Cloudbreak Pharma Files for IPO as Ophthalmology Sector Gains Momentum

Cloudbreak Pharma

Ophthalmic New Drug Developer

Another Ophthalmology Company Begins Its IPO Push!

Recently, following the IPOs of Chaoju Eye, He's Eye, Pure & Real Eye, Huaxia Eye, and Gaoshi Medical,Cloudbreak Pharma Submits IPO Prospectus, Aiming to List on Hong Kong Main Board, becoming a new footnote to the高潮 of the ophthalmology industry's listing spree over the past two years.

At this point, the leading companies in each segment of China's ophthalmology industry chain, from ophthalmic services to ophthalmic devices and then to ophthalmic pharmaceuticals, have either prepared or completed their IPO moves., once again proving the high prosperity of the ophthalmology industry.

The primary market remains equally heated. Against the backdrop of the current venture capital environment cooling down, a number of well-known ophthalmic innovation companies, including Micro-vision Medical, Zhongyin Technology, Century Kaitai, Intalight Saiwei, Shengyuan Pharmaceutical, Biyang Pharmaceutical, Disi Medical, Ruitai Biotechnology, Jiashinode, and Dianjing Biotechnology, have completed new rounds of financing this year.

Returning to Cloudbreak Pharma itself, it has gained considerable favor from VC/PE since its establishment and has now received investments from well-known institutions such as CDH Investments, CCB International, Gaoce Capital, Grand Pharmaceutical, De Capital, Huayi Capital, Yicun Capital, Bank of China International, Yingke Capital, Edge Capital, Guanzi Capital, Oriental Fortune Capital, and Xingzheng Capital.

This is related to its R&D progress and achievements. The prospectus shows,Cloudbreak Pharma has established a pipeline consisting of seven drug candidates, covering major diseases of the anterior and posterior segments of the eye., including four clinical-stage drug candidates (namely, CBT-001, CBT-009, CBT-006, and CBT-004) and three preclinical-stage drug candidates (namely, CBT-007, CBT-145, and CBT-011).

It is worth noting that once approved, CBT-001, CBT-004, and CBT-006 are expected to be the world's first-in-class drugs for treating pterygium, vascularized pinguecula, and meibomian gland dysfunction-related dry eye disease, respectively, indicating a huge market potential.

There is no doubt that, in the current booming ophthalmology industry, Cloudbreak Pharma's filing has added more fuel to the market.

The story of Cloudbreak Pharma begins in 2015.

At that time, Ni Jinsong, an alumnus of Nanjing University who had previously worked at the American Health Foundation, Pfizer, and Allergan, already had about 20 years of experience in pharmaceutical research and development. He judged that,The ophthalmology market is bound to be a large one in the future, where ophthalmic drugs present a global market opportunity, and innovative companies can achieve rapid growth.

Thus, Ni Jinsong decided to start his own business. After leaving a large company, he founded Cloudbreak Pharma in California, USA, and attracted partners who had previously worked for leading ophthalmic companies such as Allergan to join him.

In terms of direction selection,Cloudbreak Pharma primarily focuses on developing novel and differentiated therapies in the ophthalmology sector., by adopting multiple R&D approaches, to discover and develop novel and effective ophthalmic drugs in a more predictable and sustainable manner——as mentioned earlier, itsAn innovative pipeline consisting of seven candidate drugs has been established.

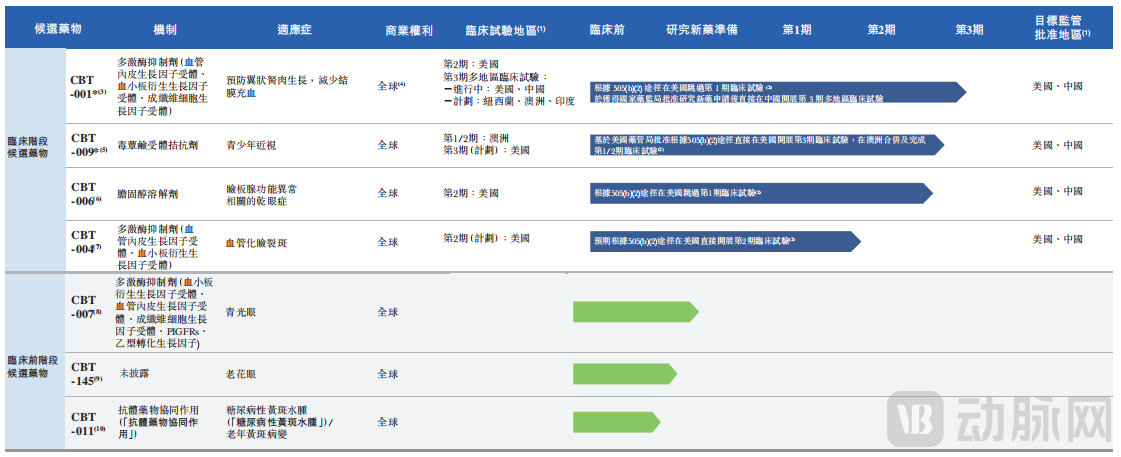

(Candidate Drug Pipeline of Cloudbreak Pharma Image Source: Prospectus)

Specifically, Cloudbreak PharmaFour drugs are in the clinical stage.. The prospectus shows,CBT-001 and CBT-004 are used to treat pterygium and vascularized pinguecula, respectively., These two types of ophthalmic diseases both have large patient populations and lack targeted and accessible drug treatments.

The other two drugsCBT-006 and CBT-009 are expected to be the world's first-in-class drug for treating dry eye disease associated with meibomian gland dysfunction and the world's best-in-class drug for treating juvenile myopia, respectively.

Among them, as one of the core products, CBT-009 eye drops received approval from the U.S. FDA on September 21, 2023, and will be the first to enter Phase III clinical trials in the United States. According to the prospectus, CBT-009 is the world's first innovative non-aqueous atropine eye drop, featuring a water-free, preservative-free, and multi-dose packaging design.

Not only that, but compared with existing aqueous atropine eye drops, the formulation stability of CBT-009 has been significantly improved, which can substantially reduce the degradation of atropine and thereby minimize the generation of impurities, allowing CBT-009 to be stored for a long time at room temperature or even high temperatures. Additionally, the CBT-009 eye drop itself has the ability to inhibit bacterial growth, eliminating the need for additional preservatives or special single-dose packaging. Moreover, as CBT-009 also functions as a comfort agent for the eyes, it offers an excellent user experience, which will greatly enhance compliance among adolescent patients.

Among the preclinical candidate drugs, Cloudbreak Pharma's three drugs each have their own strengths.Cloudbreak Pharma's CBT-007 is mainly used to improve the success rate of glaucoma filtration surgery; CBT-145 is a new chemical entity for the treatment of presbyopia; CBT-011 is a synergistic conjugate of antibody drugs for the treatment of diabetic macular edema.

It is worth mentioning that Cloudbreak Pharma has also developed two proprietary technology platforms — the MKI and ADS platforms, which are respectively used for developing drug candidates to treat anterior and posterior eye diseases. The MKI platform focuses on the development of small-molecule drugs, while the ADS platform targets the creation of antibody-small molecule drug conjugates.Based on two technology platforms, Cloudbreak Pharma is able to provide comprehensive solutions covering various ophthalmic diseases.

Over the past eight years of development, Cloudbreak Pharma has continued to expand. It established R&D and production bases in Guangzhou and Suzhou in 2018 and 2021 respectively, and set up a financial and legal center in Hong Kong in 2022.

In addition, R&D investment continues to increase. The prospectus shows that Cloudbreak Pharma's R&D expenditure increased by 80.8% from US$8.5 million in 2021 to US$15.3 million in 2022.

It is precisely due to the acceleration in research and development and clinical progress that after 8 years of dedication to the ophthalmic drug field, Cloudbreak Pharma has decided to pursue an initial public offering.

Of course, with the submission of the prospectus this time, the capital market will definitely consider the commercial prospects of Cloudbreak Pharma.

In this regard, the prospectus mentioned that CBT-001 is the most likely product to generate revenue first. Currently,Cloudbreak Pharma has signed a commercialization licensing agreement with Grand Pharmaceutical, leveraging Grand Pharmaceutical's distribution channel network to optimize the market potential of CBT-001.

At the same time, as Cloudbreak Pharma continues to advance the clinical trials of other drug candidates in its pipeline, it also hopes to leverage its cooperation experience with Grand Pharmaceutical to ensure strategic collaborations with other key market players. This will help implement a cost-effective commercialization strategy and establish global sales channels.

In other words, Cloudbreak Pharma, in collaboration with Grand Pharmaceutical, has already established commercial pathways to support the sales of the drug post-launch.

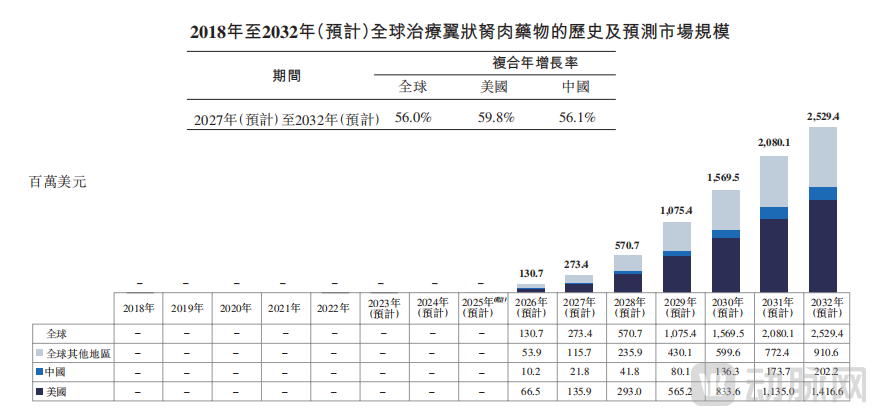

In addition, the scale of the patient population corresponding to the drug and the order of drug market entry are also important factors affecting the future commercial potential.According to the Frost & Sullivan report, Cloudbreak Pharma's CBT-001 and CBT-004 are expected to become drugs that address the issues faced by patients with pterygium and vascularized pinguecula globally. By 2032, the number of patients with pterygium and vascularized pinguecula worldwide is projected to reach 1.0771 billion and 1.2838 billion, respectively. The large patient population supports a promising market scale.

In the global market for drugs treating pterygium, the scale is expected to reach US$273 million by 2027 and US$2.529 billion by 2032, with a compound annual growth rate (CAGR) of 56.0%. Currently, there are no approved drugs globally for the treatment of pterygium. As of the submission of the prospectus, there are three clinical-stage drug candidates worldwide targeting pterygium and aiming to reduce conjunctival congestion. Among them, two candidates are in Phase II clinical trials, and one candidate, CBT-001, is in Phase III clinical trials.This means that CBT-001 may be the first to capture the market.

(Global Pterygium Drug Market Size Image Source: Prospectus)

(Global Pterygium Drug Market Size Image Source: Prospectus)

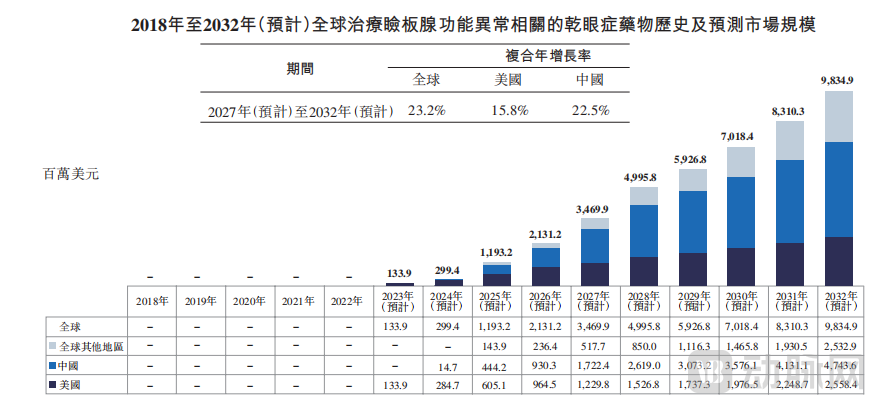

At the same time,Once approved, CBT-006 is also expected to become the world's first-of-its-kind drug for treating dry eye disease associated with meibomian gland dysfunction.To give you an idea, the global market size for dry eye disease has surpassed 10 billion US dollars. Moreover, meibomian gland dysfunction is a significant contributing factor in 70% to 86% of dry eye cases worldwide.

The prospectus shows that the number of patients with dry eye disease associated with meibomian gland dysfunction reached 835.6 million in 2022, with a compound annual growth rate (CAGR) of 1.1% from 2018 to 2022. It is expected to reach 885.4 million by 2027, with a CAGR of 1.2% from 2022 to 2027.

From this perspective, drugs treating dry eye disease associated with meibomian gland dysfunction have a promising market demand, allowing them to capture a share of the overall dry eye disease market. According to a Frost & Sullivan report, the global market size for drugs treating dry eye disease related to meibomian gland dysfunction is expected to reach $3.4 billion by 2027 and $9.8 billion by 2032, with a compound annual growth rate (CAGR) of 23.2%.

(Global Market Size for Drugs Treating Dry Eye Disease Associated with Meibomian Gland Dysfunction, Image Source: Prospectus)

(Global Market Size for Drugs Treating Dry Eye Disease Associated with Meibomian Gland Dysfunction, Image Source: Prospectus)

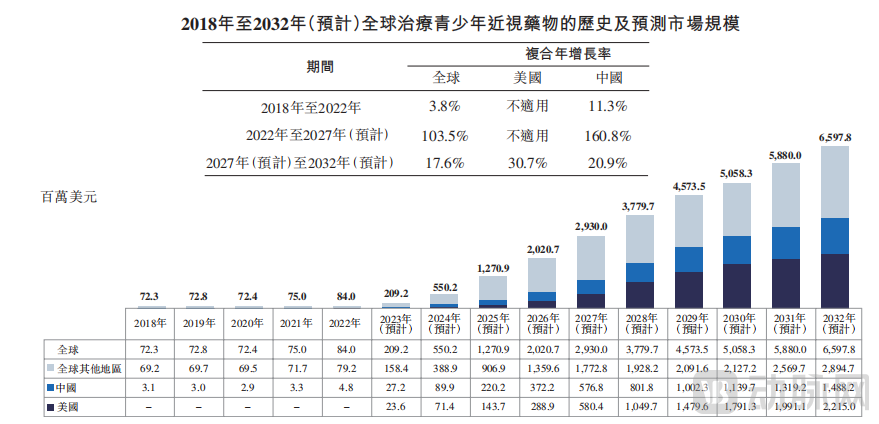

Besides,Cloudbreak Pharma's CBT-009 eye drops are positioned in the vast market for adolescent myopia drugs.According to a Frost & Sullivan report, the global market size for drugs treating adolescent myopia increased from US$72.3 million in 2018 to US$84 million in 2022, with a compound annual growth rate (CAGR) of 3.8%. It is expected to reach US$2.93 billion by 2027 and US$6.597 billion by 2032, with CAGRs of 103.5% from 2022 to 2027 and 17.6% from 2027 to 2032, respectively.

There is vast space, but currently, there are no atropine drugs approved in China for treating adolescent myopia, and no drugs approved in the United States for this condition either. Therefore, the first to gain approval and reach the market has a significant opportunity.

(Global Market Size for Myopia Drugs in Adolescents Source: Prospectus)

(Global Market Size for Myopia Drugs in Adolescents Source: Prospectus)

It is not difficult to find that Cloudbreak Pharma has taken the lead in multiple fields of ophthalmic disease medications. If clinical progress goes smoothly, the early market entry of several drugs will help it quickly enjoy market dividends, thereby achieving significant commercial returns.

The ophthalmology industry has long been considered a golden track by investors.

On the one hand, it is due to the ultra-high imagination of market space. According to the "2022 Ophthalmology Industry Research Report" released by VCBeat, since 2014, the ophthalmology market in China has maintained a double-digit high growth rate, and by 2021, the overall scale of the ophthalmology market had reached 210 billion yuan.

On the other hand, continuous policy support has also played a role. Whether it is the release of the "13th Five-Year Plan" for National Eye Health or the issuance of the "14th Five-Year Plan" for National Eye Health (2021-2025) by the National Health Commission, both have brought attention to the eye health of two major groups: the elderly and adolescents. Thanks to this, the industry will increase its focus on and procurement of ophthalmic-related drugs and devices.

Thus,VC/PE Flocking to the Ophthalmology Industry Amid Opportunities.In the past two years, top investment institutions such as Hillhouse Ventures, Sequoia China, Legend Capital, Northern Light Venture Capital, and Vivo Capital, as well as the strategic investment departments or industrial capital of giants like Tencent, Xiaohongshu, and Aier Eye Hospital, have all been strategically placing themselves in the ophthalmology sector.

It should be noted that there are already multiple listed companies in the ophthalmology services sector, with competition becoming increasingly fierce. An era where the strong grow stronger is approaching.Leading enterprises in China's ophthalmic pharmaceuticals and devices sector are still relatively scarce. Coupled with the vast global market opportunities in this field, the competition upstream in the industry has only just begun. More emerging companies are continuously striving, waiting for the right moment to overtake on the curve.

As a result, the upstream of ophthalmology (drugs + devices) has become the most focused area for capital.

First, look at ophthalmic pharmaceuticals.Currently, three mainstream directions have been formed. The first is traditional drugs, namely small-molecule chemical drugs; the second is large-molecule biologics, with ophthalmic drugs currently under research in China being mainly large-molecule drugs; and the third is the gene and cell therapy that has emerged in recent years.

Taking Zhongyin Technology, which completed financing in September, as an example, its developed ZVS101e injection is a gene replacement therapy drug for Bietti's Crystalline Dystrophy (BCD), suitable for BCD patients carrying the CYP4V2 gene mutation. It is the world's first drug to conduct clinical research and Phase I/II clinical trials for BCD. In August 2021, it received Orphan Drug Designation (ODD) from the U.S. FDA, and by the end of 2022, it obtained IND tacit approval in both China and the U.S. In February 2023, the first subject was successfully enrolled in the Phase I/II clinical trial at Tianjin Medical University Eye Hospital.

Shengyuan Medicine, which secured a new round of financing in July, focuses on tear biomarkers (Biomarker) as a key tool. Centered around the molecular mechanisms of diseases, the company is dedicated to developing innovative eye medications and precise ophthalmic Biomarker detection products. Among its developments, the dry eye drug SY-201, based on a novel mechanism, has completed Phase II clinical trials in the United States.

Next, let's look at ophthalmic devices.This field is highly segmented, including ophthalmic surgical robots, ophthalmic OCT, ICL (Implantable Collamer Lens), IOL (Intraocular Lens), orthokeratology lenses, ultra-widefield fundus cameras, phacoemulsification and vitrectomy machines, femtosecond lasers, ophthalmic surgical microscopes, optical biometers, contact lenses (including cosmetic lenses), and eyeglasses.

For instance, MicroEye Medical, which completed financing in November, has independently developed the Cleard® High-Precision Ophthalmic Surgical Robot. The original serial-parallel surgical robot technology system was created, and an exclusive serial-parallel robot mechanical structure was developed. This structure enables 5 degrees of freedom operation and micron-level precision positioning, effectively filtering out tremors and shakes that cannot be avoided by human hands. The repeatability positioning accuracy is stably controlled to within 10μm, allowing surgeons to perform operations while maintaining minimal incision tearing.

Intalight (formerly "Shiwei Imaging"), which completed financing in August, is transforming from an ophthalmic imaging company into a full-platform ophthalmic enterprise covering both diagnosis and treatment. Its representative products include ophthalmic OCTs. Taking the "Ruyi Full-Eye OCT" released in 2022 as an example, this product integrates several cutting-edge functions such as full eye-axis visualizable biometry, anterior segment OCT, posterior segment OCT, anterior segment OCTA, and posterior segment OCTA. Combined with 3D PAR technology and Deep Layer AI stratification technology, it enhances sensitivity to weak blood flow signals, achieving higher detection rates for complex lesions and early microvascular changes.

In addition to the companies mentioned above, there are quite a few emerging ophthalmology enterprises that are gaining traction and have already won capital favor. Going forward, driven by R&D and bolstered by capital, these companies are bound to continue heading towards IPOs and joining global market competition, going head-to-head with international giants.

In this process, the commercial story of China's ophthalmic innovation is bound to be sufficiently exciting and attractive.