How global biotechs like IDEAYA are boosting stocks by 90% with Chinese key assets

IDEAYA Biosciences

Targeted Therapy Drug Developer

On September 8, U.S. biotech company IDEAYA Biosciences held an R&D Day event celebrating its tenth anniversary, comprehensively showcasing its R&D pipeline, clinical progress, strategic vision, and technology platforms.

The event featured seven presentation topics, two of which focused on ADC assets from China (IDE849 licensed from Hengrui Pharma and IDE034 licensed from Biocytogen). IDEAYA highlighted the "small molecule + ADC" combination therapy as a differentiated strategic direction, with projects from Hengrui and Biocytogen serving as clinical anchors for this approach. The company anticipates that these collaborations will yield at least three new IND/Phase II cohorts within the next 12 months, positioning them as key drivers for IDEAYA's "second growth curve."

IDEAYA's Pipeline In-Licensed from China, Source: IDEAYA Website

IDEAYA's Pipeline In-Licensed from China, Source: IDEAYA Website

Among IDEAYA's 10 R&D pipelines, transactions have been disclosed for seven. As of September 26, driven by ongoing partnerships and positive clinical data, the company's stock price has risen from its 2019 IPO price of $14 per share to $26.83—a gain of approximately 92%—giving it a market capitalization of $2.351 billion. Notably, pipelines developed with Chinese partners have attracted significant attention. After IDEAYA released Phase I clinical trial data for IDE849 (SHR-4849) in small cell lung cancer, its stock price surged by up to 10% in pre-market trading on September 8.

Meanwhile, the smooth progress in clinical trials and rising stock price has allowed this clinical-stage biotech to spend its way into a stronger financial position. After concluding deals with Biocytogen and Hengrui Pharma for $406.5 million and $1.045 billion in November and December 2024, respectively, IDEAYA had an estimated cash balance of approximately $1.2 billion as of September 8, 2025, which is expected to fund its R&D investments for the foreseeable future.

IDEAYA's case is not unique. Over the past year, a growing list of overseas biotech companies—including Aadi, Aclaris, Alumis, ArriVent, BioNTech, Duality, Rapt, Instil, and Summit—have seen positive secondary market feedback by in-licensing high-quality novel drug assets from China, helping some to stage a turnaround.

Clearly, we have entered an era where Chinese novel drug pipelines are being woven into the core growth narratives of global pharmaceutical companies.

Hengrui's ADC Data Lifts IDEAYA's Pre-Market Stock by 10%

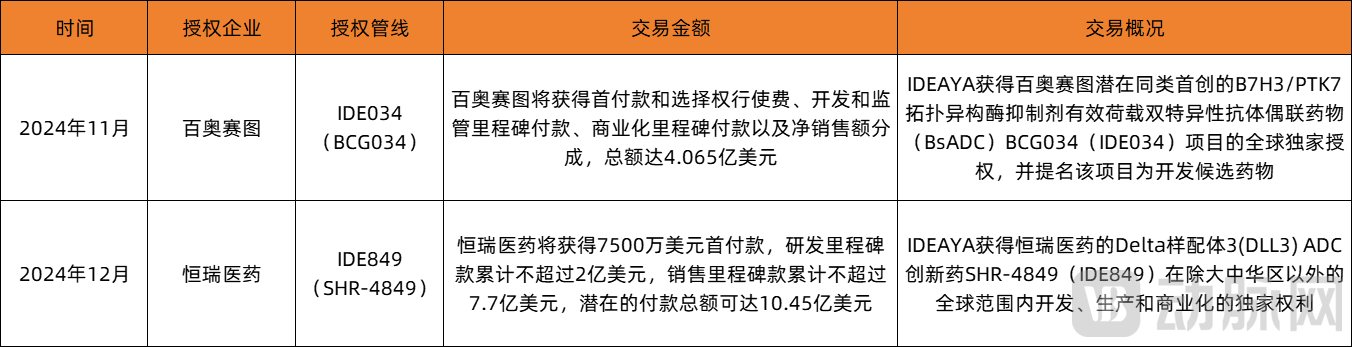

In the R&D Day materials released by IDEAYA, the documentation on drug progress spans 56 pages, with 12 pages dedicated solely to IDE849 (SHR-4849), which was in-licensed from Hengrui.

IDEAYA acquired this asset on December 29, 2024, in a deal valued at up to $1.045 billion ($75 million upfront, up to $200 million in development milestones, and up to $770 million in commercial milestones). IDEAYA holds exclusive global rights for the development, manufacturing, and commercialization of IDE849 outside Greater China. IDE849 is an innovative DLL3-targeting ADC originally developed by Hengrui.

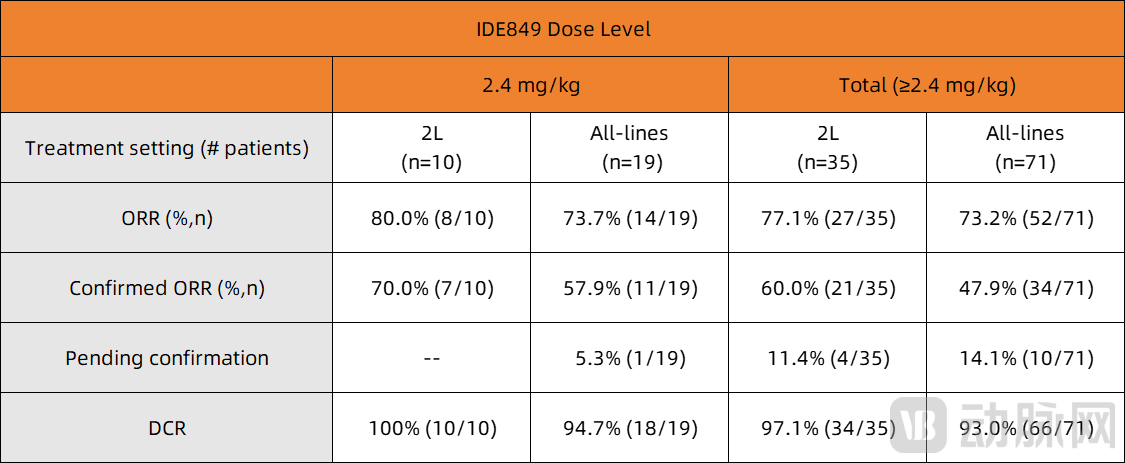

IDE849 not only featured prominently in IDEAYA's R&D Day activities, but just one day earlier, on September 7, the company issued a press release highlighting updated Phase 1 clinical trial data for IDE849 in relapsed small cell lung cancer presented at the IASLC 2025 World Conference on Lung Cancer (WCLC). The report included data from 100 patients who received IDE849 at doses ranging from 0.8 mg/kg to 4.2 mg/kg administered once every three weeks.

IDE849 Clinical Data, Source: IDEAYA Website

IDE849 Clinical Data, Source: IDEAYA Website

In terms of efficacy, IDE849 demonstrated promising antitumor activity in SCLC patients at dose levels ≥2.4 mg/kg. In the efficacy-evaluable population (n=71), the objective response rate (ORR) was 73.2% and the disease control rate (DCR) reached 93.0%. Among the second-line treatment population (n=35), the ORR was 77.1% with a DCR of 97.1%. In patients with baseline brain metastases (n=18), the ORR was approximately 80.0% and the DCR achieved 100%.

Furthermore, in the overall treated population at doses ≥2.4 mg/kg (n=86), the median progression-free survival (PFS) was 6.7 months, with a 6-month PFS rate of 55.3%. For the second-line treatment population (n=42), the median PFS was not yet reached, and the 6-month PFS rate stood at 59%.

Regarding safety, across all patients and all dose levels (n=100), Grade 3 or higher (Gr≥3) treatment-related adverse events (TRAEs) occurred in 48% (48/100) of patients, and serious TRAEs were observed in 16% (16/100). The most common TRAEs included leukopenia, neutropenia, anemia, and nausea. The TRAE-induced dose adjustment rate was 15%, while the treatment-related discontinuation rate was only 2%. No treatment-related deaths were reported.

Overall, IDE849 demonstrated a tolerable and manageable safety profile in patients with relapsed small cell lung cancer. Furthermore, IDE849 exhibited promising antitumor activity at dose levels ≥2.4 mg/kg, showing particularly encouraging efficacy in the second-line treatment population.

Currently, no DLL3-targeting ADC product has been approved for marketing globally. Leonid Timashev, an analyst at RBC Capital, noted that the ORR of publicly disclosed competing candidates generally ranges from 30% to 50%, so an ORR exceeding 70% is considered a "home run." IDE849 has the potential to become a best-in-class therapy. If its efficacy in second-line SCLC is confirmed in subsequent studies, the drug could achieve blockbuster status with peak sales potentially reaching $1 billion.

Boosted by the Phase I clinical trial data for IDE849, IDEAYA's stock price rose by up to 10% during pre-market trading on September 8. This pattern shows that by licensing novel drug assets from China, overseas biotech companies can not only secure promising pipeline candidates at a relatively low cost but also leverage subsequent positive clinical data to boost investor confidence in the secondary market, providing multi-faceted support for R&D-stage companies.

Global Biotechs Revive by Leveraging Chinese Pipelines

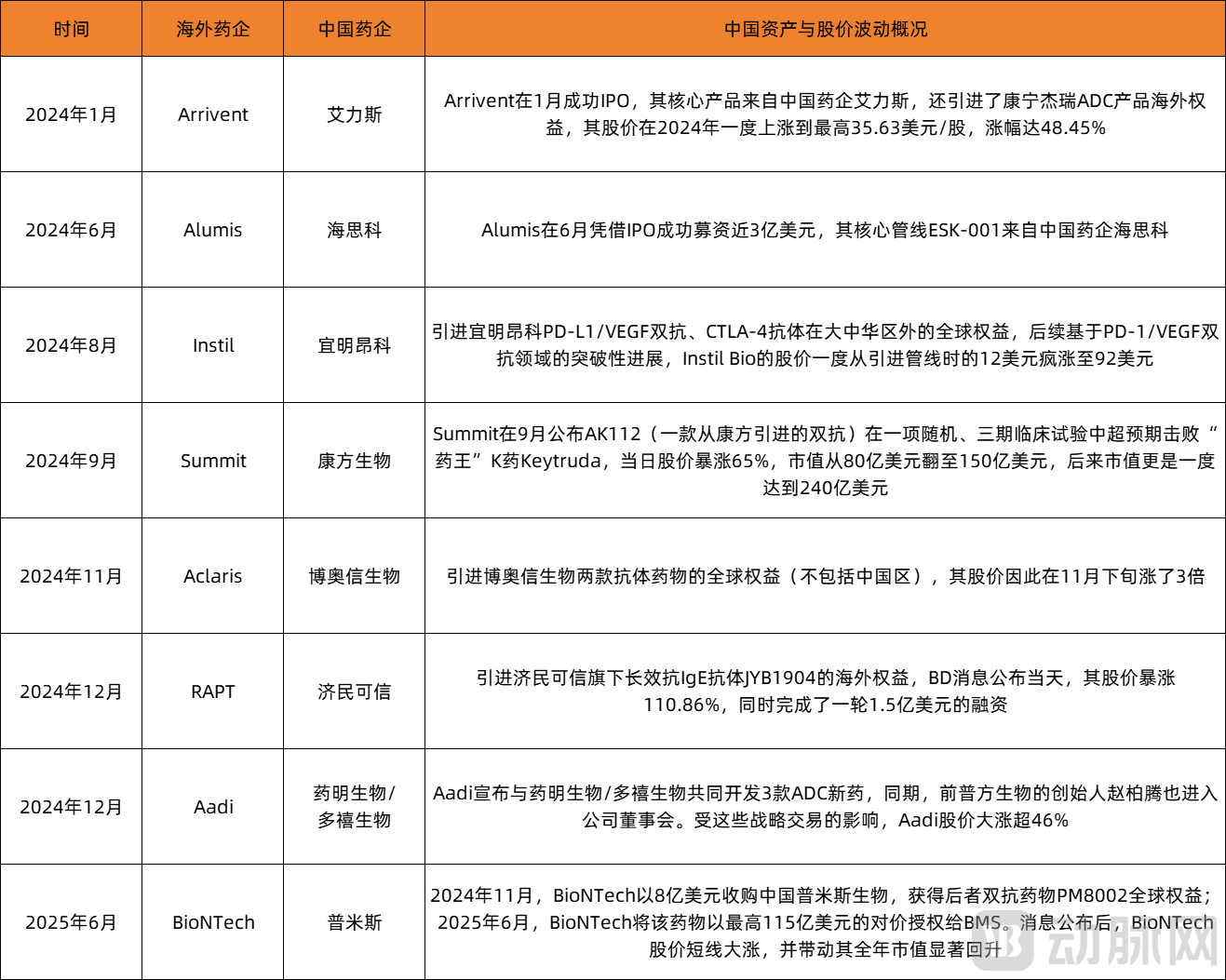

IDEAYA's story is a microcosm of a broader trend. According to incomplete statistics from VCBeat, since 2024, a growing list of global biotechs—including Aadi, Aclaris, Alumis, ArriVent, BioNTech, Duality, Rapt Therapeutics, Instil, and Summit—have achieved positive feedback in the secondary market by in-licensing high-quality novel drug assets from China, with some even turning their fortunes around.

Global Pharmaceutical Companies with Significant Stock Price Movements Tied to Chinese Pipelines

On one hand, well-funded overseas pharmaceutical companies with ample resources are increasingly casting a wide net in China, seeking innovative drug pipelines. While not all licensed assets will reach the market, the success of just one pipeline can deliver substantial returns for years.

Consider BioNTech, which held €15.9 billion in cash, cash equivalents, and security investments as of March 31, 2025. According to incomplete statistics, in recent years, BioNTech has entered into multiple licensing collaborations of various types with several Chinese biopharmaceutical companies, including AcroImmune Group, Duality Bio, Doer Bio, Biotheus, Medilink Therapeutics, Huadong Medicine, and Triastek. Many of these collaborations involve deal values exceeding $1 billion.

According to Insight Database, in the 2023 ranking of global companies by the number of in-licensed Chinese assets, BioNTech secured the second position, immediately following AstraZeneca. Notably, it ranked ahead of industry leaders such as GSK, Pfizer, and Takeda.

While BioNTech has spent substantially on its "shopping spree" in China, its subsequent resale of a Chinese biotech asset successfully exemplified the strategy of "securing substantial returns from a single deal." In a notable example, BioNTech acquired Biotheus for $800 million in November 2024, then licensed the core assets to Bristol Myers Squibb (BMS) six months later in a deal valued at over $9 billion—a return exceeding tenfold on its initial investment.

On the other hand, some overseas pharmaceutical companies facing operational challenges have relied on their teams' sharp vision and strategic judgment to acquire lifeline assets from China at favorable prices, successfully turning their fortunes around.

A prime example is Summit Therapeutics, which was once on the brink of delisting. Since its Nasdaq listing in 2015, Summit's stock price typically hovered around $5 per share. However, just before licensing Akeso's AK112, its share price had fallen to below $1. By 2022, Summit's market capitalization was just $158 million, with a cash balance of only $120 million. Under significant pressure and with financial backing from its founder, Robert W. Duggan, Summit acquired the rights to Akeso's PD-1/bispecific antibody AK112 for the U.S., Canada, Europe, and Japan. The deal involved a $50 million upfront payment and a total potential transaction value of up to $5 billion.

In September 2024, after data showed that AK112 had exceeded expectations by outperforming Keytruda in a randomized Phase III clinical trial, Summit's stock price surged 65% in a single day, propelling its market capitalization from $8 billion to $15 billion. Throughout 2024, the company's share price soared from under $3 per share at the beginning of the year to an annual high of $33.6 per share, representing a peak annual gain of 1,020%.

By achieving this dramatic valuation leap on the strength of AK112's head-to-head victory, Summit has become a emblematic case of a pharmaceutical company achieving extraordinary value through a Chinese-licensed asset.

It is evident that for strategic players like BioNTech, Chinese assets serve as high-probability "real options." They initially invest $20 million to $200 million per project in upfront payments while accumulating a portfolio of over a dozen pipelines. The success of just one or two assets enables them to rapidly recoup the entire portfolio's cost through out-licensing or co-commercialization deals, while the risks of failed projects are diluted across the portfolio—a controlled-risk model with high upside.

In contrast, for financially distressed "turnaround" biotechs, they stake their entire remaining survival on a single high-potential Chinese pipeline to achieve a dramatic reversal. Summit, as a textbook case, leveraged one Chinese asset to achieve a hundredfold valuation increase, seized the momentum to raise $235 million in a follow-on offering, and launched multiple global Phase III trials—effectively transforming a "single-drug rescue" into a platform strategy emulating Keytruda's success.

While the two strategies appear distinct, they share a common underlying logic: regardless of the path taken, the "low cost, high upside, and rapid clinical advancement" offered by innovative Chinese drugs have been indispensable core factors behind these companies' success. In recent years, Chinese pipelines have become critical assets for certain pharmaceutical companies seeking a "turnaround"—even serving as cornerstone assets for IPOs, financing, or corporate survival. Naturally, such transactions have, in turn, accelerated the valuation recalibration and international recognition of China's novel drug assets.

Two Atypical Models for Biotech Recovery

Today, the revitalization strategies of global biotechs have evolved into multidimensional, cross-market combinations of capital and pipeline operations. Beyond traditional financing, IPO/SPAC listings, and proprietary commercialization, the most significant incremental pathway for global biotechs in recent years lies in the "leveraged operation" of Chinese clinical assets, which can be broadly categorized into two types:

The first is clinical data-driven valuation uplift. Global pharmaceutical companies first secure an early-stage innovative Chinese asset—such as at the preclinical, Phase I, or Phase II stage—with an upfront payment of tens of millions of U.S. dollars. They then leverage high-enrollment clinical trial centers in Europe and the U.S. to rapidly complete proof-of-concept or registrational Phase III validation. When data from international multicenter trials read out—particularly showing superiority over standard-of-care in a head-to-head comparison—the company’s stock price often surges severalfold intraday. This allows the firm to pass the financing inflection point without equity dilution, and subsequent milestone payments can be funded through follow-on offerings or convertible bonds at more favorable terms. Companies like Summit and Aclaris leveraged impressive data from Chinese bispecific/ADC assets to achieve single-day stock price surges, dramatically boosting market valuations that were once on the brink of delisting.

The second pathway is secondary asset arbitrage, which can be further divided into two subtypes. The first involves securing global rights to a Chinese drug candidate with relatively low upfront and milestone payments, then swiftly re-licensing the asset or forming a joint venture with a multinational corporation (MNC) to achieve a high-multiple cash return within a short cycle. A representative case, as mentioned earlier, is the transaction between BioNTech and Biotheus. The second subtype follows an "IPO + partial asset sale" model. A prime example is Alumis, which leveraged Haisco's TYK2 inhibitor as a core asset to complete its Nasdaq listing, while simultaneously divesting partial rights to the program, raising nearly $300 million in total.

These two atypical recapitalization models enable biotechs—previously constrained by traditional financing and IPO channels—to leverage minimal cash investments for substantial returns. Chinese innovative assets are now evolving from a "R&D support role" into the central pillar of a "non-dilutive recapitalization mechanism" for global biotechs.

In conclusion

Regarding the out-licensing of Chinese innovative assets, concerns have emerged within the industry: Does the large-scale acquisition of these assets by global pharmaceutical companies at relatively low prices represent an exploitation of early-stage potential?

Not at all. This model represents a strategic global division of labor within the pharmaceutical industry that creates mutual benefits. The Chinese side contributes high-potential drug candidates and cost advantages, while international partners provide regulatory expertise, capital resources, and commercial capabilities. By working together to expand the market, both parties share the incremental value generated according to market principles. Therefore, focusing solely on the immediate transaction value overlooks the significant co-created value that emerges from the ongoing collaboration.

The more pragmatic challenge facing Chinese innovative biopharmaceutical companies today lies not in an inability to develop promising molecules, but in a lack of "end-to-end value realization capability." The journey of a novel drug from preclinical stages to market approval requires navigating multiple critical phases—including development, regulatory submission, and market access—each demanding specialized teams and global resources.

When BioNTech acquired Biotheus, it integrated the latter into its own global R&D system, essentially complementing the critical gap in clinical development capabilities. Similarly, when Hengrui Pharma out-licensed SHR-1905 to Aiolos, it accelerated the establishment of an international business development team to advance its global strategy—recognizing that only by mastering the full-chain capability from molecular design to global commercialization can a company break free from the cycle of low-value out-licensing.

Therefore, the globalization of China's innovative drugs requires not a defensive and restrictive stance, but an open strategy to integrate into the global innovation ecosystem. Each transaction that may appear unfavorable in the short term is, in fact, accumulating leverage for a future revolution in pricing power.