JPM Spotlight: Over $6 Billion in Deals Ignites a 'Year of Mega-M&A' as Lilly, Merck, Pfizer, and Novo Nordisk Engage in a High-Stakes Game of Strategic One-Upmanship

Johnson & Johnson

Healthcare Product Manufacturers, Health Service Providers

MSD

Pharmaceutical R&D and Manufacturer

Eli Lilly

Global Pharmaceutical R&D and Production Company

Pfizer

Pharmaceutical R&D Developer

Novartis

Drug Development and Manufacturing

Bristol-Myers Squibb

Biopharmaceutical and Nutritional Product R&D and Sales

Novo Nordisk

Insulin Developer and Manufacturer

AstraZeneca

Biopharmaceutical Manufacturer

GSK

Pharmaceutical R&D Manufacturer

Daiichi-Sankyo

Pharmaceutical R&D Developer

Recently, the 42nd J.P. Morgan Healthcare Conference (JPM Conference) was held as scheduled in San Francisco.

As one of the largest healthcare investment and industry cooperation conferences in the global biopharmaceutical and health field, the JPM Conference covers various aspects of global healthcare. The content of speeches delivered by leaders of multinational pharmaceutical companies (MNCs) at the JPM Conference also indicates the focus of their annual strategic priorities.

Notably, on the first day of the JPM conference, multinational pharmaceutical giants achieved a "strong start," reaching agreements exceeding $6 billion. Merck & Co., Inc. announced that it would acquire cancer drug developer Harpoon Therapeutics for approximately $680 million to obtain early-stage immunotherapies targeting lung cancer and multiple myeloma currently in clinical trials. Boston Scientific Corporation announced a $3.7 billion acquisition of medical device company Axonics to strengthen its position in the minimally invasive surgery market for urology and bowel treatments. Johnson & Johnson declared it would acquire biopharmaceutical company Ambrx Biopharma for up to $2 billion, betting on novel antibody-drug conjugates (ADCs) for cancer treatment, aiming to fill potential revenue gaps when the "patent cliff" hits in 2025.

In fact, in the field of cancer treatment, ADC has already become a popular track that major pharmaceutical giants are scrambling to seize. This type of drug is called a "biological missile," which can directly target and kill cancer cells while minimizing damage to healthy tissues. Apart from Johnson & Johnson, other large pharmaceutical companies, including Pfizer, AbbVie, and Merck & Co., Inc., have also previously focused on ADC products.

On the other hand, the field of obesity drugs remains a popular track that giants continue to focus on.

Eli Lilly CEO David Ricks also stated at the JPM conference that by the end of December, the company's obesity drug Zepbound was adding 25,000 new prescriptions per week. It may still be in short supply in 2024, and the company is actively addressing the issue. In 2023, Eli Lilly announced the expansion of its plant in North Carolina, USA, and the construction of a new plant in Germany. Just recently, Eli Lilly also launched a website that allows people to order the obesity drug directly from the company’s website.

Moreover, to further promote the comprehensive rollout of GLP-1 in the market, major GLP-1 "players" are actively exploring the auxiliary effects of their products in the cardiovascular field. The aim is to prove that weight loss can help reduce the risk of cardiovascular diseases and assist in getting the weight-loss indication of their products covered by medical insurance. Once successful, this could further ignite the GLP-1 market and lead to another wave of explosive growth. Analysts predict that by the end of this century, the entire obesity drug market could reach a scale of 100 billion US dollars. As pioneers in GLP-1-based obesity drugs, Eli Lilly and Novo Nordisk have already achieved billions of dollars in revenue.

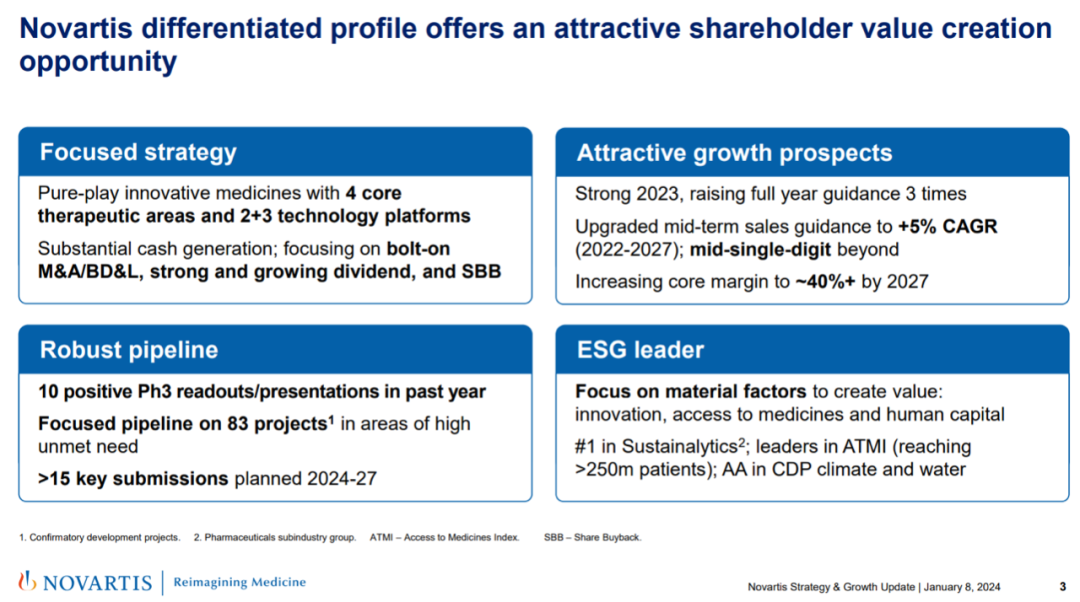

Novartis: Continuously Focused on Transforming into an Innovative Drug Company

At this year's JPM conference, Novartis' representative stated that the company aims to maintain its strategic focus on becoming a pure innovative pharmaceutical company. They believe this focused strategy will enhance profitability, support its small-scale mergers and acquisitions (M&A), business development and licensing (BD&L) strategies, sustain a strong and growing dividend, and continue its share buyback program (SBB), offering shareholders attractive value creation opportunities.

In fact, Novartis' transformation journey has been traceable for some time. Before 2014, Novartis was a diversified pharmaceutical company with a broad portfolio spanning multiple areas, including generics, ophthalmology, and innovative drugs. Starting from 2018, the company began streamlining its business structure by first spinning off its ophthalmology division, Alcon. Later, in 2022, it started divesting its generics business, Sandoz. With the spin-off of Sandoz in 2023,

Apart from divesting non-core businesses, Novartis has also been continuously implementing its transformation and development strategy. Since its transformation in 2018, Novartis has conducted share repurchases exceeding $32 billion, including a significant $15 billion share repurchase plan that began in July 2023. It is reported that approximately $13 billion in repurchases are still pending execution. Additionally, investments in value-creating small-scale mergers and acquisitions have surpassed $33 billion. Today, Novartis has become a company focused on innovative therapies, which has enabled the company to concentrate its efforts and resources on advancing the research and development of its core innovative business.

On the other hand, Novartis also emphasized at this conference its focus on four core therapeutic areas: cardiovascular-renal-metabolic, immunology, neuroscience, and oncology. This strategic direction is reflected in Novartis' $3.2 billion acquisition of Chinook to strengthen its capabilities in kidney disease. It is reported that Novartis is in the late stages of negotiations to acquire Cytokinetics. Additionally, Novartis acquired Calypso, the autoimmune spin-off subsidiary of Merck KGaA, for an upfront payment of $250 million, with a potential additional payment of $175 million. This move is part of Novartis’ strategy to enhance its portfolio in key therapeutic areas.

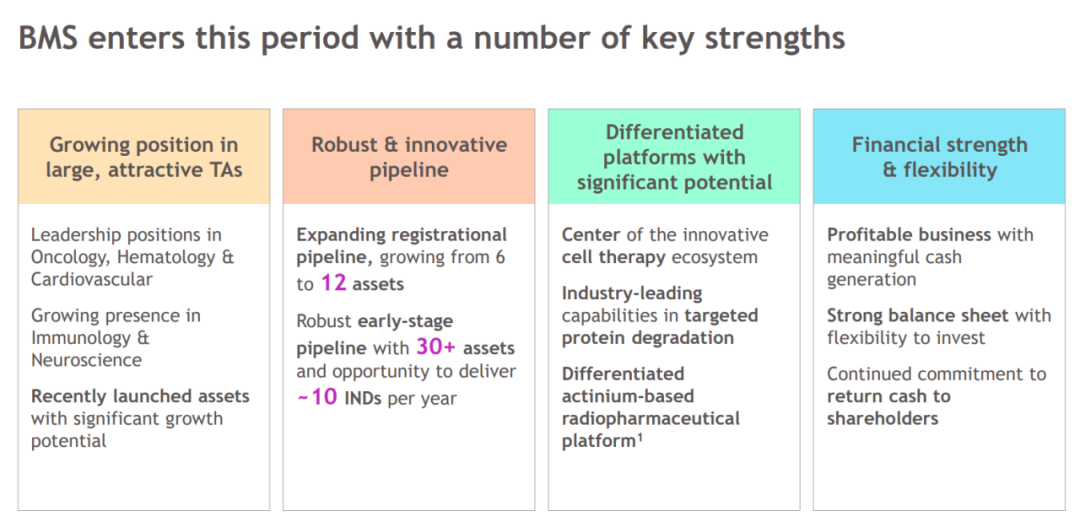

BMS: Strengthening Layout in Neurology and Oncology

Based on the presentation, BMS aims to maintain its leading position in oncology, hematology, and cardiovascular fields, while continuing the growth momentum in immunology and neuroscience. The company plans to expand its registration pipeline from 6 to 12. It will possess over 30 high-value early-stage assets and sustain an annual submission rate of approximately 10 INDs.

From the acquisitions over the past year, BMS has strengthened its patent portfolio in neurology and oncology through deals totaling approximately $35 billion. In December 2023, BMS announced two major acquisitions in quick succession. One of these was a deal with Karuna Therapeutics worth up to $14 billion. Karuna’s core product, the muscarinic antipsychotic drug KarXT, has been submitted for market approval in the United States. If approved, KarXT will become the first drug with a novel pharmacological mechanism for treating schizophrenia in decades. The other acquisition involved purchasing radiopharmaceutical biotech company RayzeBio for $4.1 billion, which will expand BMS's oncology pipeline. This move also set a new record for the highest acquisition amount in the radiopharmaceuticals sector.

BMS New Leader Chirs Boerner Says Over 16 New Products Could Be Launched by 2030. "Almost all of these products are first-class," Boerner said, "It is these pipelines that support the growth opportunities we see in the second half of this century." Meanwhile, Boerner added that with the completion of mergers and acquisitions, BMS’s business development focus will be on "licensing opportunities, partnerships, and complementary opportunities." Regarding immediate challenges, Boerner expressed optimism about the supply issues faced by the company with its CAR-T therapy Breyanzi, stating that measures have been taken to expand production capacity.

Pfizer: Strengthening Acquisition Value, Seeking New Growth

In 2023, as the market boom had passed, Pfizer found it difficult to replicate the opportunistic success it had achieved over the past three years due to market conditions. However, supported by the strong cash flow accumulated during this period, Pfizer has been aggressively "shopping" in the past two years. Through a series of mergers and acquisitions, Pfizer has strengthened its pipeline and product portfolio capabilities. Notably, Pfizer's $43 billion acquisition in 2023 set a new record for mergers and acquisitions in the pharmaceutical industry. This move also marked an important step for Pfizer to enhance its competitiveness by entering the ADC sector.

On the other hand, Pfizer also hopes to strengthen its competition with GSK in the RSV field. Last year, the RSV vaccines from both companies were approved in May, but GSK's Arexvy performed better in the market (sales in the first three quarters of 2023: $860 million vs. $375 million), with Pfizer’s product holding only 35% of the overall market share. "This is not the performance Pfizer should have, and we will take it back," Albert Bourla declared firmly.

Moreover, as a currently booming weight-loss track, Pfizer seems to hope to "get a piece of the action." Although there has been recent news of the failure of its weight-loss product, Pfizer CEO Albert Bourla still stated at the conference that the obesity drug market is an area where Pfizer can compete and win, and the company must be involved. However, since the company spent $43 billion acquiring Seagen in 2023, considering the reduction of debt costs, it is unlikely to consider acquiring late-stage obesity drugs with high price tags. Nonetheless, Bourla said that Pfizer is actively seeking potential licensing deals or acquiring early-stage obesity therapies.

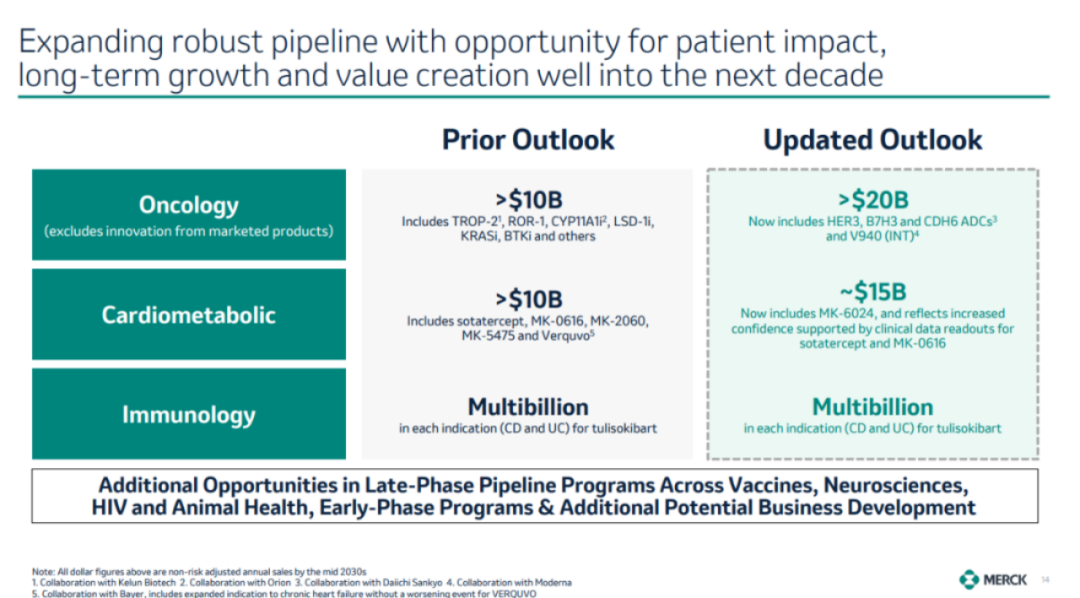

MSD: Embracing ADC, Actively Addressing the Patent Cliff of Keytruda

In 2023, MSD's Keytruda successfully claimed the throne as the world's top-selling drug, earning the title of "blockbuster drug king." However, as time progresses, the expiration of Keytruda's patent protection is drawing nearer for MSD. Once it loses patent protection, Keytruda will likely face performance pressures under the impact of generic drugs, similar to previous "drug kings."

But CEO Rob Davis said the future will focus on minimizing the decline in operations and restoring growth as soon as possible. "I know that the discussion at this stage is still focused on Keytruda and 2028," Davis said, "but we are increasingly looking beyond 2028—it's just a year." At this year’s JPM conference, Davis highlighted the company's promising pipeline assets, including three antibody-drug conjugates introduced from Daiichi-Sankyo: patritumab deruxtecan, ifinatamab deruxtecan, and raludotatug deruxtecan, as well as a cancer vaccine developed in collaboration with Moderna. Among them, patritumab deruxtecan received priority review from the FDA in December 2023 for third-line treatment of EGFR-mutated non-small cell lung cancer.

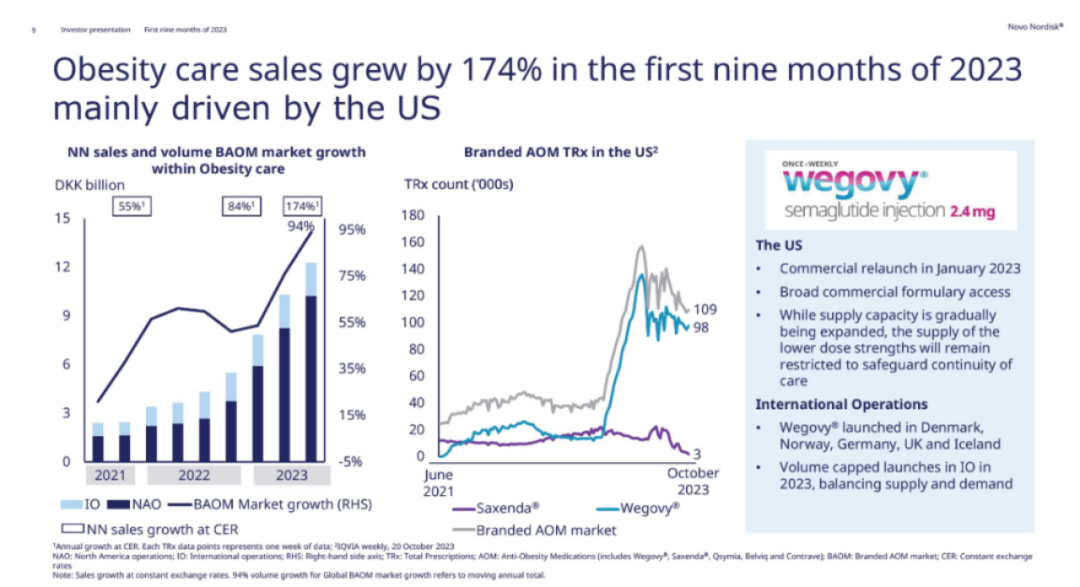

Novo Nordisk: Expansion in the Obesity Market Has Just Begun

When it comes to diabetes and weight loss, Novo Nordisk is undoubtedly one of the key giants in this field. With over 25 years of research and accumulation, Novo Nordisk has largely demonstrated their understanding of the mechanisms of obesity. Even after opening up a multi-billion-dollar market, Lars Fruergaard Jørgensen, CEO of Novo Nordisk, confidently stated, "We are just getting started."

Although the growth of the obesity product semaglutide injection Wegovy slowed down shortly after its launch due to capacity issues, Jørgensen stated that the company will further increase the product's supply capability in 2024 and continue to optimize capacity construction in the future.

To further expand its leading position in the obesity management field, Novo Nordisk initiated a frenzy of acquisitions at the end of 2023, continuing this momentum into early 2024. Following the $1.3 billion acquisition of Singapore-based biotech company KBP Biosciences in October 2023, Novo Nordisk entered into research collaboration agreements with U.S.-based biotech startups Omega Therapeutics and Cellarity in January 2024, with each collaboration potentially reaching a total value of up to $532 million.

It is reported that the acquisition of Omega is expected to enhance Novo Nordisk's potential new therapies for obesity management, replacing traditional appetite-suppressing treatments; the collaboration with Cellarity aims to uncover novel biological drivers associated with metabolic dysfunction-related fatty liver disease (MASH) and will leverage Cellarity’s platform to develop small-molecule therapies targeting the condition.

AstraZeneca: Strategic Goals Aim at 2030

At the 2024 JPM Conference, AstraZeneca's Chief Financial Officer (CFO) delivered a well-prepared speech as a representative, highlighting that AstraZeneca has set its strategic goals on a longer-term vision for 2030. Building on the overarching objective of achieving "industry-leading growth," the company aims to rank among the top three in several key areas: oncology, cardiovascular, renal, and metabolism (CVRM), respiratory and immunology (R&I), vaccines and immune therapies (V&I), as well as rare diseases.

To implement this corporate strategic goal, AstraZeneca has recently expanded its brand influence in the field through a series of mergers, acquisitions, and collaboration deals. First, in November 2023, it spent $185 million, along with up to $1 billion in future milestone payments, to reach a licensing agreement with Eccogene, bringing Eccogene’s GLP-1 product under its wing, helping AstraZeneca gain a share in the currently booming obesity market.

In addition, the company has also acquired vaccine manufacturer Icosavax to help shift its focus toward the emerging growth market of respiratory syncytial virus (RSV). After acquiring Icosavax, AstraZeneca can further expand its product coverage in the RSV field and strengthen its vaccine pipeline R&D capabilities through its RSV and human metapneumovirus (hMPV) vaccine portfolio, IVX-A12, along with Beyfortus, an immunization antibody for infants developed in collaboration with Sanofi. This will also alleviate AstraZeneca's currently limited vaccine portfolio.

Eli Lilly: Further Expand GLP-1 Extended Coverage

At this year's JPM conference, Eli Lilly's CEO David Ricks stated: "Eli Lilly and Novo Nordisk have been competing in the same field for about 100 years. We know each other well, and they are a respectable competitor. Such competition is beneficial for accelerating the development of both companies and expanding into more disease areas. A typical example is that Novo Nordisk explored the weight-loss effects of high-dose GLP-1, which drew our attention to another market opportunity for GLP-1 beyond lowering blood sugar levels — weight loss. Meanwhile, Eli Lilly has also been actively promoting its practical applications."

Mentioning the diabetes and obesity management market, the "fateful" battle between Eli Lilly and Novo Nordisk has always drawn significant industry attention. As GLP-1 products continue to evolve, from liraglutide to today's semaglutide, Eli Lilly’s tirzepatide is also eyeing the market aggressively. Besides Novo Nordisk, a group of major pharmaceutical companies are also trying to enter the field through mergers and acquisitions or newly developed GLP-1 products. The strength of these players cannot be underestimated either, as the field is witnessing a cyclical drama akin to "the mantis stalking the cicada, unaware of the oriole behind," with new products ready to take over at any time.

But Eli Lilly stated that obesity is actually a disease that affects the whole body, with conditions such as cardiovascular disease risk, obstructive sleep apnea (OSA), and non-alcoholic steatohepatitis (NASH) being potential complications. Therefore, there is still a significant clinical need in the weight loss field, and its market potential is an "unbounded blue ocean." David Ricks commented: "Eli Lilly and Novo Nordisk are not competing for a cake of fixed size, but are continuously expanding the application of GLP-1 in other disease areas."

GSK: Continued Investment in Respiratory Field

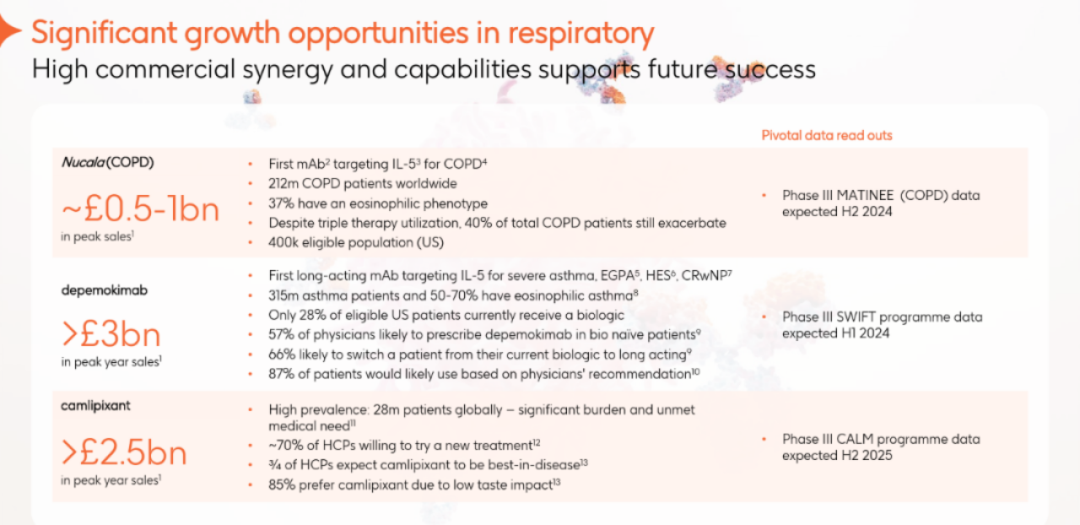

As one of the giants in the respiratory disease field, GSK continues to deepen its efforts in this area. On the basis of independent research and development, the company is also continuously acquiring potential blockbuster pipelines. In April 2023, GSK acquired BELLUS Health for $2 billion, bringing Camlipaxant, a P2X3 receptor antagonist selected for the treatment of refractory chronic cough, into its portfolio. On the other hand, in this field, Merck's Gefapixant was rejected again by the FDA, slowing down competitive pressure on the product. The company also predicted that Camlipaxant’s peak annual sales might reach $2.5 billion.

On January 9, GSK (GlaxoSmithKline) announced on its global official website that it had reached an acquisition agreement with Aiolos Bio, a clinical-stage biopharmaceutical company. The acquisition will involve an upfront payment of $1 billion and milestone payments of up to $400 million. GSK stated that this acquisition gives GSK access to Aiolos’ candidate drug, AIO-001. Notably, AIO-001 was originally licensed by Aiolos Bio from Hengrui Medicine.

Regarding GSK's proprietary pipeline, as one of the key "players" in the COPD field, its IL-5 monoclonal antibody Mepolizumab (brand name: Nucala) is currently conducting the Phase III MATINEE study for the treatment of COPD. GSK CEO Emma Walmsley stated, "If the MATINEE study yields positive results in the second half of 2024, the peak annual sales of Nucala will increase by $500 million to $1 billion."

At the same time, GSK's another long-acting IL-5 monoclonal antibody, depemokimab, will also unveil its Phase III study data in the first half of 2024. The initial indication for this product is eosinophilic asthma. Emma Walmsley believes that the peak annual sales of depemokimab could exceed $3 billion, much higher than the forecast in 2021 ($1 billion to $2 billion), adding new momentum to GSK's growth.

Daiichi Sankyo: Continues to Lead the ADC Track Trend

As a pioneer in the ADC field, Daiichi Sankyo has been delivering positive news at the start of 2024. First, its developed DS-8201 was proposed by the CDE for Breakthrough Therapy Designation to treat HER2-mutated, unresectable or metastatic non-small cell lung cancer in patients who have received at least one prior systemic therapy. Then, it was announced that the CDH6 ADC DS-6000 developed by the company received clinical approval in China for treating platinum-resistant high-grade ovarian cancer, primary peritoneal cancer, or fallopian tube cancer in patients who have undergone at least one prior line of systemic anticancer therapy.

According to the information disclosed by Daiichi Sankyo at the JPM conference, its total revenue for 2023 is expected to reach 1.55 trillion yen (approximately $10.66 billion), representing a 21.2 percentage point increase compared to 2022. The highest revenue proportion comes from Japan at 36.9%, followed by North America at 28.9%. In terms of product contributions, the main drivers are currently two products: HER2 ADC DS-8201 and the Factor Xa inhibitor Edoxaban.

Daiichi Sankyo has designed multiple ADCs through its Dxd ADC technology platform, targeting cancer cells expressing specific cell surface antigens and delivering payloads to specific targets. Currently, Daiichi Sankyo is primarily focused on the development of five ADCs, referred to as the 5Dxd ADCs: the HER2 ADC DS-8201 (Enhertu), which has been approved for marketing and is still expanding into other indications; the TROP2 ADC Datopotamab; the HER3 ADC Patritumab; and the relatively early-stage B7-H3 ADC DS-7300 and CDH6 ADC DS-6000. Notably, DS-8201 and Datopotamab are co-developed by Daiichi Sankyo and AstraZeneca.

On the other hand, in October 2023, Daiichi Sankyo reached global development and commercialization agreements with Merck for three additional ADC candidates under research, with a potential total deal value of up to 22 billion USD across the three projects. It is evident that Daiichi Sankyo has achieved significant "success" in both financial and business development aspects.

In addition to ADC products, Daiichi Sankyo also has a series of innovative R&D pipelines such as the EZH1/2 inhibitor Valemetostat, the FLT3 inhibitor Quizartinib, and the CD47 antibody DS-1471. Among them, Valemetostat monotherapy has demonstrated remarkable clinical efficacy in the treatment of peripheral T-cell lymphoma (PTCL). The latest data from its pivotal Phase II clinical trial disclosed at the 2023 ASH showed an ORR as high as 43.7% and a median DOR of 11.9 months. Additionally, Quizartinib became the first FLT3 inhibitor approved for use in combination with chemotherapy for the treatment of newly diagnosed FLT3-ITD (+) acute myeloid leukemia (AML) across all stages (induction, consolidation, and maintenance).

It can be said that, based on its ADC foundation, Daiichi Sankyo is continuously exploring new mechanisms and innovative product layouts. Through deepened cooperation with multinational corporations (MNCs), the company is driving comprehensive innovation, diversification, and sustainable development.

www.yyjjb.com.cn

Insight into Industry Trends

"Pharmaceutical Economy Herald"

Academic Official Account

Focus on the Frontiers of Oncology Academia

Terminal Official Account