Billion-Dollar Rhythm Management Market Dominated by Medtronic, Abbott, and Boston Scientific—Can Chinese Brands Break Through?

Lepu Medical

Developer and Manufacturer of Cardiac Interventional Medical Devices and Pharmaceuticals

Singular Medical

Developer, Manufacturer, and Seller of Cardiac Rhythm Management Products

Lifetech Cardio

Cardiac Rhythm Management Device Supplier

Earning Over 10 Billion USD Annually, How Attractive is the Cardiac Rhythm Management Market?

According to VCBeat, this track exceeding 10 billion US dollars is currently mainly divided among three major multinational medical device companies. Among them, Medtronic dominates the cardiac rhythm management market, generating 5.783 billion US dollars in revenue in this细分 market in 2022; Abbott and Boston Scientific are neck and neck, achieving revenues of 2.119 billion US dollars and 2.1 billion US dollars respectively in 2022. The combined revenue of the three giants in the cardiac rhythm management sector reached 10.002 billion US dollars.

(Note: Medtronic's fiscal year 2023 period is from April 30, 2022 to April 28, 2023)

Apart from the three giants, Biotronik, a leading German medical device company, also holds a significant position in the cardiac rhythm management market. According to data released by Frost & Sullivan, Biotronik's revenue in the cardiac rhythm management market was approximately $1.637 billion in 2021, accounting for 15.4% of the global market share.

It can be said that Medtronic, Abbott, Boston Scientific, and Biotronik have almost monopolized the global cardiac rhythm management market, and all of them have made substantial profits.

Strangely enough, domestic entrepreneurs who often swarm into popular tracks and blue ocean marketsFacingCardiac Rhythm ManagementFieldbut came to a halt.So far, only a few companies, such as MicroPort Cardiac Rhythm Management Limited, Lifetech Cardio, Lepu Medical, Singular Medical, and Suzhou Weiweisi Medical Technology Co., Ltd., have entered the cardiac rhythm management sector in China.

We can't help but ask: Why do domestic entrepreneurs who are keen on laying out emerging tracks collectively stop at cardiac rhythm management? How high are the entry barriers for the cardiac rhythm management market? Where does the technical difficulty lie in products related to cardiac rhythm management? Against the backdrop of global market fluctuations, do domestic entrepreneurs still have the opportunity to break into and make headway in the cardiac rhythm management track?

Cardiac rhythm management devices refer to implantable devices that treat arrhythmias and heart failure through electrical stimulation, including pacemakers, implantable cardioverter defibrillators (ICD), cardiac resynchronization therapy defibrillators (CRT-D), cardiac resynchronization therapy pacemakers (CRT-P), insertable cardiac monitors, and more.

(Cardiac Rhythm Management Product Classification)

Among them, a pacemaker is a small device implanted subcutaneously in the chest, including a pulse generator, leads, and electrodes, mainly used to treat bradycardia. When bradycardia or skipped heartbeats are detected, the pulse generator sends electrical impulses, which are conducted through the leads and electrodes to stimulate the myocardium in contact with the electrodes, causing the heart to excite and contract, ultimately achieving the purpose of treating bradycardia.

ICD (Implantable Cardioverter Defibrillator) is also a small device placed under the skin in the chest that continuously monitors the heartbeat and can stop arrhythmias with an electric shock when necessary. In practice, doctors implant the pulse generator between the pectoralis major and minor muscles and insert leads through the subclavian vein into the right ventricle of the heart to detect ECG signals and identify arrhythmias. When arrhythmia is detected, the ICD can deliver an electric shock within a short period to restore normal heart rhythm.Based on this, ICD implantation has gradually become the main treatment and preventive measure for tachycardia and sudden cardiac death.。

CRT-D (Cardiac Resynchronization Therapy Defibrillator) and CRT-P (Cardiac Resynchronization Therapy Pacemaker) are both medical devices used to treat heart failure. Heart failure can be classified into left-sided heart failure, right-sided heart failure, and congestive heart failure. After implantation in the heart, CRT devices improve the synchronization of ventricular contractions and pumping efficiency by electrically stimulating the sequential contraction of the left and right ventricles, thereby reducing mortality caused by heart failure. Specifically, CRT-P can pace both the left and right ventricles simultaneously to resynchronize the heart, while CRT-D provides high-energy defibrillation shocks on top of cardiac resynchronization to treat life-threatening rapid arrhythmias.

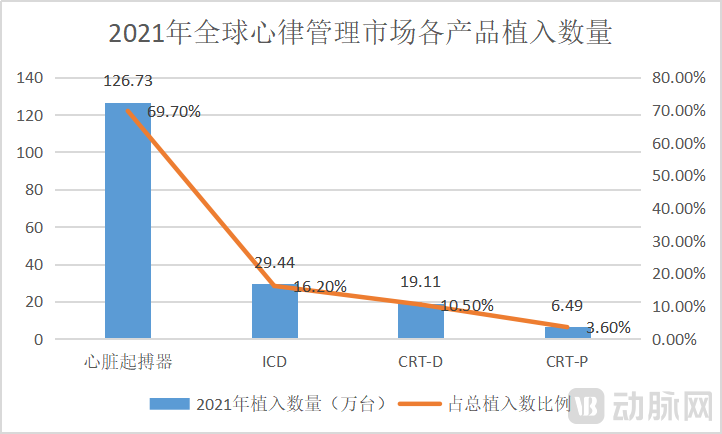

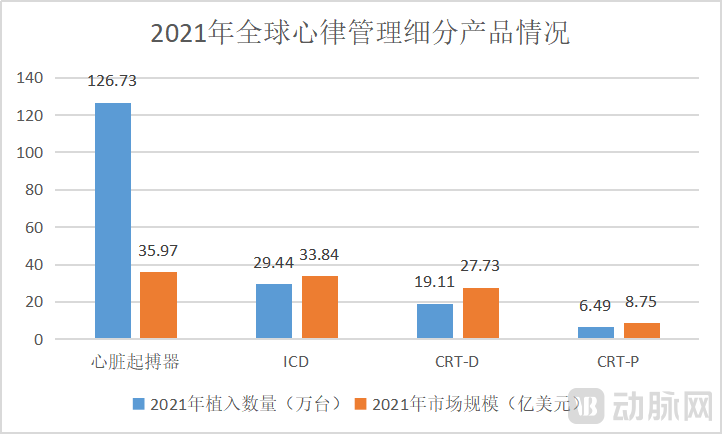

In the global cardiac rhythm management market, pacemakers are the single largest implantable device.According to the prospectus of MicroPort Cardiac Rhythm Management Limited, in 2021, 1.2673 million pacemakers were implanted globally, accounting for 69.7% of the total number of cardiac rhythm management product implants; 294,400 ICDs were implanted, accounting for 16.2%; 191,100 CRT-Ds were implanted, accounting for 10.5%; and 64,900 CRT-Ps were implanted, accounting for 3.6%.

Although the number of implants is the highest, the market size of pacemakers is about to be surpassed by ICD.According to statistics, in the global cardiac rhythm management market in 2021, the pacemaker market was $3.597 billion, the ICD market was $3.384 billion, the CRT-D market was $2.773 billion, and the CRT-P market was $875 million. It can be seen that the implantation volume of over a million pacemakers accounts for only 33.8% of the cardiac rhythm management market, while the implantation volume of less than 300,000 ICDs occupies 31.8% of the cardiac rhythm management market.

This is because compared to pacemakers, which are priced between 20,000 and 60,000 yuan each, products like ICDs, CRT-Ds, and CRT-Ps are more expensive. For instance, in Guangdong province, the average selling price of an ICD before the centralized procurement was 140,600 yuan per unit. Additionally, ICDs are considered the most effective treatment currently available for preventing sudden cardiac death. Their adoption rate is expected to accelerate, with the potential to become the next blockbuster product in the cardiac rhythm management field.

It is worth mentioning that the penetration rate of cardiac rhythm management in emerging markets such as China and India is still relatively low, and it is currently in a period of rapid growth.Meanwhile, the revenue from the cardiac rhythm management businesses of giants like Medtronic, Abbott, and Boston Scientific continues to maintain steady growth.

For example, Medtronic's Q1 2024 earnings report (April 28, 2023 - July 28, 2023) showed that: In the first quarter, the product portfolios under its cardiac rhythm management business, including defibrillation solutions, cardiovascular diagnostics, cardiac ablation solutions, and cardiac pacing therapy, all achieved mid-single-digit growth, while the Micra transcatheter pacing system achieved mid-double-digit growth.

According to data released by Frost & Sullivan, the global cardiac rhythm management device market has grown from USD 9.7 billion in 2016 to USD 10.6 billion in 2021 and is expected to reach USD 12.8 billion by 2030. Market participants include only a few companies such as Medtronic, Abbott, Boston Scientific, Biotronik, and MicroPort Cardiac Rhythm Management Limited.

Facing this blue ocean market with a large scale, few competitors, and high entry barriers, there are very few players in China. Currently, only a handful of companies such as MicroPort Cardiac Rhythm Management, Lepu Medical, Lifetech Cardio, Singular Medical, and Suzhou Weiweisi Medical Technology have made their moves. Why has cardiac rhythm management kept domestic entrepreneurs, who are usually enthusiastic about golden tracks, from flooding into the field? How difficult is the technology? And how high are the entry barriers?

VCBeat found that compared to other niche markets, the cardiac rhythm management industry has extremely high entry barriers in terms of technology, market concentration, regulation, and service.

First, cardiac rhythm management is considered the most technologically advanced细分 industry in the cardiovascular field.,Involving multiple disciplines such as cardiovascular physiology, bioengineering, computer science, electronic engineering, and materials science. Cardiac rhythm management products are small in size, capable of delivering electrical impulses, and need to be implanted into the heart, requiring extremely high levels of safety and reliability. The related technical challenges are immense, with a high entry threshold.

For example, a pacemaker is composed of components such as a pulse generator, leads, and electrodes. Inside the pulse generator, there are core components like integrated circuits, batteries, and chips. Each of these core components has technological barriers; for instance, the power release management and stability of the battery require extremely high precision. More importantly, core components of domestically produced pacemakers, such as chips, leads, and batteries, are highly dependent on imports.

Compared with pacemakers, ICDs, as high-voltage products, have higher technical difficulty. It is reported that the development of ICD products requires overcoming multiple high-difficulty technologies, such as high-efficiency high-voltage charge-discharge modules, drug-release systems for leads, UI design for programming, and sensing recognition algorithms.

Besides, another perspective also illustrates the technical difficulty of cardiac rhythm management: currently, in China, only Lepu Medical, MicroPort Cardiac Rhythm Management (under MicroPort Medical), and Lifetech Cardio have launched pacemakers; only MicroPort Cardiac Rhythm Management and Singular Medical have developed ICD products; and only MicroPort Cardiac Rhythm Management is capable of producing CRT-D.

Among them, the initial pacemaker technologies of Lepu Medical, MicroPort Cardiac Rhythm Management, and Lifetech Cardio were all sourced from overseas companies. For instance, Qinming Medical, which was acquired by Lepu Medical, was founded byCPM Company, Minnesota, USAInvested 735,000 USD and technology to establish a joint venture with Baoji Qinling Transistor Factory; MicroPort Cardiac Rhythm Management Limited under MicroPort Medical, andSorin Group ItalyJointly established; Lifetech Cardio introduced through technology transfer.MedtronicCardiac pacemaker products.

Second, the cardiac rhythm management market is highly concentrated and monopolized by giants like Medtronic., new entrants will face competition from multiple giants, making it highly challenging. Specifically, due to the high monopoly of the cardiac rhythm management industry by overseas giants,China lacks technical talent and experience accumulation in the cardiac rhythm management industry.In China, domestic companies must start from scratch in the research and development of cardiac rhythm management.

Not only do they lack technology and talent, but domestic companies also need to address issues related to funding, patents, and the supply chain. In terms of funding, cardiac rhythm management, as a high-tech threshold industry, requires companies to invest substantial capital in purchasing relevant equipment, raw materials, and core components for research and development. Additionally, after developing a product, domestic companies must spend significant funds conducting large-scale clinical trials in regions where they plan to go public, in order to submit registration applications. This threshold requirement restricts many small and medium-sized enterprises that lack sufficient funding.

In terms of patents,Overseas giants have monopolized the cardiac rhythm management industry for many years, forming patent barriers across all cardiac rhythm management products., companies in China need to bypass patents and independently develop innovative cardiac rhythm management products to avoid infringement issues.

In the supply chain, domestic companies may encounter issues such as chip discontinuation when procuring key components like overseas chips, leads, and electrodes for research and development.Overseas suppliers affected by giants unable to supplySuch situations occurred during the development of ICD products by Singular Medical, which experienced five discontinuations or supply stoppages of critical bare chips (DIE) for high-voltage modules within four years. Fortunately, today, nearly all key components of Singular Medical's high-voltage module have been replaced, truly gaining independent control over research, development, and production.

In addition to the above challenges, domestic companies that have developed related products also need to overcomeCommercialization, Market CompetitionSuch barriers. Among them, overseas giants have monopolized the market for many years, holding advantages in brand, reputation, doctor trust, and service capabilities. New entrants need to find alternative ways to enter the market.

Third, the cardiac rhythm management industry requires relevant companies to have timely after-sales service and excellent patient management capabilities.This is because, after the use of cardiac rhythm management products, they will remain in the patient's body for a long time. Relevant companies need to provide long-term support from doctors and hospitals for patients with implanted devices, and need to conduct long-term tracking of the implanted devices to ensure the proper functioning of the related products.

Overall, although cardiac rhythm management is a golden track with a large scale, rapid growth, and promising prospects, its entry barriers are high, the technical difficulty is great, and many domestic entrepreneurs find themselves unable to make progress despite their ambitions.

So far, cardiac pacemakers have been included in centralized procurement multiple times. This policy, which has the potential to alter market dynamics, provides an excellent opportunity for the accelerated development of China's cardiac rhythm management companies.

In 2019, Jiangsu carried out China's first centralized procurement of pacemakers, with an average price reduction of 15.86% and a maximum reduction of 38.18%. Subsequently, provinces and cities such as Yunnan, Anhui, Qinghai, Shandong, Fujian, Shaanxi, Beijing, Tianjin, and Hebei either independently or jointly conducted centralized procurement of pacemakers. The average price reduction for this product expanded from 15.86% to 60%, while the maximum reduction increased from 28.18% to 69%. However, in most regions, the centralized procurement of pacemakers has been relatively moderate, with an average price reduction not exceeding 50%.

The industry expects that volume-based procurement will reduce the end-user prices of rhythm management devices such as pacemakers, thereby increasing the sales volume and penetration rate of these devices.At the same time, domestic enterprises are expected to enter the market through centralized procurement, exchanging price for market share and quickly achieving commercialization.Companies with approved products in China, such as MicroPort Cardiac Rhythm Management, Lepu Medical, and Lifetech Cardio, have been awarded multiple bids in centralized procurement and achieved commercial revenue.

However, enterprises in China still face significant challenges.The prospectus of MicroPort Cardiac Rhythm Management Limited shows that in 2021, its revenue in China was 13.06 million US dollars, increasing by 51.3% year-on-year excluding the impact of exchange rate; in 2022, its revenue in China was 12.72 million US dollars, increasing by 8.4% year-on-year excluding the impact of exchange rate.

Lifetech's latest released 2023 interim results show that: In the first half of 2023, revenue from its pacemaker and cardiac rhythm management business, whose main products are implantable cardiac pacemakers and pacemaker leads, was 32.9 million yuan, a year-on-year decrease of 24.7%. Whereas in the first half of 2022, this business achieved a growth of 187.5%.

On the other hand, China has become the third-largest cardiac rhythm management market globally, with a relatively low penetration rate of cardiac rhythm management devices domestically, indicating significant room for development. Data released by Frost & Sullivan shows that in 2021, the number of cardiac rhythm management device implants per million people in Europe reached 1,065, while in China, the figure was only 89.7 implants per million people, a difference of more than tenfold.

Believe that with the improvement of China's economic level, residents' purchasing power, and patients' acceptance, the penetration rate of cardiac rhythm management devices will increase significantly. With the implementation of centralized procurement and the increase in the penetration rate of cardiac rhythm management, China’s cardiac rhythm management market will further expand. It can be foreseen that in the future cardiac rhythm management market, China will be one of the most important markets globally. Domestic companies that adapt to centralized procurement will have certain advantages.

In addition to geographical advantages, domestic enterprises have also made breakthroughs in cardiac rhythm management technology and products.

In early October 2023, the ICD product ULYS and the defibrillation lead INVICTA developed by MicroPort Cardiac Rhythm Management Limited were approved for marketing in Japan.It is reported that this ICD product adopts innovative technology with low power consumption, and its expected service life can be extended up to 8 years, the longest among currently available ICD products on the market. Additionally, this ICD product is equipped with the PARAD+ arrhythmia discrimination algorithm, which has been clinically proven to have a lower rate of inappropriate shock defibrillation.

In addition,MicroPort Cardiac Rhythm Management Limited has also laid out the latest developments in the field of cardiac rhythm management — leadless pacemakers and subcutaneous implantable cardioverter defibrillators (S-ICD).Leadless pacemakers can avoid complications associated with traditional pacemakers, such as pocket infections, lead dislodgement, and lead fractures. The S-ICD effectively avoids lead-related complications faced by transvenous ICDs and reduces the risk of infection. Currently, giants like Medtronic and Abbott have launched leadless pacemakers, Boston Scientific has introduced the S-ICD, and MicroPort Cardiac Rhythm Management Limited has laid out related products to accelerate its catch-up.

In September 2023, Singular Medical's ICD product passed the review of the National Medical Products Administration (NMPA) and entered the special review process (also known as the "Green Channel").. This product is the first implantable cardioverter defibrillator (ICD) to enter the special innovative review process. Previously, Singular Medical successfully completed China's first domestically produced ICD human clinical trial in April 2023.

According to reports, the ICD independently developed by Singular Medical has full independent intellectual property rights. It features a streamlined design and can achieve functions such as automatic sensing and pacing, 40J energy charge and discharge, and Bluetooth telemetry. Its performance rivals mainstream imported products. Through clinical research, Singular Medical has preliminarily confirmed the working status and defibrillation function of its ICD product in real human environments.

In August 2022, Suzhou Weiweisi Medical Technology Co., Ltd. was successfully selected as a leading organization for innovative tasks in artificial intelligence medical devices with its "Wearable Cardioverter Defibrillator (WCD) and Sudden Death Risk Artificial Intelligence Assessment System," becoming the main body responsible for tackling these innovative tasks.Previously, Weiweisi's WCD product had entered the green channel for innovative medical device review in 2021 and began clinical enrollment preparation in 2022. The wearable cardioverter defibrillator (WCD) can provide continuous protection during the wearing period for patients at high risk of sudden cardiac death in the short term and perform automatic defibrillation when the patient experiences cardiac arrest due to ventricular arrhythmia.

So far, companies such as MicroPort Cardiac Rhythm Management, Lifetech Cardio, Lepu Medical, and Singular Medical have ignited the spark. It is expected that more domestic companies will enter the cardiac rhythm management field in the future, accelerating innovation and breaking through barriers. Meanwhile, giants like Medtronic, Abbott, and Boston Scientific will find it increasingly difficult to constrain China's cardiac rhythm management industry.