Cardiovascular Device Company Hanyu Medical Voluntarily Withdraws from STAR Market IPO

Hanyu Medical

Structural Heart Disease Interventional Devices and Electrophysiology Product R&D, Manufacturer

Pioneer in Medical Device Media Reports

Share Professional Medical Device Knowledge

On the evening of January 16,SSE Announces Decision to Terminate the Review of Shanghai Hanyu Medical Technology Co., Ltd.'s STAR Market IPO; Direct Cause is Company and Sponsor CICC Withdrawing Application/Sponsorship.The company's IPO application was accepted on March 1, 2023, and the first round of inquiries was received on March 24, with subsequent completion of the response.

Hanyu Medical is primarily engaged in the research, development, production, and commercialization of interventional devices for structural heart disease and electrophysiology products. The company’s predecessor, a limited company, was established in December 2016 and was restructured into a joint-stock company in December 2020. The company currently has a total share capital of 79,875,001 shares.

According to the prospectus disclosed in March 2023, the company complies with and meets Article 2.1.2 of the "Rules for the Listing of Sci-Tech Innovation Board Stocks on the Shanghai Stock Exchange."The listing standard stipulated in the first paragraph, item (v):"The estimated market value is no less than 4 billion yuan, and the main business or products need to be approved by relevant national departments, with a large market space and having achieved phased results. Pharmaceutical industry enterprises need to have at least one core product approved for Phase II clinical trials, and other enterprises that meet the positioning of the STAR Market need to have obvious technical advantages and meet corresponding conditions."And the company meets the specific requirements of the "Guidance No. 7 on the Application of the Listing Review Rules for the Sci-Tech Innovation Board of the Shanghai Stock Exchange — Application of the Fifth Set of Listing Standards for Medical Device Companies."As an innovative medical device R&D company planning to adopt the fifth set of listing standards, the company alerts investors to focus on the following characteristics and risks:

1. The core products of the company have not yet been marketed, the company has not yet made a profit and expects to continue to incur losses.

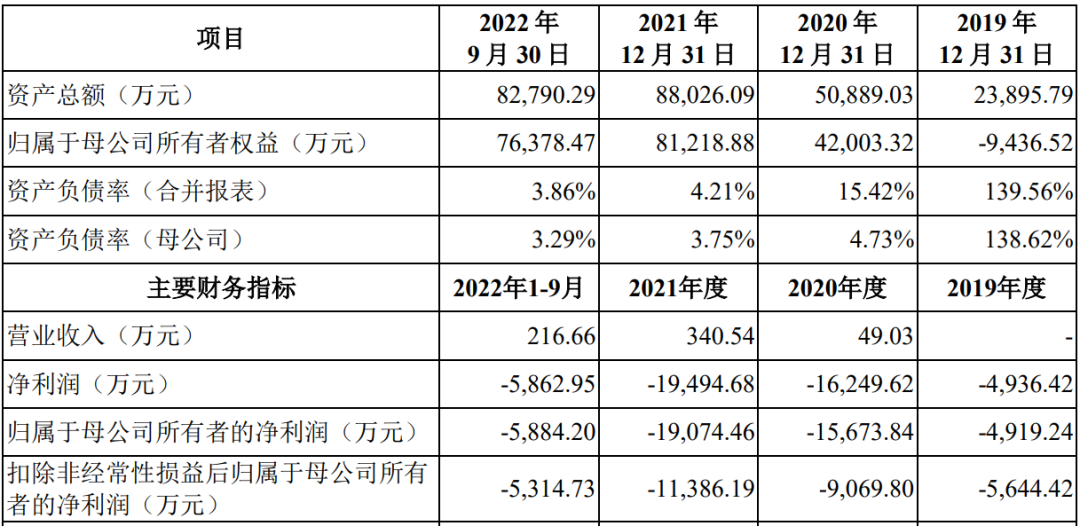

As of the date of this prospectus, the Company's core products have not been approved for marketing, and commercial production and sales have not commenced. The Company has not yet achieved profitability and has accumulated uncompensated losses. For the years 2019, 2020, 2021, and the period from January to September 2022, the net profit attributable to the Company's ordinary shareholders was -RMB 49.1924 million, -RMB 156.7384 million, -RMB 190.7446 million, and -RMB 58.8420 million, respectively.The net profit attributable to the parent company's ordinary shareholders after deducting non-recurring gains and losses was -RMB 56.4442 million, -RMB 90.6980 million, -RMB 113.8619 million, and -RMB 53.1473 million, respectively. As of the end of September 2022, the company's accumulated undistributed profit was -RMB 344.7114 million.For a period of time in the future, the company expects to have accumulated losses that have not been offset and will continue to incur losses.

2. The company anticipates the need for large-scale, ongoing R&D investment in the future.

During the reporting period, the Company invested a substantial amount of funds in preclinical research, clinical trials, and pre-market preparations for innovative medical devices. For the years 2019, 2020, 2021, and January to September 2022,The company's R&D expenses were 30.4044 million yuan, 43.7758 million yuan, 66.2875 million yuan, and 43.5518 million yuan, respectively.As of the date of this prospectus,The core product of the company, ValveClamp, is in the pre-market registration and approval stage, two products are in the clinical trial stage, and all other products are in stages prior to clinical trials.The Company will still need large-scale and continuous investment in R&D to support preclinical research, clinical trials, and marketing application for its pipeline products. For a period of time in the future, the Company expects to continue to incur losses, and the accumulated deficits will continue to expand.

During the reporting period, the company's main financial data are as follows:

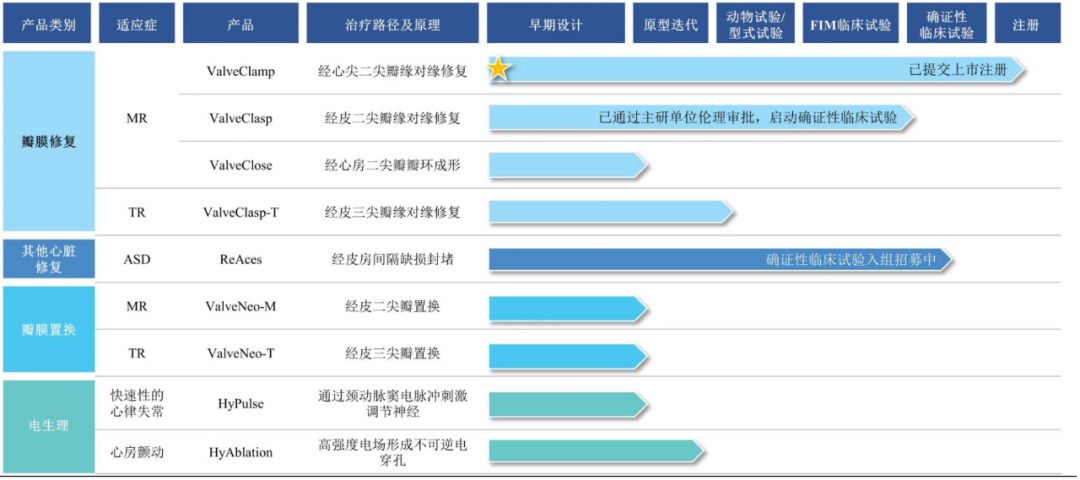

As of March 2023, the company's R&D product pipeline includes five innovative medical devices for repair targeting mitral regurgitation, tricuspid regurgitation, and congenital atrial septal defect, two innovative replacement medical devices respectively for mitral regurgitation and tricuspid regurgitation, and two electrophysiology products. The progress of the company’s product development is as follows:

The core products of the company include ValveClamp, ValveClasp, and ReAces, among which ValveClamp obtained its registration certificate in September 2023.

1. ValveClamp Mitral Valve Clip System (“ValveClamp”)

ValveClamp Mitral Valve Clip System is a transapical edge-to-edge mitral valve repair system developed by the company for interventional treatment of mitral regurgitation. ValveClamp utilizes a transapical approach, with a short distance from the device entry incision to the mitral valve, allowing the delivery system to be easily coaxial with the native valve. The position and angle of the device can be directly controlled, providing more sensitive and precise mechanical transmission, and convenient operation.The product's surgery can be completed in a regular operating room with ultrasound assistance, without the need for a DSA interventional operating room. This reduces the requirements for surgical equipment configuration while avoiding X-ray exposure for both patients and doctors.According to the results of the confirmatory clinical trial, the average catheter operation time for ValveClamp was only 24.88 minutes, with a short learning curve for doctors, significantly lower than other similar products already on the market globally.

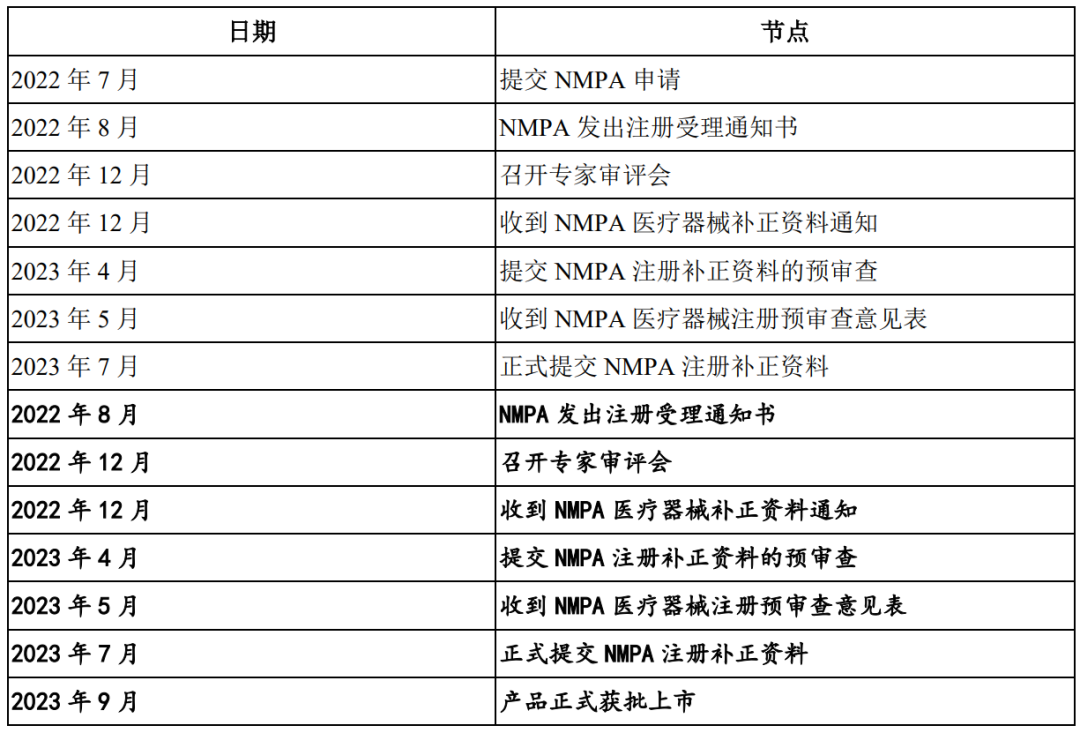

The registration application for ValveClamp has been completed, and the key event milestones are as follows:

During the entire process of communication with relevant departments such as the National Medical Products Administration and the Center for Medical Device Evaluation, the company did not receive any significant negative feedback, nor were there any major issues pending resolution or implementation. The main discussions revolved around the review process and supplementary materials. No significant adverse events occurred during the registration review process, and there were no key issues that would substantially impact the product's market launch.The product obtained its registration certificate in September 2023.

2. ValveClasp Percutaneous Mitral Valve Clip and Delivery System (“ValveClasp”)

The company, leveraging the technical experience accumulated from the development of the ValveClamp clip, has developed the ValveClasp product using a percutaneous approach. The ValveClasp product adopts a percutaneous access method and inherits the design concept of ValveClamp. It abandons the traditional rigid structure design and creatively uses a clamping arm with an elastic outer frame. It also solves the challenge of securely connecting the elastic frame to the rigid structure without interfering with the locking mechanism or increasing the diameter of the interventional catheter. This allows it to increase the clipping range, reduce the proportion of patients requiring two clips, and significantly lower surgical risks and costs.

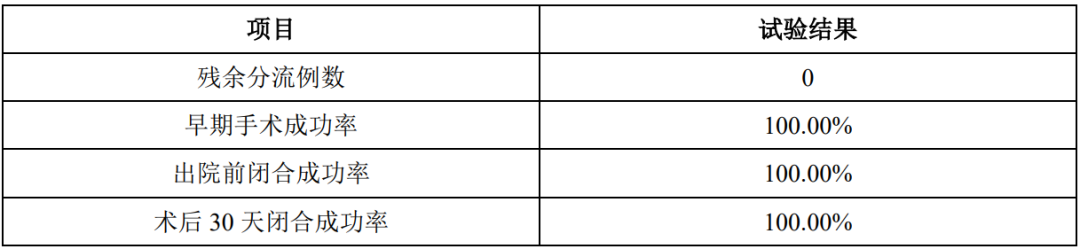

The issuer disclosed the interim clinical study reports of five FIM clinical trials in the prospectus, and the results showed that:

Due to the company's plan to relocate its production site to the Xinzhuang Industrial Zone in Minhang District in 2023, according to the requirements of the "ISO13485-2016 Quality Management System," production activities and the advancement of clinical trial phases can only continue after the completion of the production process change. Therefore, the company plans to continue advancing the confirmatory clinical enrollment for the ValveClasp product after the relocation of the production site.

(1) Enrollment Progress: As of March 31, 2023, the FIM clinical trial has completed enrollment of 5 cases. Currently, the company's ValveClasp has begun enrollment for the confirmatory clinical trial.

(2) Trial Data/Results Update: No relevant data updates

(3) Forecast of Subsequent Key Nodes and Arrangements

The product has applied for and passed the special review for innovative medical devices in March 2023, and its technological advancement has been fully recognized by relevant departments.

3. ReAces New Atrial Septal Defect Occluder ("ReAces")

ReAces, a novel atrial septal defect occluder developed by the company, is the world's first puncturable occluder. It retains the basic structure and working principle of the traditional occluder with "two discs and a waist" to ensure safe and effective occlusion. The central area of the occluder has no metal components and features a thin flow-blocking membrane design, which effectively blocks blood flow through the occluder while allowing for simple and feasible puncture and sheath delivery.

The issuer disclosed the interim report of the clinical study in the prospectus, and the results of its efficacy showed:

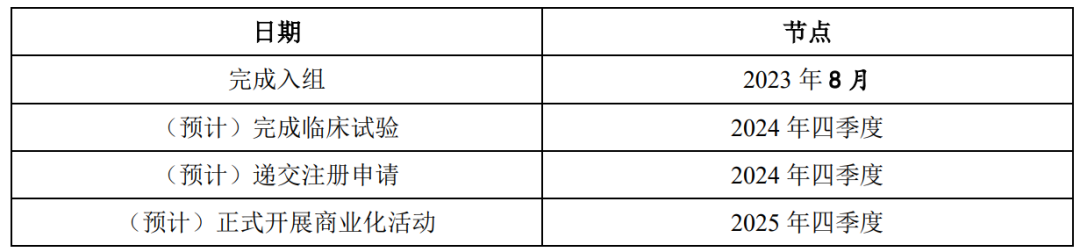

As of now, the specific progress of the clinical trials for the ReAces product is as follows:

(1) Enrollment Progress: As of August 2023, the company has completed all enrollment work for the ReAces product.

(2) Trial Data/Results Update: The FIM clinical trial for the product is still in the follow-up phase, with no data updates available yet; the confirmatory clinical trial completed enrollment in August 2023, and there are currently no data updates.

(3) Forecast of Subsequent Key Nodes and Arrangements

The company submitted an application for the special review of innovative medical devices in March 2023.

According to the disclosure, as of September 7, 2023, except for MitraClip and the company's ValveClamp, which have already been marketed,A total of 22 interventional devices for mitral regurgitation have entered the clinical trial stage.Including 17 repair devices and 5 replacement devices. The aforementioned products constitute competitors to the issuer's products.

Currently, the ex-factory price of MitraClip in China is about 210,000 yuan, and the expected ex-factory price of ValveClamp is about 100,000 yuan.

In the field of mitral valve, currently in China, only MitraClip and ValveClamp, developed by the company, were approved in June 2020 and September 2023 respectively.In 2022, the total number of surgeries was only 310, and transcatheter mitral valve intervention was still in the early stage of market introduction.

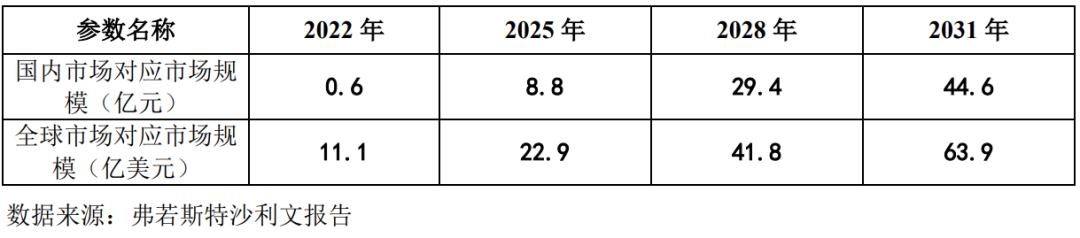

The core products of the issuer in the mitral valve repair field, ValveClamp and ValveClasp, both adopt the edge-to-edge technical approach. Their corresponding market potential is:

Accordingly, in 2022, the market size for mitral valve repair in China and globally was RMB 0.6 billion and USD 1.12 billion, respectively. By 2031, it is estimated that the market size for mitral valve repair in China and globally will reach RMB 4.53 billion and USD 6.456 billion, respectively.

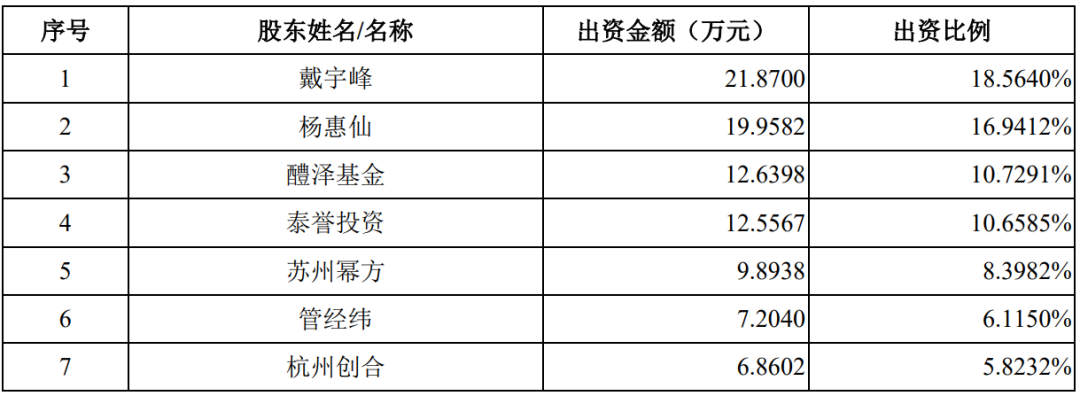

As of January 1, 2019, the company's registered capital was RMB 1,178,088 yuan, with 14 shareholders, as follows:

1. On May 28, 2019, Taizhou Mifang, Tibet Longmaid, Dongzheng Fuxiang, and the Transformation and Upgrading Mother Fund signed the "Equity Transfer Agreement," stipulating that Taizhou Mifang would transfer its 1.2230% equity in Hanyu Medical (corresponding to a registered capital of 14,408 yuan) to Dongzheng Fuxiang for 7.949491 million yuan, and Tibet Longmaid would transfer its 2.50% equity in the company (corresponding to a registered capital of 29,452 yuan) to the Transformation and Upgrading Mother Fund for 16.25 million yuan.

2. In July 2019, Panmao Shanghai signed the "Equity Transfer and Capital Increase Agreement" with Hanyu Medical and its shareholders. On July 8, 2019, Guan Jingwei, Taiyu Investment, Hangzhou Chuanghe, and Panmao Shanghai signed the "Equity Transfer Agreement." The aforementioned agreements stipulated that Panmao Shanghai would contribute RMB 150 million in cash to increase the capital of Hanyu Medical, of which RMB 176,713 would be included in the registered capital, and the remaining RMB 149,823,287 would be included in the capital reserve fund. The registered capital increased from RMB 1,178,088 to RMB 1,354,801. It was agreed that Guan Jingwei would transfer 2% of Hanyu Medical's equity (corresponding to a registered capital of RMB 23,562) to Panmao Shanghai for RMB 18 million; Taiyu Investment would transfer 2% of Hanyu Medical's equity (corresponding to a registered capital of RMB 23,562) to Panmao Shanghai for RMB 18 million; Hangzhou Chuanghe would transfer 3% of Hanyu Medical's equity (corresponding to a registered capital of RMB 35,343) to Panmao Shanghai for RMB 27 million.

3. On July 6, 2020, Panmao Shanghai, Xiamen Yuhui, Xiamen Qianshan, Dongzheng Guanlan, and Yang Huixian signed the "Equity Transfer Agreement," stipulating that Yang Huixian would transfer 1.75% equity (corresponding to a registered capital of 23,709 RMB) of Hanyu Medical to Panmao Shanghai for 24.5 million RMB; transfer 0.6563% equity (corresponding to a registered capital of 8,891 RMB) to Xiamen Yuhui for 9.1876 million RMB; transfer 0.2187% equity (corresponding to a registered capital of 2,964 RMB) to Xiamen Qianshan for 3.0629 million RMB; and transfer 0.8750% equity (corresponding to a registered capital of 11,854 RMB) to Dongzheng Guanlan for 12.2495 million RMB.

On the same day, Panmao Shanghai and Hetang Health signed the "Equity Transfer Agreement," stipulating that Hetang Health would transfer 0.6689% equity (corresponding to a registered capital of RMB 0.9062 million) of Hanyu Medical to Panmao Shanghai for RMB 9.3643 million; Dai Yufeng and Hetang Investment signed the "Equity Transfer Agreement," stipulating that Hetang Investment would transfer 0.6689% equity (corresponding to a registered capital of RMB 0.9062 million) of Hanyu Medical to Dai Yufeng for RMB 9.3643 million.

4. On July 19, 2020, Anji Qiyue entered into an "Capital Increase Agreement" with Hanyu Medical and its shareholders, stipulating that Anji Qiyue would contribute RMB 32.5 million in cash to subscribe for the newly increased registered capital of Hanyu Medical. Of this amount, RMB 71,305 was credited to the registered capital, and the remaining RMB 32,428,695 was credited to the capital reserve. The registered capital of Hanyu Medical increased from RMB 1,354,801 to RMB 1,426,106.

5. On July 30, 2020, Ganzhou Biyuewu and 13 other investors signed the "Equity Transfer and Capital Increase Agreement" with Hanyu Medical and its shareholders. At the same time, Ganzhou Biyuewu and the 13 other investors separately signed the "Equity Transfer Agreement" with shareholders such as Dai Yufeng, Guan Jingwei, and Lizze Fund. The agreements stipulated that Ganzhou Biyuewu and the 13 other investors would acquire a total of 161,087 yuan of capital contribution held by the original shareholders in Hanyu Medical for 248.5 million yuan. Additionally, they would invest 248.5 million yuan to increase the capital of Hanyu Medical, with the new registered capital of 126,567 yuan being subscribed by Ganzhou Biyuewu and the 13 other investors. The company's registered capital increased from 1,426,106 yuan to 1,552,673 yuan.

6. On October 26, 2020, Guan Jingwei, Suzhou Mifang, Yueyin Investment, Anji Curvature, Huzhou Jingxin, and Shanghai Jinci signed the "Equity Transfer Agreement." Guan Jingwei transferred 0.3280% of Hanyu Medical's equity (corresponding to a registered capital contribution of RMB 0.5093 million) to Huzhou Jingxin for RMB 10 million and transferred 2.2932% of Hanyu Medical's equity (corresponding to a registered capital contribution of RMB 3.5605 million) to Anji Curvature for RMB 38.984 million. Suzhou Mifang transferred 1.6402% of Hanyu Medical's equity (corresponding to a registered capital of RMB 2.5466 million) to Huzhou Jingxin for RMB 50 million, and Yueyin Investment transferred 0.9841% of Hanyu Medical's equity (corresponding to a registered capital contribution of RMB 1.5280 million) to Shanghai Jinci for RMB 30 million.

7. On March 4, 2021, Yunfeng Fund, Ruihua Capital, EF Hui Da, Pingxiang Yuhua, Suqian Lingdao, Ganzhou Jiaomujiao, Shanghai Jiedao, Oct Fund, Hanyu Medical, and the then-registered shareholders of Hanyu Medical signed the "Capital Increase Agreement for Shanghai Hanyu Medical Technology Co., Ltd." Yunfeng Fund, Ruihua Capital, EF Hui Da, Pingxiang Yuhua, Suqian Lingdao, Ganzhou Jiaomujiao, Shanghai Jiedao, and Oct Fund invested RMB 455 million in cash to subscribe for an additional registered capital of RMB 4,875,001 yuan. Specifically: Yunfeng Fund contributed RMB 200 million in cash to subscribe for an additional registered capital of RMB 2,142,857 yuan, with a premium of RMB 197,857,143 credited to the capital reserve fund; Ruihua Capital contributed RMB 65 million in cash to subscribe for an additional registered capital of RMB 696,429 yuan, with a premium of RMB 64,303,571 credited to the capital reserve fund; EF Hui Da contributed RMB 20 million in cash to subscribe for an additional registered capital of RMB 214,286 yuan, with a premium of RMB 19,785,714 credited to the capital reserve fund; Pingxiang Yuhua contributed RMB 55 million in cash to subscribe for an additional registered capital of RMB 589,286 yuan, with a premium of RMB 54,410,714 credited to the capital reserve fund; Suqian Lingdao contributed RMB 35 million in cash to subscribe for an additional registered capital of RMB 375,000 yuan, with a premium of RMB 34,625,000 credited to the capital reserve fund; Ganzhou Jiaomujiao contributed RMB 10 million in cash to subscribe for an additional registered capital of RMB 107,143 yuan, with a premium of RMB 9,892,857 credited to the capital reserve fund; Shanghai Jiedao contributed RMB 20 million in cash to subscribe for an additional registered capital of RMB 214,286 yuan, with a premium of RMB 19,785,714 credited to the capital reserve fund; Oct Fund contributed RMB 50 million in cash to subscribe for an additional registered capital of RMB 535,714 yuan, with a premium of RMB 49,464,286 credited to the capital reserve fund. Note: It is estimated that the post-investment valuation is approximately RMB 7.455 billion.

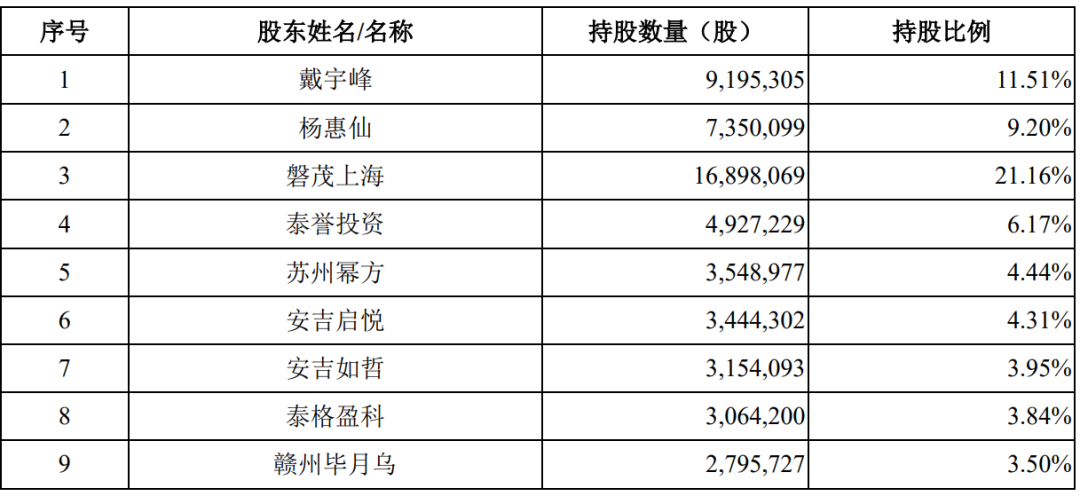

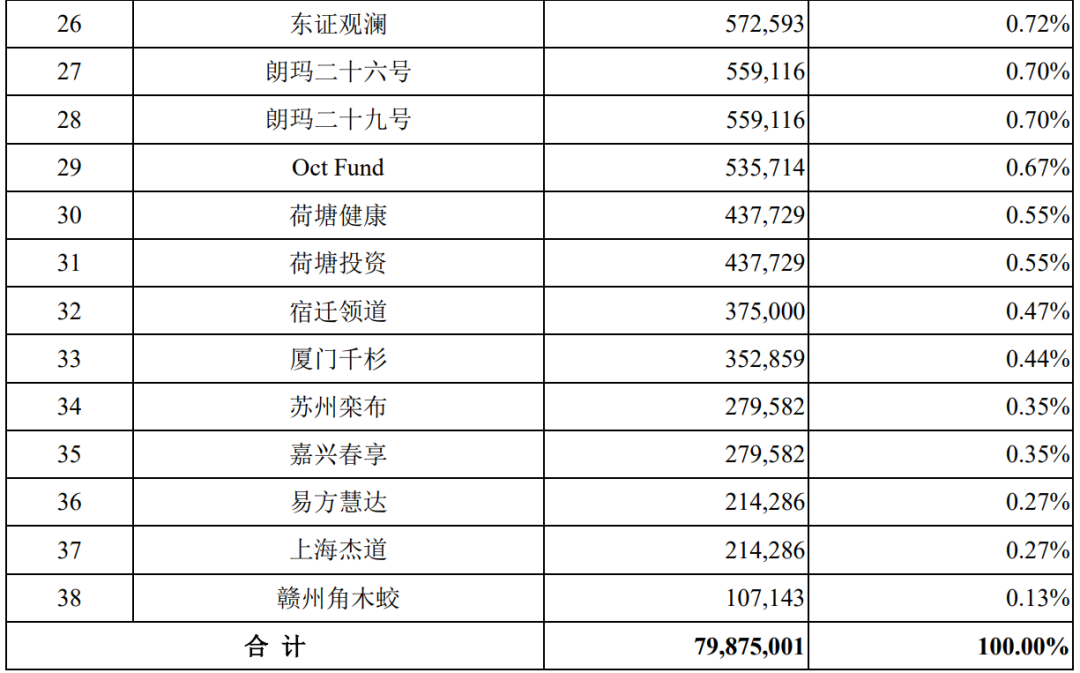

After the completion of this capital increase, the equity structure of Hanyu Medical is as follows:

1. Core Technology Source

According to the filing materials: 1) The issuer has acquired 12 invention patents and 16 utility model patents from Zhongshan Hospital, as well as 2 invention patents and 1 utility model patent from Wuxi Second People's Hospital. Some of these patent transfers did not provide internal hospital approval documents or failed to undergo public disclosure procedures; 2) The principle design of the issuer’s core products, the ValveClamp clip and the ReAces occluder, originated from innovations developed by Dr. Pan Wenzhi's team at Zhongshan Hospital during clinical practice. After acquiring the relevant patents, the issuer made significant improvements; 3) Pan Wenzhi, a core technical staff member of the issuer, is the Chief Physician at Zhongshan Hospital, the first inventor of the original ValveClamp patent, and one of the main inventors of the original ReAces patent. Since the establishment of Hanyu Medical, he has served as a clinical medicine advisor, signing an expert consultant employment agreement with the company and receiving remuneration for his services; 4) Apart from Pan Wenzhi, the issuer has five other core technical staff members working on the development of nine research products; 5) The issuer continues to collaborate with Zhongshan Hospital on medical-engineering projects. In September 2022, both parties signed the "Framework Cooperation Agreement" for a national medical center key project titled “Independent Intellectual Property Structural Heart Disease Device Innovation R&D,” with a contract value of 100 million yuan. Specific cooperation details will be agreed upon separately.

2. Regarding the Estimated Market Value

According to the filing materials, the issuer has chosen the fifth set of listing standards for the Sci-Tech Innovation Board (STAR Market) to file for listing. The sponsor institution used the market value/research and development (R&D) expenses multiple to evaluate the issuer. Based on the median of the market value/R&D expenses multiples of 10 comparable companies, multiplied by the average R&D expenses of the issuer during the reporting period, the estimated market value is approximately 5.77 billion yuan, not less than 4 billion yuan.

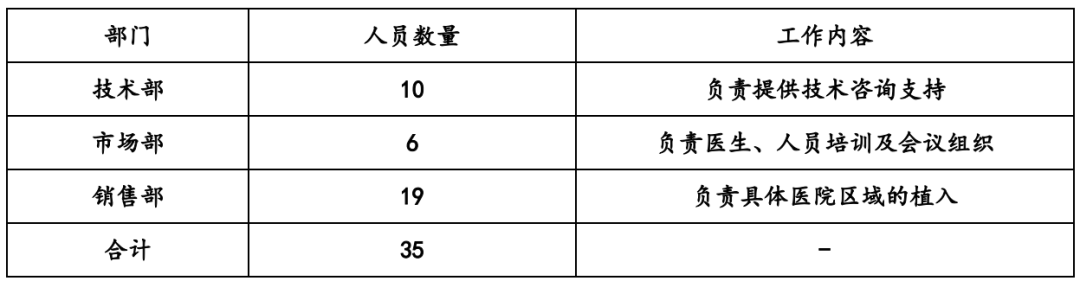

3. About the Commercialization Team

In terms of commercialization, the company has begun to establish a commercialization team, mainly composed of personnel from the Marketing Department, Technical Department, Sales Department, and other departments, as shown in the table below:

4. Regarding the Standardization of Financial Internal Control and Fund Transactions

According to the filing materials: 1) During the reporting period, the issuer had instances of paying salaries and consulting fees to its employees and external consultants through third-party companies, and there were cases of employees collecting bonuses on behalf of others; 2) Dai Yufeng, the actual controller of the issuer, and Yang Huixian had financial transactions with senior management, other individual employees, mainly involving share platform stock transactions, housing loans, and personal fund turnover.

More exciting content

Welcome to follow WeChat Video Channel

2,300 Units: Mindray Secures Major Order in the United States

Medtronic, Johnson & Johnson's Partner, Giant's New Acquisition

Over 20 Million Units: Global Ventilator Giant Issues Level-One Recall

World's First, MR-Guided Proton Therapy System

Medtronic: Plans to Close Five Production Bases

Focusing on Localization, Another Medical Device Giant Lands in China

Top 100 Medical Device Companies Restructure, Cut 5% of Workforce

JPM24: Top Ten Medical Device Events

Giant with 90 billion yuan in revenue plans to spin off its medical division for IPO

9,428 Units: Johnson & Johnson Subsidiary Issues Class I Recall

BusinessBusiness cooperation email: qxzj@landianyiliao.com