GLP-1 Fails to Disrupt CGM Market as Sector Grows 30% YoY, Fueling Chinese Brands’ Global Expansion

Abbott

Diagnostic and pharmaceutical product manufacturers

Decans

Developer of High-Performance Orthopedic Implants and Surgical Technique Systems

With the deepening of clinical research, GLP-1 has demonstrated excellent application scenarios in multiple fields and significantly impacted niche markets such as the weight-loss market. As a result, there were once concerns in the market about whether GLP-1 might negatively affect diabetes-related segments like CGM.

Recently, Abbott announced its 2023 Q3 financial results while revising downward its annual profit guidance. Abbott's Q3 revenue reached $10.1 billion, with cumulative revenue for the first three fiscal quarters of 2023 amounting to $29.868 billion and cumulative net profit at $4.129 billion, representing year-over-year decreases of 11.01% and 30.02%, respectively.

Despite a 32% decline in Abbott's diagnostics business revenue, Abbott's CGM sales grew by 30.5% in Q3 this year, with quarterly revenue reaching $1.4 billion, marking one of the few highlights in the earnings report. As of Q3 2023, Abbott's CGM business has generated a total revenue of $3.9 billion, with over 5 million global users.

Coincidentally, another leading company focusing on CGM, Decans Medical, reported its Q3 earnings at the end of October, showing a 27% year-over-year increase in quarterly revenue, with its CGM business also experiencing rapid growth. As of 2023 Q3, Decans Medical's total revenue reached 2.588 billion USD, including a 24% growth in revenue from the United States and a 33% increase in international revenue.

In addition to the continuous support for CGM from U.S. health insurance, Abbott and Decans have both mentioned the boost that GLP-1 drugs give to CGM. At the same time, more clinical studies also support introducing several core indicators in CGM as new standards into diabetes clinical management in addition to HbA1c.

CGM is poised for an acceleration in adoption, and for domestic brands, seizing this opportunity to join the overseas expansion wave could present a significant chance for rapid growth.

Abbott and Decans successively released their respective studies confirming the positive impact of GLP-1 drugs on CGM.

The reason why both CGM industry leaders have done this is that the market once worried that the application of GLP-1 drugs would affect the development prospects of CGM. The market's concerns are not unfounded, as the launch of GLP-1 drugs has had a significant impact on many niche sectors.

In the weight loss sector, the number of bariatric surgeries performed using Intuitive Surgical's da Vinci surgical robot has declined for two consecutive quarters. Despite a 19% year-over-year increase in surgeries performed by da Vinci systems in Q3 this year, the market remains unimpressed, leading to a drop in stock price. Johnson & Johnson also stated that GLP-1 drugs have impacted bariatric surgery devices, causing related products under their portfolio to grow less than expected. Meanwhile, Allurion, a gastric balloon company invested in by Medtronic, has seen its stock price fall by more than half since going public in August.

Such a horror story did not happen to CGM.

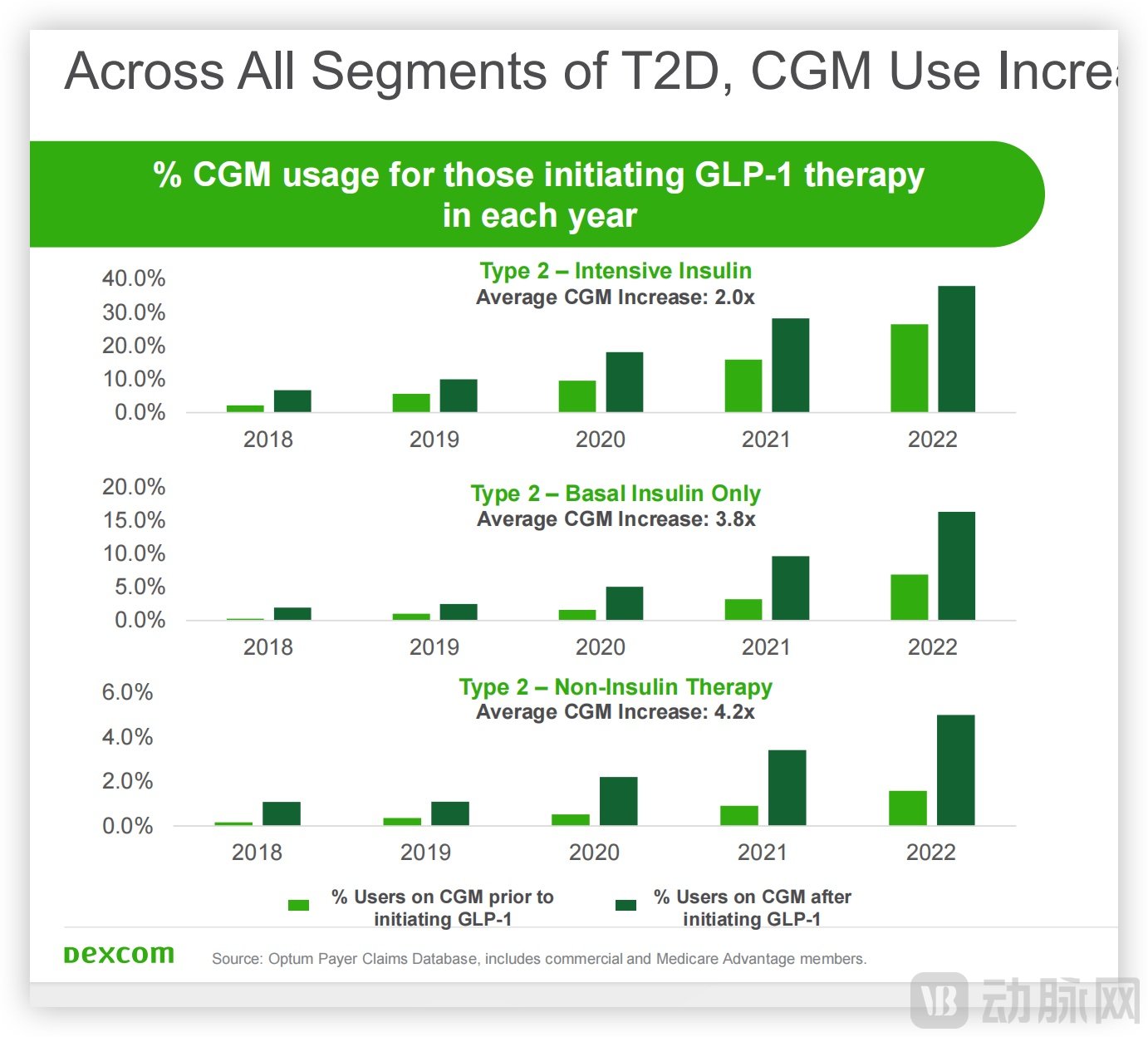

In September, Decans also announced a study based on Optum insurance at its investor conference, stating that after intensive insulin users started using GLP-1 drugs, their usage of CGM doubled compared to the past, while basal insulin users and non-insulin users saw their CGM usage increase nearly fourfold after starting GLP-1 drugs.

Decans Research on the Positive Drive Between CGM and GLP-1, Image Source: Official Website

The synergy between GLP-1 and CGM has become a new clinical driver.

Decans believes that, whether it is the support needed for long-term human metabolic health or the adjustment of short-term treatment plans, the combination of CGM + GLP-1 can help patients achieve a more lasting state of health, with both presenting a mutually reinforcing positive effect.

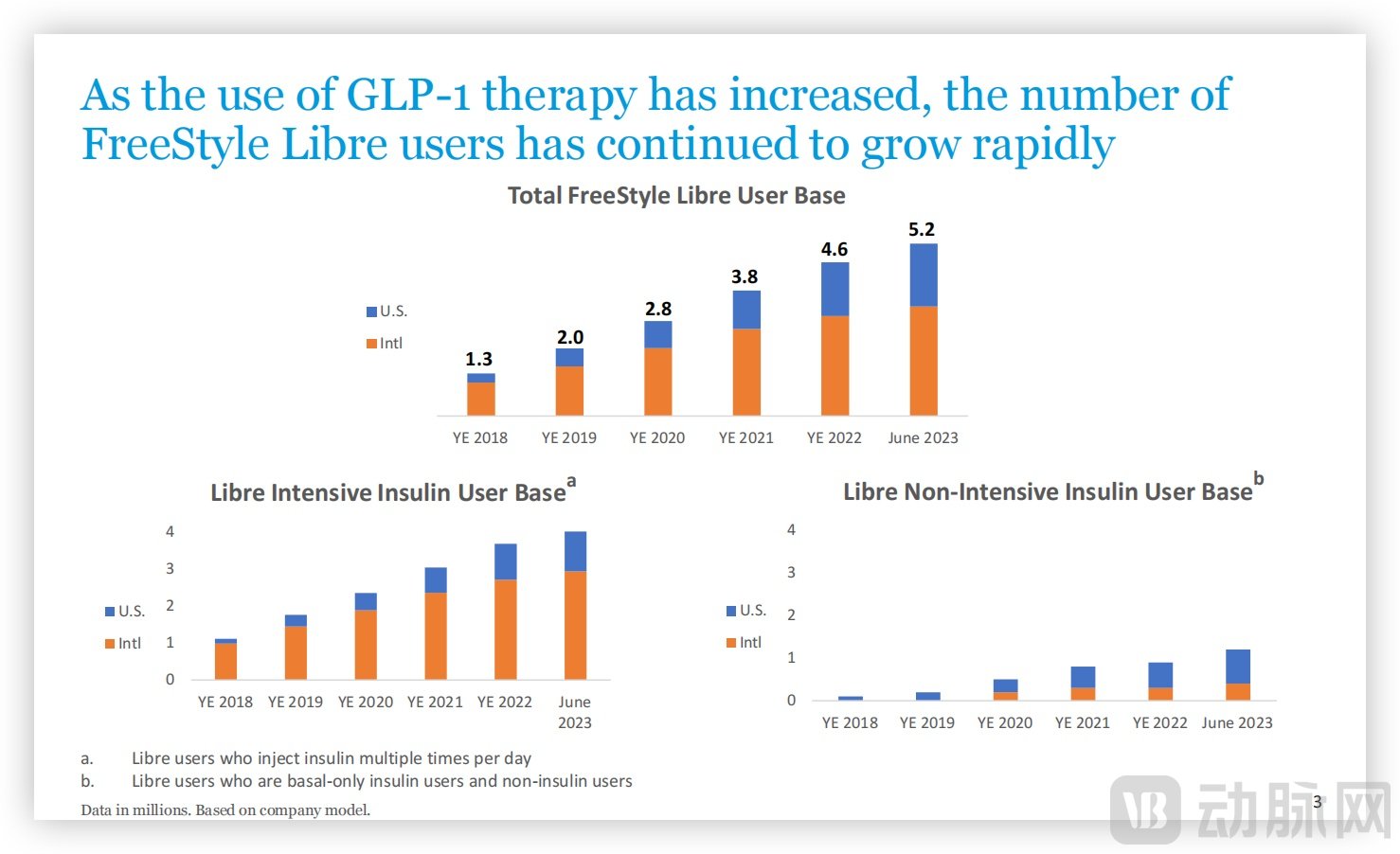

Despite Decans' study shedding light on the relationship between GLP-1 and CGM, its small sample size has left some doubts in the market. Shortly after, Abbott released its insurance reimbursement data based on the U.S. retail pharmacy channel, covering mainstream Medicare insurance in the U.S., including nearly 300 million users, of which about two-thirds are Abbott CGM product users, providing a sufficiently large sample size.

Abbott also believes that GLP-1 and CGM are mutually reinforcing, image source: official website

From the data published by Abbott, whether in the U.S. market or the international market, with the increase in GLP-1 drug market penetration, the number of CGM users is also growing rapidly. The two have not formed an either-or situation but instead are rising together. In addition, Abbott has calculated the proportion of its Freestyle Libre users who take GLP-1 drugs, showing that the percentage of GLP-1 drug usage among Abbott's CGM user base is also gradually increasing.

Notably, the group adopting both GLP-1 drugs and CGM demonstrates higher treatment adherence. Therefore, Abbott concluded that the relationship between CGM and GLP-1 is more mutually reinforcing rather than competitive.

Not only Decans and Abbott, but another diabetes giant Insulet has also conducted similar research, reaching a similar conclusion.

The research from industry giants, along with the supporting evidence of their own performance, has dispelled the gloom that once hung over the CGM track. In the future, as the application scope of GLP-1 expands, it will also drive CGM to embrace new growth.

An increasing number of clinical studies have confirmed that CGM will play an equally important role as HbA1c in the future of diabetes management.

At the recently concluded 59th Annual Meeting of the European Association for the Study of Diabetes (EASD), experts from multiple countries delivered numerous reports and shared insights on diabetes, with Continuous Glucose Monitoring (CGM) being one of the key topics. In the past, CGM was generally considered an advanced alternative to traditional fingerstick blood glucose monitoring. However, the presentations at this conference highlighted the significant value of CGM in providing additional metrics beyond glycated hemoglobin (HbA1c) as new standards for glucose management. Furthermore, several experts shared the clinical advantages of CGM from various perspectives.

CGM can provide new blood glucose management parameters beyond HbA1c.

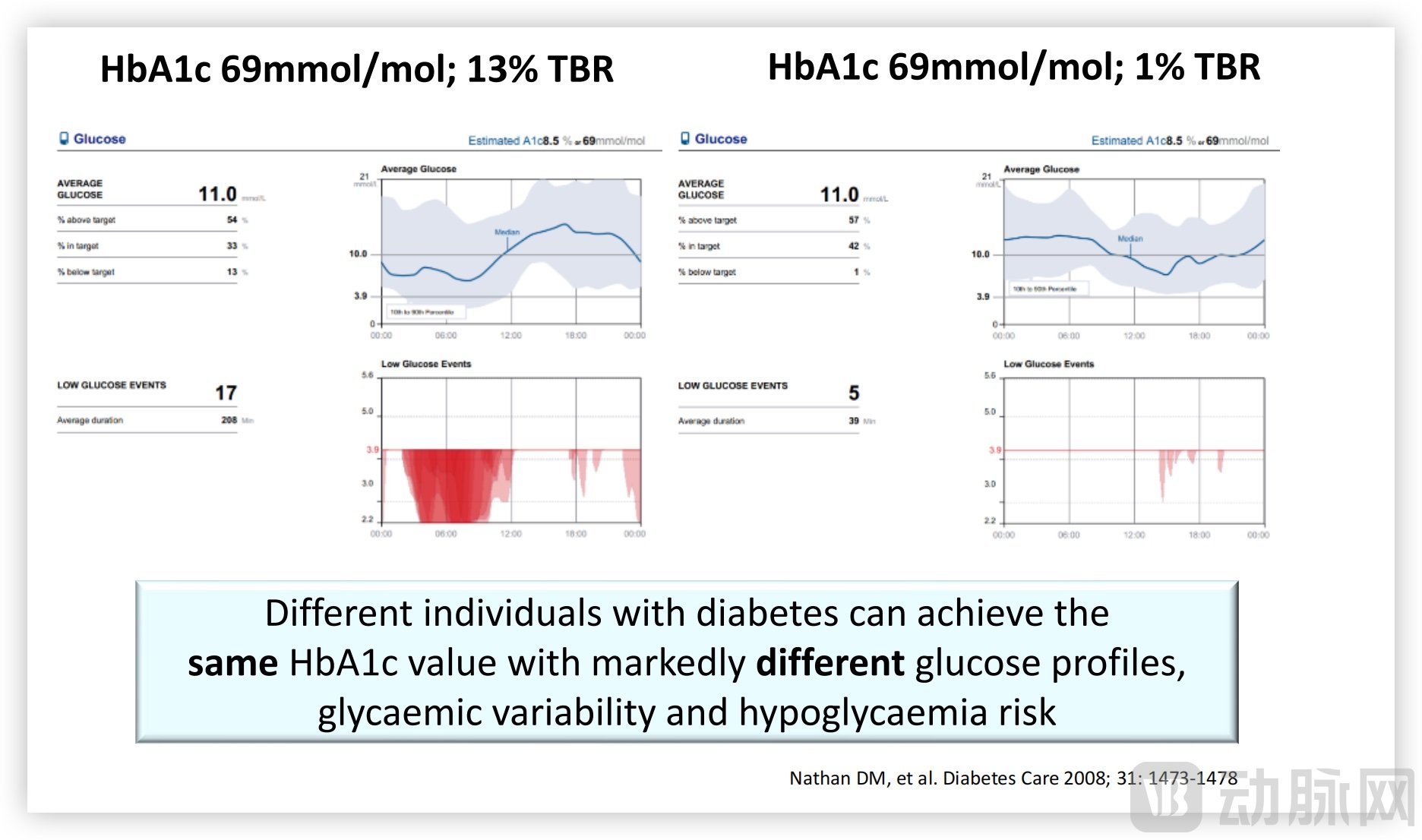

Professor Emma Wilmot from the University of Nottingham pointed out that although HbA1c is positively correlated with microvascular complications and serves as a useful indicator for assessing the risk of diabetic complications, having been widely used in clinical practice in the past, there are significant differences among different diabetic patients in their blood glucose profiles, glycemic variability, and hypoglycemia risks even at the same HbA1c levels. HbA1c mainly reflects average blood glucose levels over a period of time rather than real-time blood glucose concentration, making it a relatively rough measure. It cannot reflect current blood glucose levels in real-time, nor can it show trends in blood glucose fluctuations, warnings for high or low blood sugar, or specific recommendations for blood sugar control.

Same HbA1c Value, Different Blood Glucose States; Image Source: EASD

The Time in Range (TIR) and Ambulatory Glucose Profile (AGP) provided by Continuous Glucose Monitoring (CGM) can be introduced as important parameters for glycemic adjustment in diabetes management. They effectively enhance hypoglycemic treatment and risk warnings, while also beginning to transform traditional diagnostic and treatment models. In the past, doctors assessed HbA1c levels and provided adjustment plans, which patients passively followed; now, patients inform doctors of their TIR results and propose adjustment ideas based on their lifestyle, after which doctors evaluate and provide guidance.

Diabetes management is a complex project that requires the integration of clinical outcomes and life experiences. If HbA1c represents clinical outcomes, then CGM can provide life experiences, and only by combining the two can balance be achieved.

Report from Professor Richard M. Bergenstal of the University of Minnesota also suggests the need to incorporate CGM alongside HbA1c to enhance the quality of diabetes management. Professor Bergenstal believes that effective diabetes management relies on the following: 1. Minimizing occurrences of hyperglycemia; 2. Avoiding risks of hypoglycemia; 3. Reducing the risk of vascular complications; 4. A reasonable lifestyle plan.

In the past, HbA1c has been used as the diagnostic standard in clinical practice. However, years of epidemiological investigations have found that the proportion of hyperglycemia and hypoglycemia among patients with type 1 and type 2 diabetes continues to rise, making the HbA1c metric far from sufficient for achieving high-quality diabetes management. From real-world cases, the introduction of CGM not only helps patients control blood glucose but also addresses weight issues, adjusts lifestyles, alleviates diabetes-related emotional problems, and optimizes medication treatment plans.

Taking the Glucose Management Indicator (GMI) in CGM as an example, in a study involving over 1,440 patients, GMI and HbA1c showed similar distributions and correlations in the continuous progression of retinopathy. As one of the core indicators of CGM, GMI can play a significant supporting role in clinical blood glucose management.

GMI can assess a patient's short-term blood glucose control and promptly provide guidance for lifestyle adjustments. Previous studies have shown that 14 days of CGM data is sufficient to predict the trend of blood glucose changes over the next three months, meaning the GMI index can demonstrate greater value in medium- to long-term blood glucose management. With the introduction of new parameters such as GMI, TIR/TBR, patients can benefit from more refined diabetes management plans.

In addition, experts have also conducted research on the reduction of hospitalization rates for type 1 and type 2 diabetes patients using CGM, as well as the association between the key CGM parameter TIR and cognitive dysfunction and hippocampal damage in adult patients with type 2 diabetes. Multiple clinical studies have shown that in the future, CGM will not only be used for checking blood glucose levels but will also play a greater clinical role.

Europe is becoming the next fiercely competitive market for giants.

In the Q3 financial report, both Abbott and Decans believe that the European market will be the focus of future efforts. Currently, the growth rate of CGM in the European market remains at 18%~20%, mainly driven by the increase in penetration among type 2 diabetes patients. In 2023, major European countries, including the UK, Germany, and France, are expected to include CGM in the reimbursable medical insurance coverage for type 2 diabetes patients.

The development and popularization of CGM in Europe, like the U.S. market, cannot be separated from insurance support. The threshold price for CGM reimbursement in the U.S. market has increased from $166 in 2016 to $226 this year, with the excess covered by insurance (out-of-pocket costs account for about 20%). At the same time, the scope of insurance coverage has been expanded to include more patient groups. The underlying logic is that insurance encourages patients to continue using CGM to help control their conditions and reduce complications, thereby reducing overall healthcare expenditures.

Abbott actively promotes multiple real-world studies on CGM being conducted in Europe. For instance, a retrospective study of the French National Claims Database showed that type 2 diabetes patients using insulin once daily experienced a significant reduction in acute diabetes complications after using CGM, with hospitalizations decreasing by 67%.

Thanks to the support from clinical research, in June this year, France announced the approval to expand the reimbursement scope of CGM. Previously limited to type 1 and type 2 diabetes patients requiring intensive insulin therapy, it will now be extended to all diabetes patients using basal insulin. This is expected to add about 3 million patients who will use CGM, with both Abbott and Decans set to benefit. France has become the first European country to expand CGM insurance coverage, and this wave of expansion may continue.

Not only Abbott, but Decans has also been making frequent moves in Europe. After the new generation G7 obtained European CE certification last year, Decans was prepared to compete with Abbott. At the beginning of this year, Decans announced that it would invest 300 million euros to establish its first production base in Europe in Ireland, with an expected annual output of millions to meet the rapidly growing market demand in Europe.

Although Europe has basically implemented universal health care, the health care funds of various countries are relatively tight after the epidemic. Therefore, there is a rigid demand for CGM products with higher cost performance.

From the product perspective, Abbott's Freestyle Libre 3 and Decans' G7 have similar functions with minor differences. However, one Libre 3 has a usage cycle of 14 days, while the G7 cycle is 10 days, making Abbott’s daily cost cheaper. Taking the German market prices as an example, the annual cost for Abbott is approximately 1250 euros, while Decans’ annual price is about 1650 euros.

At present, the European market is still dominated by Abbott and Decans. Medtronic's new generation CGM Simplera has just received certification, and it will take time to enter the market and participate in the competition.

Such a competitive landscape is a familiar script for domestically-produced CGM that have emerged from the encirclement of Abbott and Medtronic in the Chinese market. Participating in the competition in the European market will also be a challenge faced by the development of the domestically-produced CGM industry.

The domestic market in China is becoming increasingly competitive, and domestically produced CGMs need a second growth curve.

During the Double Eleven period, two newly approved CGM companies this year, Sinocare and Yuwell Medical, launched aggressive promotions for their CGM products, lowering the unit price of CGM to the 100-200 RMB range. In the Tmall V-list for blood glucose products, the two companies ranked at the top. Two years ago, the domestic CGM product prices were generally in the 400-600 RMB range. Two years later, CGM has entered the "rock-bottom price" range.

Although the Double Eleven promotion is only a short-term activity, it reflects a trend - the CGM market in China is starting to become highly competitive.

An insider in the CGM industry told VCBeat: "The raw material cost of CGM is not high. The yield rate determines the cost. Although different technical routes lead to different processes, making it difficult to conduct a unified evaluation, reaching a price point of over 100 is close to the bottom line."

As Chinese companies continuously update their technologies, the number of domestically produced products on the market has gradually increased and their quality has reached mainstream standards after breaking through the barriers set by Abbott and Medtronic. For instance, the service life of sensors generally reaches 14 days, while Sinocare and Meqi Medical have even extended it to 15 days. The Mean Absolute Relative Difference (MARD), which measures testing accuracy, has also been decreasing, with SinoBio reaching 8.83% and Sinocare achieving an impressive 8.71%. Compared with earlier products, the newly launched CGM products offer a better user experience, enhancing patients' willingness to purchase.

Competing on products and then on prices is ultimately not a long-term strategy, as China-produced CGMs begin to target overseas markets.

The three newly approved domestic CGM enterprises, Sibase Bioelectronics, Sinocare, and Yuwell Medical, have all announced their expansion into Europe. Both Sinocare and Sibase Bioelectronics' CGM systems have obtained conformity certificates based on the EU Medical Device Regulation (REGULATION (EU) 2017/745, abbreviated as MDR). This means that their products have gained access qualifications to enter the European market. Meanwhile, Yuwell Medical also stated that its new generation of CGM products is currently undergoing MDR certification.

To achieve success in the European market, domestically produced CGMs need to meet the needs of insurers, doctors, and patients.

For insurance, the lowest cost paid when obtaining similar products is their primary demand. For doctors, they are willing to recommend a product to users only after understanding it, managing patients who have used it, or being exposed to it during academic activities; at the same time, the product needs to be covered by different types of insurance. For patients, key factors for accepting a product include doctor recommendations, inclusion in insurance reimbursement, and affordable out-of-pocket expenses.

Therefore, at the 2023 EASD Annual Meeting, we saw the presence of Yuwell and Sinocare, actively participating in international conferences to build their brand influence.

For overseas markets, leveraging the shoulders of giants to cross the river is a reasonable tactic. For instance, Decans Medical entered the German market in 2016, initially adopting a distributor model, which did not yield good results. Later, the establishment of a direct sales team led to improved performance—Abbott followed a similar approach. Currently, the German market accounts for approximately 30% to 40% of Abbott's European sales and about 10% of Decans' European sales.

With the example set by industry giants, China-produced CGM enterprises have also made early arrangements.

As early as 2016, Sinocare made an international layout in the diabetes field through the acquisition of THI and PTS in the United States. In recent years, it has continued to promote the construction of localized market teams in Asia, Africa, and Latin America, establishing multiple subsidiaries. In the future, Sinocare will rely on the global sales and service network system established by PTS, THI, and Sinocare, leverage domestic production advantages, increase the promotion of CGM overseas, and serve more patients with diabetes.

Yuwell Medical has also made strategic moves in Europe over the past few years. Whether it’s through Germany's Primedic or Italy's MIR Medical, their channels and teams have laid a solid market foundation for Yuwell's future growth in Europe.

In the European market, the high standards set by Abbott and Decans make it challenging for newcomers. In terms of products, a MARD value below 9% and being calibration-free are required to gain the trust of doctors; in terms of price, it is difficult to win the favor of insurance companies unless it is more than 20% lower than existing products.

It is foreseeable that the domestically produced CGM, which has struggled to break through in the domestic market, is not afraid of such competition. Whether it is the boost from GLP-1 or the expansion of usage scenarios through clinical research, both have had a positive impact on the market. Seizing this opportunity for rapid development, the timing is perfect for domestically produced CGM to expand overseas.

References:

Riddlesworth TD, Beck RW, Gal RL, et al. Optimal Sampling Duration for Continuous Glucose Monitoring to Determine Long-Term Glycemic Control. Diabetes Technol Ther. 2018 Apr;20(4):314-316.

Nathanson D, et al. SO 67-821. EASD Annual Meeting 2023.

Eeg-Olofsson K, et al. SO 67-818. EASD Annual Meeting 2023.