GSK Inks $3.28 Billion Deal to Acquire Two China-Developed ADCs from Hansoh Pharma

Hansoh Pharma

Pharmaceutical Research, Production, and Sales

GSK

Pharmaceutical R&D Manufacturer

On December 20, Hansoh Pharma announced that it had entered into a licensing agreement with multinational pharmaceutical company GSK. GSK will be granted an exclusive global license (excluding mainland China, Hong Kong, Macao, and Taiwan) to develop, manufacture, and commercialize HS-20093, a drug developed by Hansoh Pharma.

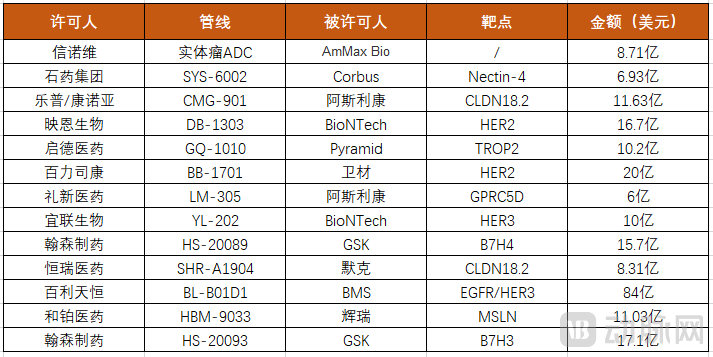

According to the agreement between both parties, the total amount of this transaction exceeds 1.7 billion US dollars, of which Hansoh Pharma will receive an upfront payment of 185 million US dollars and is eligible to receive milestone payments of up to 1.525 billion US dollars upon the achievement of related events for this product.

At the same time, after the commercialization of this product, GSK will also pay Hansoh Pharma a tiered royalty on global net sales outside mainland China, Hong Kong, Macao, and Taiwan.

HS-20093 is a novel B7-H3-targeted ADC drug, covalently linked by a fully humanized B7-H3 monoclonal antibody and a topoisomerase inhibitor (TOPOi) payload. It is currently undergoing multiple Phase I and Phase II clinical trials in China for the treatment of lung cancer, sarcoma, head and neck cancer, and other solid tumors.

This is already the second transaction cooperation reached this year between GSK and Hansoh Pharma on the ADC project.

Total of $3.28 Billion for Two Deals

In October this year, Hansoh Pharma reached a major product licensing agreement with GSK worth a total transaction value of $1.57 billion. Hansoh Pharma granted GSK the global rights outside Greater China for its self-developed B7-H4 ADC project HS-20089. Hansoh Pharma will receive an upfront payment of $85 million, along with potential milestone payments of up to $1.485 billion.

Two months later, the two parties reached an even larger transaction for the B7-H3 ADC project HS-20093.

HS-20093 and HS-20089 are undoubtedly the flagship assets of Hansoh Pharma. Among more than 30 innovative drugs in clinical stages developed by Hansoh Pharma, these two products are ADCs with leading global progress.

HS-20089 is composed of a humanized lgG1 anti-B7-H4 monoclonal antibody linked via a cleavable linker to a topoisomerase I inhibitor payload, with a DAR value of 6. B7-H4 is a transmembrane glycoprotein of the B7 superfamily, showing limited expression in normal tissues but overexpressed in a series of solid tumors such as breast cancer, ovarian cancer, endometrial cancer, and cholangiocarcinoma. Therefore, B7-H4 can also serve as a tumor biomarker, and ADCs are one of the mainstream development directions currently.

HS-20089 Project for Treating Patients with Advanced Solid Tumors Debuted at the ESMO Conference in October This Year. The Phase I Clinical Trial Results Showed That, Among 33 Evaluable Patients, the ORR Was 24.2%. In 16 Patients with TNBC (Triple-Negative Breast Cancer), 6 Achieved PR, with an ORR of 37.5%. The ORR in the High-Dose Group Was 41.7%, Demonstrating BIC Potential.

Looking at the layout of targets in the ADC track, the B7-H4 target is relatively niche compared to the crowded HER2, CLDN18.2, and CD19 targets. Currently, there are only four B7-H4 ADCs globally that have entered clinical stages. HS-20089 is currently the most advanced B7-H4 ADC in global development, followed by AstraZeneca's AZD8205, which is in Phase I/II clinical trials. Seagen/Pfizer's SGN-B7H4V and Mersana's XMT-1660 are both in Phase I clinical trials.

The HS-20093 project is the frontrunner among China-produced B7-H3 ADC new drugs. Currently, there are nine drugs targeting the B7H3 globally that have entered the clinical stage. The most advanced is MacroGenics' vobramitamab duocarmazine, which is in Phase II/III clinical trials. Close behind is Hansoh Pharma's HS-20093, which has initiated the Phase II ARTEMIS-002 study for indications including myeloma and soft tissue sarcoma. At a similar stage of progress is Daiichi Sankyo's ifinatamab deruxtecan.

In China, apart from Hansoh Pharma's HS-20093 being in Phase II clinical trials, similar products from companies such as Yilian Biotech, Bio-Thera, and Mabwell have also entered the clinical stage, with Hansoh Pharma leading the domestic R&D progress in this category.

The deal with Hansoh Pharma is of great significance for GSK to enhance its ADC portfolio. Part of GSK's strategic R&D focus includes targeted therapies for tumor cells and gynecological cancers. The company holds multiple research assets targeting endometrial cancer, as well as several other ADC projects currently undergoing oncology evaluation. Additionally, GSK has an approved ADC drug, Blenrep, which received FDA approval in August 2020 for treating patients with multiple myeloma who have failed four prior lines of therapy. The two deals with Hansoh Pharma will bolster GSK’s ADC pipeline across various cancer indications.

Transaction Amount Exceeds $22 Billion, MNCs Aggressively Procure China ADC

The recent global investment boom in ADCs contrasts sharply with the initial market entry of ADCs. Pfizer launched Mylotarg for leukemia treatment in 2000, but later withdrew it and reintroduced it at a lower dose. The second ADC approved in the U.S. was Seagen's Adcetris, which received its first FDA approval in August 2011 for the treatment of Hodgkin lymphoma and systemic anaplastic large cell lymphoma. It wasn't until 11 years later that it was approved as the world’s first ADC for frontline therapy. Since then, nearly a dozen ADC drugs have been launched globally, sparking increased interest in the ADC category.

GSK is just one of the large pharmaceutical companies that have been aggressively purchasing ADCs in China in recent months. Prior to this, Merck followed in the footsteps of AstraZeneca and BioNTech, paying $4 billion upfront to co-develop three of Daiichi Sankyo's promising ADC products. It also reached a development collaboration agreement for an ADC pipeline with China's Kelun-Biotech.

Just last week, BMS also joined the acquisition of China's ADC pipeline by partnering with SystImmune, a subsidiary of Baili Tianhe, and prepaid $800 million for the development of its Phase II solid tumor bispecific ADC candidate. Meanwhile, after acquiring Seagen, Pfizer struck a collaboration deal with Harbour BioMed for the MSLN-targeted ADC drug HBM9033.

2023 ADC Licensing Deals of Chinese Pharmaceutical Companies

Pacific Securities once released a research report stating that as of December 2023, there have been over 20 overseas transactions involving Chinese-produced ADCs in the past two years, with Chinese pharmaceutical companies once again becoming the main innovators. The firm believes that Chinese pharmaceutical companies excel at engineering-based innovations, and ADCs offer far greater room for modification compared to other types of innovative drugs. In the future, ADCs will become a standard tool in cancer treatment, and the golden age of ADCs is just beginning.

Since 2018, 15 to 57 ADC candidates have entered clinical trials each year. As of March 31, 2023, there are over 500 ongoing clinical trials worldwide involving 222 ADC candidates, among which 130, 75, and 17 are currently in Phase I, Phase II, and Phase III clinical trials, respectively. More than 100 abstracts related to ADCs were presented at the 2023 American Society of Clinical Oncology (ASCO) Annual Meeting, showcasing the vigorous clinical development progress of ADC drugs.

MNC's Acquisition of China's ADC Pipeline Not Only Signifies Multinational Pharmaceutical Companies Accelerating Layout in the ADC Sector, but Also Represents a Test of Strength for Chinese Pharmaceutical Companies Amid the Current Capital Winter. China's Innovative Drug Industry is Transitioning from a Model Focused Solely on Pipeline Progress to a Dual Competition Model Based on Overseas Expansion Speed and Pipeline Progress.

References:

1.https://www.sohu.com/a/731330283_121029209

2.https://baijiahao.baidu.com/s?id=1776906333323792133&wfr=spider&for=pc