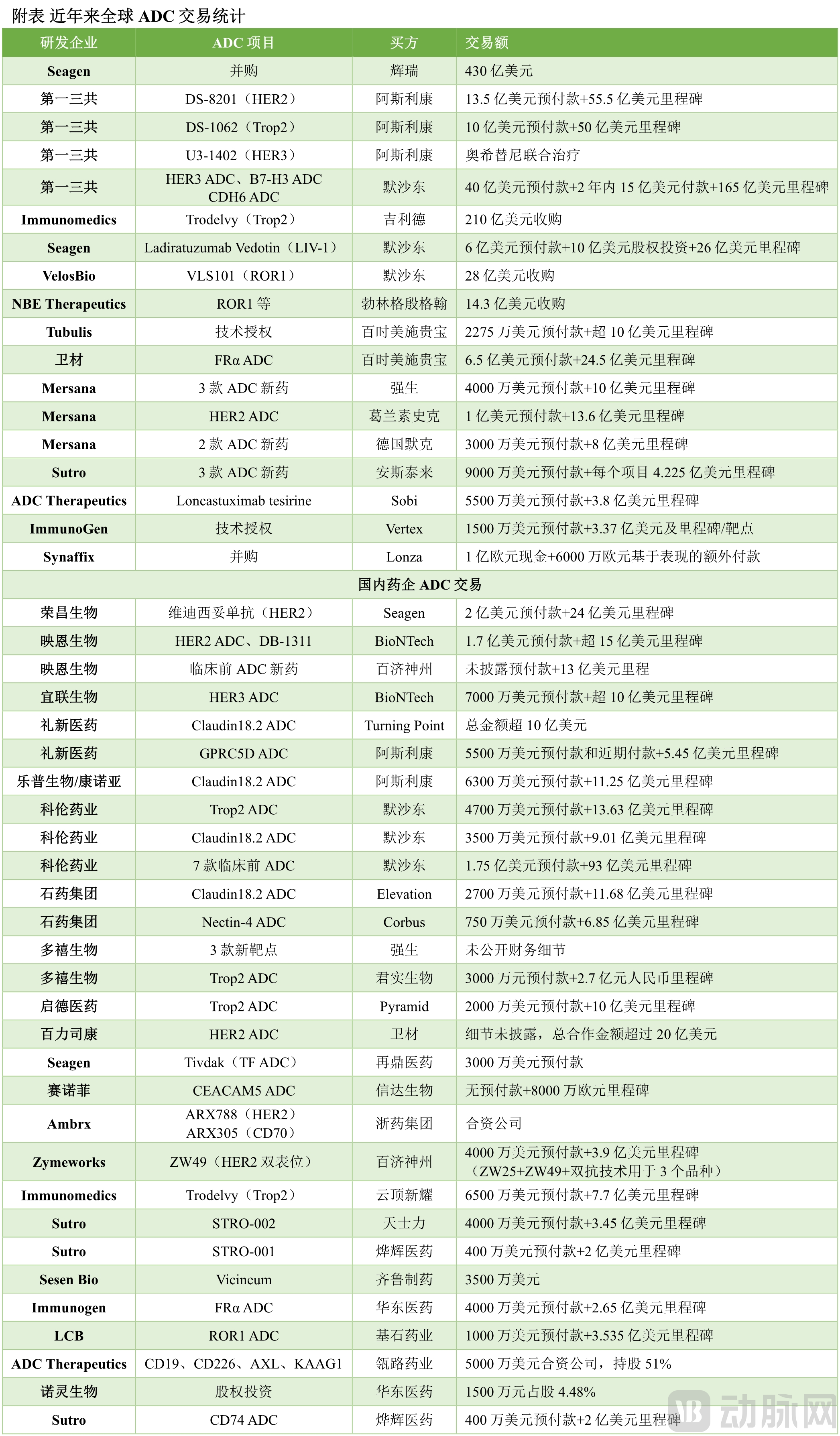

Daiichi Sankyo's DXd-ADC technology platform has gained recognition from AstraZeneca and MSD, cumulatively achieving $35 billion in licensing partnerships, with upfront payments totaling as high as $6.35 billion.

In recent years, the transaction volume in the ADC field has exceeded tens of billions of dollars, making it the most watched track in the innovative drug sector. MSD places particular emphasis on the ADC track, with an important direction after PD-1 combined with chemotherapy being the combination with ADC, further solidifying its leading position in the oncology field.

Global ADC Deal Statistics in Recent Years (Source: Armstrong Biopharmaceutical Information)

According to data from the prospectus of LePu BioPharm, the global ADC drug market size is expected to reach US$10.4 billion in 2024 and US$20.7 billion in 2030. The market is growing strongly, with a compound annual growth rate (CAGR) of 30.6% from 2019 to 2024 and a CAGR of 12.0% from 2024 to 2030.

The ADC market in China did not emerge until 2020. Although it started relatively late, it coincided with the golden age of ADC drug development, attracting global innovative pharmaceutical companies to enter the market. Overseas enterprises are increasingly investing in China's pharmaceutical market, creating a favorable situation for domestic Biotech pipelines to expand internationally.

There is no doubt that the United States holds a global leading position in the biopharmaceutical industry. As the center of global biopharmaceutical development, the U.S. has formed five major biopharmaceutical industry bases, including Boston, San Diego, and the North Carolina Research Triangle Park, achieving comprehensive development and innovation in细分药品领域 such as oncology drugs, immunology drugs, cardiovascular drugs, anti-infective drugs, vaccines, and neurological drugs.

According to Sullivan data, as of June 10, 2022, using market capitalization ranges of $50 billion and $10 billion, there are 11 pharmaceutical companies in the U.S. market with a market cap above $50 billion, accounting for 2.6% of the total number of companies in the U.S. pharmaceutical sector, yet representing 84.9% of the total market value. There are 8 companies with a market cap between $10 billion and $50 billion, holding approximately 7.1% of the market value. The top 39 companies with a market cap above $10 billion make up only 4.5% of the total number of companies in the U.S. pharmaceutical sector, but their combined market value reaches $2.3 trillion, accounting for 92.1% of the total market value of the pharmaceutical sector.

For enterprises targeting the global market, it is inevitable to develop their product pipelines with the "dual filing in China and the U.S." strategy. Innovative technology platform companies in China have the potential to explore different targets for generating more products, but such companies have limited resources and energy, necessitating external collaborations for mutual growth and success.

Therefore, when it comes to the selection of partners, it is best to have different orientations for different targets. But essentially, it is still necessary to consider whether the other party can form a complementary advantage with oneself, whether they are willing to provide resources and capabilities to commercialize the product, and ensure the maximization of the company's rights and interests.

Analyzing the overseas expansion of other Biotech companies in China, it is not difficult to find that these successful companies, in addition to having solid underlying technologies to support project advancement, must also possess resources and development strategies in BD (Business Development).

For example, when interacting with partners, most foreign pharmaceutical companies possess mature industrialization experience and comprehensive resources deeply rooted in the local pharmaceutical market. Many domestic companies often value their resources during collaborations.

Secondly, a good cooperative relationship requires close and comprehensive communication before reaching an agreement. Relationships and understanding need to be built through long-term, frequent exchanges, including comprehension of product technology, innovation logic, and clinical data. Such exchanges will无形中 also form a perception and recognition of the overall strength of the enterprise. Importantly, domestic companies in China should also take the initiative to speak out, actively participate in activities, and engage in face-to-face communication to help the industry and partners better understand the company itself.

Looking back at the pharmaceutical industry's expansion overseas, it is actually no longer a "one-way pursuit" for Chinese pharmaceutical companies. Recently, almost every week brings good news of domestically produced pipelines going global.

The rapid growth of China's biopharmaceutical market cannot be underestimated, and at the same pace, the source innovation of China's pharmaceuticals is also growing rapidly. The overseas markets have also recognized this potential, extending olive branches to domestic companies. Meanwhile, companies like Pure Genuine, Impelino, and Phstar, operating both domestically and internationally, are actively assisting domestic enterprises in conducting global clinical trials, submitting regulatory approvals, and implementing commercial strategies.

According to Sullivan data, the market size of biopharmaceuticals in China was RMB 312 billion in 2019 and is expected to reach RMB 712.5 billion by 2024 and RMB 1,302.9 billion by 2030. The compound annual growth rate (CAGR) from 2019 to 2024 is 18.0%, and the CAGR from 2024 to 2030 is 10.6%. During these two periods, the global biopharmaceutical market size CAGR is 9.8% and 9.0%, respectively.

Eisai, AstraZeneca, Roche, GSK, Sanofi, MSD, and several other global pharmaceutical giants have been highly active in the Chinese market in recent years. Taking today's star company BioNTech as an example, within the last 10 months of this year alone, it has reached licensing cooperation agreements for over seven projects with Chinese companies such as Yilian Biotech, DualityBio, OncoC4, and Premas Biotech.

Think about it from another perspective: When domestic companies talk about dual filings in China and the U.S. or "In China for Global," will overseas companies in the future also consider entering the Chinese pharmaceuticals market as the gold standard for their global strategies?