Global MedTech Giants Accelerate Local Manufacturing in China, Signaling Strategic Shift Toward Integrated Localization and Supply Chain Reshaping

Boston Scientific

Medical Device Manufacturer

In October 2023, China announced the complete removal of foreign investment access restrictions in the manufacturing sector.

This favorable policy is undoubtedly aimed at attracting global high-end manufacturing owners and enhancing China's position in the global high-end manufacturing industry.

High-end medical devices are known as the "jewel in the crown" of the manufacturing industry. China is the world's second-largest medical device market, but its domestic medical device industry has long exhibited the "two 90%" characteristics: 90% of high-end medical devices rely on imports, and about 90% of domestically produced medical devices are mid-to-low-end products.

Against the backdrop of favorable policies, the medical and pharmaceutical sector had the highest frequency of visits by executives of multinational companies visiting China in 2023.

Multiple medical technology MNCs (multinational corporations) have also committed to increasing their investments in China, making significant contributions to the Chinese industrial chain. Companies such as Boston Scientific, Intuitive Surgical, BD Medical, and GE Health have directly announced expansions in their research, development, production, and manufacturing operations, enhancing localized production capacity.

Among them, Boston Scientific has established its first production and manufacturing base in China, with the project located in Lingang, Shanghai, and it is a major foreign investment project in Shanghai, similar to Tesla's energy storage Gigafactory.

As MNCs Establish Factories in China, the Boundary Between Domestically Produced and Imported High-End Medical Devices is Gradually Blurring, Reshaping China's High-End Medical Device Industry Chain; the Center of Global Advanced Medical Device Manufacturing is Expected to Shift to China.

Why Are MNCs Choosing to Build Factories in China?

The answer to this question can be found in the financial reports of major MNCs. It's not difficult to notice in the annual reports that China remains the most attractive medical technology market in the world.

According to data from Roland Berger's "Current Status and Trends of China's Medical Device Industry Development," in 2022, the scale of China's medical device market is expected to reach 958.2 billion RMB, with a compound annual growth rate of approximately 17.5% over the past seven years, making it the world's second-largest market outside of the United States. The growth rate, scale, and innovation ecosystem of China’s medical technology market continue to attract multinational corporations (MNCs) to expand their presence.

Although China is already the world's second-largest medical technology market, revenue from the Chinese market accounts for only about 10% of global total revenue in MNC financial reports, or even lower. For instance, Medtronic's revenue from the Chinese market makes up approximately 7% of its total revenue.

The potential of the ever-growing medical technology market still needs to be further tapped, and localization is the booster for increasing revenue in the Chinese market.

Building factories in China can directly increase the revenue share from the Chinese market. Take Philips as an example. Philips began implementing a localization strategy in China ten years ago. Currently, nearly 100% of Philips' precision diagnosis business product lines (including ultrasound, CT, and other products) are produced in China. Through deep localization, revenue from the Chinese market accounts for 15% of Philips’ total revenue.

The driving factors for MNCs to build factories in China include both opportunities and challenges.

One aspect of the challenge comes from payment reform, with the goal of deepening the medical and health system reform clearly stating the normalization of centralized bulk procurement of medical consumables. At the same time, deepen the reform of diversified and composite medical insurance payment methods, implementing Diagnosis-Related Groups (DRG) payment or Diagnosis-Intervention Packet (DIP) payment reform in no less than 70% of coordinated regions. Medical insurance cost control makes sustaining high growth in the Chinese market more challenging.

Another aspect of the challenge comes from the changing competitive landscape, with an increase in local competitors in China's high-end medical device industry.The number of local players in China's medical device market is increasing, and their strength is also growing.

The "involution" characteristics of the Chinese market, such as declining profit margins and severe homogenization competition, place higher demands on the cost control capabilities and market responsiveness of MNCs. Improving operational efficiency and reducing costs while increasing effectiveness have become imperative.

In terms of labor factors, China has a large number of mid-to-high-end talents with innovative capabilities and industrial support; during the COVID-19 pandemic, China's supply chain also demonstrated safety and resilience. MNCs setting up factories in China can not only reduce production costs and respond more agilely to changes in the Chinese market but also efficiently integrate global resources.

How will multinational companies setting up factories in China reshape the high-end medical device industry chain in China?

First, the localization rate of high-end medical device products will be increased to enhance China's advanced medical device manufacturing capabilities.

Taking Boston Scientific as an example, Boston Scientific is a global leader in the cardiovascular and surgical device fields. In the precision PCI market, Boston Scientific boasts a diverse and comprehensive product portfolio including IVUS, balloons, stents, and more, holding dominant positions in multiple细分 markets worldwide. In the field of cardiac electrophysiology, Boston Scientific is the first medical technology company globally to offer a complete set of "ice," "fire," and "electricity" atrial fibrillation ablation solutions.

Through its localization strategy in China, in 2022, Boston Scientific's Polaris intravascular ultrasound system officially received local registration certification, achieving local production while also supplying the global market. The intravascular ultrasound system involves various high-barrier technologies, including high-torque transmission microcatheter design and implementation, imaging algorithms and precise control, and miniature ultrasound transducers.This product, made in China, will bring rich manufacturing experience and technical accumulation to the domestic industry.

Boston Scientific's establishment of a production and manufacturing center in Lingang, Shanghai, will lead to more advanced medical devices, such as the Polaris intravascular ultrasound system, being manufactured in China. This not only strengthens China's high-end medical device manufacturing capabilities but also has the potential to drive the export of China's high-end medical devices.

From Huawei in China to China for the globe, as MNCs engage in technology research, development, and industrialization in China, MNCs can also serve as a bridge for high-end domestically produced medical devices to reach international markets.

The second major spillover effect is the boost to the upstream industrial chain.MNCs Establishing Manufacturing Centers in China Follow Two Major Development Trends: Achieving Complete Localization of Finished Products Before Localizing Core Components; Localizing Basic Products Before Advancing to High-End Medical Production Lines.

This trend can be verified by the development in the medical imaging field. GE and Philips were the first to set up factories in China, and currently, the localization rate of GE Healthcare and Philips' imaging diagnostic products produced in China has exceeded 90%. Among them, more than 2,000 components used in GE's Beijing factory are provided by over 600 local suppliers.

It can be foreseen that MNCs building factories in China will bring more opportunities to the upstream industrial chain, and the upstream parts industry produced in China is expected to further grow.

At present, the integrity, stability, and competitiveness of China's medical device industry chain are not strong overall. In particular, the localization rate of high-end medical devices is not high, innovation resources of domestic enterprises are limited, and there are few companies engaged in the independent research and development of key components and important raw materials. China has also been a major importer of medical devices.

Taking high-value cardiovascular consumables as an example, the manufacturing of China's cardiovascular industry generally relies on overseas suppliers; for instance, over 90% of medical precision catheters come from imported suppliers.

The establishment of a manufacturing center in China by a leading cardiovascular intervention company like Boston Scientific is expected to drive the development of China's cardiovascular intervention medical device industry chain. The production and manufacturing centers set up by multinational corporations (MNCs) in China are likely to cultivate local suppliers while leading domestic component suppliers to the global stage, injecting more vitality into the high-end medical device industry chain.

The establishment of a production and manufacturing center is actually a strategic microcosm of MNC's deepening localization in China.

Recently, McKinsey pointed out in an article that the model of MNCs and domestic companies relying solely on sales and multi-layer distributors during the high-growth period of the industry is no longer sustainable.Due to the continued uncertainty of policies, it is more challenging to maintain high growth in China's medical technology market, and MNCs need to readjust their models to address these challenges.

What strategic adjustments can lead to success? McKinsey believes that MNCs need to reallocate commercial resources. Companies that focus on innovative, high-growth product categories will perform better in competition compared to those that only concentrate on existing products in the Chinese market.

McKinsey pointed out that Boston Scientific and Abbott are representatives of this strategic adjustment. In 2022, Boston Scientific accelerated the launch of a series of innovative products in the Chinese market, including the Rezūm Thermal Therapy System for treating benign prostatic hyperplasia, the TheraSphere Y90 Glass Microspheres System, and the SpaceOAR Absorbable Hydrogel Spacer. Boston Scientific also invested more resources to support the entry of additional innovative products into the Chinese market.

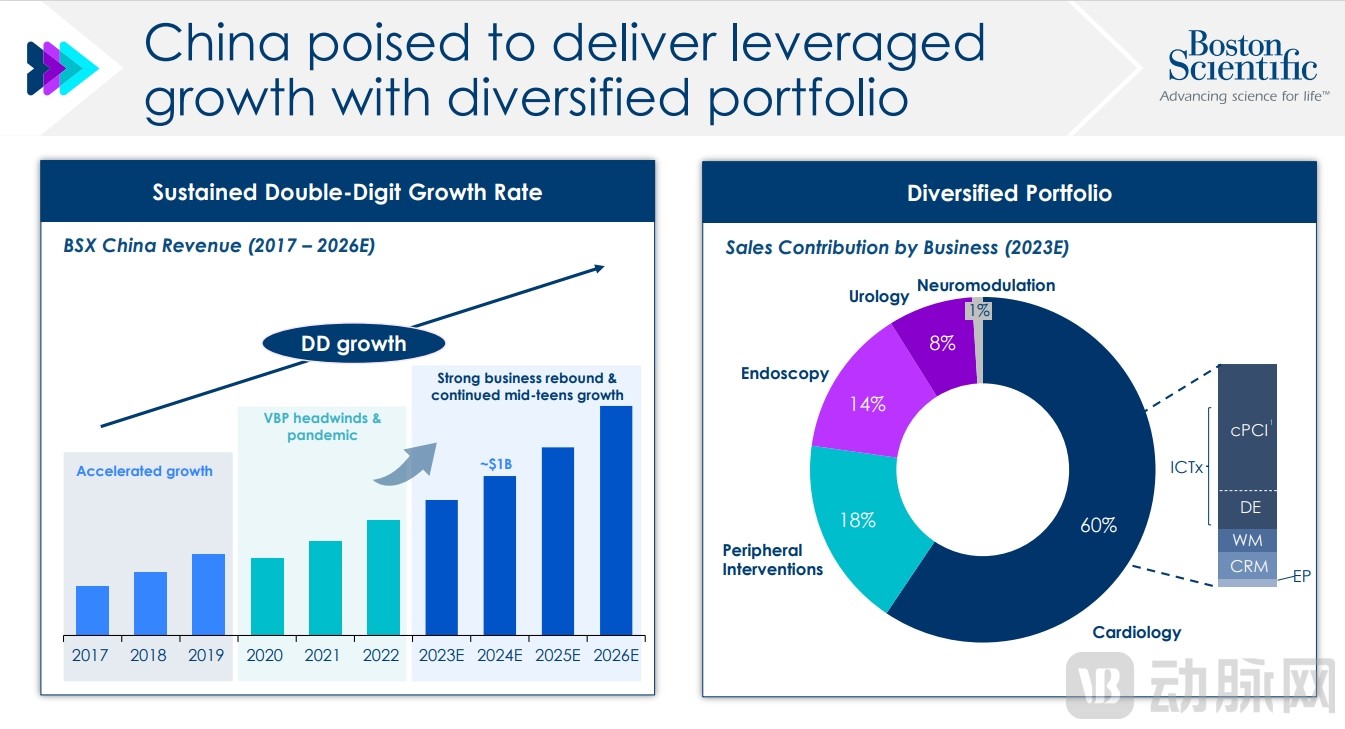

Boston Scientific Corporation elaborated on its China market strategy at the 2023 Investor Conference.

First, Boston Scientific believes that China, with its unparalleled growth, scale, and innovation ecosystem, is one of the most attractive medical technology markets.

In terms of revenue expectations, by 2024, Boston Scientific's revenue in the Chinese market will exceed 1 billion US dollars. Despite facing challenges, it is still expected to achieve double-digit growth.

Boston Scientific will leverage its strengths, avoid weaknesses, and prioritize speed, localization, and scale. It will focus on highly differentiated product technologies, continuously seek new growth points, and accelerate product launches and market penetration through agile and localized operations to maintain competitiveness.

Boston Scientific China Market Revenue Outlook and Composition Image Source:Boston Scientific 2023 Investor Day

The construction of the first factory in China this time means that Boston Scientific has realized the full-chain localization of R&D, access, investment, and production, establishing a diversified localized ecosystem and closed loop.

McKinsey also pointed out in the article that Abbott has reallocated commercial resources, reducing the number of drug-eluting stent sales personnel affected by centralized procurement, and focusing on continuous glucose monitoring products.

As MNCs increase their localization efforts, they are establishing innovation centers in China, collaborating with Chinese innovative companies, investing in Chinese startups, and building factories in China. This series of strategies has also led to the gradual domestic production of imported products.

According to the "Measures for the Administration of Government Procurement of Imported Products," imported products refer to: products that enter China through customs clearance and are produced outside of China's customs territory. Products manufactured domestically by MNC enterprises can also obtain registration certificates for medical devices in China.

For example, the da Vinci surgical robot and Boston Scientific's intravascular ultrasound have both received "Guo Xie Zhu Zhun" certification.

MNC Enterprises' Products Receive NMPA Import Registration Numbers, Indicating That These Products Are Also Categorized as Domestically Produced in Terms of Market Access and Tender Procurement — The Distinction Between Domestic and Imported Products Is Eliminated. How Will This Trend Impact the Landscape of China’s Medical Device Market?

For MNCs, they can first better consolidate their existing market advantages.Landing mature products in the Chinese market can reduce costs and increase efficiency, supply the Chinese market more quickly, and expand the market share of existing products. Especially in centralized procurement, MNCs can respond more flexibly.

On the other hand, the localization of MNC enterprises can also drive the cultivation of new markets more quickly.China's medical device industry started late, and several innovative technologies and therapies have been less applied domestically. MNCs are increasing their localization efforts, which can more quickly foster and drive growth in niche sectors, establishing a first-mover advantage in emerging markets.

MNCs with a global vision can quickly and敏锐ly perceive market changes. However, in the past, due to product approval cycles and market education cycles, it took several years to slowly cultivate the domestic market.

The Localization Strategy Provides MNCs with Multiple Approaches to Accelerate This Process, Including Collaboration with Innovative Enterprises, Green Channels for Product Approval, and Local R&D.

Taking the burgeoning field of disposable endoscopes as an example, the domestic disposable endoscope sector is still in its early stages of development, with a large number of application scenarios yet to be explored, and there is an urgent need for more mature products to be commercialized.

Globally, Boston Scientific is the leader in disposable endoscopes for the gastrointestinal tract. Directly introducing disposable endoscope products comes with high costs and long cycles. To accelerate the development of this market, Boston Scientific and SinoView plan to establish a long-term collaboration on the commercial promotion and market sales of a single-use electronic choledochoscope (percutaneous) in mainland China. By leveraging the MNC’s well-established channel network and extensive professional education programs, they aim to reach a broader market across China.

For companies in China, the increased localization efforts by MNCs also benefit the expansion of the innovation ecosystem, allowing domestic innovative enterprises to achieve broader market coverage with the help of MNCs.

From initially conducting market education in China, to accelerating the introduction of products into China, to investing in China's medical innovation technology, and then to establishing manufacturing facilities, MNCs are increasingly deepening their roots in China. The enormous healthcare demand, coupled with a well-established industrial infrastructure and an excellent business environment, is attracting MNCs to firmly develop within China.

It is worth mentioning that these multinational medical device giants are seeing not only the production capacity of the Chinese market, but also the domestic market's research and development and innovation capabilities. In the future, we can expect more achievements in the localization of MNC enterprises, helping China grow into a global advanced medical device manufacturing center.

Reference article: Most influential countries in the international medical device trade: Network-based analysis - PMC (nih.gov)

Looking at Boston Scientific's Plant Establishment in China and Its China4China Strategy —— MedTalks

Upgrading medtech commercial operations in China | McKinsey