Why Are AI-Developed Drugs Piling Up in Phase II Clinical Trials?

NVIDIA

Artificial Intelligence Computing Service Provider

XtalPi

Computation-Driven Innovative Drug R&D Provider

Empowering new drug research and development with digital intelligence has always been regarded as the most valuable path for AI in the healthcare field. With this belief, life science AI companies worldwide have invested hundreds of billions of funds into this area in recent years.

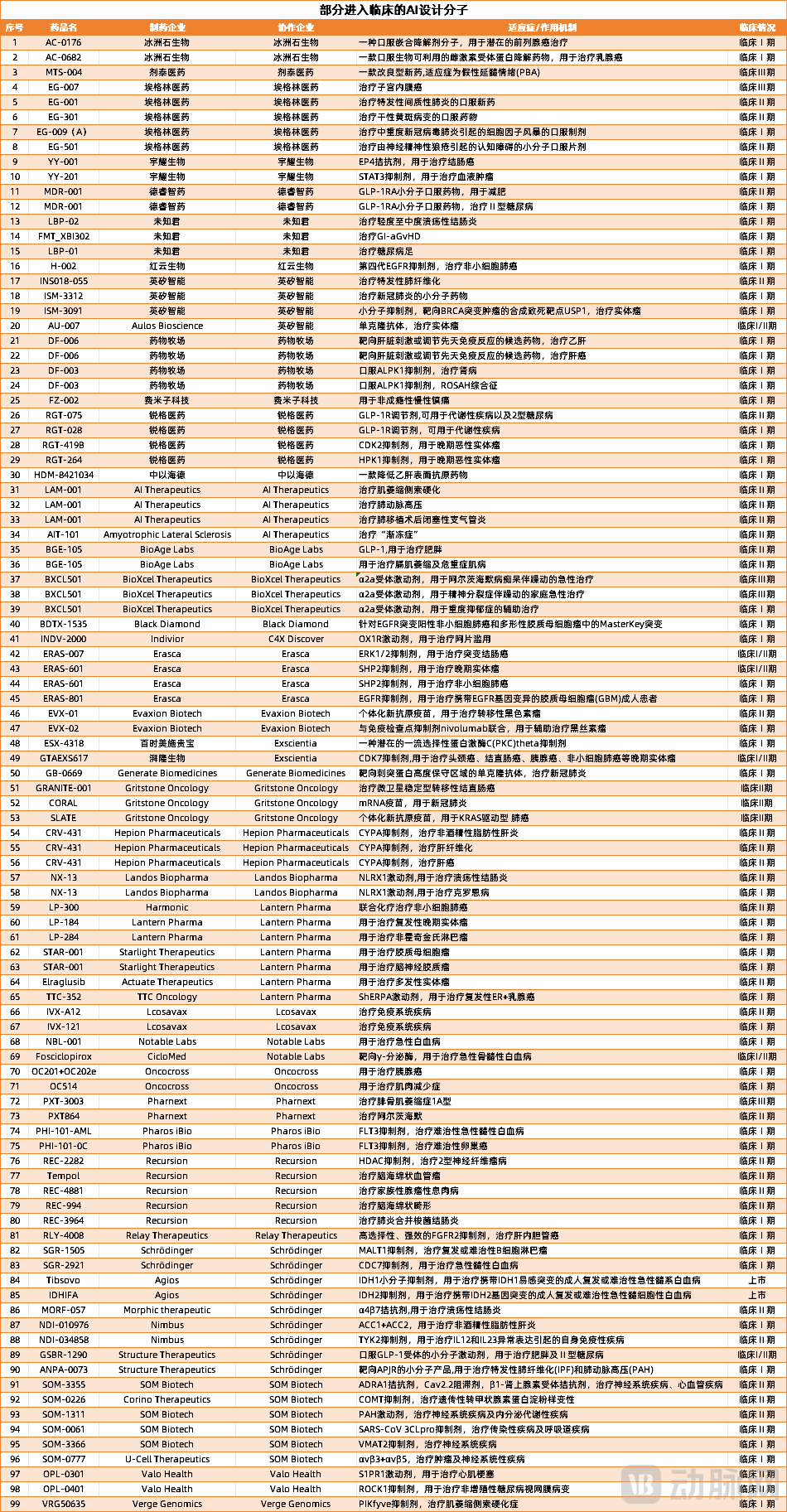

According to incomplete statistics from VCBeat: As of October 31, 2023, AI Biotech has participated in at least 116 pipelines that have entered clinical trials globally, which has increased by two orders of magnitude compared to 2020.

However, the risks behind new drug development will not make concessions just because it is a new technology. Among the more than a hundred pipelines, 16 have been discontinued or removed from the official website, and one drug has been downgraded in clinical trial priority. The remaining 99 pipelines still have some time before completing clinical trials, with over half in Phase I clinical trials and more than one-third in Phase II clinical trials.

A total of five pipelines have been fortunate enough to enter Phase III clinical trials, with two drugs successfully reaching the market. However, these drugs either underwent AI adjustments after being licensed-in, or were mainly developed along traditional pathways or repurposed from existing drugs, with AI playing a minimal role or its involvement being unclear.

In other words, no drug primarily driven by AI has yet entered Phase III clinical trials.

Active Pipeline Held by Life Science AI Companies

Active Pipeline Held by Life Science AI Companies

(Clinical Phase I - Market Launch Stage, Incomplete Statistics, As of October 31, 2023)

Such results seem to not reflect the value of AI Biotech's early financing, which often amounts to hundreds of millions, and fail to demonstrate AI’s role in advancing drug research and development.

It is hard not to arouse curiosity about why new drugs developed by AI struggle to get past Phase II clinical trials?

In 2014, Sumitomo Dainippon Pharma, a veteran Japanese MNC, partnered with Exscientia, a British AI-driven drug discovery company, to focus on discovering new psychiatric treatment drugs targeting monoamine G protein-coupled receptors (GPCRs).

At that time, Sumitomo focused on Exscientia's automatic compound generation technology and AI prediction models based on knowledge graphs. The former theoretically ensures the feasibility and novelty of synthesized compounds, while the latter can predict the pharmacological activity of targets, the toxicological impact on targets, and some characteristics of pharmacokinetics.

By combining both, Sumitomo理论上能够预测由自动结构生成的大量虚拟化合物的药理活性和药代动力学特征,进而在化合物的发现与验证环节省下巨额成本。

The cooperation between the two parties was once very smooth. In an experiment to design 5-HT1A receptor agonist active drugs, they initiated a biweekly cycle model: Exscientia proposed compounds, Sumitomo's chemistry team was responsible for synthesis, and the pharmacology team evaluated these compounds.

With the support of innovative models, Sumitomo and Exscientia constructed over 350 molecules within a year, eventually establishing the precursor to DSP-1181 and advancing it into clinical trials. This marks the world’s first AI-designed molecule to enter the clinical stage, reducing the time from initial conception to final confirmation from the industry average of 4.5 years to less than one year.

However, the good start of DSP-1181 did not help it achieve further breakthroughs. Due to the Phase I clinical study not meeting the expected standards, DSP-1181 was discontinued in 2022.

In addition, DSP-0038 (a dual-target 5-HT1a receptor agonist and 5-HT2a receptor antagonist for the treatment of Alzheimer's disease) and EXS-21546 (an A2a receptor antagonist for the treatment of advanced solid tumors), both under Exscientia, have also encountered issues. The former disappeared without a trace after being removed from the official website, while the latter was directly discontinued due to failure to meet therapeutic expectations.

Todd Wills from the American Chemical Abstracts Service once conducted a detailed analysis of the novelty of three drugs developed by Exscientia that have entered clinical trials. He found that all three drugs faced issues of insufficient novelty.

After analyzing the DSP-1181 series of patents, Wills found that these molecules are very similar to haloperidol, a typical antipsychotic drug approved by the FDA in 1967. In this sense, Exscientia is likely optimizing a molecular backbone that has been discovered for a long time.

Among the 350 other molecules synthesized and analyzed during the discovery of DSP-1181, a large number were similar to haloperidol, while some mimicked 28 other FDA-approved drugs, including lamotrigine (an antiepileptic drug and mood stabilizer). Therefore, DSP-1181 may have been disadvantaged in the early stage by the lack of an intelligently supported knowledge graph.

Unlike Exscientia's failure, in 2022, the British AI pharmaceutical leader Benevolent AI halted the clinical development of BEN-229, a topical pan-Trk inhibitor for treating atopic dermatitis, because it failed to meet the secondary efficacy endpoint in Phase II clinical trials.

In the Phase Ⅱa study, the primary endpoint of BEN-229 measured safety and tolerability, while the secondary endpoint assessed the proportion of patients who showed improvement in the Eczema Area and Severity Index (EASI) and the Numerical Rating Scale (NRS) for pruritus.

Although the results of the primary endpoint met the expected goal, they did not show a statistically significant impact on the EASI or NRS endpoints for participants in the treatment group; in other words, the drug's efficacy was not proven.

Analyzing the reasons for BEN-229's failure, some experts believe that the earliest issues may have arisen during the project initiation phase.

For a long time, the main treatments for mild and moderate atopic dermatitis have been topical corticosteroids (TCS) and calcineurin inhibitors (TCI). Later, PDE4 inhibitors, IL-4/IL-13 inhibitors, and JAK inhibitors emerged for treating moderate to severe patients.

However, when evaluating pathways, knowledge graphs do not seem to accurately assess the risks of new drug development. BenevolentAI’s choice of the Trk receptor as a target is akin to straying from the well-lit main road into a winding path filled with unknowns.

It should be noted that mentioning the discontinuation of several drug developments such as DSP-1181 and BEN-229 is not to demonstrate that AI technology itself lacks revolutionary value for life sciences. These failed pipelines were typically initiated many years ago, and together they account for less than 10% of the total pipeline volume.

On the contrary, these cases are more like valuable experiences found by the pioneers in the pursuit of AI, telling the followers: to change the possibility of clinical success, it is not only about better molecules, but also about grasping every detail in project initiation, compound discovery, and the clinical trial process.

As for the phenomenon of AI-developed drugs clustering in Phase II clinical trials, life science AI companies themselves are the main cause. Since most of them were established around 2020, their self-developed or collaborative pharmaceutical enterprises have only been operating for 2 to 4 years. In the early stages of drug optimization exploration, reaching Phase II clinical trials can be considered a normal pace. To truly assess AI's capabilities, it will take at least another 3 to 5 years.

Although the notion that AI-developed drugs struggle to surpass Phase II clinical trials is merely an illusion, AI Biotech is indeed encountering some challenges during this period.

The key to Biotech's survival in the face of the疯狂expenditure on new drug research and development lies in financing. The same applies to AI Biotech.

In the past few years, top-tier institutions such as Sequoia China, Hillhouse, and Temasek; internet giants like Tencent and Baidu; and multinational pharmaceutical companies such as Eli Lilly, Sanofi, and Fosun Pharma have successively invested in AI for life sciences, supporting a large number of innovative AI Biotech explorations.

However, by 2022, the U.S. secondary market was sharply halved, with only 20 projects launched throughout the year, 11 of which were in healthcare, representing a staggering 94% decline. The domestic AI pharmaceutical sector also experienced its first cooling in funding, with only 32 financing events recorded between August 31, 2022, and October 31, 2023, showing a decrease compared to 47 events during the same period in 2022 and 43 events in 2021. Additionally, in 2023, most of the financing in the AI pharmaceutical sector focused on projects below Series A.

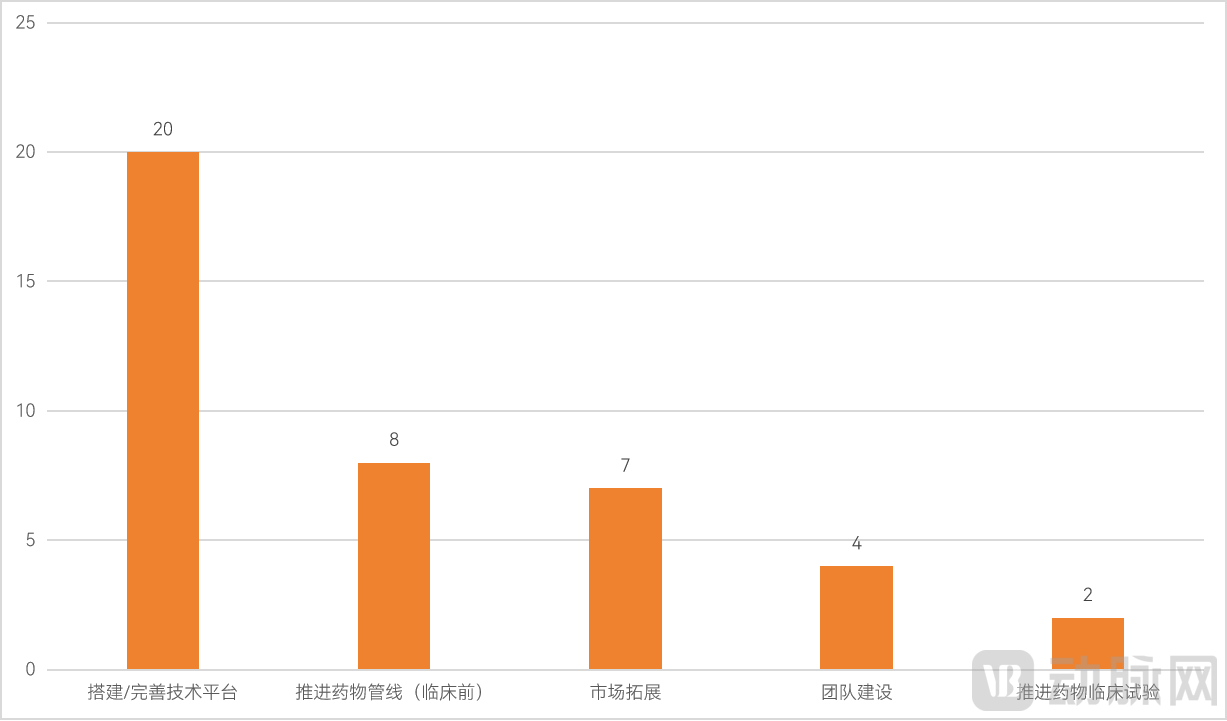

According to statistics, among the financing purposes, only DrugFarm, which completed its C-round financing, and RedCloud Biotech, which completed its B+-round financing, used the funds to advance drug clinical trials. The remaining financings were at relatively early stages, used for building technology platforms and advancing preclinical drug research.

The use of financing reflects the changing role of AI in drug development. While the allure of independently developing a drug and bringing it to market is strong, many AI Biotechs have shifted their focus to SaaS platforms and CRO services when the funding required for supporting platforms and pipelines becomes too large and the companies lack sufficient capital.

2023 Statistics on the Use of AI Pharmaceutical Financing

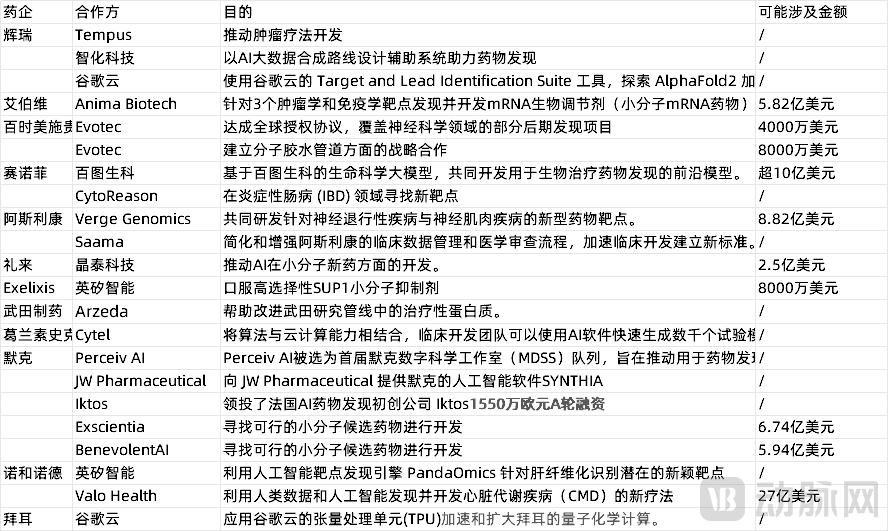

Moreover, compared with the previous two years, the number of collaborations in 2023 has slightly decreased, with upfront payments and total contract values also declining. Over the span of 10 months, collaborations such as AbbVie's partnership with Anima Biotech worth $582 million; Sanofi’s collaboration with BioMap exceeding $1 billion; Merck KGaA's announcement of partnerships with BenevolentAI and Exscientia amounting to $1.268 billion; and Novo Nordisk’s $2.7 billion collaboration with Valo Health have collectively bolstered expectations for AI in 2023.

Some Pharmaceutical Companies' Collaborations with AI Enterprises in 2023

Reduced collaborative payments mean that pharmaceutical companies have raised their requirements for AI Biotech, also prompting the latter to review their pipelines and consider the commercial prospects of new drugs after they hit the market.

Under the dual trends, many AI Biotech companies have attempted to transform or divest their pipelines. For instance, the discontinuation of the COVID-19 indication for BGE-175 (a PGD2-DP1 inhibitor aimed at reducing the severity of infectious diseases like COVID-19) under BioAge Labs was due to the loss of an ideal commercialization scenario as the pandemic subsided. Similarly, Black Diamond's decision to halt the development of BDTX-189 (a small molecule inhibitor for treating HER2 allosteric mutations) was driven by the company’s 30% workforce reduction to control costs and significantly cut expenses.

For AI Biotech, both options might help the company survive more easily, but they will also prolong the time that clinical trials remain in Phase II.

Under objective data, AI in the life sciences seems somewhat diminished, but this could also be an illusion caused by the current macroeconomic situation. In such times, cross-industry comparisons may reveal the essence of the industry more clearly than comparisons over time.

NVIDIA's extensive investment in the new drug development field this year, as well as Sanofi's all-in commitment to AI, are both conveying their recognition of this new technology and their willingness to invest funds and time into it.

We may also need to abandon the binary view of whether a new drug is successful or not, and look at the AI in life sciences track with a different perspective.

After all, even if it cannot reach the 80%-90% R&D success rate expected by many, as long as the average success rate of 7.9% (data from BIO, Informa Pharma Intelligence, and QLS reports, research period from 2011 to 2020) is increased to 10%, AI can effectively accelerate the output of new drugs and unleash value sufficient to match the current investment scale.

Then, the boost this technology gives to the life sciences confirms its meaningful existence.