AbbVie and BMS Bet $23 Billion on a Single Target: The Rise of Muscarinic Agonists in Neuropsychiatry

Karuna Therapeutics

Developer of Treatment Drugs for Mental and Neurological Disorders

AbbVie

Innovative Drug Developer

Bristol-Myers Squibb

Biopharmaceutical and Nutritional Product R&D and Sales

Cerevel

Biopharmaceutical Manufacturer

Just before the end of 2023, AbbVie Inc. reached a deal agreement with Cerevel Therapeutics, LLC to acquire all its outstanding shares at $45.0 per share, with a total value of approximately $8.7 billion. Merely two weeks later, Bristol-Myers Squibb Company and Karuna Therapeutics, Inc. entered into a definitive agreement, with BMS acquiring Karuna at a 53.35% premium per share, amounting to a total transaction value of approximately $14 billion.

Notably, both Cerevel and Karuna are dedicated to the development of drugs in the neuroscience field, with their core pipelines focusing on muscarinic agonists. AbbVie has long been deeply involved in the autoimmune sector, while BMS has continuously concentrated its efforts in the oncology field. At the end of 2023, both companies unexpectedly made significant investments in a new area, targeting the same point. What exactly are AbbVie and BMS planning to do?

The two companies that were acquired did not have any products on the market, and their core assets were all in the research pipeline.

Cerevel, acquired by AbbVie, was founded in 2018 as a spin-off of Pfizer's neuroscience assets in collaboration with Bain Capital. In 2020, Cerevel went public through a merger with the SPAC Arya Sciences. Currently, Cerevel has disclosed five pipeline products that have entered clinical stages.

The leading pipeline is Tavapadon, a selective partial agonist targeting the dopamine D1/D5 receptor subtypes. Three Phase 3 trials and an extension trial for Parkinson's disease are currently underway. Data is expected to be released gradually in 2024.

However, Tavapadon is not Cerevel's core asset. Emraclidine, a highly selective muscarinic M4 positive allosteric modulator (PAM), is considered Cerevel's most valuable asset. It is a potential Best-in-Class drug and next-generation antipsychotic for the treatment of schizophrenia.

BMS's acquisition of Karuna centers on its core pipeline, KarXT (xanomeline-trospium), an oral M1/M4 muscarinic acetylcholine receptor agonist, which is being developed for the treatment of schizophrenia and as an adjunctive treatment for psychosis in Alzheimer's disease.

Currently, the medications used for schizophrenia, whether typical antipsychotics such as haloperidol and chlorpromazine or atypical antipsychotics like risperidone and olanzapine, primarily rely on direct action on dopamine receptors or serotonin receptors. While they can effectively improve the positive symptoms of the disease, their effects on negative symptoms and cognitive symptoms are limited. Additionally, these medications come with side effects, presenting certain limitations in their use. Patient compliance tends to be low, and there is a characteristic high relapse rate.

Therefore, from a clinical perspective, schizophrenia is a market worth betting on.

KarXT adopts a new pharmacological mechanism and does not directly block dopamine receptors, representing a novel therapy for schizophrenia.

Currently, KarXT is in the regulatory review stage, with the PDUFA date set for September 26, 2024. Due to its more advanced progress, the transaction price this time is higher. Notably, Zai Lab holds the rights to KarXT in Greater China and has already received clinical approval in China after obtaining the license from Karuna Therapeutics.

Two multinational pharmaceutical giants spent $23 billion on acquisitions, with muscarinic receptors as the core assets. What makes them so attractive?

"Red umbrella, white stem" muscarine becomes a hope for schizophrenia.

Some mushrooms contain trace amounts of muscarine, which primarily acts on the parasympathetic nervous system and is classified as a neurotoxin. The English initial letter of muscarine is "M," so muscarinic receptors are also abbreviated as M receptors. There are five subtypes of M receptors (M1 to M5). M receptors are present in cardiac muscle, skeletal muscle, smooth muscle, and glandular cells. Therefore, muscarine poisoning can lead to a series of clinical symptoms such as bradycardia, breathing difficulties, vomiting, diarrhea, and fecal incontinence.

As early as the 1990s, research demonstrated that stimulating muscarinic receptors, particularly the M1 and M4 receptors, could alleviate psychotic symptoms and cognitive impairments. However, due to the non-selective stimulation of muscarinic receptors in both the central nervous system and peripheral tissues by muscarinic receptor agonists, which caused severe side effects, and the inability at the time to find a method for targeted, specific modulation of M receptors in tissues, drug development was hindered and ultimately shelved.

KarXT, as a compound drug, consists of Xanomeline and Trospium, the former being an agonist of the M1 and M4 subtypes, and the latter an antagonist of the M receptor.

Xanomeline was initially used to treat cognitive issues in Alzheimer's patients. Later clinical studies found it also effective for psychiatric symptoms. However, it simultaneously activates M receptors in the gastrointestinal system, causing side effects. Trospium, a broad-spectrum M receptor antagonist used to treat overactive bladder, has a structure that makes it difficult to cross the blood-brain barrier into the brain. Therefore, it can be combined with Xanomeline to inhibit the excessive activation of muscarinic receptors in peripheral tissues while Xanomeline takes effect, minimizing peripheral toxicity and controlling side effects.

Emraclidine, developed by Cerevel, takes a different approach as a novel, highly selective M4 receptor positive allosteric modulator (PAM). It exhibits high specificity for M4 and shows no significant agonistic effect on M1, thus eliminating the need to simultaneously block peripheral M1 receptors. Therefore, Emraclidine is also referred to by Cerevel as a next-generation psychiatric drug with BIC potential.

The Lancet published the results of a Phase 1b clinical trial of Emraclidine. The study showed that, after 21 days, the PANSS total score decreased by an average of 14.2 points in the 30mg once-daily dose group and by an average of 9.22 points in the 20mg twice-daily dose group, compared to an average decrease of 5.60 points in the placebo group. Compared with the placebo, the 30mg once-daily and 20mg twice-daily dose groups had a reduction of 30% or more in PANSS scores.

Not only Emraclidine and KarXT, but muscarinic receptor agonists are becoming a popular target for psychiatric disorders.

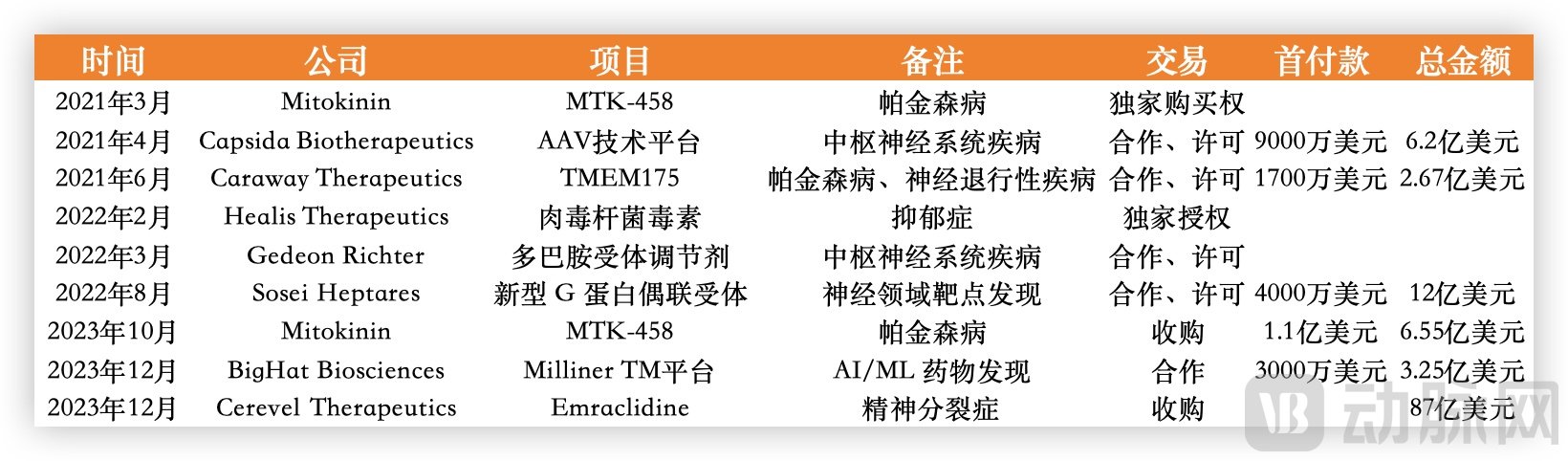

As an example, NBI-1117568, an oral selective muscarinic M4 receptor agonist developed by Sosei Heptares, entered into a collaboration and licensing agreement between Sosei and Neurocrine on November 22, 2021. Under this agreement, Neurocrine obtained the rights to develop and commercialize Sosei’s drug candidates intended for the treatment of major neurological disorders. Currently, NBI-1117568 has advanced to Phase 2 clinical trials. In addition, Neurocrine is also developing another oral muscarinic M1/M4 selective dual agonist, NBI-1117570.

Neumora's NMRA-266, currently in Phase 1 clinical trials, is also a highly selective positive allosteric modulator of the M4 receptor.

As a leading pipeline, KarXT has achieved relatively ideal results in multiple clinical trials. In a Phase 2 clinical trial named EMERGENT-1, 182 patients with schizophrenia were divided into a control group and a KarXT treatment group. At the time of grouping, the PANSS score for the KarXT treatment group was 97.7, and after 5 weeks of treatment, it decreased by 17.4 points; in contrast, the control group only dropped by 5.9 points, showing a significant difference between the two groups. In the Phase 3 clinical trial EMERGENT-2, the KarXT treatment group decreased by 21.2 points, while the control group decreased by 11.6 points; comparing the two groups, the treatment group showed an additional reduction of 9.6 points, with a significant difference.

With the aging of the population and changes in lifestyle across society, the incidence of neurological diseases will continue to rise in the future, and market demand in the field of neuroscience will also grow steadily. For schizophrenia, a chronic mental illness, it has been decades since a drug with a new mechanism emerged. The advent of new drugs not only holds commercial value but also significant social value.

The core reason for the two major pharmaceutical companies' simultaneous efforts in the same field lies in their constrained performance.

First to make a move, AbbVie's core product Humira, after holding the "top drug" crown for many years, has finally faced patent expiration. In the first three quarters of 2023, its revenue was $11.1 billion, marking a 29% year-on-year decrease. Although AbbVie hopes that Skyrizi and Upadacitinib can take over Humira’s role in the autoimmune field, these products cannot shoulder such a heavy responsibility in the short term. Therefore, towards the end of 2023, AbbVie made moves to expand its pipeline with nearly $20 billion.

BMS seems to be more determined, starting with a $14 billion investment, showing a sense of overtaking from behind. From the financial report, it's not hard to see the reasons. According to the Q3 2023 financial data, BMS's revenue for the quarter was approximately $11 billion, a year-on-year decrease of 2%. This marks the fifth consecutive quarter of declining performance for BMS from Q3 2022 to Q3 2023.

As the core products accounting for the majority of BMS's revenue, Eliquis and Opdivo, two cardiovascular and oncology drugs, generated revenues of $9.332 billion and $6.622 billion respectively in Q1~Q3 2023, representing year-over-year growth of only 2.54% and 9.76%. In contrast, their growth rates were 12.48% and 9.0%, respectively, during the same period in 2022.

The slowdown in the growth of core products has led both AbbVie and Bristol-Myers Squibb to seek breakthroughs beyond their traditional areas of strength.

The reason for choosing the neuroscience field is not without aim. Take AbbVie as an example: although the autoimmune sector, despite its decline, remains the primary source of revenue, declines have occurred in areas such as oncology, aesthetics, and ophthalmology. The only sector showing growth is neuroscience, with a year-on-year increase of 16.7%.

AbbVie's Revenue Situation for the First Three Quarters of 2023, Data from Corporate Earnings Reports

Such achievements would not have been possible without AbbVie's long-term strategic layout in the neuroscience field. For instance, in 2019, AbbVie acquired Allergan for $63 billion, which not only strengthened its position in the medical aesthetics sector but also brought key neuroscientific products such as BOTOX, Vraylar, and Ubrelvy into its portfolio. In the first three quarters of 2023, AbbVie’s neuroscience division generated $5.623 billion in revenue, with these three drugs accounting for approximately 85% of that total. This performance allowed the neuroscience division to surpass oncology and become the second-largest revenue source after immunology.

AbbVie's Layout in the Neurology Field Over the Past Three Years, Data Compiled from Public Information

Although in the field of psychiatric drugs, there is only one major product, Vraylar, and only ABBV-932 in the pipeline for bipolar disorder, the acquisition of Cerevel brings not only Emraclidine, which has Best In Class potential, but also supplements to the rest of the psychiatric drug pipeline.

At the same time, AbbVie's investment in psychiatric drugs is continuously increasing. AbbVie's Chief Commercial Officer Jeffery Stewart stated in a December investor conference call, "We have put significant effort into marketing Vraylar, spending $13.1 million solely in November on DTC advertising for the drug, as DTC is becoming a more efficient promotional method as the stigma surrounding mental health gradually diminishes."

Of course, this acquisition of Cerevel will not help AbbVie's revenue in the short term. Its CEO also stated at the investor conference that this acquisition is mainly for future consideration, and the performance brought by the acquisition is more about the next decade.

Bristol-Myers Squibb's 17 marketed drugs, source: company earnings report

Relatively speaking, BMS's layout in the neurology field is still in its early stages. Based on the indications of the 17 marketed drugs disclosed in its financial report, there are no corresponding products. However, the new generation JAK inhibitor autoimmune drug Sotyktu developed by BMS, which targets TYK2, has already begun to be applied in the neurology field.

In January 2024, American company Myrobalan Therapeutics announced the completion of a $24 million Series A financing round, with one of its core pipelines being a TYK2 allosteric inhibitor aimed at reducing neuroinflammation. Just a month earlier, in December 2023, Sudo Biosciences completed a $116 million Series B financing round, with funds to be used for advancing two TYK2 pipelines targeting neurodegenerative diseases into clinical trials.

Sudo’s project is a potential first-in-class, best-in-class brain-penetrant TYK2 inhibitor, with promise for the treatment of relapsing and multiple sclerosis as well as neurodegenerative diseases such as Alzheimer's disease and amyotrophic lateral sclerosis (ALS). Currently, in China, there are also BHV-8000 (Phase 1 clinical trial) by HiLight Pharmaceutical and WD-910 (preclinical) by Wenda Medicine involved in this field.

Emerging Biotechs Start Targeting TYK2 at the Nervous System, and BMS Will Naturally Not Stand Idly By. From This Perspective, BMS’s Acquisition of Karuna Is Not Only About KarXT Itself but Also Values the Capabilities Cultivated Through Years of Deep Expertise in the Neurology Field.

As early as 2012, Karuna acquired the ownership of Xanomeline from Eli Lilly. In 2016, Karuna initiated Phase 1 clinical trials for KarXT in the treatment of schizophrenia, which were completed in 2017. Since then, Karuna has continued to raise funds for Phase 2 clinical trials of KarXT. During the Series A financing round, Karuna brought in individual investor Steven Paul and appointed him as the company's CEO.

Steven Paul worked at Eli Lilly for 17 years, leading the company's development of the xanomeline project. In the following years, under Steven Paul’s leadership, KarXT advanced rapidly, and its New Drug Application was submitted in 2023. Over the next two years, Karuna will continue to complete multiple clinical safety studies for KarXT while initiating clinical trials for Alzheimer’s disease. In 2023, Karuna also entered into a licensing agreement with Goldfinch Bio to introduce GFB-887 for the treatment of mood and anxiety disorders.

Over the years, Karuna has built an excellent R&D team around its core pipeline in the neuroscience field and relevant clinical indications, achieving significant clinical progress and continuously increasing the value of its core assets. Since its initial public offering, Karuna's market value has risen from less than $7 billion to over $10 billion at one point, delivering approximately 45 times returns to investors in just a few years. The enormous potential Karuna has demonstrated in the neuroscience sector is also one of the reasons why Bristol-Myers Squibb is willing to spend $14 billion on the acquisition.

BMS CEO Stated at the Recently Concluded JPM Conference: The Company’s Pipeline Has Never Been This Robust. Over the Next Six Years, BMS Will Launch More Than 16 New Products, Most of Which Are FIC/BIC. This Extensive and Diversified Product Pipeline Will Become the Main Driver of BMS's Revenue Growth in the Next Decade.

The development journey of Cerevel and Karuna Therapeutics also sets an example for many biotech companies: to demonstrate their value, the key lies in diligently focusing on clinical needs, and impressing the market with outstanding clinical data, rather than hyping concepts or telling stories.

The entry of AbbVie and Bristol-Myers Squibb is just the beginning. Whether it is schizophrenia, Parkinson's disease, depression, or mood disorders, there are significant unmet clinical needs. The future market related to these conditions will be even more exciting.

A $23 billion entry in one month, psychiatric drugs begin to attract market attention.

The pathogenesis of psychiatric disorders is complex, and the difficulty of drug development is high. In the past decade, new drugs approved by the FDA for marketing have mainly focused on schizophrenia, severe depression, postpartum depression, attention deficit hyperactivity disorder, and bipolar disorder.

Not only AbbVie and Bristol-Myers Squibb, but also Novartis, Roche, Sumitomo, Merck and other multinational corporations (MNCs) have been making strategic moves in recent years. Multiple pharmaceutical companies have drugs in the late clinical stages, and in the near future, we may witness the launch of several new medications.

It is worth noting that the targets of these new drugs in the late stage of development are relatively concentrated, such as the serotonin receptor 5HT1 family and dopamine receptors for schizophrenia drugs, but there are also some new targets emerging. Whether it is the aforementioned muscarinic receptor agonists, or those related to NMDA receptor activation or targeting TAAR1, there are projects that have entered Phase 3 clinical trials.

Progress in the Development of Certain Psychiatric Drugs, Data from Public Information

According to Clinicaltrials data, in 2023 alone, there were 176, 187, 52, 94, and 74 clinical trial registrations initiated for schizophrenia, major depressive disorder, postpartum depression, attention deficit hyperactivity disorder, and bipolar disorder, respectively. Frost & Sullivan had predicted that the global neuroscience drug market size would grow from $160 billion in 2022 to $220 billion by 2028.

Due to the difficulty, high cost, and low success rate of central nervous system drug research and development, there have been few participants. However, with the entry of major companies and new therapies entering the late stages of development, this field is expected to burst with vitality in the future.

References:

DOI:10.3390/cancers3010971

DOI:10.1016/S0140-6736(22)01990-0

https://www.biospace.com/article/the-neuropsychiatric-pipeline-10-late-stage-therapies-to-watch-/