Pfizer Completes $43B Seagen Acquisition Amid Strategic Pivot to Oncology and Post-Pandemic Restructuring

Seagen

Monoclonal Antibody Developer

Pfizer

Pharmaceutical R&D Developer

Pfizer went downhill in 2023.

In 2022, Pfizer made history for large pharmaceutical companies—due to COVID-19-related indications, Pfizer broke through the $100 billion revenue mark for the first time, becoming the first pharmaceutical giant with sales on a scale of tens of billions. According to the annual earnings report, COVID-19-related products contributed significantly to sales—the vaccine Comirnaty generated $37.8 billion in revenue; the oral medication Paxlovid generated $18.9 billion in revenue, totaling as high as $56.7 billion. More than half of the revenue was related to COVID-19, which also set the stage for a sharp decline in stock prices in 2023.

With over a hundred billion at stake, in a sense, the market's expectations for Pfizer have been blindly inflated.Pfizer also realized this, with the annual outlook projecting a 29% to 33% decline in performance, approximately $67 billion to $71 billion. The full-year 2023 revenue forecast for the COVID-19 vaccine Comirnaty is expected to decrease by 70% year-over-year; the full-year 2023 revenue forecast for the COVID-19 drug Paxlovid is expected to drop by 95% year-over-year.

With its COVID-19 products plummeting and its GLP-1 pipeline failing, leading to the termination of development, Pfizer's investor confidence is hanging by a thread. Industry media Endpoints News pointed out that Pfizer was the worst-performing large pharmaceutical stock in 2023, dropping 44% within the year and losing approximately $140 billion in market value.

On December 14, Pfizer announced the completion of its acquisition of Seagen, a leading ADC company.Walking down the slope of stock prices, Pfizer has heavily invested another 43 billion yuan, showing its determination to double down on ADC and bolster its oncology sector. But more challenging questions remain: how to complete large acquisitions amid increasing antitrust scrutiny? And how to bridge the growth gap brought by such acquisitions?

The primary challenge of the Seagen acquisition comes from antitrust reviews by the U.S. Federal Trade Commission (FTC) and the European Commission. A background factor is that the FTC has strengthened its scrutiny of merger deals in recent years, with the investigation process becoming increasingly complex, the review period lengthening, and being related to the scale of the deal.

"To address the concerns of the FTC,"In March, Pfizer terminated the Bavencio cooperation agreement with Merck, transferring the related development and commercialization rights to Merck, while retaining a 15% royalty on net sales.Bavencio, a PD-L1 inhibitor for the treatment of locally advanced or metastatic urothelial carcinoma (mUC), generated $271 million in sales for Pfizer in 2022. Nine years ago, the upfront payment for this deal was $850 million.

Whether this transfer had a direct effect on regulatory approval is unknown, but the determination for the deal and transformation is crystal clear. As a result, the European Commission unconditionally approved Pfizer's $43 billion acquisition deal, stating that the transaction would not cause competition concerns, mainly due to two aspects:

lAlthough the two companies have overlapping pipelines and marketed products in the fields of breast cancer, bladder cancer, colorectal cancer, cervical cancer, and lung cancer, their products exhibit "differentiation and complementarity," targeting "different patient populations" with "different modes of action and treatment methods." Therefore, the acquisition is unlikely to cause disruption, delay, or repositioning of overlapping or similar pipelines.

lThe acquisition and merger are "unlikely to have a negative impact on prices," and the market behind the products is "highly competitive" — with numerous global players in the oncology field and the ADC market, the deal will not lead to a loss of innovation.

Later, Pfizer doubled down on the issue with Bavencio.Irrevocably and unconditionally donate 15% of the net sales revenue as royalty to the American Association for Cancer Research (AACR),Support cancer prevention and treatment research. With such actions, Pfizer ended the waiting period of the antitrust law on December 11, completing all regulatory approvals required for the acquisition of Seagen.

In the March announcement of the acquisition, Pfizer expects to achieve this through$310 Billion in New Long-Term Debt, Combined with Short-Term Financing and Existing CashProvide substantial funding for this transaction. In the third to fourth full year following the completion of the transaction, it is expected to result in moderate to slight growth in adjusted diluted earnings per share (EPS). Nearly one billion US dollars in cost efficiencies will be achieved within the third full year after the completion of the transaction.

In May, Pfizer announced the pricing of a debt issuance consisting of eight tranches of notes, with interest rates ranging from 4.450% to 5.340%, and maturities from 2025 to 2063.The notes will be issued by Pfizer Investment Enterprises Pte., a wholly-owned subsidiary of Pfizer. The net proceeds from this offering will be used as part of the financing for Pfizer’s proposed acquisition of Seagen. If the merger is terminated or not completed by the agreed date, the notes will be subject to a special mandatory redemption (at a price equal to 101% of the aggregate principal amount of the series), except for the issuance of the 10-year notes and 30-year notes.

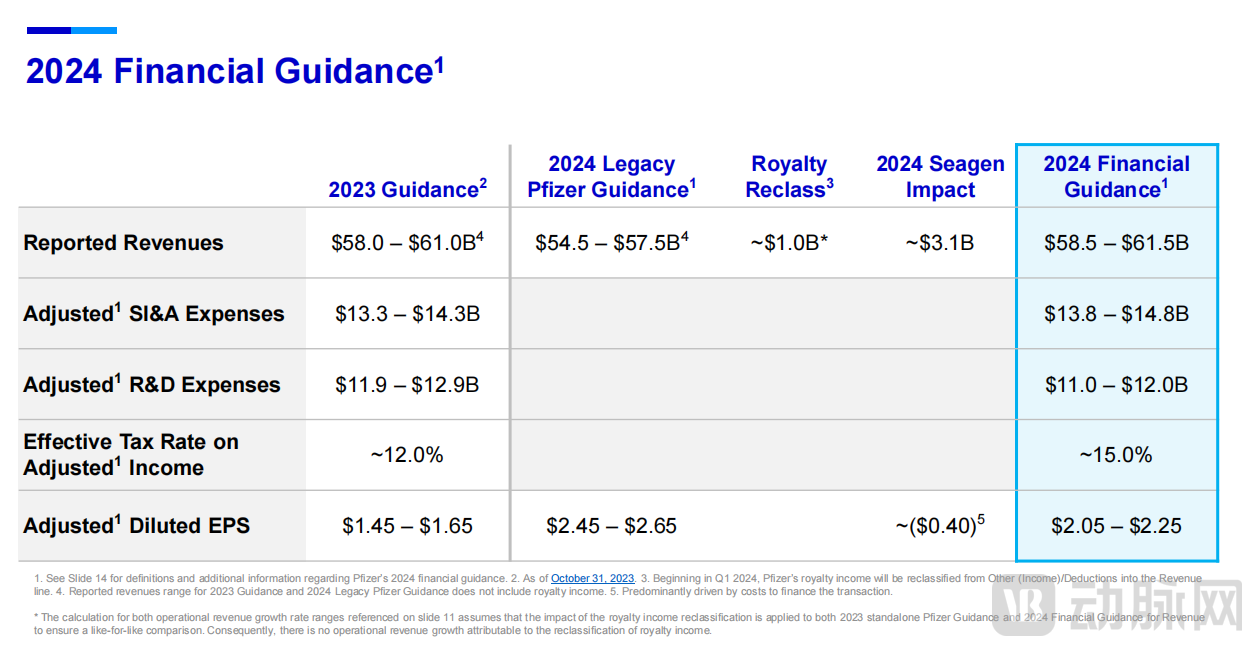

In the 2024 outlook updated on the 12th, Pfizer also noted that the expected impact of the Seagen acquisition would be a $0.40 per share dilution.

Before the release of its Q3 financial report, Pfizer had already announced its $3.5 billion cost-cutting plan, including the closure of its plant in Peapack, New Jersey. Of this amount, $1 billion is expected to be realized in 2023, and another $2.5 billion is expected to be realized in 2024 — meaning that Pfizer will undergo more cost-cutting measures next year.

Of course, layoffs are the main act in cost-cutting measures. Recently, during a live video conference with employees, Pfizer CEO Albert Bourla suddenly announced the layoff plan without any prior warning. Some employees immediately raised questions: Will my supervisor take a pay cut? Others expressed dissatisfaction in the comment section regarding the company's seemingly "arbitrary layoffs."

Just four months later, on December 12, Pfizer increased the amount of its cost-cutting plan from $3.5 billion to $4 billion, allocated within sales, information, and administrative (SI&A) expenses and R&D costs. Albert Bourla stated, "This puts us on track to regain our pre-COVID-19 pandemic operating profits." Foreign media reported that layoffs have begun for workers at Pfizer's plants in the U.S. and the U.K.

The main adjustments in the updated 2024 earnings outlook include the removal of royalty fees, inclusion of Seagen’s expected revenue, and accounting for the $0.40 dilutive impact from the acquisition of Seagen. After the update, Pfizer’s 2024 revenue is projected to be between $58.5 billion and $61.5 billion.Excluding COVID-19 products Comirnaty and Paxlovid, Pfizer's revenue growth is expected to be 8%-10%. Excluding the expected contributions from COVID-19 products and Seagen products, revenue growth is expected to be 3%-5%.

The acquisition announcement pointed out that oncology remains the largest growth driver in the global pharmaceutical industry. This acquisition will strengthen Pfizer's position in this field while expanding the global commercialization progress of Seagen's innovative drugs, jointly accelerating the next generation of potential cancer breakthroughs.

On a deeper level, this acquisition announces that Pfizer's future business direction will focus heavily on the field of oncology. In tandem, Pfizer will restructure its commercial framework, expedite the integration of Seagen, and enhance execution focus, speed, and quality.

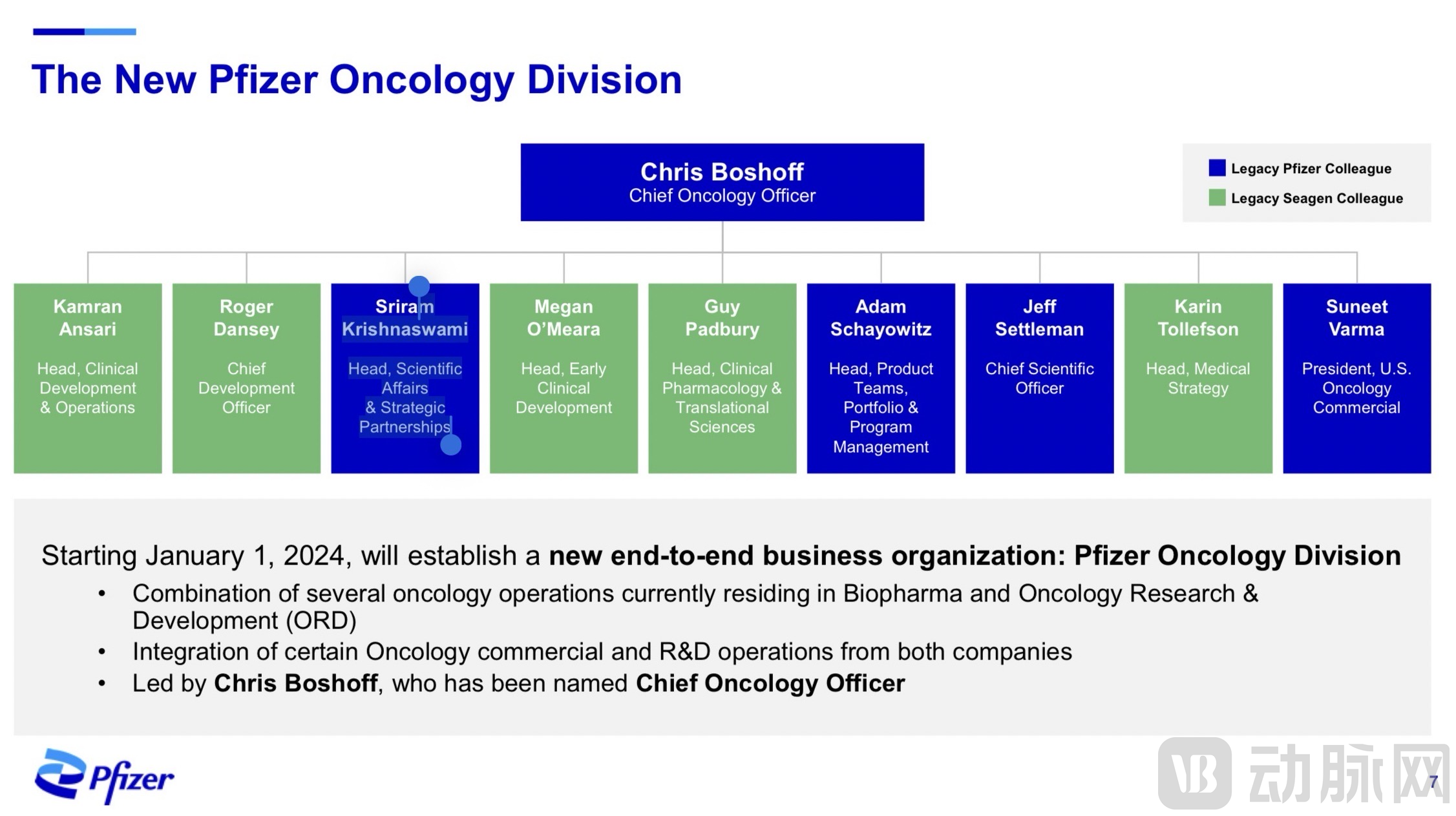

Specifically, starting from January 2024, Pfizer will create a new "Pfizer Oncology Division," integrating parts of the commercial and R&D oncology products from both companies.End-to-End Business Organization, led by Dr. Chris Boshoff, who is about to become the Chief Oncology Business Officer and Executive Vice President, and directly managed by Chairman and CEO Albert Bourla.

"Specific Structure of Pfizer's Oncology Division"

"Specific Structure of Pfizer's Oncology Division"

As can be seen from the specific structure, as an end-to-end business organization, "Pfizer Oncology" integrates the entire business line of oncology products from R&D, compliance to commercialization. The announcement also pointed out that this department will include several oncology business portfolios from Biopharma and Oncology Research & Development (ORD).The overall adjustment of the structure and the management system directly reaching Albert Bourla demonstrate Pfizer's determination to develop the oncology field.

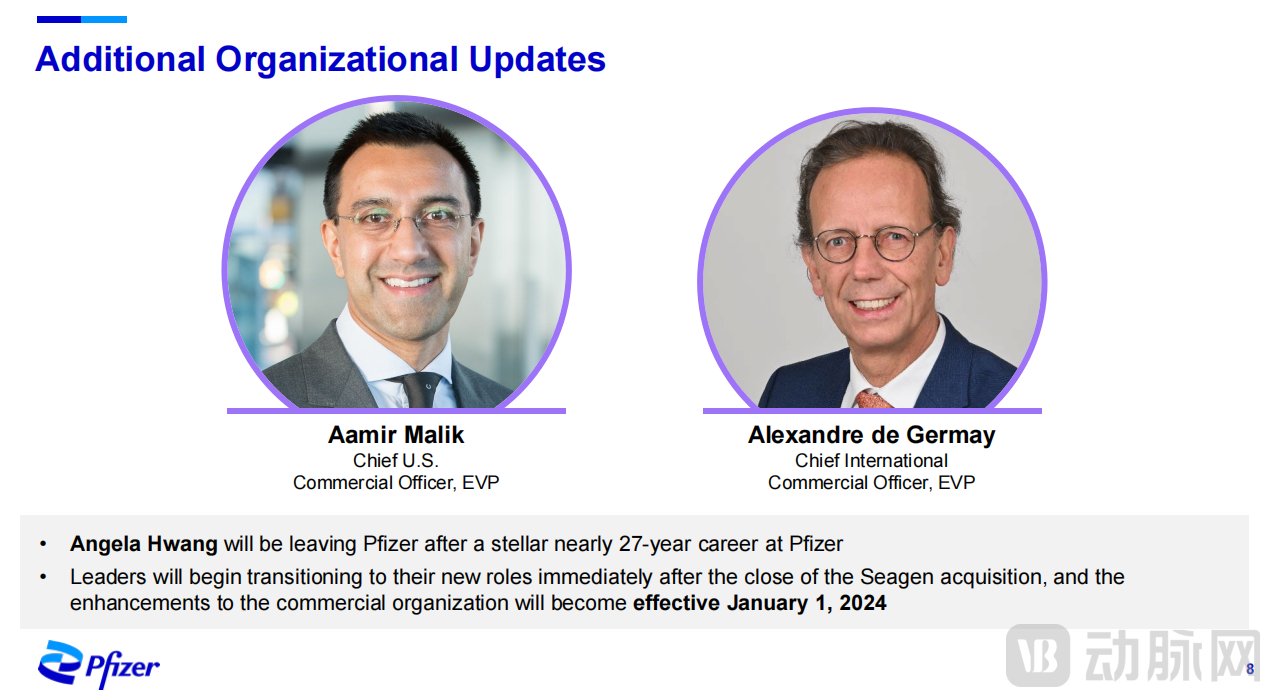

In addition, the non-oncology commercial organization will be split into two major business units: Pfizer U.S. Commercial Operations and Pfizer International Commercial Operations, both directly managed by Chairman and Chief Executive Officer Dr. Albert Bourla. Pfizer U.S. Commercial Operations will be led by Aamir Malik, who will serve as Chief U.S. Commercial Officer and Executive Vice President; Pfizer International Commercial Operations will be led by Alexandre de Germay, who will join Pfizer as Chief International Commercial Officer and Executive Vice President.

At the same time, Angela Hwang (Waiming Huang), Chief Commercial Officer and President of Global Biopharmaceutical Business at Pfizer, who has served for 27 years, will leave Pfizer. She will continue to act as an advisor to help Pfizer transition to the new model.

In October, due to the U.S. government returning approximately 7.9 million treatment courses of Paxlovid under EUA (Emergency Use Authorization), Pfizer reduced its 2023 revenue guidance for COVID-19 products by $9 billion, expecting a low period.However, this marks the beginning of the commercial transition for Pfizer's COVID-19 products.

As the distribution of Paxlovid with the EUA label has been discontinued, Paxlovid with the NDA (New Drug Application) label will enter the U.S. pharmaceutical system, with costs borne by individuals and insurance programs. Sales forecasts will also be determined based on the commercial market conditions. Pfizer will distribute the product to all sales channels by the end of this year, supporting the commercialization of Paxlovid starting January 1, 2024.

In addition,RSV Vaccine AbrysvoApproved for marketing in May, achieving $375 million in sales in Q3——Ranked among Pfizer's top seven products by sales in the first quarter, accounting for 2.8%.Pfizer expects that approximately 80 million elderly people and 1.5 million pregnant women will be suitable for vaccination during this year's to next year's RSV high season. This means that Abrysvo will continue to contribute significant growth to the company’s performance throughout the year. The commercialization of both vaccines will inject a new wave of growth and confidence into Pfizer’s 2024 market.

"Seagen's drugs, late-stage development plans, and pioneering expertise in antibody-drug conjugates (ADC) will complement Pfizer's oncology portfolio."

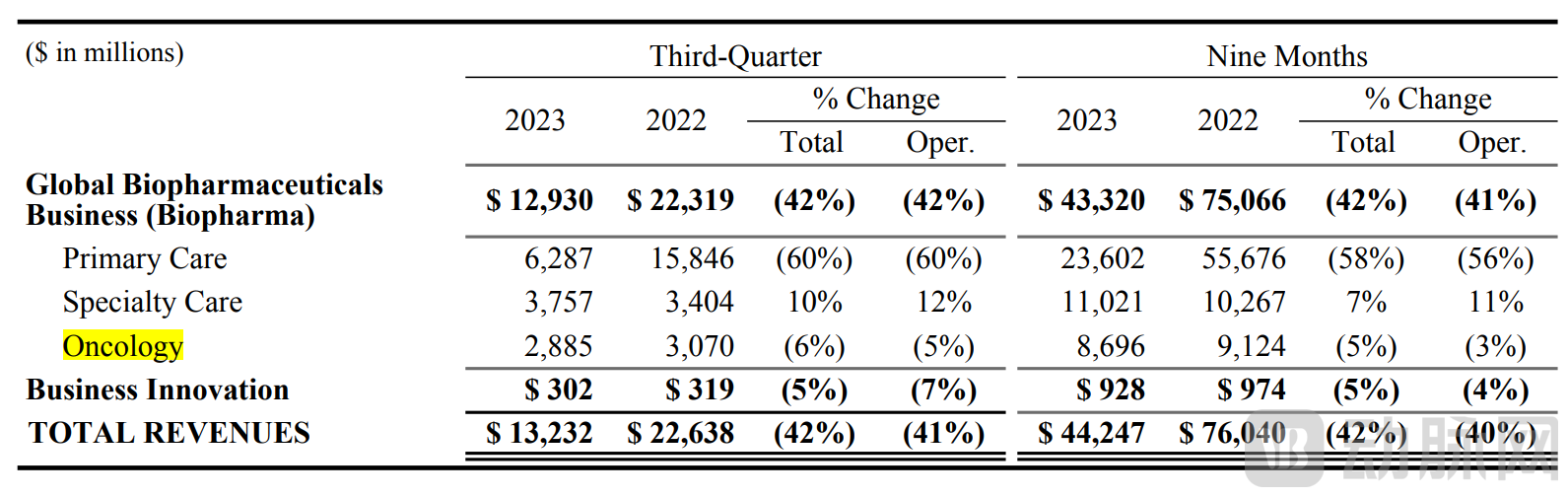

Before the acquisition, Pfizer's "Oncology" segment included 24 approved innovative cancer drugs and 33 clinical development pipelines, primarily focused on four major areas: breast cancer, genitourinary cancers, hematology, and precision medicine.However, Pfizer's Oncology segment was relatively weak in terms of profitability in the past, ranking only third, with revenue in the first three quarters falling short of $10 billion, a year-on-year decrease of 6%.The largest revenue-generating product is Palbociclib, which was launched in 2015 for breast cancer indications. It is now facing issues such as the impending patent cliff, lack of early inclusion in medical insurance, declining sales, and insufficient subsequent growth momentum.

Pfizer 2023 Q3 Earnings Report

Pfizer 2023 Q3 Earnings Report

In the ADC field, Pfizer only has two commercialized products, which are Oglivozumab and Gemtuzumab, acquired from Wyeth in 2009 for $68 billion.After merging with Seagen, Pfizer will additionally own four approved ADC products, including Adcetris (the first-line treatment for refractory Hodgkin's lymphoma), Padcev (locally advanced or metastatic urothelial cancer), Tukysa (locally advanced unresectable or metastatic HER2-positive breast cancer), and Tivdak (recurrent or metastatic cervical cancer).

The 2022 financial report disclosed that Seagen's total annual revenue was $2 billion, with net product sales of $1.7 billion, representing a year-over-year increase of 23%.Pfizer expects acquisitions of Seagen to bring in an additional $10 billion in annual revenue from the products by 2030.At the same time, Seagen will bring an early-stage ADC oncology pipeline that doubles the existing portfolio, along with a specialized ADC team, enriching the R&D reserves and supporting future growth. It is reported that half of the new leadership in Pfizer's oncology division will be long-standing Pfizer employees, while the other half will come from Seagen.

Objectively speaking, after achieving a fleeting billion-dollar revenue, Pfizer has sufficient "capital" and preparation to take over Seagen at one stroke. However, the market reaction was far more intense than Pfizer had anticipated — after announcing the 2024 forecast, the stock price fell another 7% before the opening on the 13th, with its market value dropping to 150.5 billion US dollars.

After reaching the peak, any path you take will be downhill. The key is whether a company can land smoothly and find the next intersection leading to the summit. Seagen's $3.1 billion in annual revenue pales in comparison to Pfizer's whopping $43 billion, but the "world's largest pharmaceutical company" doesn’t need a rescue story.